DEO - Diageo: A Leader In The Premium Alcoholic Beverage Market

Summary

- Alcohol is one of the fastest growing segments in the consumer staples category.

- Diageo is positioned to ride the wave of premiumization, the "spirits takeover," and the rise of new markets.

- As a British company, Diageo enjoys less institutional coverage.

- At a P/E multiple of 20 and FCF yield of 3.75%, Diageo is trading at a discount compared to its peers.

- If you're already paying for its drinks, why shouldn't you get your fair share of Diageo's profits?

Editor's note: Seeking Alpha is proud to welcome Yuval Rotem as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Diageo (DEO) is a strong buy because of its leadership in the fast-growing alcohol industry. The company is currently undervalued based on its historical multiples and its peers. In my opinion, the lower growth in North America is overexaggerated and creates an appealing entry point.

Company Introduction

Diageo operates in the alcoholic beverage industry. It sells scotch, whiskey, gin, vodka, rum, tequila, liqueur, wine, beer, and more. The company's brand portfolio is nothing short of spectacular, with names like Johnnie Walker, Guinness, Tanqueray, Baileys, Smirnoff, Captain Morgan, Crown Royal, Don Julio, Ciroc, Casamigos, Ketel One, and many more.

{kind=link}

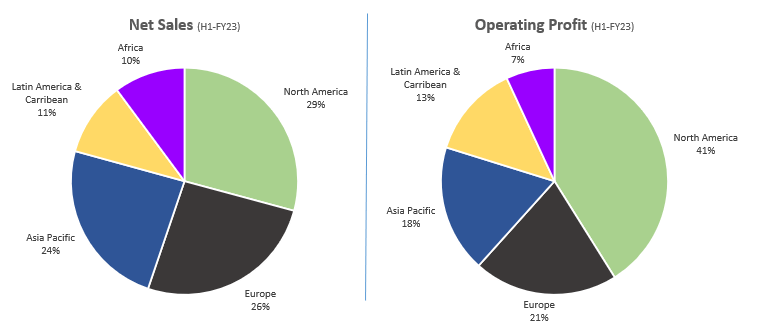

Diageo's operations span worldwide, with operations in North America, Europe, Asia Pacific, Africa, Latin America, and the Caribbean. The exposure to each of those geographies is as follows:

Created by author using data from Diageo's financial reports

{kind=link}

Diageo is uniquely positioned in both the on-trade market (out of home) and the off-trade market (at home) thanks to its premium diversified portfolio. I believe many investors who are occasional at-home drinkers have at least one bottle made by Diageo in their house, and those who go out will definitely enjoy a drink based on a Diageo-owned brand.

Alcoholic Beverages Market and Growth Prospects for the Company

The alcoholic beverages market in 2022 is estimated by Statista at $1.6T, with expected growth of 5.42% between 2023 and 2027. Diageo is guiding to 6% sales growth and 7.5% operating profit growth in the midterm, reflecting a gain in market share and the shift-to-spirits dynamic. As of today, beer is the largest segment in the market (~$600M). However, it's constantly losing share to other segments, mainly hard seltzers, wines, and spirits. Between those, the premium categories are leading the growth. According to Ivan Menezes, Diageo's CEO, more than 30% of Americans spent more than $50 on a bottle of alcohol in 2022, an increase of eight points compared to 2021.

Valuation

| Company |

| P/E TTM |

| EV/EBITDA TTM |

| EPS Growth (5-Year) |

| Sales Growth (5-Year) |

| Diageo |

| 22.51 |

| 16.94 |

| 4.13% |

| 6.83% |

| Brown Forman |

| 35.08 |

| 23.84 |

| 3.71% |

| 5.65% |

| Campari |

| 37.30 |

| 22.77 |

| 10.62% |

| 6.19% |

Note: Data as of Feb. 10, 2023.

Even though it's the largest company in terms of total sales, Diageo's sales growth is the highest among its peers. As will be discussed below, I do not believe the reason investors got scared out of the stock after its latest earning release is material. I cannot find a reasonable justification for the company's significantly lower multiple compared to its peers.

Diageo is selling for a P/E of 20.2 on 2023 earnings, excluding share buybacks. During the past 10 years, its average P/E was 23.8, which reflects 18% upside in the near term. Assuming 7.5% EPS growth in the midterm (respective to management's guidance) and a 2025 exit P/E multiple of 20, one should expect a CAGR of 14% in the upcoming three years.

Addressing the Recent Drop - Growth Deceleration in North America

Diageo's Investor Presentation

{kind=link}

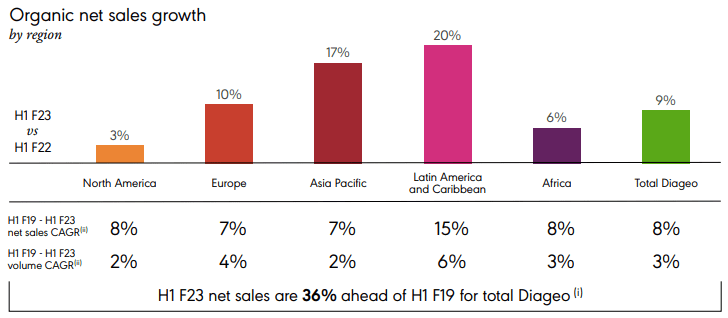

As shown in the previous section, North America is a large chunk of the company's operating profit and sales. Investors worry about the 3% growth in one of the company's main markets.

However, I would point out that Diageo is somewhat in the middle in terms of exposure to North America compared to its relevant peers. For example, Brown-Forman (BF.A)(BF.B) sees ~50% of its sales from North America and doesn't disclose its operating profit from each geography. Campari (DVDCF)(DVCMY) is on the lower end of that, seeing ~27.5% of its sales in the U.S. region.

In the last six months of 2022, Brown-Forman saw organic growth of 11% in the U.S., compared to Diageo's "miserable" 3%. One should wonder what happened to the main source of profits for Diageo. According to management, there are two main reasons for lagging. The first reason is large market share and price increases:

As expected, growth in the U.S. spirits category is normalizing, trending toward a historical mid-single-digit range. ... [In] market share, we are at a global level where 75% of the world is in green. That's a high benchmark. In the U.S. context, we're holding share ... [as] we're coming off a period where we've grown significant share. And we've also taken price ahead of the industry, if you look at the last 3 years. And so flat share in the first half, but fully expect and want to ... get back into the share growth mode in the U.S. And I expect in the medium term, we will do that.

The second reason is timing:

In the first half of fiscal 22, the recovery in the on-trade channel, resilient consumer demand in the off-trade channel and the partial easing of supply chain constraints on certain products, resulted in the replenishment of stock levels by distributors and retailers towards normalized levels on several brands. The impact of lapping this replenishment resulted in depletions being significantly ahead of shipments across some brands in the first half of fiscal 23.

Allow me to add another reason - Diageo is a much larger company compared to Brown-Forman. For the second half of 2022, Diageo's sales (GBP3,847M) in the U.S. were more than 4.5x Brown-Forman's ($1,016M). In addition to that, Diageo saw significant growth between 2019 and 2022, growing 8% organically compared to Brown-Forman's 8.6%.

It should also be noted Diageo's highest growing region, Latin America and the Caribbean, also became its best-performing region in terms of margins. To conclude this point, I do not believe the slower growth in the first half of FY2023 is scary at all, and it does not justify a discount on Diageo's earnings. Diageo is growing across all regions and the company has demonstrated its ability to produce high margins in regions outside North America.

Risks

The first risk is regulation. The alcohol industry is a highly regulated one. Diageo and its peers are already mandated to pay excise taxes at around 33% of gross revenues. An increase in the excise taxes or a change in the regulatory structure doesn't seem like a significant risk, but one that should be taken into account.

Regarding competition, in the past few years many influencers entered the alcohol market - for example, there's Kendall Jenner and her 818 brand. In addition, Diageo competes with boutique distilleries and local beer makers. Increasing competition is always a risk, but Diageo showed resilience and was able to hold or gain share in 75% of markets after years of significant share gains.

Looking at valuation, multiple contraction is certainly a risk in an industry that is sometimes associated with negative public opinions. I do not believe the alcohol industry faces a future similar to tobacco, but this is a possible scenario.

Regarding leverage - which is a risk for every company, especially in times of rising interest rates - Diageo's management is very aware of its balance sheet and consistently talks about capital allocation priorities and leverage goals (2.5-3 debt to EBITDA). Currently, the company sits at 2.8x debt to EBITDA and does not face any material leverage risk.

Conclusion

At a time when brand value is one of the strongest moats a company could aim for, Diageo owns more than 20 worldwide famous brands. The company is able to grow faster than competitors even though it's much larger. Diageo enjoys an impenetrable distribution chain, very capable management, and a strong balance sheet. I see no reason whatsoever for the company to trade 18% below its historical P/E multiple, and believe investors will enjoy 14% CAGR for the next three years.

For further details see:

Diageo: A Leader In The Premium Alcoholic Beverage Market