DEO - Diageo: Growth Should Continue Just Like It Did Historically

2023-09-22 13:21:46 ET

Summary

- Diageo has the potential for continued growth, which should drive a market re-rating.

- Diageo's ability to adapt and thrive, as evidenced by its 6.5% organic net sales growth in FY23, suggests a positive outlook for the company.

- Valued at 19x forward earnings, Diageo has a 17% upside potential, supported by its premium market position and profit margins.

Investment Action

Based on my current outlook and analysis of Diageo (DEO), I recommend a buy rating. I expect the market to re-rate the stock upwards, closer to its historical average of 21x forward earnings, as it realizes Diageo can continue to perform just like it did in the past. The key catalyst to drive a re-rating is likely when US organic sales turn positive, signaling that the current weakness is just a blip.

Basic Information

Diageo stands as a global trailblazer in the realm of premium beverages, boasting an extensive repertoire of over 200 brands and a formidable presence in excess of 180 countries. Its product portfolio demonstrates remarkable diversity, spanning the realms of both spirits and beer. Among the well-recognized and cherished labels under the Diageo umbrella are household names like Johnnie Walker, Guinness, Tanqueray, Baileys, and Captain Morgan.

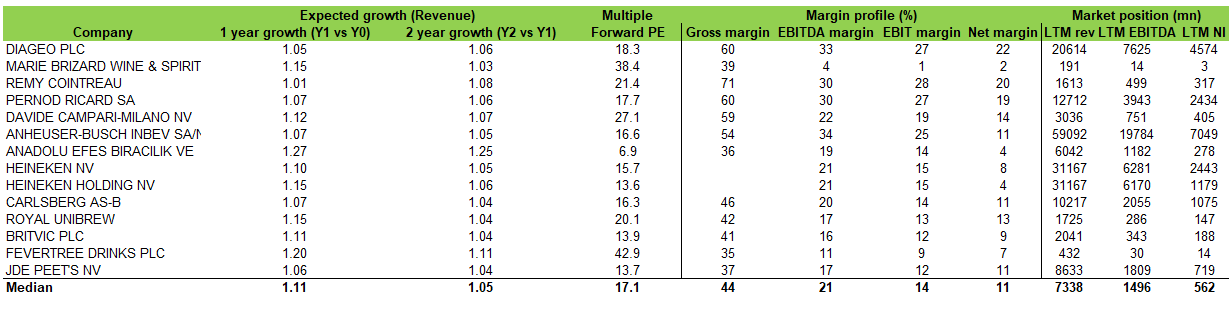

Operating within a vast and mature industry, Diageo finds itself at the heart of a sector estimated to be valued at a staggering $1.6 trillion in 2023 , with projected growth of 2.5% expected over the ensuing decade. Among its noteworthy competitors are industry heavyweights such as Remy Cointreau, Pernod Ricard (PRNDY), Anheuser-Busch InBev (BUD), Heineken (HEINY), Carlsberg, Royal Unibrew, and more.

Review

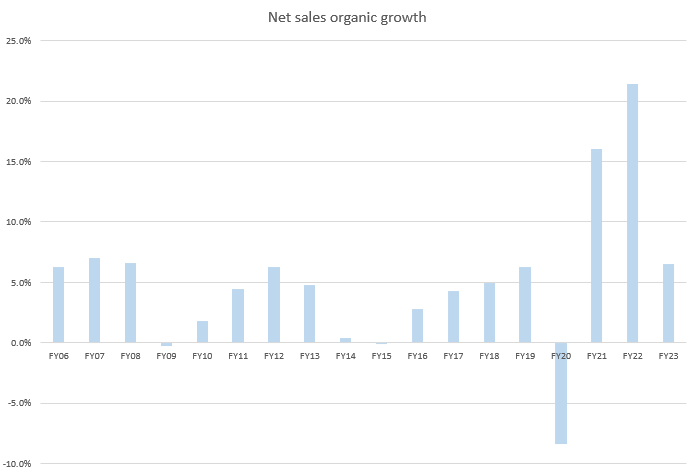

Diageo reported a total volume of EU243 million for FY23, representing an organic volume growth decline of 0.8% for the year. However, net sales grew 10.7% to GBP 17 billion, a 6.5% increase on an organic basis (10.7% on a reported basis). The 6.5% organic net sales growth was positive as it is in line with the business's historical organic growth, suggesting that the highs and lows of the COVID growth swing are now over. This was also the second consecutive year that the EBIT margin has stayed in the low 30% range, suggesting that margins are stabilizing.

{kind=link}

Since 2H23 organic sales and EBIT growth improved sequentially, I anticipate this trend to continue into FY24. However, I believe that Diageo's performance in the United States will be the main focus of investors, and that this will serve as a catalyst for the stock's re-rating. Organic growth dropped to -2.5% in 2H23, raising market concerns that growth may have peaked in the US, a significant region for the business (36% of total revenue in FY23). When compared to regions that are still experiencing organic growth, this is very concerning. Since management is positive that they can reclaim share by innovating in RTD and the Crown Royal brand, and by maintaining share gains in tequila, US bourbon, and scotch, I believe the market will eventually return it to its pre-recession mid-single-digit level. To elaborate, on the former, management plans to increase brand innovations, including flavors aimed at recruiting new customers, now that the Crown Royal supply constraints have been resolved. As Diageo will only compete in premium, category-growing, brand-supporting RTDs, rather than price-sensitive mass market RTDs for spirits, I anticipate positive pricing and brand-position accretion.

Overall, I am expecting Diageo to continue growing, just as it has historically declined steadily. The recent FY23 results clearly indicate resilient consumer demand, albeit with pockets of weakness (the US). However, if one were to take a step back, organic sales remained resilient, with Diageo continuing to showcase its ability to raise prices in 2H23. Pricing growth was apparent across all regions, ranging from low-single-digit growth to mid-teen percentage ranges. This speaks well of the Diageo brand position, which allows it to raise prices in the current difficult times.

Cycling back to the US discussion, the tequila market is at the center of this discussion because it is affected by both the lower-end and the high-end of the market. For these two ends, lower-end consumers are more sensitive to pricing, while the luxury end is seeing slower growth as it was partially driven by aspirational spending. Diageo's suffered from these dynamics as they had to raise prices for their products to support the long-term health of their brands. Naturally, the higher prices knock off lower-end consumer demand and further reduce the aspirational spending of luxury consumers. I would attribute some of these weaknesses to the current weak consumer climate, as some of them trade down to cheaper alternatives. Nonetheless, I should point out to readers that the super-premium tequila segment, which is more relevant for Diageo brands, has been expanding at a faster rate and has been the primary driver of the category's expansion. This is crucial because it shows that Diageo is expanding into the right segments. Once the US economy recovers, I expect growth to accelerate as Diageo experiences recovery growth and growth in the super-premium category.

Valuation

Author's work

I believe Diageo can grow at 6%, which is in line with its historical organic sales track record. While the US might have shown some weakness due to the tequila segment, I expect things to recover once the US economy returns to normal and consumers start to reverse the trade-down movement. I reiterate the point that Diageo continues to see growth in the super premium tequila segment. From a margin standpoint, Diageo has always been in the 20–25% range, and I expect the business to stay within this range (at the midpoint). With these assumptions, the business should generate GBP4.3 billion in earnings in FY25.

I am valuing Diageo at 19x forward earnings, a slight premium to peers’ median of 17x, as I believe the market will recognize that the business can continue to perform just like it did historically. Relative to peers, this premium is warranted as Diageo has a much larger market position at GBP20 billion in revenue vs. the median at only GBP7.3 billion. While Diageo's growth is slower, it has a much better profit margin profile, reflecting its premium position.

Based on my model, there is a 17% upside for the stock.

{kind=link}

Risk and Final Thoughts

I think the risk is that the US continues to see a slowdown for extended periods of time as the US economy continues to stay sluggish. Recall that my bullish argument is that consumers would regain confidence and reverse the trade-down movement. Should this not be the case, the stock could see further pressure as investors extrapolate the business slowdown in the US.

Summing up, I recommend a buy rating for Diageo. Diageo, a global leader in premium beverages, is poised for continued growth, mirroring its historical performance. The market is expected to recognize this potential and re-rate the stock closer to its historical average of 21x forward earnings. Recent results, such as the 6.5% organic net sales growth in FY23, demonstrate the company's ability to adapt and thrive. With improving trends in the United States and a focus on brand innovation and premium offerings, the outlook remains positive. Valuation-wise, Diageo's premium position justifies a valuation of 19x forward earnings in my view, slightly higher than peers due to its larger market presence and better profit margins. This valuation suggests a 17% upside potential.

For further details see:

Diageo: Growth Should Continue Just Like It Did Historically