DEO - Diageo: Celebrities Are Changing The Industry (Post-Earnings Rating Downgrade)

2023-08-11 12:28:50 ET

Summary

- Diageo is a leader in the alcoholic beverage market, there is no doubt about that.

- The company had a decent FY23 despite headwinds from higher inventory levels, a tougher consumer environment, lower in-home consumption, and the sudden death of its legendary CEO, Ivan Menezes.

- However, Diageo's performance during the year raises questions about the company's moat, growth potential, and profitability capabilities.

- The competitive landscape in the alcohol industry is intensifying. As evident by the flux of celebrity-owned brands, the entry barriers are no longer high, and Diageo is showing signs of weakness with market share losses and declining margins.

- I don't expect Diageo will provide investors with market-beating returns, and therefore, I downgrade the stock to a Hold.

Diageo ( DEO ) is a leader in the alcoholic beverage market, there is no doubt about that. Fiscal 2023 was a decent year for the company, as it was able to grow sales by 10.8% while overcoming several headwinds, including increased inventory levels, a tougher consumer environment, lower in-home consumption, and the sudden death of its legendary CEO, Ivan Menezes, may he rest in peace.

That being said, Diageo's performance during the year raises questions about the company's moat, its growth potential, and profitability capabilities, as a public feud with rapper Sean "Diddy" Combs, combined with a flux of celebrity-owned brands, unsuccessful marketing campaigns, and a significant margin contraction, caused the stock to underperform.

I expect Diageo will continue to lead its category, but I find its competitive moat significantly weaker, primarily due to a major decrease in barriers to entering the industry. Thus, I downgrade Diageo to a Hold.

Background

In February of this year, I wrote my first article about Diageo, which happened to be my first article on Seeking Alpha. I claimed the company is ' A Leader In The Premium Alcoholic Beverage Market ', and while I believe my writing has materially improved since, I encourage you to read my overview of the company's brands and strategy.

In short, Diageo focuses on the premium and super-premium alcoholic beverage market, with its portfolio of above-average priced brands, comprised of worldly renowned names like Johnny Walker, Tanqueray, Baileys, Captain Morgan, Don Julio, and many more.

Diageo's focus on those specific segments of the market is strategically logical, as these segments are the fastest growing within the alcohol industry, which is seeing beer continuously lose share to spirits.

In my previous article, I rated Diageo a Strong Buy, as I viewed its discount compared to underperforming peers as unjustified. The stock has essentially stagnated since, which means it underperformed the market by 7%.

Let's see what changed my thesis, and why I decided to downgrade it to a Hold.

Celebrities Are Changing The Alcohol Industry

Peyton Manning, Ryan Reynolds, Dwayne Johnson, Michael Jordan, Matthey McConaughey, LeBron James, Bruno Mars, Steph Curry, Kendal Jenner, Mark Wahlberg, Jay-Z, Snoop Dogg.

This is not a list of random celebrities, it's only a very partial list of celebrities who own an alcohol brand.

The problem here, in my opinion, is two-fold. First, those celebrity brands are obviously taking some share from Diageo. Second, they force the company to participate in the M&A market, buy brands for elevated prices, and increase its marketing spend.

Diageo Is Losing Market Share

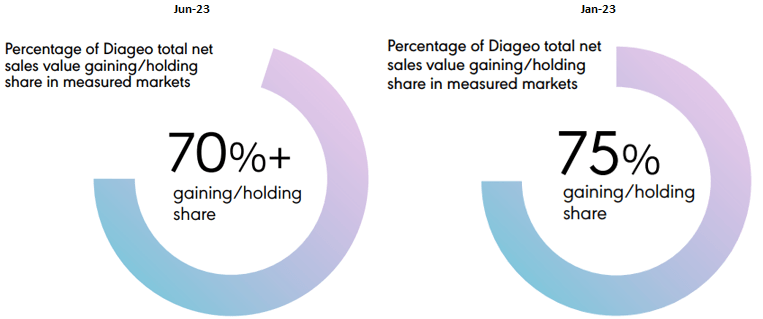

In January 2023, Diageo reported that 75% of its NSV (net sales value) gained or held share in measured markets. A few months later, we're seeing that only 70% of its NSV is gaining or holding market share. With the help of some simple math, we can understand that 30% of its NSV is losing market share, not a small number at all.

{kind=link}

Diageo FY23 Results Presentation

FY23 is also the first in the last three years in which the company lost market share in the US. While it's not only celebrities that are taking share from Diageo, the trend is alarming, and I think it's reasonable to assume celebrities have a big part to do with it.

Diageo FY23 Results Presentation

Furthermore, the company's recent feud with Puff Daddy can't be sitting well with his fans and acquaintances. Even if it sounds ridiculous and the rapper has no case, I think it will definitely damage the company's brand image, even a little bit. It could also affect the company's ability to do business with celebrities in the future, which leads me to my second point.

Profitability Is Deteriorating

In 2017, Diageo purchased George Clooney's Casamigos tequila for $1 billion. In 2020, the company purchased Ryan Reynolds' Aviation gin for $610 million. I don't doubt Diageo's ability to purchase brands at a price that's accretive for shareholders, but it's clearly more expensive to rely on such acquisitions which include a premium for the celebrity's name.

Created by the author using data from Diageo's financial reports.

In addition to the money spent on large acquisitions, the competitive landscape is intensifying. In an attempt to maintain market share, we can clearly see the company is increasing its marketing spend. As a percentage of sales, marketing expenses have been increasing consecutively since 2016, reaching an all-time high in 2023, and I don't see this trend changing direction any time soon.

Furthermore, the return on ad spend (ROAS) is deteriorating, with unsuccessful campaigns like Crown Royal, a brand that the company spent a lot of money on, including a Super Bowl commercial, and was one of the worst performers in terms of volume in 2023, declining by 12%.

{kind=link}

Created by the author using data from Diageo's financial reports.

As we can see, margins are still significantly below 2018-2019 levels. A decent chunk of the decline could be explained by higher commodity prices and Covid-19 effects, but there are apparent headwinds from increased marketing spend, as well as royalty arrangements with celebrities in some brands.

Bottom Line

I believe that slow-growers like Diageo must have a significant competitive moat for them to become market-beating investments over time. Diageo significantly underperformed the S&P 500 in the last decade, and I see no reason why this will change over the next decade, in light of its weakening competitive moat.

Fiscal 2023 Financial Review

Now that we're done explaining what changed my investment thesis, let's briefly go over the company's results in FY23 before we discuss valuation. Diageo reported sales of GBP 17.1 billion, reflecting growth of 10.8% for the full year. The majority of growth came from the first half, which enjoyed easy comparisons. In the second half, Diageo's revenue grew by a mere 2.6%.

{kind=link}

Diageo FY23 Results Presentation

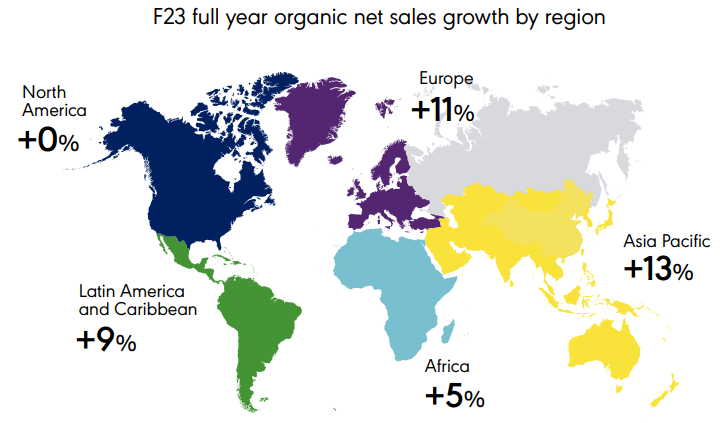

Looking at geographies, North America remained flat throughout the year, whereas Asia Pacific and Europe increased by double-digits. Unfortunately, Europe and Asia Pacific are the weaker geographies in terms of profitability, with only Africa below them.

Diageo FY23 Results Presentation

Regarding price tiers, we can see that standard outgrew premium and super premium, reflective of the tougher economic environment which is leading consumers into trading down.

{kind=link}

Diageo FY23 Results Presentation

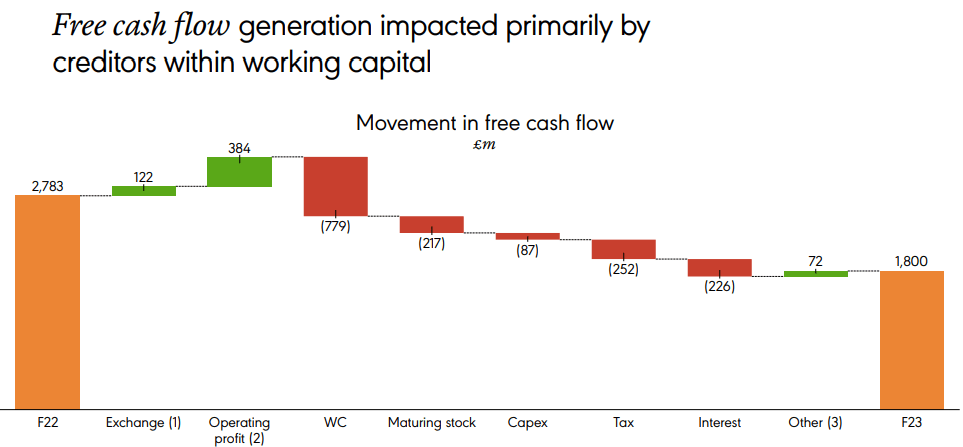

The worst line item for the year was free cash flows, which totaled GBP 1.8 billion, an 8-year low. Free cash flow margins were 10.1% and were affected by higher interest rates and a significant increase in working capital caused by higher inventory and lower trade payables.

Overall, it wasn't the best year for Diageo to say the least, and the second half was much worse than the first.

Valuation

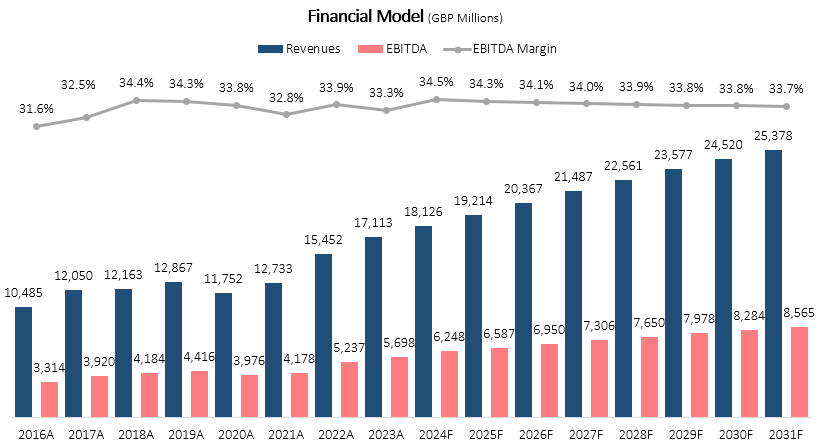

I used a discounted cash flow methodology to evaluate Diageo's fair value. I expect the company will grow revenues at a CAGR of 4.9% between FY23-FY31, in line with the alcoholic beverages market.

I project EBITDA margins will decrease gradually to 33.7% in FY31, as operating margins will remain below historical levels due to increased competitive pressures, and the gap between depreciation & amortization and capex closes.

{kind=link}

Created and calculated by the author based on Diageo financial reports and the author's projections

Taking a WACC of 8.1%, and adding Diageo's net debt position, I estimate the company's fair value at GBP 74.1 billion or GBP 32.92 per share. Translating to dollars, I estimate the fair value of the NYSE-listed Diageo stock at $168, reflecting 3% downside to the current market price.

Conclusion

The competitive landscape in the alcohol industry is intensifying. As evident by the flux of celebrity-owned brands, the entry barriers are no longer high, and Diageo is showing signs of weakness with market share losses and declining profitability.

The company's second-half results were underwhelming, reflecting a significant growth slowdown, as well as worsening cash cycles and return on marketing investments.

I don't expect Diageo will provide investors with market-beating returns, and therefore, I downgrade the stock to a Hold.

For further details see:

Diageo: Celebrities Are Changing The Industry (Post-Earnings Rating Downgrade)