DGEAF - Diageo: Cyclical Headwinds Provide A Nice Entry Point

2024-01-18 10:15:07 ET

Summary

- Diageo has significantly underperformed the global staples basket recently, with cyclical headwinds hitting earnings and the stock modestly de-rating in terms of its P/E multiple.

- Weakness in Latin America & Caribbean has led to downgraded 1H FY2024 guidance, but headwinds there look largely macro-related after a prior good run in the region.

- The stock trades modestly below its long-run average valuation based on subdued FY2024 EPS estimates, with growth at the low end of company targets enough to deliver solid returns from here.

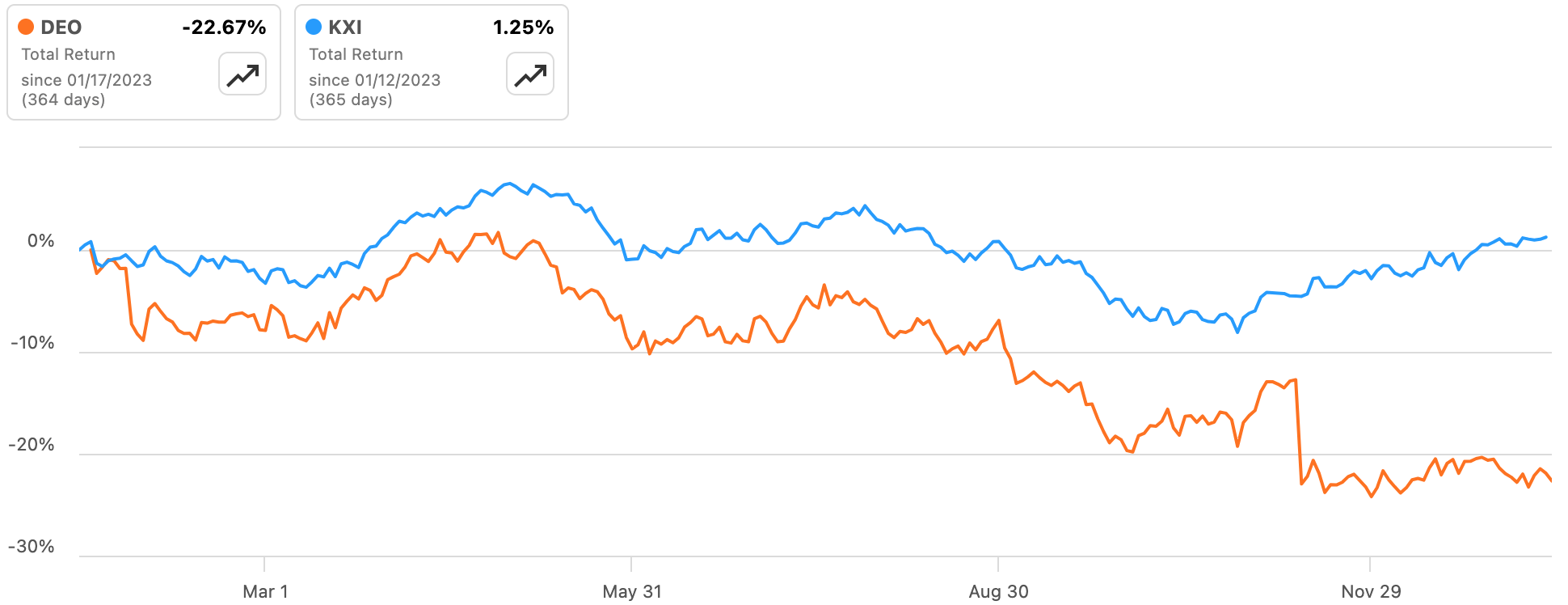

Shares of alcoholic beverage giant Diageo ( DEO ) have been on a poor run recently, with the ADSs underperforming global staples ( KXI ) by almost 25ppt over the past twelve months on the back of a circa negative 23% total return in that time.

{kind=link}

Stockholders here have been hit hard by a one-two combination of declining earnings and valuation multiple de-rating, with the company battling some cyclical headwinds whilst the stock's P/E has contracted modestly at the same time. Although frustrating for current investors, recent softness in the business looks largely transient in nature, and with the stock now below its long-run average P/E based on declining forward EPS, now looks like a good time to begin accumulating these shares.

Cyclical Headwinds Don't Tarnish A Great Business

Leaving recent headwinds to one side for a moment, Diageo possesses one of the stronger long-term investment cases among mega-cap staples stocks. I say that for three broad reasons:

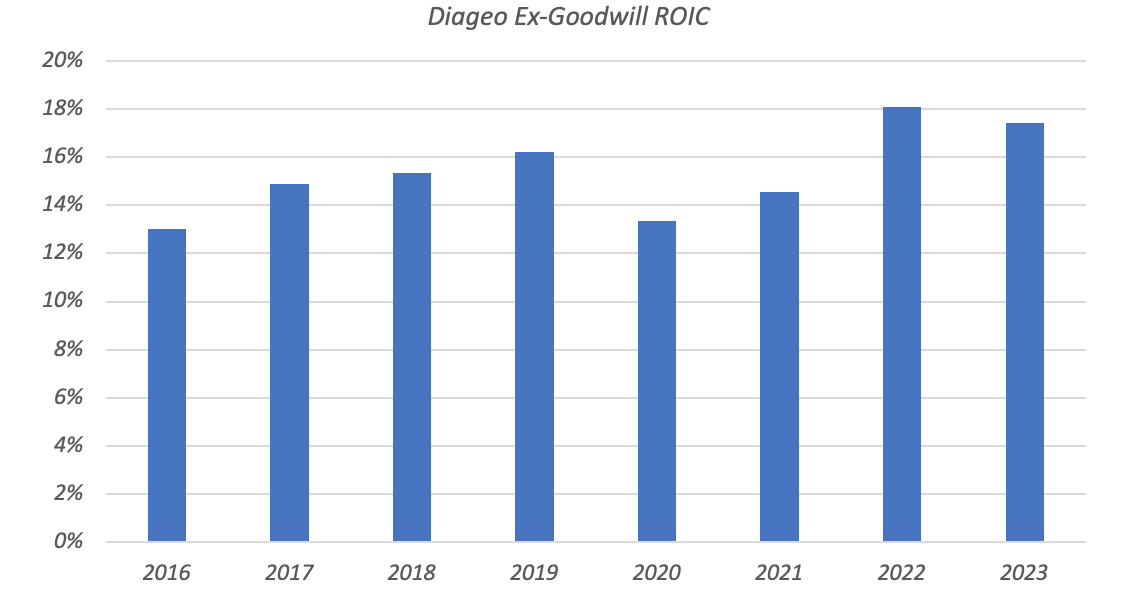

Strong Underlying Profitability . Diageo averaged a mid-teens ex-goodwill return on invested capital between 2016 and 2023 (as per the company's definition used in annual reports, excluding goodwill). This allows for a relatively high payout ratio (on dividends, buybacks, M&A etc.), with relatively less need to retain earnings to fund organic growth.

Data Source: Diageo Annual Reports, Author Calculations

{kind=link}

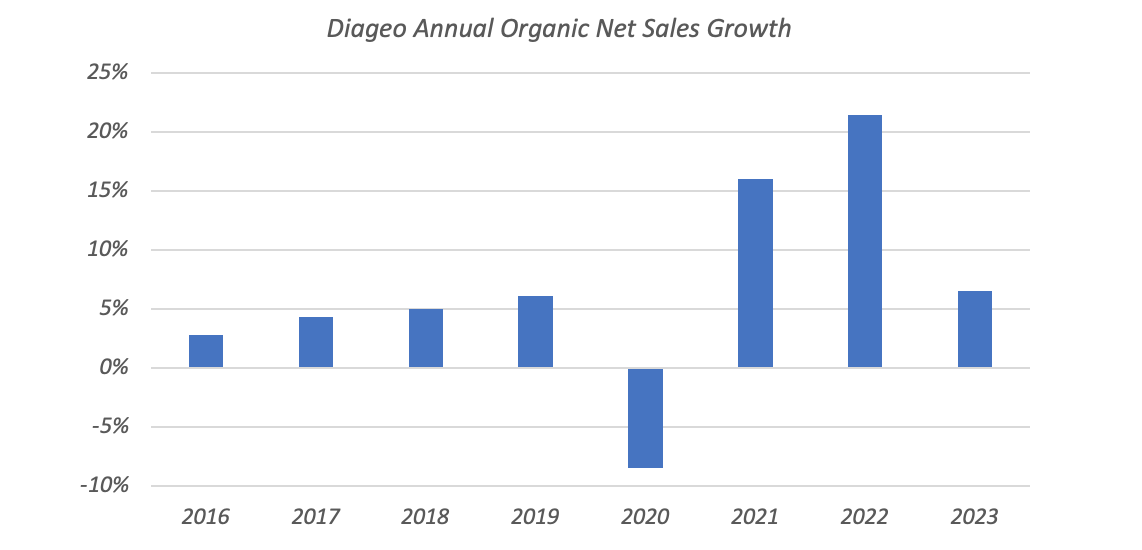

Good Organic Growth Potential . The benefit of high ROIC depends largely on possessing reasonable growth potential. The global alcohol market has a circa 4% CAGR growth outlook, but this masks the skew in terms of both category (e.g. spirits versus beer) and price tier, with 'premium and above' tiers typically growing faster than the market. Similarly, developed market growth is aided by secular shifts from beer to spirits, while emerging markets see a tailwind from rising incomes. Diageo targets a 5-7% CAGR in organic net sales growth, achieving an average closer to the high-end of that range in recent years (albeit with high volatility due to COVID).

Data Source: Diageo Annual Reports

{kind=link}

Broad Product Portfolio . Individual spirits categories can be highly cyclical depending on consumer preferences at any given moment. Diageo has a broad product portfolio, with leading brands and market shares in scotch (e.g. Johnnie Walker) , gin (e.g. Gordon's ), vodka (e.g. Smirnoff ), rum (e.g. Captain Morgan ) and tequila (e.g. Don Julio ). By net sales, scotch (~25%), beer (~15%), tequila (~12%), vodka (~9%), rum (~5%) and gin (~5%) point to a balanced portfolio, allowing the firm to capture some upside during individual category cycles while also limiting the impact of category downturns.

Headwinds Appear Largely Cyclical

That said, the company's skew to spirits (~80% of net sales) does introduce cyclicality to its business. This is playing out now, with the company downgrading guidance in calendar Q4 2023. Previously, 1H FY2024 was seen delivering a "gradual improvement" in organic net sales growth versus 2H FY2023 (N.B. Diageo's fiscal year ends in June). FY2023 organic net sales growth was 6.5% overall, but with stronger performance in H1 (+9% organic net sales growth) implying only circa 3% growth in H2.

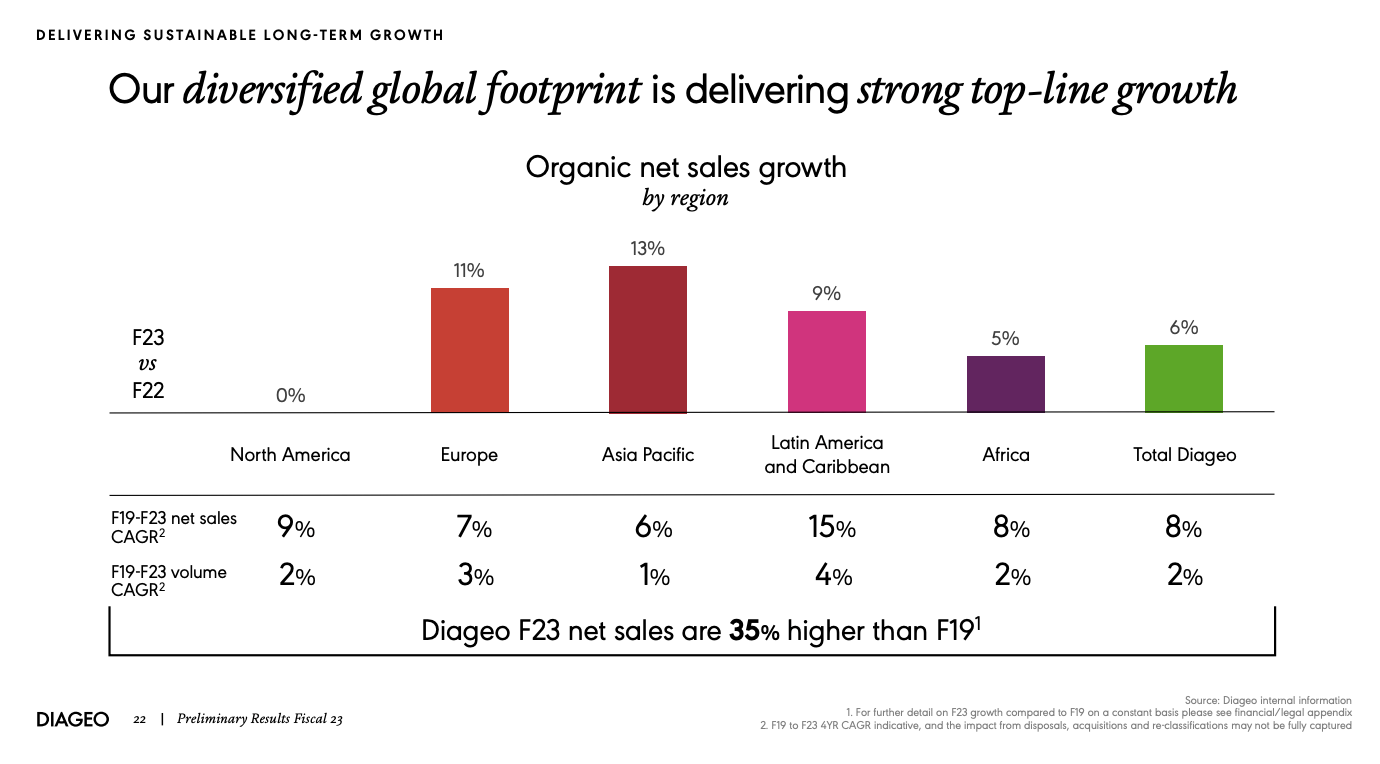

Guidance has since been downgraded to "slower growth than the second half of fiscal 23", principally on the back of a weak outlook in Latin America and Caribbean ("LAC"), where organic net sales are expected to decline by over 20% year-on-year. Consumer finances are weakening, and the associated downtrading means retailers are opting to run down the relatively high inventory levels they built up during better times. Complicating matters is that retailers were probably happy to build up inventory levels in response to post-COVID inflation, as rising prices can make this a profitable trade for retailers.

The above probably flattered results in previous periods, with the current softness representing normalization. Indeed, LAC was previously a very strong performer, delivering a FY19-23 net sales CAGR of 15% and volume CAGR of 4%, making it the best performing geography on those metrics in that period. As such, I think it is fair to view these issues as largely transient and cyclical rather than company specific.

Source: Diageo FY2023 Annual Results Presentation

{kind=link}

Other areas are mixed but performing better. In North America (40% of sales; 50% of EBIT), performance is seen improving sequentially in 1H FY2024, albeit this is off a fairly low base as FY2023 organic net sales growth was flat having risen 3% in H1 (implying a weak H2). With U.S. spirits still growing, this does imply the company has been losing some market share, but again this looks to be in part due to consumer downtrading. I would note that Diageo has increased the "premium-plus" share of its net sales by 7ppt since FY2019 which, while beneficial to growth over the long run, may also have introduced extra cyclicality and therefore potential short-term volatility to its business.

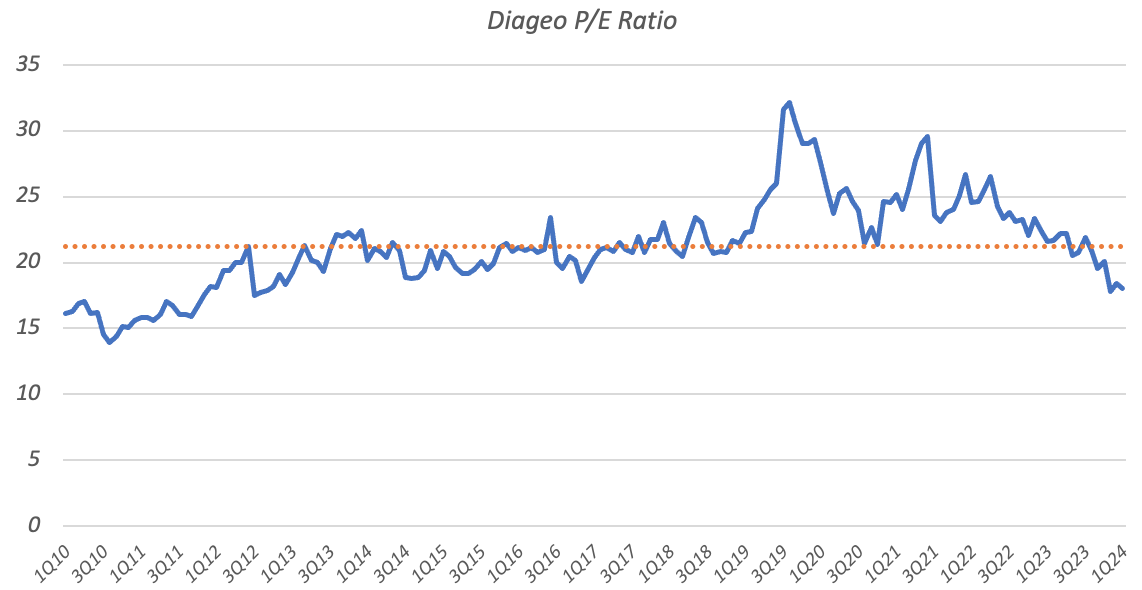

Diageo Stock Has Also De-Rated

The above partly explains Diageo stock's recent poor performance, with the current FY2024 consensus EPS estimate of $1.87 (~$7.50 per ADS) implying a roughly mid/high-single-digit year-on-year decline. However, Diageo stock has fallen by just over 25% over the past twelve months, implying that valuation multiple de-rating has also played a significant part in driving recent poor returns. At $139 in current trading, Diageo trades on a P/E of around 18.5x consensus EPS, down from over 20x FY2023 EPS a year ago. The current valuation also puts the stock below its long-run average of a little over 20x EPS.

Data Source: Yahoo Finance, Diageo Annual Reports, Author Calculation

{kind=link}

While the discount remains modest, this is based on estimated FY2024 earnings, which are likely to be depressed due to the cyclical factors outlined above. Assuming a recovery nearer the low-end of management's targets gets us to a 6% long-term EBIT CAGR. This can lead to attractive stock returns given the company can likely deliver modest incremental growth to EPS via stock buybacks. I base that on current leverage (~2.5x EBITDA) and the company's attractive ROIC profile mentioned previously, with a circa 7.5% EPS CAGR being my base case. With an additional 2.9% from the current dividend (~$4.02 per ADS), total returns would land in the 10-11% annualized area, with added upside should growth land above the low-end of company targets.

While I do expect a modest tailwind from the P/E re-rating up to 20x, this is not necessary for investors to realize acceptable returns. A 20x P/E is higher than the market average, though justified for reasons already mentioned, namely that Diageo's growth prospects are around average (relative to the stock market) but its capital returns potential is above average on account of its higher profitability. Together, this should result in a premium valuation for the stock. With returns potential looking attractive even at the low-end of company targets, now looks like a good opportunity to begin accumulating these shares, and I open on Diageo with a 'Buy' rating.

Risks

The main risks to Diageo come from sales and EBIT growth expectations. Sales growth could land lower than expected for numerous reasons, including structurally lower growth in developing markets, a reversal/pause in the ongoing shift to spirits in developed markets, as well as a reversal in the outsized growth in premium-plus categories. These are all largely linked to broader GDP growth, and would render management's growth targets overly ambitious. I see less category-specific risk to Diageo given the breadth of its portfolio, though the company is relatively light in certain areas (e.g. U.S. whiskey). Likewise, the operating leverage implied in management's longer-term growth targets may fail to materialize for various reasons (e.g. higher marketing spend needed to support brands), which would also render growth targets overly ambitious.

For further details see:

Diageo: Cyclical Headwinds Provide A Nice Entry Point