DGEAF - Diageo: A Consumer Staple Winner For FCF

2023-04-04 02:26:42 ET

Summary

- Diageo plc is a global alcoholic beverage company.

- Diageo is benefiting from innovation, premiumization, and the general health of the alcohol industry.

- Margins are market-leading, with an EBITDA-M of 34%. They remain very rigid, unlike peers who have seen leakage.

- Debt and capital distributions are managed well, which should mean sustainable returns ahead.

- Our valuation of the business suggests a 14% upside while the business continues to outperform consumer staples businesses.

Company description

Diageo plc ( DEO / OTCPK:DGEAF ) is a global alcoholic beverage company that produces, market, and sell a range of alcoholic beverages including scotch, whisky, gin, vodka, rum, tequila, wine, brandy, and beer.

The company's portfolio includes popular brands such as Johnnie Walker, Guinness, Tanqueray, Baileys, Smirnoff, and Captain Morgan.

{kind=link}

Share price

Diageo's share price has performed well historically for a mature business, although its last decade has been slower than prior periods. The business has grown well but has shown some weakness in transitioning to the next stage of its future.

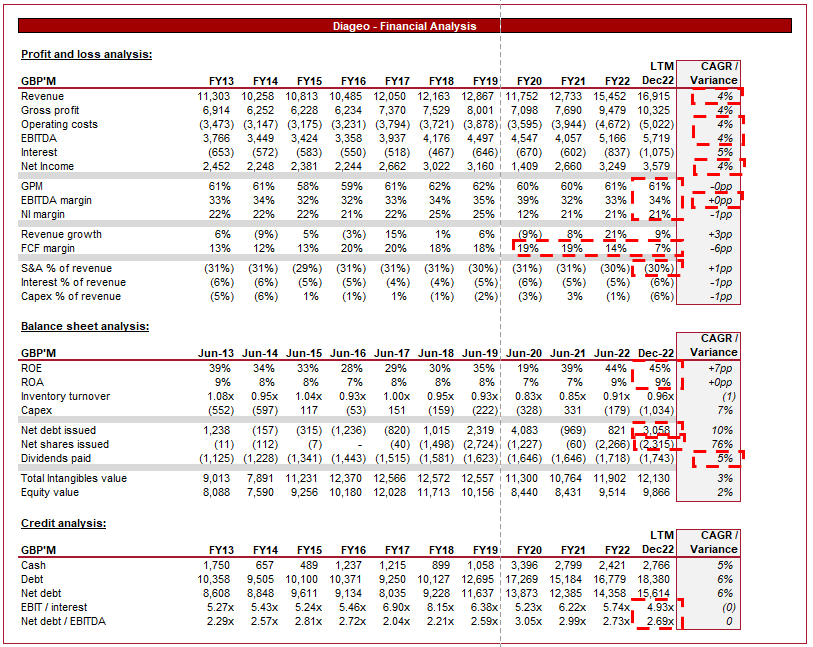

Financial analysis

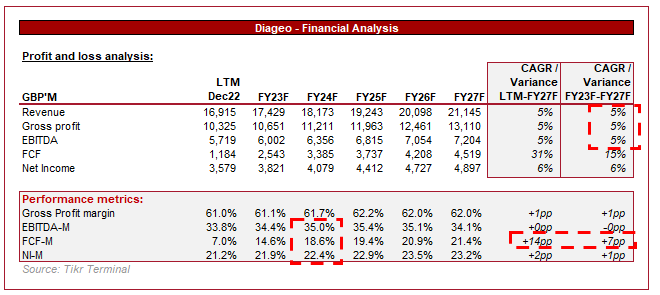

Diageo Financial performance (TIkr Terminal)

{kind=link}

Presented above is Diageo's financial performance for the last decade. The business is a financial powerhouse that has seen some chinks in its armor.

Revenue

Revenue has grown at a CAGR of 4%, although this hides the two periods of negative growth (excl. Covid-19). The business looks to have reinvigorated growth again and looks to be attractive long term, for the reasons we will state below.

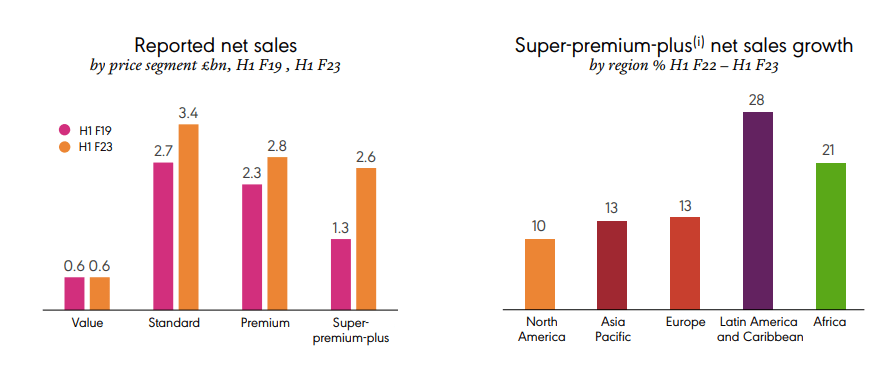

Consumers are increasingly willing to pay a premium for high-quality and premium beverages, with trends suggesting these products are actually superior in the eyes of consumers. Premiumization is driving growth in the beverage segment, with Diageo positioned perfectly to exploit this given its impressive portfolio. Reported sales from these segments have grown the fastest and are a trend seen across all geographies.

Reported sales by segment (Diageo)

{kind=link}

We believe the reason is that it is an industry where expertise makes a difference, by which we mean taste. Unlike most other industries, new entrants do not come in and compete on price but instead stay premium and attempt to compete on product. This is something we see in the fashion industry as well, another sector that has seen a "premiumization" trend. We continue to refer to this as a trend but it is a several-year shift in the industry that does not look to be slowing.

Organic sales (Diageo)

The COVID-19 pandemic sped up a shift in drinking occasions, with more consumers drinking at home or for specific social occasions, rather than simply at bars or restaurants. Diageo has done well to foster this cultural niche, teaching individuals how to make cocktails and marketing this as an enjoyable option for gatherings. This has led to healthy demand across spirits and in our view, more "sustainable" demand for it, as it's less dependent on what is considered the hot brand.

Product demand (Diageo)

In recent years, we have seen greater competition from new entrants, who have used a more down-to-earth marketing approach to sell a tailor-made experience to consumers. This has been done by innovating with flavor, as well as creating a buzz online. Diageo has a strong focus on innovation but is proactive in the M&A market as a means of supplementing its current suite of brands.

Acquisitions and Disposals (Diageo)

Health-conscious consumers are driving demand for low and no-alcohol products, as they seek to reduce their alcohol consumption without sacrificing social experiences and the enjoyment of consumption. The industry has reacted rapidly to this, historically hamstrung by the inability to close the taste gap. This, however, is changing. An interesting component the beverage industry did not expect is the interest from non-alcoholic individuals, who are increasingly looking to try these products as a means of joining the social occasion. Diageo has launched an alcohol-free version of its current products, such as Gordon's and Smirnoff, as well as acquiring brands who specialize in these products such as Seedlip .

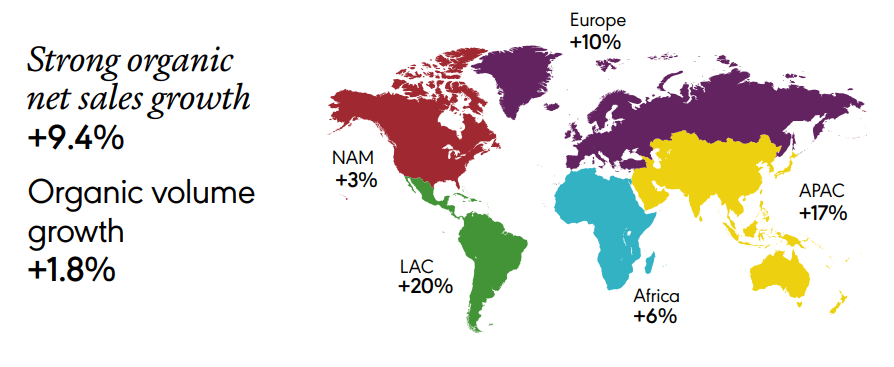

We are also big fans of Diageo's geographical split. The company operates in all the key geographies, giving it greater diversification against potential regional shocks such as legislation, as well as allowing the business to build truly global brands. Importantly, Diageo is seeing growth across the board, suggesting its brands are relatively competitive.

{kind=link}

As we mentioned, health-conscious individuals demand non-alcoholic products but many are being driven away from alcohol in general. There are concerns about health and wellness, and the general caloric intake that comes with regular alcohol consumption. This trend is expected to impact the sales of traditional high-alcohol beverages, such as spirits, with a portion likely lost. We are not overly concerned due to the ability to sell substitutes acting as a "soft landing".

Economic conditions could pose short-term headwinds for the business. As inflation remains high, consumers are increasingly seeing their discretionary incomes decline, as a greater portion of income is allocated to living costs. Due to this, less money will be spent on social gatherings, as consumers act more defensive in the short term. This is especially the case with alcohol given how expensive it can be. The good news is that many drinkers are unlikely to completely forego consumption and so we will not see anything dramatic occur, but it could be a slow year.

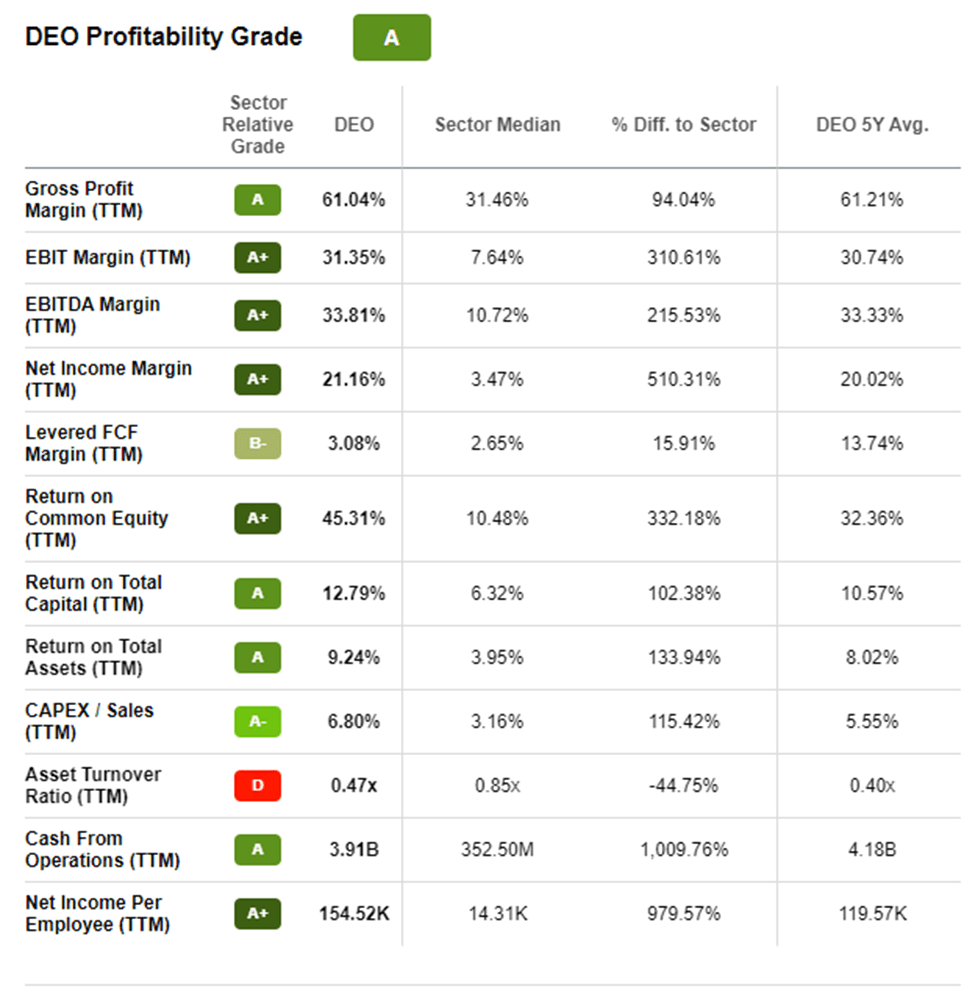

Margins

Diageo has experienced extremely rigid margins, with essentially no movement from this time 10 years ago. The company had made gains in FY18/FY19 but this does not look sustainable. Despite the rigidity, Diageo has experienced some margin compression from inflationary pressures, which could continue into FY23, but so far this has been successfully offset.

OPM bridge (Diageo)

This is pretty fantastic cost control from Diageo in our view as our research into the beverage industry has shown many others are struggling. Fevertree ( OTCPK:FQVTF ) experienced a c.44% increase in glass costs, as well as other inflationary issues causing EBITDA-M to decline to 11% from 29% in FY19. Anheuser-Busch Inbev ( BUD ) has also struggled with inflationary pressures, experiencing a decline from 39% (FY19) to 32% (FY22). This makes Diageo highly attractive on a relative basis.

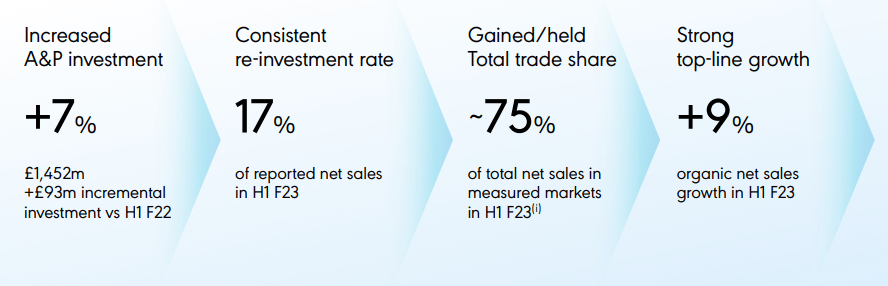

Management's marketing expenditure remains strong, allowing the business to gain or maintain market share across 75% of its total net sales.

{kind=link}

The net impact of these factors is an EBITDA margin of 34% and a FCF conversion of 7%, which looks to be below the historical normalized level of c.18/19% due to inventory accumulation. Our view is that this is highly attractive, as it should allow the business to fund strong distributions to shareholders.

Balance sheet

Diageo's improving profitability through growth is reflected in its ROE, which has gradually improved as Management has either allocated cash wise to acquisitions or distributed through buybacks.

Management has been proactive with its debt allocation, gradually raising capital across the historical period. This has been done alongside the growth of the business, carefully keeping ND/EBITDA in the 2-3x range. Our view is that 3x is a healthy maximum and so concurs with Management's goal here. Debt has been cheap to raise so why not maximize this?

Dividend payments have been sustainably growing at a rate of 5%, while buybacks were initiated from FY18 onward. If we use LTM and FY22 as a benchmark, the company generates around £2.6BN before cash financing expenses. Assuming a small amount of incremental debt issued, we will likely see cuts to buybacks as c.£1.8BN allocated to dividends.

Outlook

Diageo outlook (TIkr Terminal)

{kind=link}

Presented above is Wall Street's consensus view on Diageo's coming 5 years.

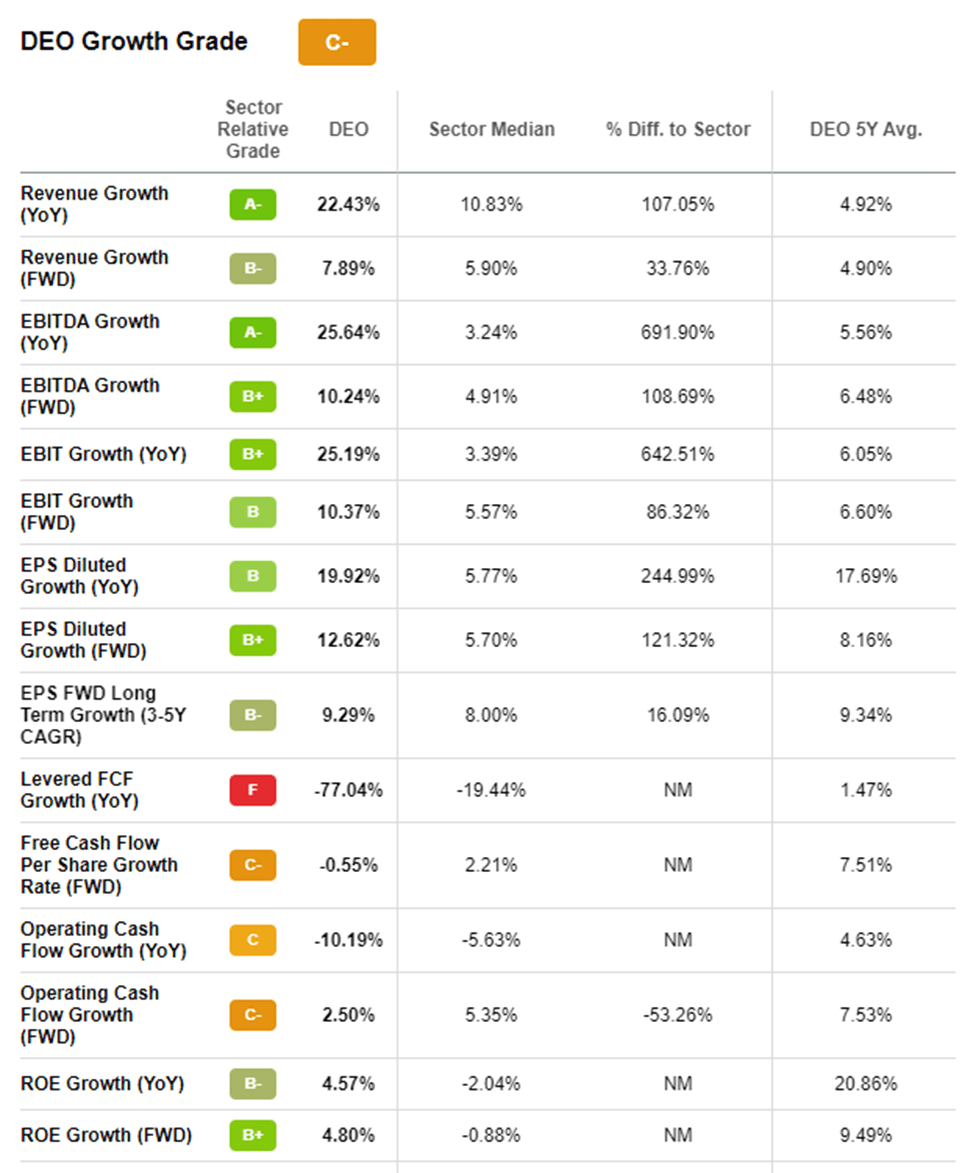

Analysts are forecasting continued strong revenue growth at a slightly higher rate of 5%. This will be driven in large part by the premiumization of its products, allowing high prices to be commanded.

Slight margin improvement is expected but not to a substantial degree. This seems reasonable as the business is highly mature and there is little identifiable value on the table.

It should be noted that Management is more bullish than analysts, with their medium-term guidance at 6-9%. This suggests some upside on execution alone.

Management guidance (Diageo)

Peer comparison

{kind=link}

Presented above is a comparison of Diageo to a cohort of consumer staples businesses, which are overarching the main competitors to capital for the business.

Diageo performs extremely well, significantly outscoring across most metrics. What is key is the c.23% EBITDA positive delta and the c.18% NI delta. This should allow Diageo to fund superior returns over time through distributions.

{kind=link}

Not only does Diageo outperform on a profitability basis but on growth too. The company has and is forecast to grow key metrics at a greater rate, driven by industry tailwinds.

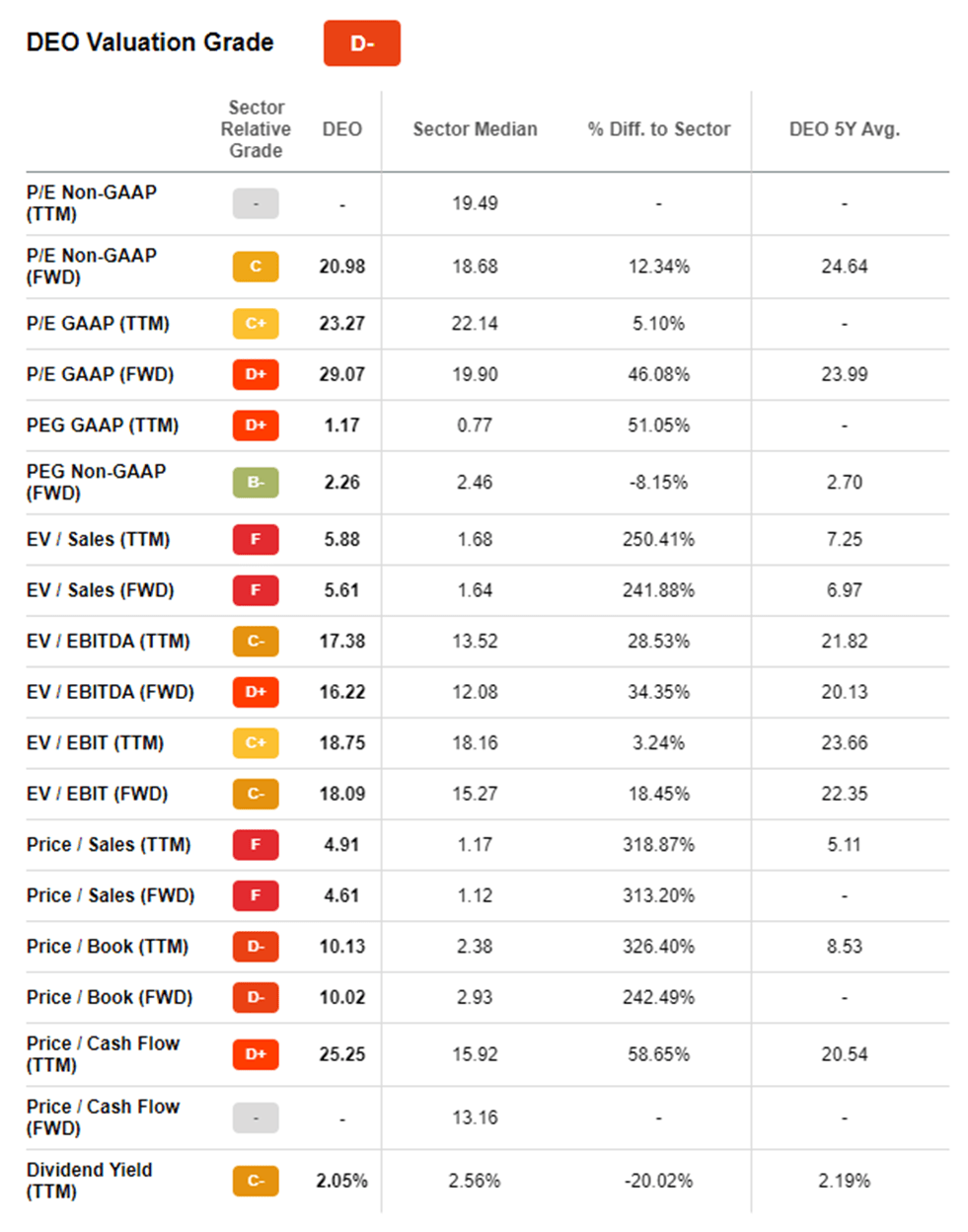

Valuation

{kind=link}

With superior profitability and growth, it is unsurprising to see Diageo trading at a premium to this peer group. With a NTM EBITDA multiple of 16x, and a NTM earnings ratio of 29x, the business looks attractive in our view given it is below its 5Y average.

We have conducted a DCF valuation to quantify the upside, with our key assumptions being:

- Revenue growth of 5-6%, remaining conservative against Management's view

- FCF conversion improving to 18-20%.

- An exit multiple of 16x, a perpetual growth rate of 3%, and a discount rate of 7%.

Based on this, we derive an upside of 14%.

Final thoughts

Diageo is a commercially attractive business. The industry is experiencing a shift toward premium brands, an area in which Diageo specializes. Further, the company continues to innovate both alcohol and non-alcohol-based beverages, gaining on genuine consumer interest. We like the profitability and see no real downside risk. The stock is a great defensive choice for sustainable distributions and a bet on consumers. Relative to peers the margins hold up and our valuation suggests so capital appreciation is on the table.

For further details see:

Diageo: A Consumer Staple Winner For FCF