TRUMF - Diabetes Deep-Dive With DexCom And Embecta: Polar Opposite Diabetes Plays

Summary

- DexCom is young, innovative, admired, and (consequently) highly valued.

- Embecta is old, lethargic, lacks coverage, and (consequently) lowly valued.

- Growth and value investors may find respective equities interesting.

- I use DXCM and EMBC as a lens to view developments in the space.

The purpose of this article is three-fold: to give an overview of the diabetes value-chain; divergences in growth; and to identify two interesting businesses.

DexCom ( DXCM ) is an exciting diabetes-focussed med-tech company solving neglected problems in an effective oligopoly with domestic (US) and international growth aplenty. Contrast this with Embecta ( EMBC ): an attractive business treated as a cash cow and underinvested in. The likes of DexCom signals the diabetes industry is transforming. Embecta has not, and now faces disruption from several angles. Differences extend to financials and capital structure. Both are healthy businesses but appeal to different groups of investors.

1 Diabetes care primer

1.1 Diabetes care challenges

First, it is worthwhile to broadly explore diabetes and companies involved. Broadly, diabetes is:

- Chronic, and growing.

- Severe, to varying levels.

- Undiagnosed, often.

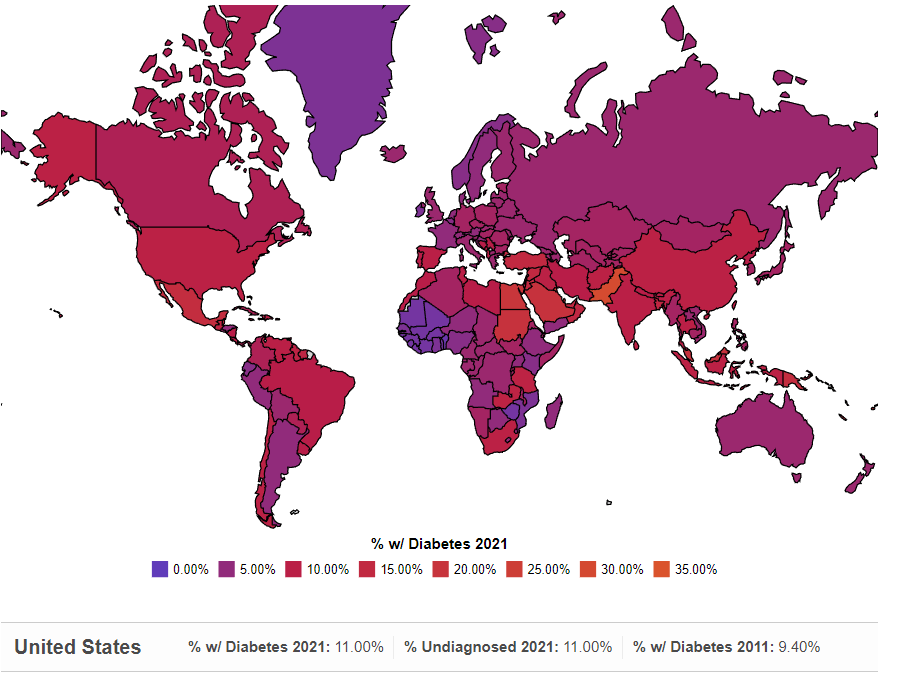

Diabetes is a chronic disease that, without effective patient outcomes, has wide-ranging adverse health consequences – including death. It is also a growing problem, fuelled by improving personal lifestyles, globally. The number of diabetic people is expected to grow by 46% by 2040. Moreover, diabetes is difficult to manage despite treatments like for diabetes (e.g., basal insulin) being available for ~100 years. Type 1 diabetics require more active management and thus are most visible to participant organizations in diabetes care. Yet, Type 1 makes up less than ~6% of all diabetics in the US – with similar patterns globally. Type 2 diabetes is typically less severe but more prevalent and costly to society. Therefore, Type 2 diabetes is where most commercial opportunities lie. For example, DexCom has marketed its continuous glucose monitor devices (CGMs) mostly to Type 1 diabetics but hopes to market to Type 2 diabetics. Similarly, novel treatments like GLP-1 agonists developed by the likes of Novo Nordisk ( NVO ) and Eli Lilly ( LLY ) are aimed at Type 2 diabetics. As stated, the prevalence of diabetes correlates to higher living standards and, therefore, more developed economies. People in regions like Northern Europe often don't have diabetes and therefore contradict ( figure below ) – suggesting other factors affect diabetes' prevalence like availability of cheap calories or genetic dispositions – but this observation, generally speaking, holds true.

{kind=link}

Diabetes per capita per country. (worldpopulationreview)

Yet, incidences will still grow worldwide because diabetes remains underdiagnosed. ‘Underdiagnosis’ may include those who are diagnosed late or undiagnosed entirely.

- Late diagnosis : Symptoms for diagnosing diabetes, like tiredness and thirst, typically present late – as late as 12 years after complications first arise. Delayed outcomes can lead to greater disfunction of the pancreas and tissue damage. Although severe diabetics must take insulin, earlier diagnosis enables treatment using GLP-1s, that promote secretion of hormones needed to naturally produce insulin. Better awareness and treatments mean diagnosis is happening earlier.

- Missed diagnosis : “ 46% of people [globally] with diabetes are undiagnosed ”. Mostly because of poor medical coverage in emerging economies, it is also because diabetes’ symptoms oftentimes start as mild. For example, diabetics are often only diagnosed when they go into Diabetic Ketoacidosis ( DKA ) – effectively, when insulin production ceases.

Novo Nordisk coins these observations as the "Rule of Halves" in old investor presentations. You can find discussion of this in a 2016 Seeking Alpha article from Marathon Investing .

Of the estimates 415 million people with diabetes, about 50% are diagnosed, of whom about 50% receive care, of whom about 50% achieve treatment targets, of whom about 6% live a life free from diabetes-related complications.

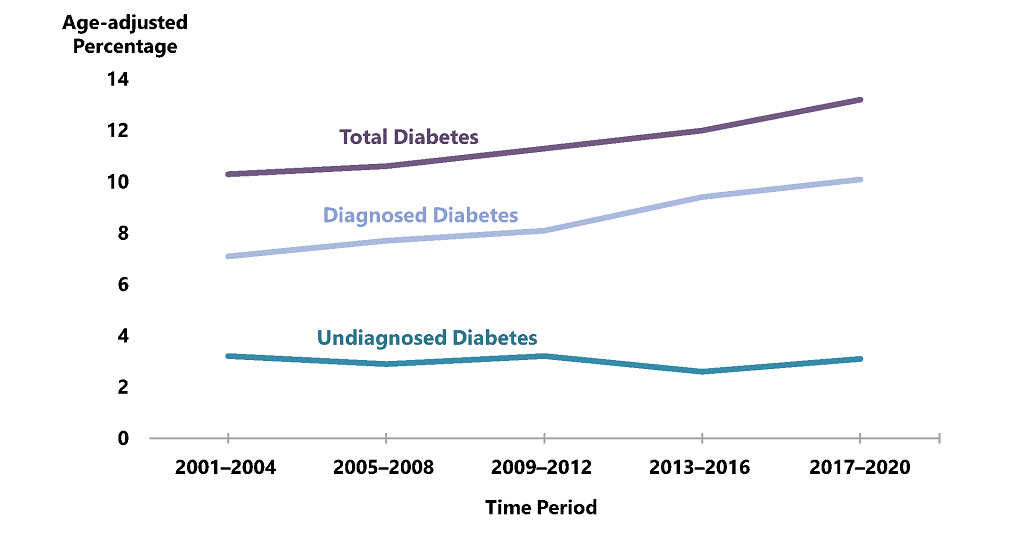

Fortunately, underdiagnosis is decreasing in the developed world ( figure below ). Unfortunately, once diagnosed, diabetes can be difficult to manage. Much healthcare spend is directed towards this, due to significant return on investment ((ROI)) present in improving patient outcomes pre-hospital.

{kind=link}

Percentage of people in the US diagnosed with diabetes. (CDC.gov)

1.2 Diabetes care innovations

Managing diabetes requires constant vigilance to avoid a hypoglycaemic or hyperglycaemic attack. Fear, inconvenience, and general discomfort of treatments, like administering insulin via needle, are common pain points. It is unsurprising that commercial organizations are trying to better diabetes care outcomes across Pharmaceuticals, Delivery, and Management.

1.2.1 Pharmaceuticals

As a medication, basal insulin (a substitute for natural insulin) remains critical for diabetics where pancreatic function fails. Dominated by Novo Nordisk, Eli Lilly, and Sanofi ( SNY ), its necessity has brought commoditization with weak pricing. The USA historically was an exception, but government-backed generics are coming as soon as 2024 . Insulin is the end destination for all diabetics. Thus, innovation largely occurs in adjacent areas where value can be added.

| Drug class |

| Description |

| Market size / growth |

| Drugs available |

| Embecta ( EMBC ) |

| Medical devices. Injectables for diabetes. |

| 1,130M |

| 32.6% |

| 1,900 |

| 1,650M |

| Novo Nordisk ( NVO ) |

| Pharmaceuticals for diabetes. Integrated injectables unit. |

| 20,200M |

| 43.1% |

| 52,696 |

| 299,960M |

| HTL-Strefa (Private) |

| Medical devices. Injectables for diabetes. |

| 87M ( 2018 ) |

| - |

| ??? |

| - |

| Terumo Corporation ( OTCPK:TRUMF ) |

| Medical devices. Injectables. |

| 5,780M |

| 14.0% |

| 28,294 |

| 21,400M |

| Ypsomed ( OTCPK:YPHDF ) |

| Medical devices. Injectables and pumps for diabetes. |

| 503M |

| 7.7% |

| 2,000 |

| 2,760M |

| Insulet ( PODD ) |

| Medical devices. Pumps for diabetes. |

| 1,100M |

| 5.1% |

| 2,300 |

| 20,340M |

| Tandem ( TNDM ) |

| Medical devices. Pumps for diabetes. |

| 703M |

| -4.0% |

| 2,000 |

| 2,890M |

| Medtronic ( MDT ) |

| Medical devices. Diversified. |

| 2,328M* |

| 22.3% |

| 95,000 |

| 116,500M |

Table 2 : Notable companies operating in diabetes delivery. *Diabetes Care unit used, for comparison. **Market capitalization as of 3. February 2023. Source: Various.

1.2.3 Management

Diabetes management has become increasingly sophisticated over the past two decades. The traditional method, single-point finger measures (pricking a finger), has limitations in terms of frequency, ease-of-use, and accuracy. In the 80s and 90s, Medtronic pioneered (again) Continuous Glucose Monitoring devices (CGMs): providing real-time insights and alerts to users. Digitization, miniaturization, and the ‘Internet of Things’ has helped CGMs become a standard of care . Adoption rates (mostly in the West) were spurred by the telehealth boom onset by COVID-19. Thus, a near doubling of the addressable market is expected by 2030. Today, the CGM market is dominated by DexCom and Abbott Laboratories ( ABT ) with the G-series and Freestyle Libre brands, respectively.

| Name |

| Description |

| Sales (USD, FY) |

| Profitability (EBIT, FY) |

| Employees (FY) |

| Market Cap ((USD))** |

| ~34.2 million |

| ~26.8 million |

| ~7.0 million |

| ~4.0 million |

| ~3.4 million |

| ~1.7 million |

Table 4 : Breakdown of diabetics' groups in the US. Source: Various.

Given its advantages, there is no reason why, over time, most insulin-using diabetics won’t use a CGM. Cost is one point of friction: the private monthly cost of G7 device is anywhere from 170 USD ( UK ), to 225 USD ( Canada ), to ~300 USD ( USA ). Thus, healthcare programmes’ willingness to reimburse patients is critical to CGM adoption. Monthly costs are given because CGM sensors are regularly replaced. Recurring costs are probably preferred by health providers because it eases budgeting. Beyond economics, evidence of safety and effectiveness will make or break probability of reimbursement. Fortunately, DexCom devices have been approved by medical agencies with clout like the Food and Drug Administration and the European Medicines Agency . A patient may not wear DexCom device, but I cannot see a scenario where CGMs are not widely available…

2.1.2 TAM

...for intensive insulin-using diabetes at least. The justification for non-insulin-using Type 2 diabetics and, further still, non-diabetics to use CGMs is less clear, due to limited evidence. CGMs at lower price points with simplified functionality, like the newly launched DexCom ONE , will reduce hesitancy but ultimately formal medical scrutiny is required. For now, anecdotal evidence like diabetics being more cognizant of how food affects their blood sugar levels when using CGMs, and better avoiding hyper(hypo)glycaemia, is supportive. Should physicians and medical bodies recommend CGMs then Table 4 suggests a larger market. This larger market may take an unknown number of years to realise, and therefore I view this big opportunity as a call option - for now. Beyond diabetes, hypoglycaemia and hyperglycaemia have additional risk factors like heart disease and loss of vision, respectively. Regardless, diabetes is where glucose monitoring is most useful.

{kind=link}

DexCom believes it can broaden its scope beyond insulin-using diabetics. For now, I remain sceptical (comments appreciated!). (DexCom presentation at the 41st Annual J.P. Morgan Healthcare Conference)

2.1.3 International expansion

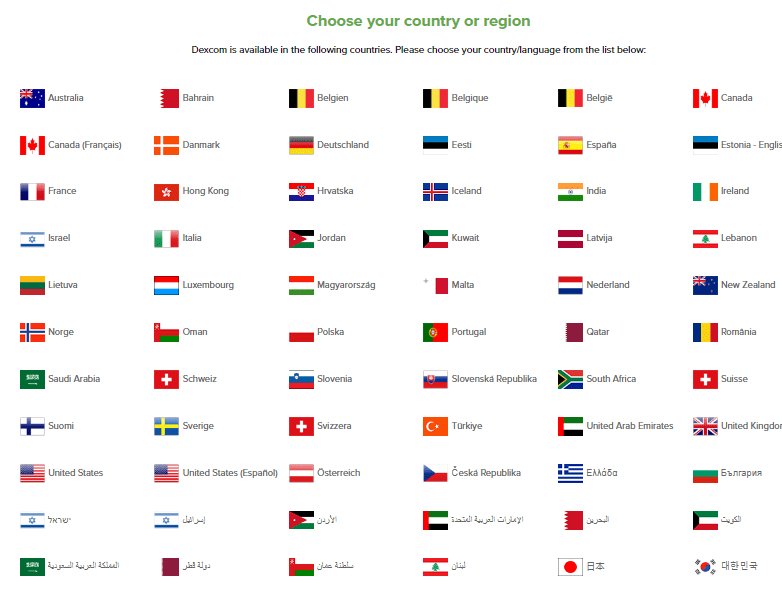

To avoid covering old ground, diabetes is a growing global problem. Simple. Touching on reimbursement, early signs are that non-US healthcare programmes will follow the US approach to reimbursement, from advanced economies like Germany to emerging economies like Lithuania. DexCom needs ubiquity to maintain its moat and therefore global scale must be part of the thesis. Scaling supply-chains and distribution will be tough, especially given competition with Abbott Labs. Presently, Abbott is ahead internationally. Its Libre products are at a lower price point – critical in emerging markets. The DexCom ONE is designed to be price competitive and for diabetics dosing insulin using injectables – a positive read-through for Embecta. I foresee global expansion as a credible opportunity with probability of logistical mishaps.

{kind=link}

Its global website makes clear how widely available DexCom devices are becoming. (DexCom)

2.1.4 Maturing business and returns profile

Maturing supply-chains are a sign of DexCom growing up. This hopefully coincides with profitability and returns or, at the very least, shareholders’ demands for it. Demands will only intensify amid a rising interest rate environment. The bull case should be DexCom margins match peers Abbott Laboratories and Medtronic. Currently, operating margins (chart below) trail ABT and MDT by ~50%. Levered free cash flow margins of DXCM, ABT, and MDT are ~3.5% , ~16.8% , and ~13.1% , respectively. The widening gap is largely a consequence of high CAPEX and interest paid by DexCom. Expanding manufacturing through a factory in Malaysia is a headline capital expense. Moreover, its unit economics are yet to mature. The bulk of a CGM’s cost is the receiver and transmitter, which are largely one-off costs. Sensors inserted into a user’s body are replaced every 10 days. This is a recurring purchase for patients and healthcare programmes, with higher margins.

2.1.5 Competition remains constant

The financial benefits of a maturing DexCom can be best reaped if costs are controlled. Competition could erode this. Current competition in its limited form is an ideal situation for DexCom. There are arguments to support benefits continuation of this and rebuff this.

Regulatory hurdles to commercialize CGMs is an immediate barrier to entry. A deciding factor is the accuracy of interpolations (predictions) made by the CGM. Therefore, the availability of quality data becomes a notable competitive advantage – something incumbents have in abundance. It’s like a network effect: the more patients, the better the product, the more widely recommended by physicians. Additionally, distribution of devices via healthcare programmes increases stickiness – as we all know public bodies rarely make sudden decisions. DexCom ONE, which likely will be sold through more D2C channels, will reduce this barriers’ significance, where DexCom’s brand becomes more crucial.

Future technologies and the Apple ( AAPL ) threat is a big unknown. Though DexCom, Abbott, and Medtronic make up as much as ~91% of CGMs available (excl. China), far more people own an Apple Watch. Apple is rumoured to roll out glucose monitoring as soon as 2024. Regulatory hurdles and proving efficacy will delay this risk, and likely keep current CGM cohorts using dedicated CGMs, yet any breakthrough would dent DexCom’s ambitions beyond diabetes.

3 Embecta, a short overview

Person using an embecta insulin pen. (Embecta)

In a position of immediate competitive risks is Embecta: the world's largest manufacturer and provider of insulin-specific needles. Formerly a division of Becton, Dickinson ( BDX ), it was spun-off in April 2022. During, it was a cash cow and underinvested in .

Needle remains the most common delivery method for administering insulin but, as patch pumps proliferate, Embecta finds itself in an identity crisis: become a pump manufacturer or bet on markets where cost and reimbursement challenges will limit uptake of insulin pumps. Management (headed by external hire Dev Kurdikar ) has chosen to do both, by:

- Lowering EBITDA margin guidance as R&D is increased to develop pumps.

- Expanding further in emerging markets as “ a [long-term] core injection market ”.

Moreover, Embecta guiding for flat growth until 2024 further tempers investors’ likely enthusiasm. Yet, diabetes remains a lucrative and attractive end market. Therefore, can we reconcile such guidance with underlying tailwinds discussed? Do syringes have underlying poor economics? How realistic is it that Embecta successfully develops a pump? Let’s investigate.

3.1 Growth of syringes compared to industry

The insulin syringes market is mature. GLP-1 treatments, like Rybelsus (Novo Nordisk) are increasingly being administered orally. Furthermore, GLP-1s help prolong diabetics’ ability to effectively produce insulin, delaying their uptake of insulin. Pumps are the clearer threat to Embecta and could limit net volume growth in the US as new insulin users are offset by patients shifting to using insulin pumps. Immediately, there are some concerns for Embecta. To quantity the lack of growth, over the course of the 2020s markets for diabetes devices (pumps, CGMs, etc.) and insulin (which complements insulin) are expected to growth at ~6% and ~3% , respectively.

Insulin injectables will grow fastest in emerging markets. International and emerging market sales are 45.4% and ~16.0% of Embecta FY22 Q4 sales, respectively. Mid-high single digit growth here is possible but, in the short-term, group growth will be offset by US sales declines. Anaemic growth forecasts are starting to make sense.

3.2 Economics of syringes compare to industry

The economics of Embecta are peculiar, with high EBITDA margins of 35.4% (DexCom EBITDA margins are 14.9% ) but seemingly weak control over their economics. To grow revenue, volume and/or pricing must grow. Volume should be reasonably forecastable – despite risks outlined. Pricing power, however, appears low. Recent Seeking Alpha commentary by Ian Bezek reaches similar conclusions. It appears price increases have minimal contribution to top-line growth - but I am unsure if it is just poorly communicated. For example, during the FY22 Q4 earnings call CFO Jake Elguicze appeared to indicate price rises only offset the loss of contract manufacturing revenue (5-10M USD). Price caps in the US may not translate into further pricing pressure, though, as the CEO indicated that consequent wider access could benefit Embecta.

3.3 Probability of pump expansion and competition

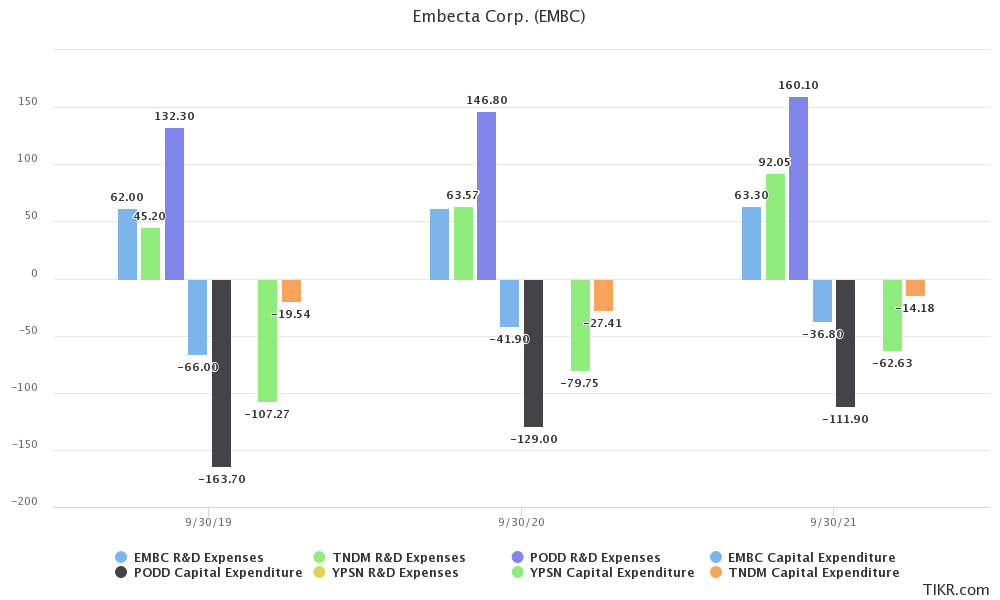

Really where the cookie crumbles though for Embecta thesis is pumps. Success or no success, CAPEX and R&D will increase - something Embecta is financially capable of - to levels potentially similar to peers (see chart).

{kind=link}

Insulet ((PODD)) markedly spends more than peers (Tandem: TNDM, Ypsomed: YPSN) on R&D (non-capitalized) and CAPEX (capitalized). This may mean rising costs for Embecta ((EMBC)). (TIKR)

The impact to FCF may be marked. Assuming R&D rises a further $50M to ~$110M and CAPEX rises to $100M for Embecta, FCF margins (based on Net Income guidance) could half, to 17.5%. Pumps are highly competitive with high intellectual and capital barriers to entry. Moreover, partnerships are crucial, be those with insulin suppliers (e.g. Sanofi) or CGM manufacturers (e.g. DexCom). Embecta has logistical and other scale advantages. By developing pumps to target insulin-using Type 2 diabetics with larger insulin reservoirs, Embecta hopes to differentiate. Yet, as competencies in developing, commercializing, and marketing insulin pumps are unproven, I view success as a tall order.

4 Valuing DexCom and Embecta

DexCom and Embecta are in polar positions and should be valued accordingly. The following table shows Mr. Market views DXCM and EMBC very differently:

| Name |

| Market Cap ((USD))* |

| Fwd PE ratio |

| Fwd PEG ratio |

| Fwd EV/EBITDA |

| DexCom ( DXCM ) |

| 41,730M |

| 121.2x |

| 4.8 |

| 56.4x |

| Embecta ( EMBC ) |

| 1,650M |

| 16.1x |

| 0.6 |

| 9.9x |

Table 5 : Direct valuation comparisons of DexCom and Embecta. *As of Friday, 3. February 2023. Source: Seeking Alpha and company guidance.

Mr. Market’s different views are justifiable, given discussions above. Nonetheless, I take a similar approach when valuing DXCM and EMBC because of the associated opportunity cost. Moreover, I keep assumptions to a minimum because it introduces complexity that does not necessarily make forecasts more accurate. Discount rates are set to 15%: constructed from a 10% desired return adjusted by a 50% stupidity factor. Feel free to constructively disagree with the approach taken.

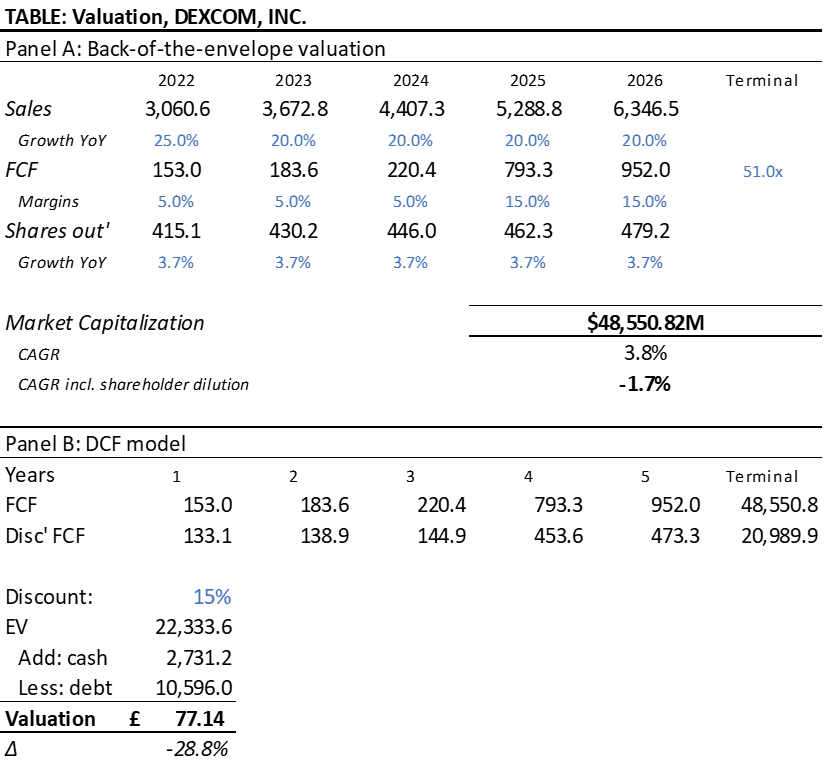

4.1 DexCom from an investment POV

To value DexCom, assumptions and points underpinning rationale are indicated below:

- Revenue growth : Consensus estimates, per TIKR, are for ~19% annualised through to 2026. This seems reasonable and not overly ambitious, in my view, given opportunities discussed.

- FCF margin : As discussed, the DexCom bull case is margins increase to levels akin to Abbott, where FCF margin has ranged from 14.1% (2017) to 20.1% (2021). I am optimistic about the business and therefore I believe 15.0% FCF margins is achievable.

- Shares outstanding : SBC is inevitable, but I factor it in by diluting shares by the 5-year average of 3.7% annually.

- Terminal multiple : I see growth for DexCom continuing throughout 2020s. Given that the Healthcare & Pharmaceutical sector and the Medical Devices industry trade at a premium, I am willing to be very optimistic, assigning a Terminal multiple of 51.0x 2026E P/FCF.

First, taking a simple back-of-the-envelope method, I struggle to reach a positive CAGR with what I believe is an optimistic view on DexCom. Second, if I were to discount this back to a present value, it would take for DexCom to reach a share price of ~77 USD – though I would probably be reasonably interested in the 80-90 USD range.

{kind=link}

DexCom valuation, as of Friday 3. February 2023. (Author)

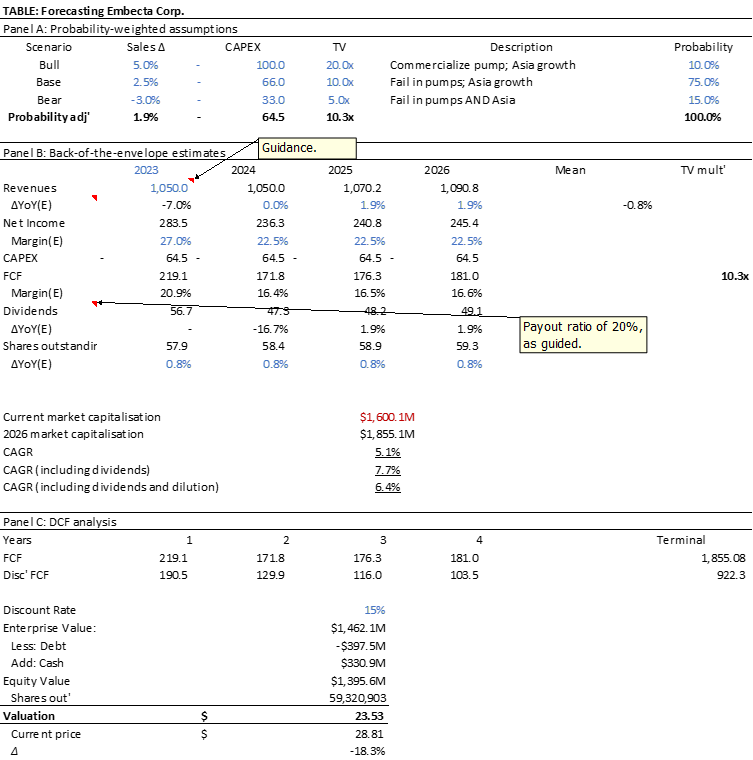

4.2 Embecta from an investment POV

Less so than DexCom, the valuation of Embecta is characterised by divergent scenarios. Where there is uncertainty, probability-weighted assumptions are used. Rationale underpinning these assumptions is indicated below:

- Revenue growth : Management has guided for flat revenue until FY2024. Beyond which, I ascribe in the base case ~2.5% YoY sales growth due to insulin broadly growing at ~3.0%.

- Net Income margin : Management has guided for 27.0% net income margin in FY2023. Pump development and salesforce expansion in Asia, I believe, will lead to rising R&D and SG&A expenses. Thus, I cut expected net income margin to 22.5%.

- CAPEX : As a base estimate, I believe Embecta CAPEX will be akin to Ypsomed. Therefore, I assign flat CAPEX spend of 66M USD across periods modelled in the base case.

- Shares outstanding : EMBC diluted shares outstanding increased by 0.8% in its first year as a public company. Developing pumps will require attracting talent that would otherwise go to competitors. Annualising this rate feels appropriate.

- Terminal multiple : If Embecta commercializes an insulin pump, the rerating alone will make EMBC a worthwhile investment, but that’s a big IF. A probability-weighted terminal value ((TV)) of 10.4x 2026E P/FCF is applied.

First, taking a simple back-of-the-envelope method I reach a middling CAGR; it would take a share price of ~22 USD to reach a 10% to 15% annualized return. Second, discounting these assumptions back to present value, a fair value is assigned around ~24 USD. Given uncertainties prompt me to be as conservative as possible.

{kind=link}

Embecta valuation, as of Friday 3. February 2023. (Author)

4 Concluding thoughts (where in diabetes is quality highest)

When considering diabetes care, it is worth reflecting on the end goal of treatments: to fully emulate pancreatic function. In medical devices, this would be an artificial pancreas. This is already possible with Closed Loop Insulin Pumps, where a pump talks to a CGM in a self-regulating manner. No matter the delivery method, basal insulin is required. Therefore, quality is arguably highest in the likes of Novo Nordisk and Eli Lilly. In medical devices, CGMs and pumps are clear improvements over traditional methods of glucose testing and insulin delivery, respectively – great news for DexCom, less so for Embecta. Continual uptake of CGMs is set to continue due to low costs vs. benefit for healthcare providers and broad utility across all diabetics. DexCom is well positioned against competitors due to its established, trusted brand; data advantages; and open connectivity. Yet, the widely known story makes it challenging to confidently generate good returns at its current valuation. Valuation is less of an issue for Embecta, on the other hand, but rather execution of strategy. Costs will prohibit insulin pumps adoption to wealthier countries and individuals, where Embecta will suffer. It needs to expand into emerging markets and develop pumps – something former parent Becton, Dickinson, and Co. has struggled to do. I remain on the side-lines of DXCM and EMBC for different reasons.

For further details see:

Diabetes Deep-Dive With DexCom And Embecta: Polar Opposite Diabetes Plays