DGEAF - Diageo: Promising Scotch Development But Near-Term Challenges

2023-06-25 22:30:31 ET

Summary

- The company expects a US industry slowdown and destocking to persist, but we see a potential recovery in the Asia-Pacific region.

- Diageo's Scotch business is showing solid results, particularly in Latin America, while the company remains cautious about near-term US performance.

- Compelling valuation versus Campari. We believe this is a reasonable entry price for an economic moat business.

Following our recent release on Davide Campari called " A Pass For Now ," we deep-dived into the beverage alcohol sector and decided to move on with Diageo plc ([[DEO]], [[DGEAF]]) analysis. The company is a worldwide distributor and manufacturer of drinks. Diageo engages its activities in the beverage alcohol industry with a collection of brands (more than 200) across beer and spirits. Diageo's leading brands include Tanqueray, Johnnie Walker, Guinness, Smirnoff, and Baileys, among others (Fig 1). Before going deeper into the analysis, we should say that consumer staple stocks may present a good opportunity for entry after the recent move. In recent months, the segment has been sold in favor of more aggressive choices. This opens up entry opportunities at more reasonable prices.

{kind=link}

Diageo main brands

Source: Diageo corporate website - Fig 1

The company is going through a period of internal transformation. First, Diageo decided to delist its ordinary shares on Euronext Paris and Euronext Dublin. The reasons? Lower trading volumes, higher trading costs, and more administrative obligations resulted from the status of being listed on the two stock exchanges. The company specified that it would remain among the blue chips of the London and Wall Street Stock Exchange. Secondly, there was the recent death of Ivan Menezes , Diageo's CEO for over ten years with 25 years in the company, and Debra Crew was appointed as the new head (in early June). In addition, Diageo also presented to the investor community an update on its Scotch portfolio, which is the company's largest category of brands .

Upside: premiumization, scale, and new markets

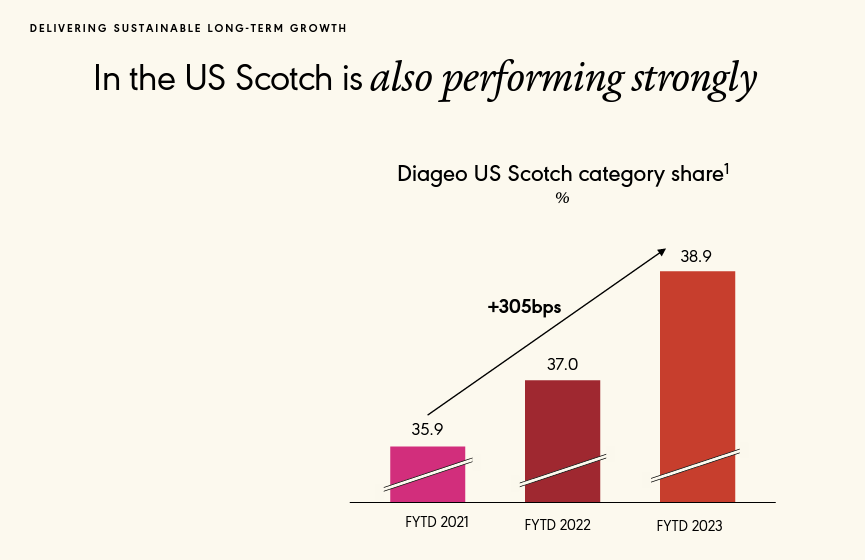

Starting with the Scotch Portfolio update, this was the first event hosted by Debra Crew. Diageo's scotch business equals approximately 25% of the company's top-line sales and represents 50% of the company's US core operating profit. This is why this event was very felt by the investor community. The management remains confident in the category, and the company's latest update shows solid results in the LatAm region. However, the US business is the near-term focus, and Scotch performed poorly until April. Thanks to the latest Nielsen data, the category has been back to growth in May to a mid-single-digit rate, and we expect a further normalization in H2. Here at the Lab, we believe that the stock's recent de-rating already reflects this negative development. As a reminder, Diageo's Scotch division has increased at a 9% CAGR in recent years, thanks also to solid volume growth (4%). This performance was recorded thanks also to India and LatAm evolution. Our internal team views this event as an attempt to broaden Diageo's equity story beyond the US, given that Scotch's business is accretive to margins. Despite that, Diageo's US fundamentals remain strong, and moving on with the Tequila analysis, we should report that several incumbents are entering the market, but the company is currently holding market share.

{kind=link}

Diageo in the US

Source: Diageo latest PPT called " Our Vibrant Scotch Portfolio "

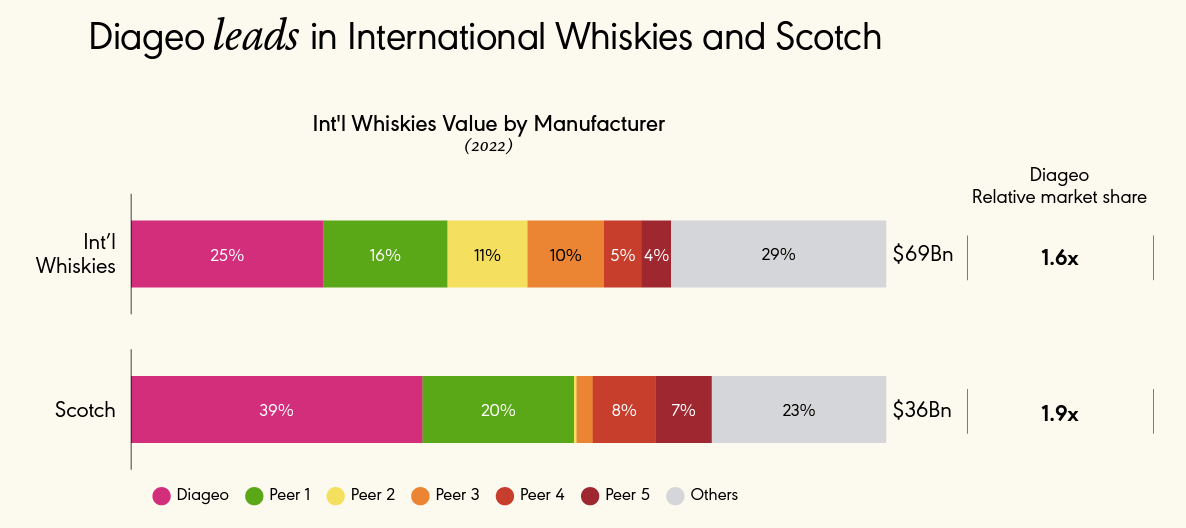

According to the latest presentation, the company held a 25% market share in the international whiskies market and outperformed its closest peers with a 1.6 ratio. Moreover, Diageo accounted for 39% of the global scotch market, with a market share of 1.9x larger than the next player.

{kind=link}

Diageo vs comps

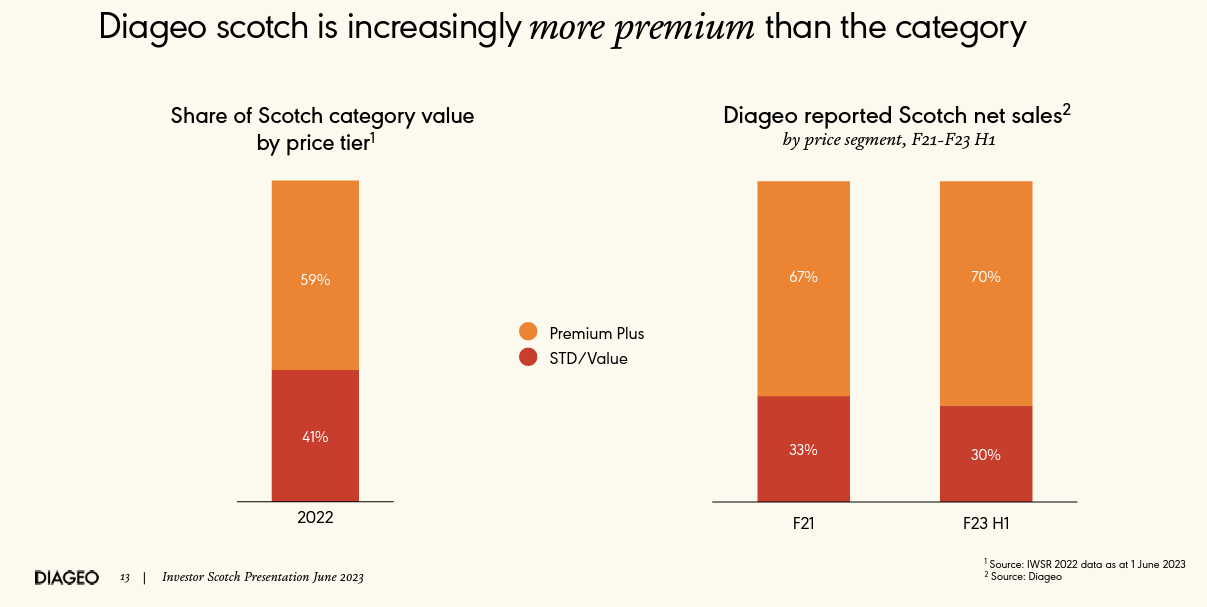

On the other hand, spirits are taking market share, and the category is still in the premiumization phase. Consistent with its closest peers, the CEO is confident about the category returning to mid-single-digit revenue growth. In H1, 70% of Scotch sales were due to a premium portfolio compared to the 67% recorded in the fiscal year 2021. Investment in the segment supply infrastructure will enable the company to enhance its margin. Diageo is also investing in Scotch tourism with distillery visitor centers across Scotland.

{kind=link}

Diageo Scotch premium evolution

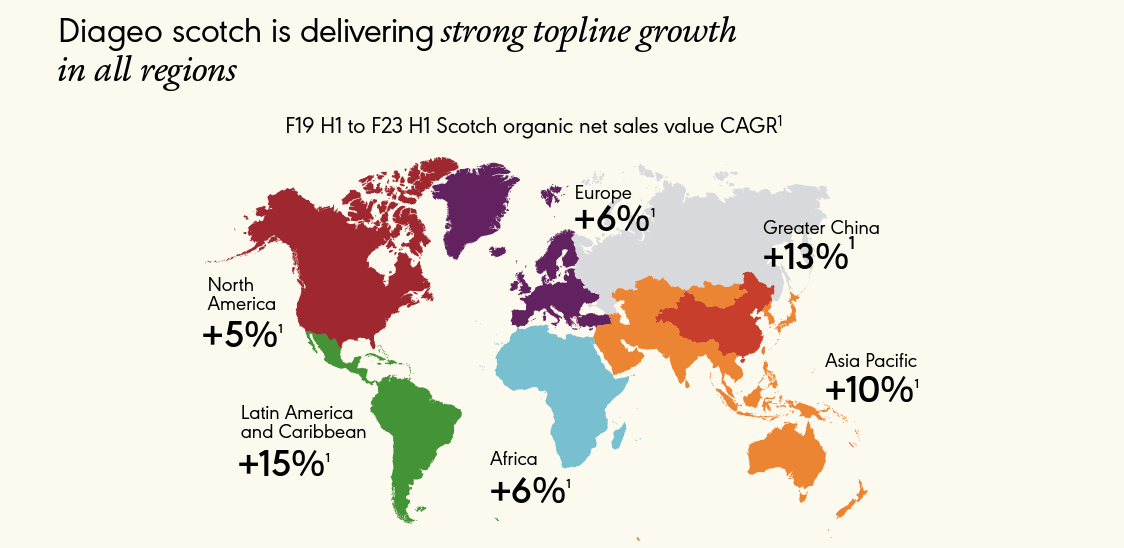

We see a greater emphasis on recruiting new consumers in Emerging Markets. Diageo has the marketing ability to increase market share penetration through innovation, expanding serving rituals, and tapping into unique occasions. China's re-start from the COVID-19 lockdown might offset US weaknesses. The recent Chinese destocking paves the way for a solid business recovery which we estimated for H2. Looking at the APAC, India recorded a reliable performance, with Diageo's business up by 11% and 18% in the premium category. Related to the LatAm area (including the Caribbean), there are more than 340 million potential clients above legal purchase age compared to 160 million in the US. This already represents 33% of the total Diageo Scotch division and is estimated to grow significantly. We are unsurprised to see a plus 15% in top-line sales, outperforming all the other regions.

{kind=link}

Diageo Scotch evolution per GEO area

Conclusion and Valuation

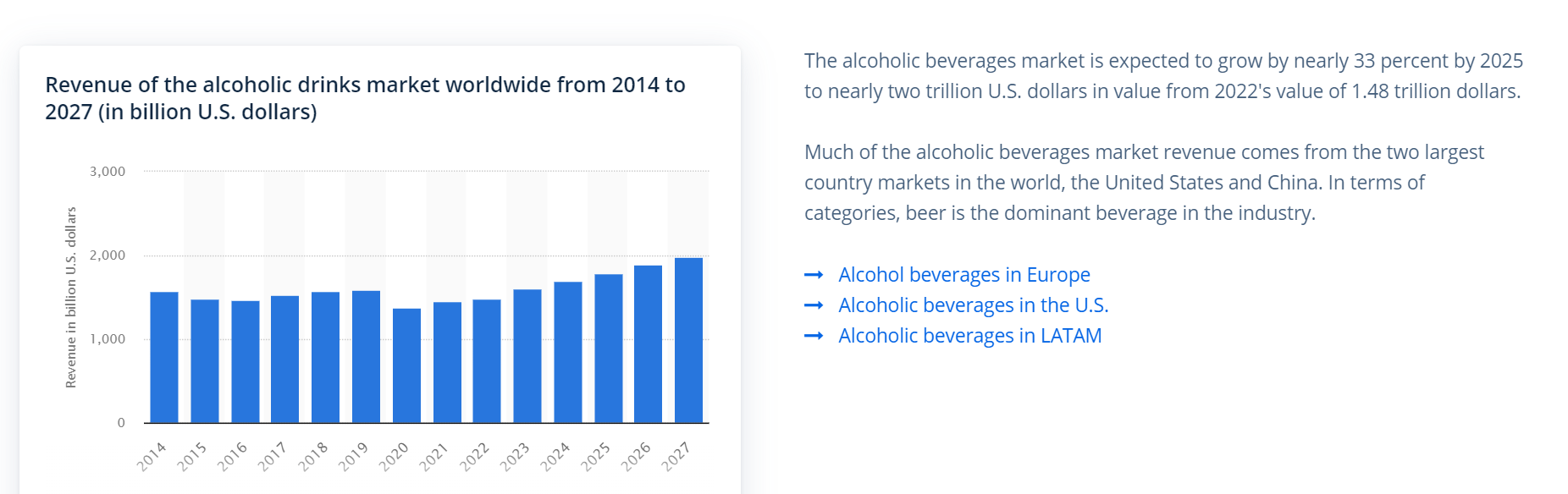

In 2022, the total beverage alcohol market was estimated to be $1.4 trillion (Fig below). Here at the Lab, given Diageo's scale and ability to increase the selling price, we believe the company will increase its fiscal year 2024 group organic revenue and core operating profit by 6.2% and 7.5%, respectively, and we are at a consensus mid-point. According to IWRS , the Scotch category is one of the growing areas expected to grow at a 5% volume per year. With premiumization and an international footprint, we believe Diageo will (once again) outperform the market. As already mentioned, we think that US weaknesses are already well reflected in de-rating, and the company has underperformed the European staples by approximately 12% year-to-date. Our internal team does not forecast significant risks to the company's organic operating profit thanks to an upside in the APAC region. Valuing the company with a historical price earning of 20.5x, we derive a price target of £38.50 with a clear buy rating. Having recently analyzed Davide Campari , we believe Diageo offers more capital upside appreciation, including a higher dividend per share (2.35% vs 0.49%). Currently, Campari is trading at a 45% premium compared to large-cap spirit companies such as Pernod and Diageo. We believe such discount is not justified. Downside risks include a slower recovery in China, a slowdown in Europe and the US, regulatory risks, and a sterling FX appreciation.

{kind=link}

Alcoholic Beverages market value evolution

Source: Statista

For further details see:

Diageo: Promising Scotch Development, But Near-Term Challenges