DEO - Diageo: Fears Of U.S. Slowdown After H1 Creating A Bargain

Summary

- Diageo shares fell 5.5% after results last week and are at 20.7x CY22 EPS and 24.8x pre-COVID FY19 EPS. The Dividend Yield is 2.3%.

- H1 FY23 results were strong, with organic growth of nearly 10% in Net Sales and EBIT, but sales growth in North America was just 3%.

- While investors fear a downturn, we are relatively sanguine because Diageo's premium-led sales growth should be resilient.

- North America's growth since FY19 has been reasonable, Europe was resilient in H1 despite weak macro, and China is reopening.

- With shares at 3,445.0p, we expect a total return of 69% (17.1% annualized) by June 2026, in about 3.5 years. Buy.

Introduction

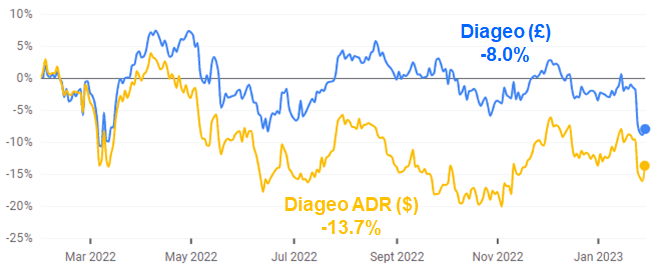

Diageo plc ( DEO ) released their H1 FY23 results last Thursday (January 26), and shares fell 5.5% in London that day. Diageo shares have now fallen 8.0% in U.K. pounds in the past year, and its American Depository Receipts (“ADRs”) have fallen 13.7% in U.S. dollars over the same period:

{kind=link}

Compared to the level at which we originally initiated our Buy rating in July 2019, Diageo shares have gained just 7.8% (after dividends) in U.K. pounds in roughly 3.5 years, though including 24.9% from the end of 2020.

Diageo shares are now back to the level of their pre-COVID peak in August 2019, following good FY19 results. The subsequent decline in the share price coincided with a slowdown in sales growth in Europe & Turkey and LATAM & Caribbean, which took Diageo’s organic Net Sales growth down to 4.2% and its organic Adjusted EBIT growth down to 4.6% for H1 FY20 (June-December 2019), just before the COVID-19 outbreak:

{kind=link}

H1 FY23 results were strong. Net Sales and Adjusted EBIT both grew by nearly 10% organically year-on-year, and currency added a further boost (in U.K. pounds). Investors are concerned about recent earnings being a cyclical peak, partly because organic sales growth in North America decelerated to just 3%. We are relatively sanguine for a number of reasons. Sales growth in recent years has been led by premium products, which should be more resilient. The deceleration in North America was overstated because shipments ran behind depletions by 1 ppt, sales growth was strong in Europe despite difficult macro, and the end of “zero COVID” policies in China should also help. For now, management are generally confident about H2 and have reiterated FY23-25 targets. Diageo shares are at a cheap 20.7x P/E on CY22 EPS and a reasonable 24.8x P/E even on FY19 EPS. The Dividend Yield is 2.3% and another £500m of buybacks have been announced. Our forecasts indicate a total return of 69% (17.1% annualized) by June 2026. Buy.

Diageo Buy Case Recap

Our invest ment case ( revisited in deta il in December) on Diageo has been based on the structural volume and value growth in global spirits, and Diageo’s ability to take advantage of this growth:

- The global spirits industry is benefiting from structural increases in the population of drinkers, penetration rates (including share gains from wine and beer) and premiumisation. In 2010-21, total Retail Sales Value of spirits grew at a CAGR of 4.1%, with Premium spirits growing at 8.1% and Super Premium+ spirits growing at 14.8%

| Global Spirits Retail Sales Value Growth (2010-21) Source: Diageo results presentation (FY22). NB. TBA = Total Beverage Alcohol, RTD = Ready To Drink. |

- Diageo can grow sales faster than the spirits market thanks to its over-indexation to premium brands (57% of its net sales by FY22), as well as its strong brands, scale, and capabilities in innovation, marketing and distribution

- Diageo can continue to expand its operating margin, from a combination of pricing, positive mix shift, operational leverage and cost efficiencies

At its November 2021 investor day , Diageo has set out long-term targets to increase its share of the global Total Beverage Alcohol market from 4.0% to 6.0% by 2030. For FY23-25, management is targeting a “consistent” 5-7% organic net sales growth and a “sustainable” 6-9% organic EBIT growth annually:

| Diageo FY23-25 Targets Source: Diageo investor day presentation (Nov-21). |

We believe Diageo’s medium-term targets to be achievable, based on its performance in recent years.

H1 FY23 results actually showed significantly stronger growth rates than Diageo’s medium-term targets.

Diageo H1 FY23 Result Headlines

H1 FY23 results were strong. Net Sales and Adjusted EBIT both grew by nearly 10% organically year-on-year, and currency added a further boost so both grew by high-teens (in U.K. pounds) on a reported basis:

| Diageo Profit & Loss ( H 1 FY2 3 vs. Prior Year) Source: Diageo company filings. |

Strong H1 FY23 growth followed an already strong prior-year period where Net Sales grew 19.6% organically and Adjusted EBIT grew 25.4% organically, rebounding from the COVID-impacted June-December of 2020.

Organic Net Sales growth of 9.3% in H1 FY23 consisted of 1.8% growth in volume and 7.6% in price/mix, with the latter “reflecting price increases taken by all regions” and including a “high-single-digits” contribution from price.

Adjusted EBIT Margin grew 9 bps organically year-on-year, with a decline in Gross Margin (due to cost inflation) more than offset by smaller margins for Marketing costs and Other Operating Expenses (though both grew by double-digits in absolute terms, after currency). Management also stated they achieved £220m of cost savings in H1 FY23, taking total savings achieved to £600m of the £1.2bn savings targeted in FY22-24. Including currency, Adjusted EBIT margin shrunk 57 bps year-on-year.

Adjusted Net Income grew 14.1%, less than Adjusted EBIT, due to both higher Finance Charges (from a higher interest rate and currency swap losses) and higher tax (from a higher tax rate, the result of a negative mix shift in profits).

Adjusted EPS grew 17.1%, more than Adjusted Net Income, after buybacks helped reduce the share count by 2.5%.

While group headlines were strong, some investors were concerned by a deceleration in North America.

Diageo’s H1 North America Slowdown

Diageo shares likely fell after H1 FY23 results because investors are concerned about a cyclical peak, and such fears were supported by a deceleration in North America.

North America Net Sales only grew 3% organically year-on-year, and its Adjusted EBIT fell 2% organically due to a small margin decline. Of the four remaining regions, three saw organic Net Sales growth of 10% or more (except the relatively small Africa region); all four saw organic Adjusted EBIT growth in double-digits:

| Diageo Net Sales & EBIT by Region ( H1 FY2 3 vs. Prior Year) Source: Diageo company filings. |

In addition, North America’s 3% organic Net Sales growth was the product of a 4% organic decline in volume and an approximately 7% price/mix benefit; volume fell in every product category except Ready-To-Drink:

| Diageo V olume & Net Sales G rowth – North America ( H1 FY2 3 ) Source: Diageo results release (H1 FY23). |

However, we are relatively sanguine about the prospects of a North American slowdown for a number of reasons.

Premium-Driven Growth Likely More Resilient

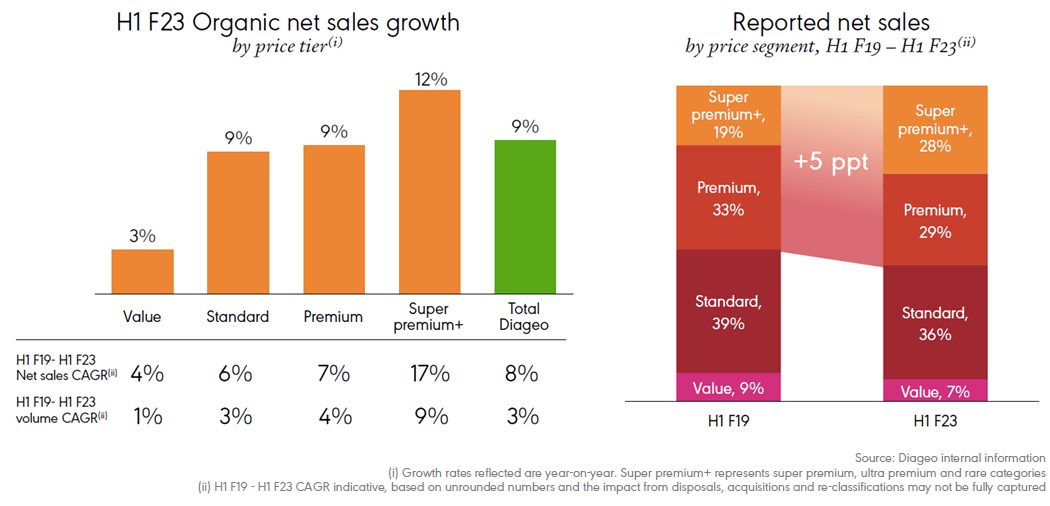

Diageo’s sales growth in recent years has been led by premium products, which should be more resilient.

While Diageo Net Sales have grown at an organic CAGR of 8% between H1 FY19 and H1 FY23, growth has been led by the Super Premium+ price tier, which has grown at a CAGR of 17%; Net Sales CAGR was slightly below group average for Premium (7%) and Standard (6%), and much lower than group average for Value (3%):

| Diageo Net Sales Growth B y Price Tier ( H1 FY19 to H1 FY2 3 ) Source: Diageo results presentation (H1 FY23). |

{kind=link}

Together the Super Premium+ and Premium price tiers represented 57% of Net Sales in H1 FY23, up 5 ppt from H1 FY19. Products in these price tiers are more likely to be consumed by people with higher disposable incomes, who in turn are less likely to be impacted by an economic downturn. (As we discussed in our December article, during the Global Financial Criss Diageo’s Adjusted EBIT grew by 4% in FY09, 2% in FY10 and 5% in FY11 – Diageo’s performance at the next downturn should be better because of the premiumization and diversification since then.)

Diageo U.S. Deceleration Likely Overstated

The deceleration in Diageo’s North American business in H1 FY23 was also likely somewhat overstated, as revenues were based on actual shipments, which were running 1 ppt behind depletions.

During H1 FY23 Diageo also held its overall market share (gaining in the “on” trade but losing in the “off trade”), in contrast to gaining share previously, possibly due to above-average price hikes. As CEO Ivan Menezes explained on the earnings call :

“In the US context, we are holding share at TBA (Total Beverage Alcohol). We are coming off a period where we have grown significant share and we have also taken price ahead of the industry … We want to get back into the share growth mode in the US and I expect in the medium-term we will do that”

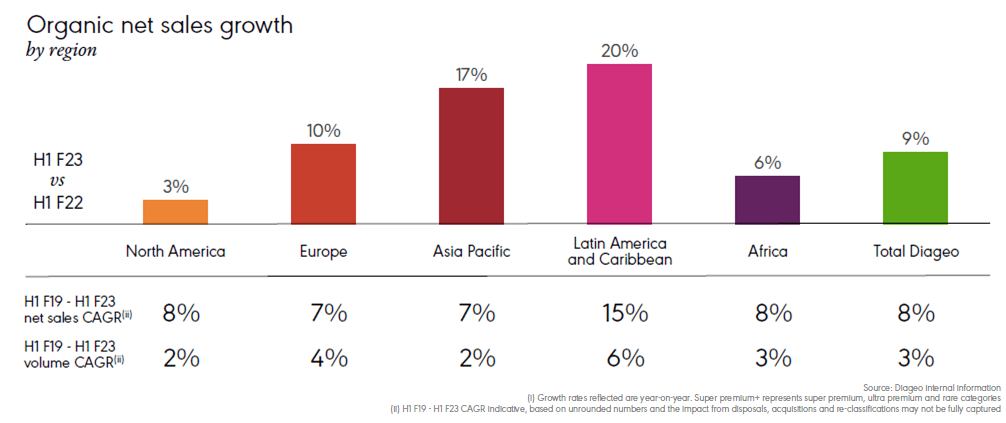

Diageo’s Net Sales growth in North America since FY19 has not been much higher than those in other regions (which did not see a deceleration in H1 FY23). North America’s organic Net Sales CAGR between H1 FY19 and H1 FY23 was 8%, in line with group average and only 1 ppt ahead of Europe and Asia Pacific:

| Diageo Net Sales Growth B y Region ( H1 FY19 to H1 FY2 3 ) Source: Diageo results presentation (H1 FY23). |

{kind=link}

The North American spirits market has historically grown at mid-single-digits annually. Diageo’s 8% CAGR in H1 FY19 to H1 FY23 is higher than this, but reasonable in the context of its focus on the premium end of the market (which has grown faster) and its market share gains.

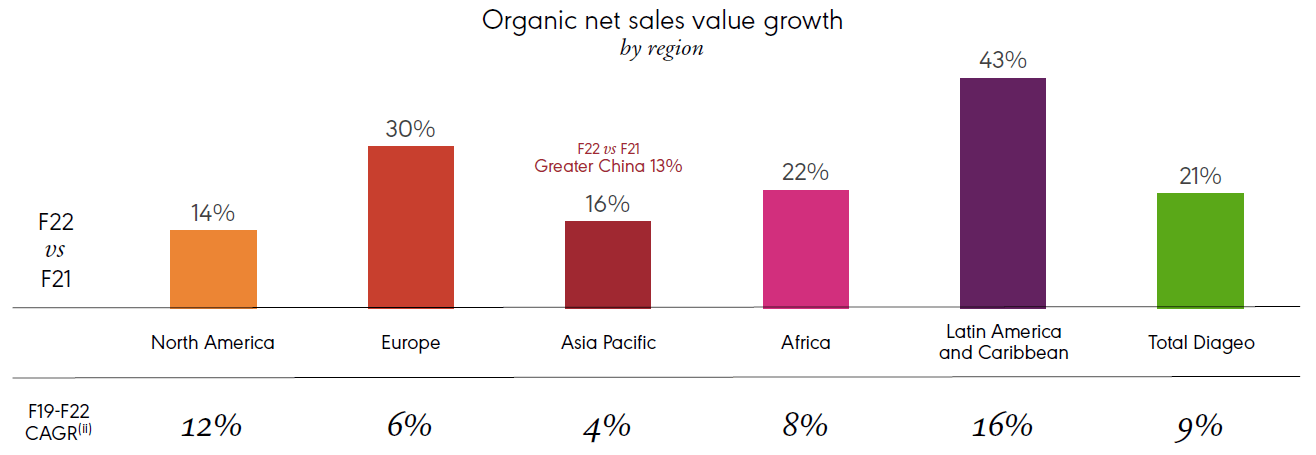

In fact, the H1 FY23 deceleration in Diageo’s Net Sales in North America as well as continuing strong growth in most other regions mean that mid-term sales CAGR (from FY19) is now much more even across regions than in FY22:

{kind=link}

What we saw in H1 FY23 is therefore likely no more than a normalization of growth rates in each region to their long-term trends, but with FY22 representing a permanently higher base due to an acceleration of ongoing trends (premiumization, Diageo market share gains, etc.) during COVID-19.

The decline in Adjusted EBIT Margin in North America in H1 FY23 was the result of both cost inflation and Diageo having “invested strongly in A&P, also in digital and capabilities” in the period. It should also be seen in the context of North America historically having had the highest margin within the group (43.7% vs. the group’s 34.5% in H1 FY22).

Therefore, we do not believe Diageo’s sales in North America represent much of a cyclical peak. In the event of a U.S. recession, there might be some negative impact on Diageo sales, but likely modest and temporary in nature.

Strong Growth in Europe Despite Poor Macro

We also take comfort from how sales growth was strong in Europe despite the difficult macro environment there.

| Diageo V olume & Net Sales G rowth – Europe ( H1 FY2 3 ) Source: Diageo results release (H1 FY23). |

Organic Net Sales growth was 10% in Europe, and double-digits in most key countries and regions, except the U.K. (with a uniquely weak economy following Brexit) and Eastern Europe (due to Diageo exiting Russia).

End of “Zero COVID” in China to Help

The end of “zero COVID” policies in China since early December should also help Diageo sales.

China is around 5% of Diageo sales and has historically grown at double-digits. However, the disruption from China’s abrupt reopening (and subsequent mass COVID infections) meant that Greater China Net Sales only grew by 2% organically in H1 FY23, and Chinese White Spirits sales groupwide actually shrunk 7% organically.

A recovery in Chinese demand should help Diageo sales, though this may not fully materialize in H2 FY23, as the key Chinese New Year period was “subdued in terms of socialising and consumption” (according to Diageo).

More Currency Benefit from Weak Pound

Diageo will likely see a further benefit (in U.K. pounds) from currency, as current spot rates for key currencies remain modestly lower than in FY22 (GBP/USD at 1.23 is about 5% lower, and GBP/EUR at 1.13 is about 4% lower):

| Diageo Key Exchange Rates (FY2 1-22 ) Source: Diageo results presentation (FY22). |

Based on 2022 year-end spot rates (GBP/USD at 1.20 and GBP/EUR at €1.13), management were expecting a positive currency impact of £300m on EBIT in FY23, or about 6% of FY22 Adjusted EBIT.

Confident on H2, Mid-Term Targets Reiterated

For now, while not giving short-term guidance, management are generally confident about H2. Comments by CEO Ivan Menezes on the call include:

“The US industry should be in solid mid-single-digit growth in the second half. We expect to perform in line, ideally better.”

“The European consumer obviously is something that we've put a lot of scrutiny behind. We're confident we will continue to maintain the share momentum. What the external world does, we will deal with.”

“We're not seeing a weakening of the premiumisation trend really anywhere: Latin America, Asia, India, certainly in the developed world.”

Management has also reiterated Diageo’s FY23-25 targets. CFO Lavanya Chandrashekar said on the call:

“We are well?positioned to deliver our medium?term guidance of consistent organic net sales growth in the range of 5% to 7% and sustainable organic operating profit growth in the range of 6% to 9% for fiscal 23 to fiscal 25.”

Diageo Stock Dividend Yield & Valuation

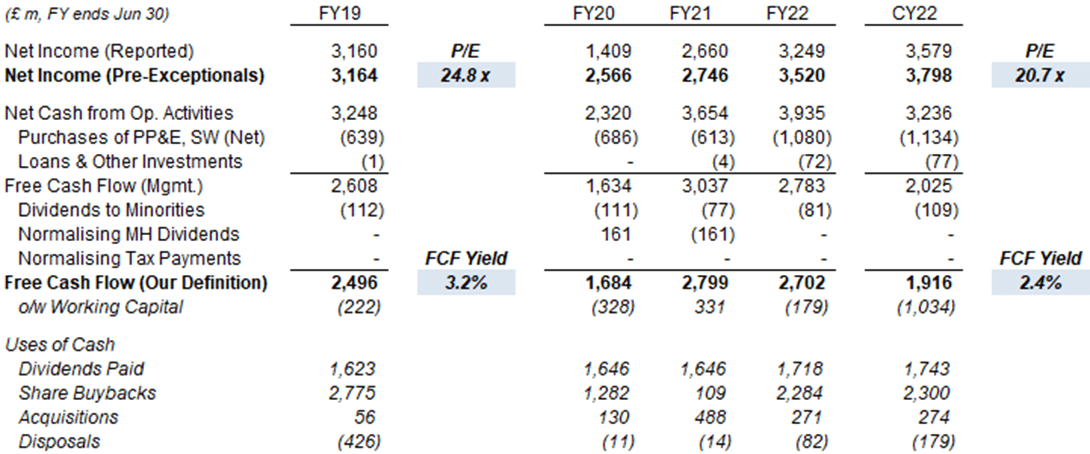

At 3,445.0p, relative to CY22 financials, Diageo shares have a cheap 20.4x P/E and a 2.4% Free Cash Flow (“FCF Yield”); even relative to pre-COVID FY19, shares have a reasonable 24.8x P/E and a 3.2% FCF Yield:

| Diageo Earnings, Cashflows & Valuation (FY19 - CY 22) Source: Diageo company filings. NB. FY21 £290m dividends received included £161m for CY19 and £128m for CY20. |

{kind=link}

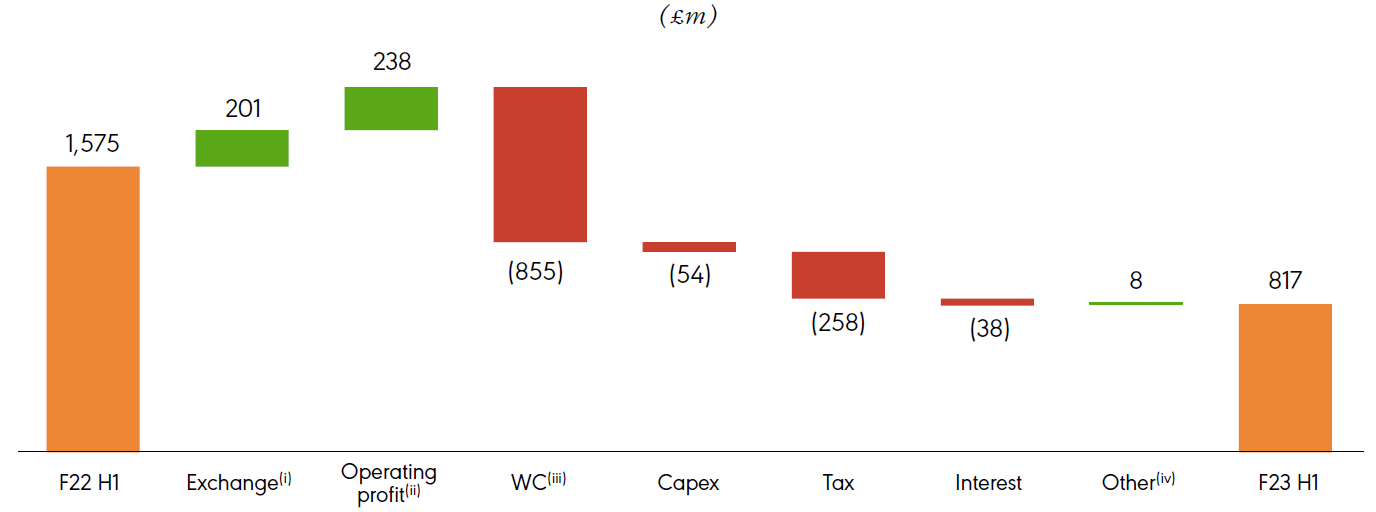

CY22 FCF was dragged down by a FCF decline in H1 FY23. This was largely due to much higher working capital outflows, the result of creditors returning to pre-COVID norms (about £500m), higher inventories (£150m) and maturing stock (not quantified); a higher tax payment (£258m) was also a factor:

{kind=link}

Dividend raised its interim dividend by 5% at H1 FY23 results, taking last-twelve-month dividends to 77.65p, which represents a Dividend Yield of 2.3%. The Dividend Cover is now 2.1x, compared to a 1.8-2.2x target.

Share buybacks of £554m were carried out in H1 FY23. Diageo now intends to complete the last £300m of its £4.5bn FY20-23 share repurchase program early, by the end of February 2023 instead of June 2023, and the Board has authorized another £500m of buybacks, to be completed by June 2023. The £800m total to be repurchased by FY23 year-end is equivalent to 1% of the current market capitalization.

Net Debt / EBITDA was 2.5x at December 2022, flat year-on-year, though actual Net Debt has increased from £12.8bn to £15.6bn. Management now intends to remain at this low end of the 2.5-3.0x range, due to macro uncertainties.

Illustrative Diageo Stock Forecasts

We reduce our forecasts slightly due to macro uncertainty and a slightly stronger U.K. pound. We now assume:

- FY23 Net Income growth to be 11.0% (was 12.5%), implying H2 growth of 5%

- Thereafter, Net Income grows at 8.0 % annually (was 8.5%)

- Dividends to be based on a 50% Payout Ratio (unchanged)

- Share count to fall by 1.0% annually (unchanged)

- FY26 year-end P/E of 25.0x (was 27.0x)

Our new FY26 EPS of 220.4p is 3% lower than before (226.5p):

| Illustrative Diageo Return Forecasts Source: Librarian Capital estimates. |

With shares at 3,445.0p, we expect an exit price of 5,510p and a total return of 69% (17.1% annualized) by June 2026, in about 3.5 years.

Is Diageo Stock a Buy? Conclusion

We reiterate our Buy rating on Diageo stock.

For further details see:

Diageo: Fears Of U.S. Slowdown After H1 Creating A Bargain