DGEAF - Diageo: Fairly Valued

2023-06-24 07:23:06 ET

Summary

- Diageo reported great results for the first half of fiscal 2023.

- The company will profit from a growing underlying market and the company can grow due to acquisitions.

- Despite the economic moat that Diageo has around its business, the stock is not a great investment right now and fairly valued at best.

It has been more than two years that I covered Diageo plc (DGEAF) (DEO) for the first and only time. In my article published in early January 2021 I acknowledge that the British company had a good business model and wide economic moat around its business, but I had doubts due to the valuation of the business.

Now almost two and a half years later, the stock is trading more or less for a similar price as back then. But a similar stock price does not mean that the business must still be overvalued. The fundamental business have improved in the meantime and a price which was not justified in January 2021 might be justified now. Let's take a closer look.

Interim Results

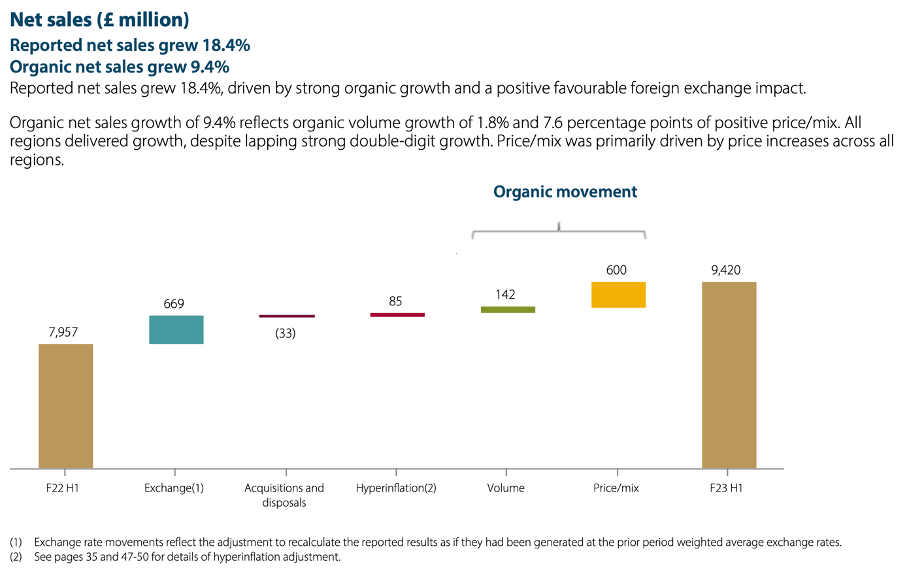

For starters, let's look at the interim results of Diageo (the annual results will not be published before August 1, 2023). In the first half of fiscal 2023, reported sales were GBP 13,219 million and compared to the same timeframe last year (GBP 11,753 million) sales increased 12.5% year-over-year. In case of Diageo, it makes sense to subtract the excise duties (indirect taxes on the sale of alcohol or tobacco). When subtracting that amount, we get net sales of GPB 9,420 million for H1/23. When comparing that amount to GBP 7,957 million in H1/22 we get a year-over-year growth rate of 18.4%.

Diageo Net Sales H1/23 (Diageo H1/23 Earnings Release)

{kind=link}

However, when looking at the chart above, we see that exchange rates made a huge contribution to year-over-year growth. Nevertheless, organic sales grew 9.4% year-over-year (with price/mix contributing 7.6% YoY growth) are a solid growth rate for a mature business like Diageo. Operating income increased from GBP 2,743 million in H1/22 to GBP 3,161 million in H1/23 - resulting in 15.2% year-over-year growth. And diluted earnings per share increased 19.8% year-over-year from 84.0 pence in the same timeframe last year to 100.6 pence in the first half of 2023.

{kind=link}

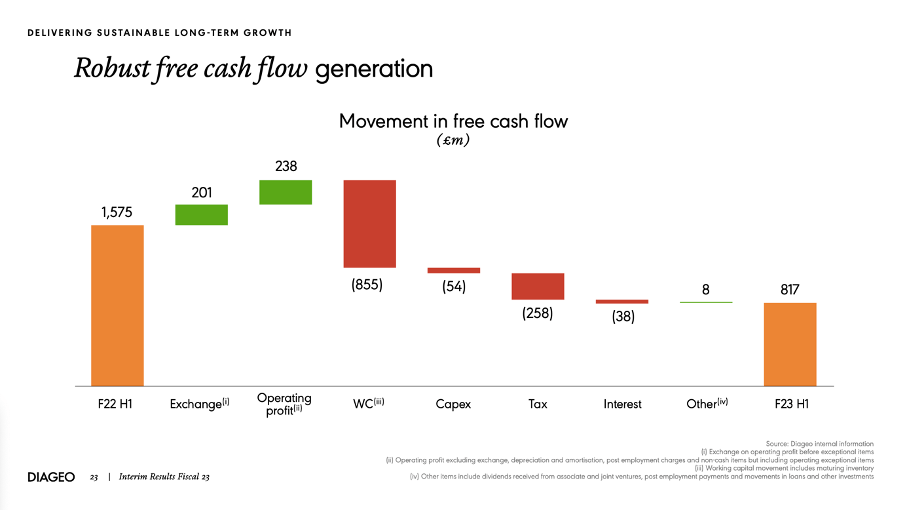

While earnings per share grew with a high pace, free cash flow declined from GBP 1,575 million in H1/22 to GBP 817 million in H1/23 - resulting in 48.1% year-over-year growth.

Diageo H1/23 Results (Diageo H1/23 Earnings Release)

{kind=link}

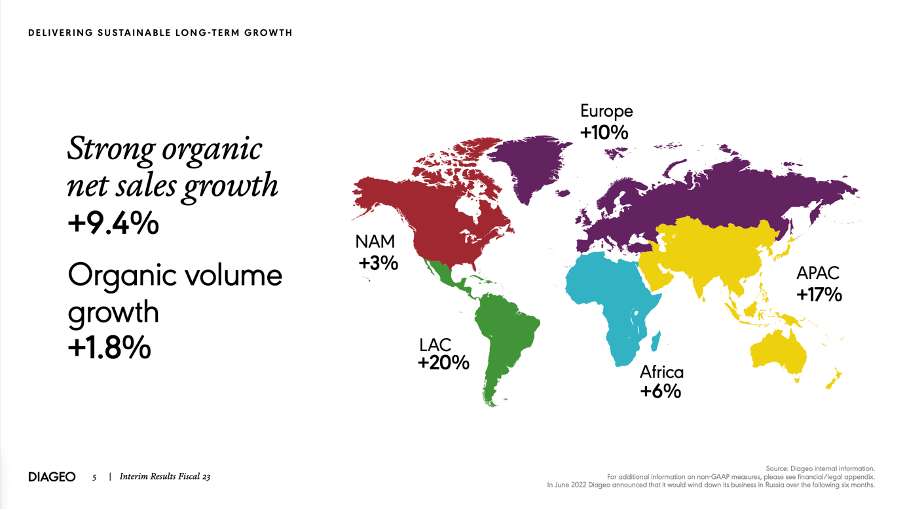

And when looking at the different regions, we see especially high growth rates in Latin America (20% YoY growth in H1/23), Asia-Pacific (17% growth) and Europe (10% growth).

{kind=link}

Growth

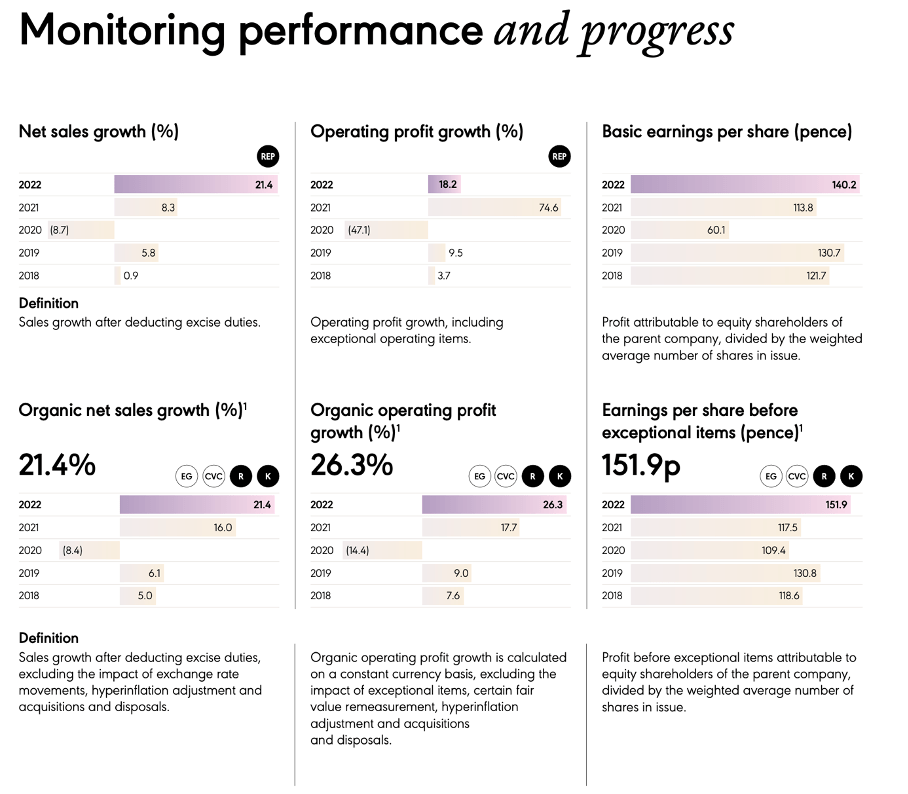

When not only looking at the growth rates in the last few months but in the last few years, Diageo can actually report solid growth rates.

{kind=link}

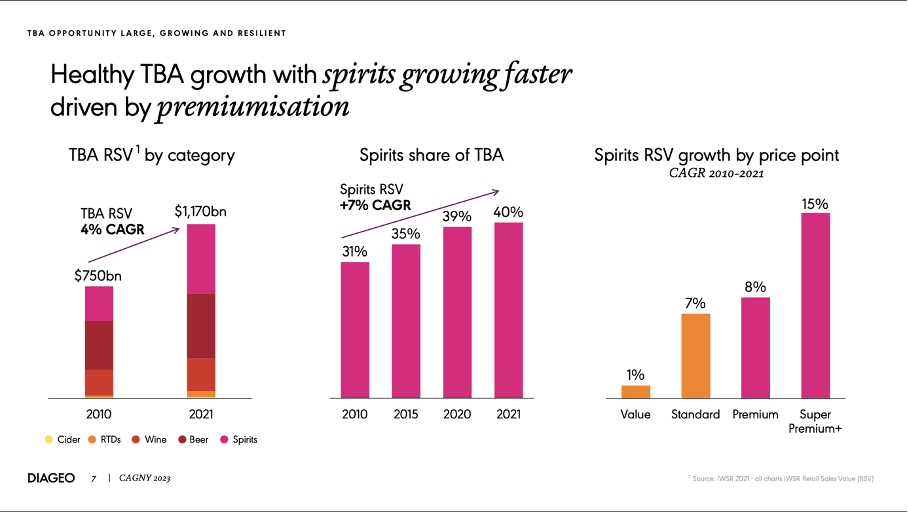

And when trying to look into the future, the underlying trends for the overall market are quite positive. In the years between 2010 and 2021, the total beverage alcohol (TBA) market was growing with a CAGR of 4% and spirits (the segment Diageo is focused at) even gained market shares and was growing with a CAGR of 7%. When looking at the spirits market by price point, we can see that especially premium and super premium plus grew with a high pace and these are the two categories Diageo is mostly focused on. If these trends should continue, Diageo might be positioned well for years to come.

Diageo CAGNY 2023 Presentation

{kind=link}

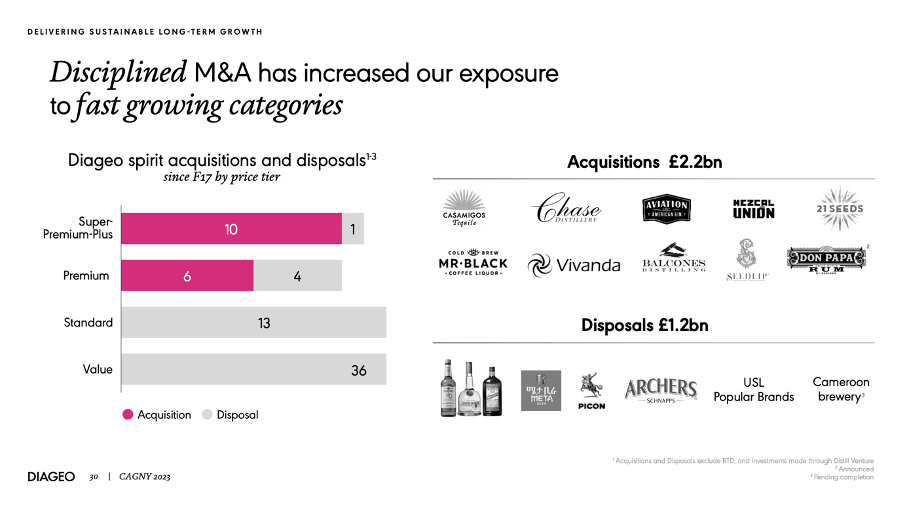

Diageo also made acquisitions in the last few years - especially in the high-end market that was growing with the highest pace in the last few years. In the last five years, Diageo made 10 acquisitions in the Super-Premium-Plus tier and 6 acquisitions in the Premium tier.

Diageo CAGNY 2023 Presentation

{kind=link}

And it certainly might be a strategy to make further acquisitions in the years to come. But Diageo needs the balance sheet with the necessary cash to support acquisitions. On December 31, 2022, Diageo already had GBP 2,305 million short-term borrowings and bank overdrafts as well as GBP 15,304 million in long-term borrowings. When comparing the total debt to the total equity of GPB 9,866 million we get a debt-equity ratio of 1.78, which is rather high. And when comparing the total debt to the operating income of fiscal 2022 (GBP 4,409 million) it would take four years to repay the outstanding debt. Both metrics are still acceptable but, in my opinion, Diageo should not take on a lot of additional debt. Of course, we should not ignore GBP 2,766 million in cash and cash equivalents.

Diageo CAGNY 2023 Presentation

{kind=link}

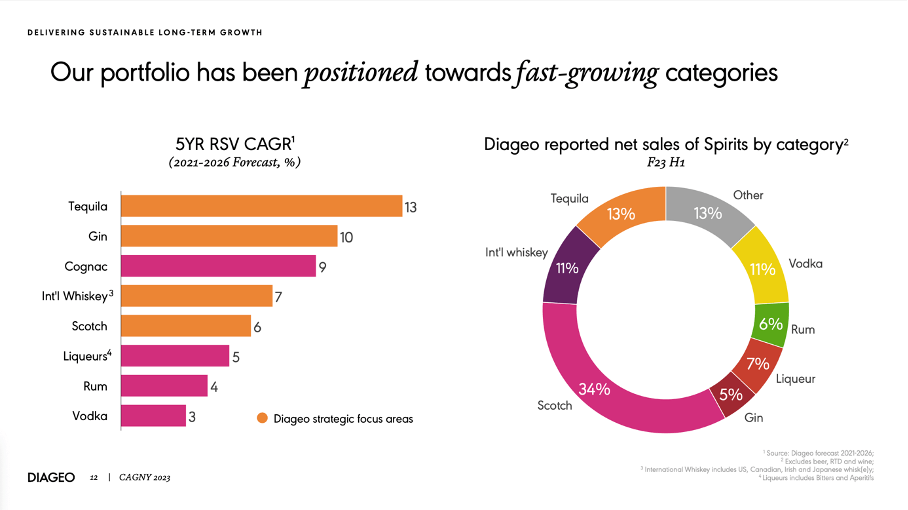

Diageo will also focus on its growth categories and should also be able to achieve organic growth in the next few years. Especially Tequila (13%) and Gin (10%) were growing with a high pace over the last few years and the company will focus on these two categories. Additionally, the company will focus on International Whiskey and Scotch, which was growing only 6% in the last few years and was responsible for 34% of net sales.

Diageo CAGNY 2023 Presentation

{kind=link}

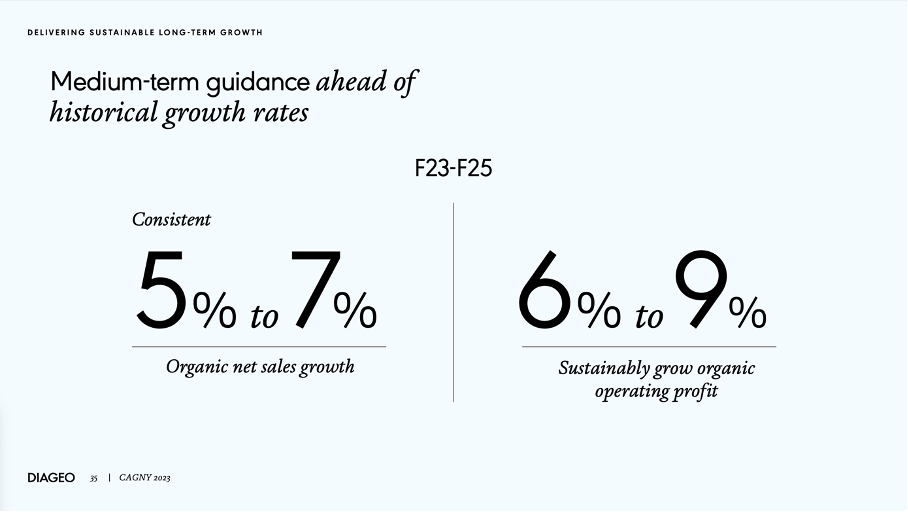

And for the next few years, Diageo has solid mid-term growth targets of 5% to 7% organic net sales growth and 6% to 9% organic operating growth.

When talking about growth rates in the quarters and years to come, we also must take into account how drinking habits might change during recessions. In theory, we formulated two theses: One would be of a recession leading to higher levels of unemployment and a tighter budget which is increasing the stress level for people and leading to higher alcohol consumption. The other thesis is that the disposable income is declining, and people will spend less and are saving on non-essential items like alcohol. Of course, this is not the case for addicts. And there are studies for both theories and pieces of information that might verify the argument (see here , here and here ). At best, we can describe the picture as mixed but should keep in mind that a potential recession in the next few quarters might have a negative impact on the business.

Economic Moat

And we should not ignore that Diageo has a wide economic moat around its business that will help the company to report stable growth rates in the years to come and maybe continue to gain market shares (or at least hold its market share and not lose business to a competitor). In my last article, I explained the economic moat of Diageo:

As Diageo is an aggregation of many different brands, the source of the company's moat seems quite obvious. The different world-leading brands create a competitive advantage as some of the brands are increasing the customer's willingness to pay a higher price.

(…)

The brand names might also reduce the search costs for the customers. By recognizing a brand like Smirnoff or Johnnie Walker, I know I can trust the product and be sure I will get a similar quality as in the past and a similar product. A brand name is reducing the complexity for the customer when making a buying decision. And Diageo has many well-known brands like Smirnoff, Guinness, Captain Morgan or Baileys.

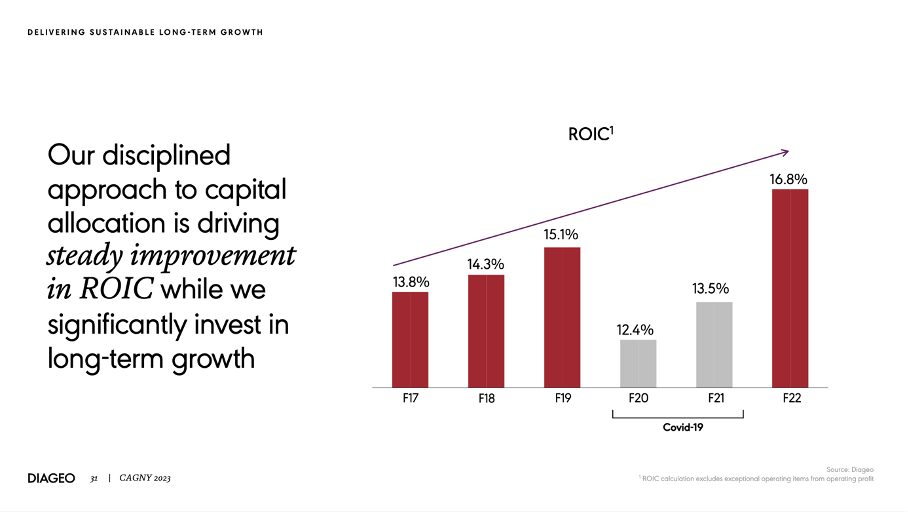

And when looking at return on invested capital as one of the most important metrics for a wide economic moat, we see increasing numbers over time - and even during the two COVID years, Diageo reported an RoIC above 10%.

Diageo CAGNY 2023 Presentation

{kind=link}

Intrinsic Value Calculation

At the time of writing, Diageo is trading for 22.76 times earnings, which is neither extremely expensive nor extremely cheap. And it is below the average P/E ratio of the last 10 years (which was 26.24). While Diageo is fairly valued when looking at the P/E ratio, the price-free-cash-flow ratio is painting a different picture. With a P/FCF ratio of 38.49 right now, the stock is anything but cheap and trading above the average P/FCF ratio of 30.67 in the last ten years.

Instead of looking at these simple valuation metrics we can also use a discount cash flow calculation to determine an intrinsic value for the stock. As basis for our calculation, we can look at the cumulative free cash flow of the last three years, which was GBP 8,271 million and is leading to an average free cash flow of GBP 2,757 million. And as the number is close to the free cash flow of fiscal 2022 (GBP 2,783 million) we take that number as basis. When looking at growth rates in the last few years we see high levels of consistency (which is making it easier to calculate an accurate intrinsic value) and we can assume growth rates of 7% for the next ten years followed by 6% growth till perpetuity. As always, we assume a 10% discount rate and use 2,281 million outstanding shares for our calculation which leads to an intrinsic value of GBP 32.74 for the stock and is making Diageo fairly valued (trading at 3330 pence right now). And as four ordinary shares of Diageo represent one Diageo ADS - and of course also considering the exchange rate between Great British Pound and the US Dollar right now - we get an intrinsic value of $166.41 for the ADS.

Conclusion

Diageo seems to be well positioned to keep growing in the mid-to-high single digits by focusing on the high-end market (which was clearly outperforming the other market segments in the last few years). And the wide economic moat around the business will protect Diageo from competitors stealing market shares. Overall, Diageo seems to be fairly valued at this point and making the stock still a hold.

For further details see:

Diageo: Fairly Valued