DGEAF - Diageo Stock: Finally A Buy Now After The Sharp Drop

2023-11-14 00:39:28 ET

Summary

- Diageo shares fell sharply after management revised its guidance for the first half of fiscal 2024 due to a materially weaker expected performance in its Latin America and Caribbean segment.

- In this update, I discuss my views on the bad news, taking into account management's comments made during Friday's Q&A session.

- I will also touch on the potential impact of the conflict in Israel and explain why I was somewhat disappointed by management's comments in relation to the North America segment.

- I will also briefly discuss Berkshire Hathaway's stake in DEO stock, which was established sometime in the first quarter of 2023 and has not been increased since.

- Finally, I will give a brief valuation update and share whether I have increased my position following Friday's drop in the share price.

Introduction

The stock of U.K.-based alcoholic beverage company Diageo plc ( DEO , DGEAF ) fell sharply on Friday, November 10, after the company issued a trading update revising its guidance for the first half of fiscal 2024 (ending December 31, 2023) due to significantly weaker than expected performance in its Latin America and Caribbean ((LAC)) segment.

I first covered Diageo stock in February 2022 and compared it to Brown-Forman Corp. ( BF.A , BF.B ) and Constellation Brands, Inc. ( STZ ) in January and March 2023 , respectively. While Diageo is undoubtedly a strong company with a well-rounded brand portfolio (e.g. Johnnie Walker, Oban, Talisker, Singleton, Lagavulin, J&B, Guinness), I found the stock too expensive to justify adding to the position I had accumulated in the midst of the pandemic in 2020.

In this update, I will provide my views on Diageo's trading update, including management's prepared remarks and the analyst Q&A . Given the stock is now trading close to its pandemic low of approximately £25, I share whether I consider it a buy now after the drop or still too expensive amid the current challenges. I will also briefly discuss Berkshire Hathaway's ( BRK.A , BRK.B ) stake in Diageo, which was established sometime in the first quarter of 2023 and has not been increased since then.

What To Make Of The Weak Performance In Latin America

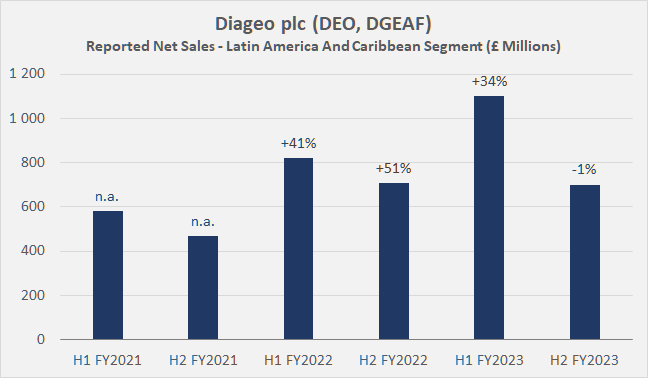

Diageo recorded a particularly strong performance in its Latin America and Caribbean segment in fiscal 2023 (ended June 30, 2023), with actual and organic sales growth of 18% and 9%, respectively. The segment was responsible for 10.5% of fiscal 2023 consolidated net sales. However, what looks like a very strong performance is in fact only the result of price increases, as the segment's volume actually decreased by 0.9%, both on an actual and organic basis.

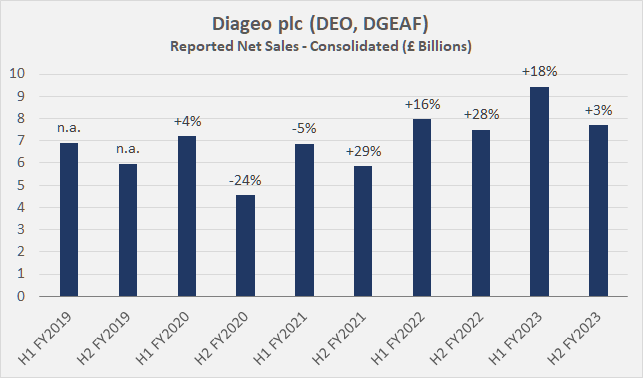

Admittedly, the comparison with the first half of fiscal 2023 (organic volume and sales growth of 6% and 20%, respectively, and reported net sales growth of 34%, Figure 1) is a difficult one. However, it is nonetheless quite surprising that organic sales are expected to decline by more than 20% in the first half of fiscal 2024, as the already weak performance in the second half of fiscal 2023 could have pointed to pent-up demand. By comparison: in previous years, sales in the first half of the year were around 20% higher than in the second half due to seasonal factors, while sales in the first half of fiscal 2023 were a whopping 57% higher than in the second half.

Figure 1: Diageo plc (DEO, DGEAF): Latin America And Caribbean segment sales (own work, based on company reports)

{kind=link}

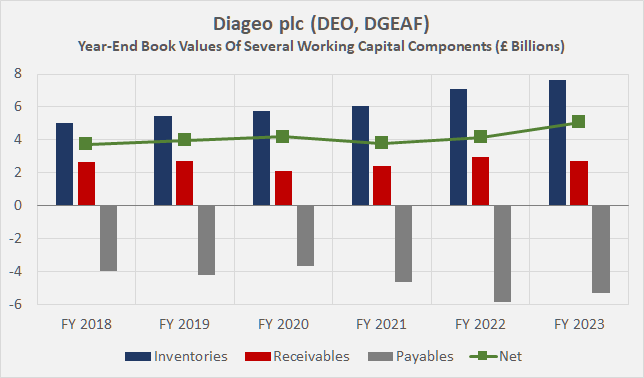

In addition to the difficult comparison, the sharp decline in Diageo's LAC segment is due to unfavorable inventory movements (Figure 2), weaker-than-expected economic activity, and a weak consumer (lower disposable income). Diageo is seeing consumer downtrading, which points to the successful premiumization of its brand portfolio on the one hand, but also to weaker diversification from a pricing perspective, making the company's sales more cyclical. However, management pointed out in its remarks that the company continues to gain market share in most markets, with Mexico being a notable exception, where Diageo is facing pronounced difficulties due to its spirits-focused portfolio. Mexico, which already recorded a 4% decline in volume in fiscal 2023, is responsible for more than 25% of the LAC segment's sales, which corresponds to around 2.7% of consolidated net sales.

Figure 2: Diageo plc (DEO, DGEAF): Trade receivables, inventories, trade payables and their net effect at year-end (own work, based on company reports)

{kind=link}

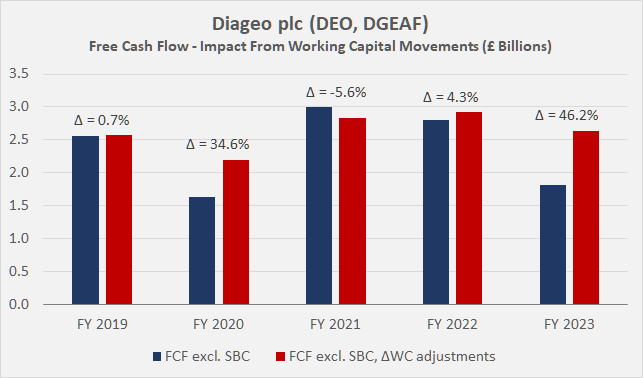

As management acknowledged during the conference call (but to some extent this was already expected), the inventory overhang led to a weaker price trend to facilitate destocking. However, as we have seen with several other companies suffering from excess inventory after the pandemic, this is a temporary effect. That said, free cash flow was already significantly impacted in fiscal 2023 (note the difference in Figure 3), and due to the necessary destocking, I expect a disappointing result for fiscal 2024 as well. It's worth keeping in mind inventory markdowns, meaning that the expected decline from the book value of inventories at the end of fiscal 2023 does not necessarily translate directly into free cash flow.

Figure 3: Diageo plc (DEO, DGEAF): Free cash flow excluding stock-based compensation, before and after having adjusted for working-capital movements on a three-year rolling average basis (own work, based on company reports)

{kind=link}

However, returning to the difficult comparison, investors should ask themselves why Diageo's LAC segment performed so strongly in the first half of fiscal 2023, leading to relative weakness in the second half of the year and, as we learned on Friday, also in the first half of fiscal 2024. I think it is reasonable to expect that consumers in Latin America have been stocking up out of fear of continued high inflation (due in part to the political environment) and possibly also in anticipation of disproportionate price increases due to the known weakness of local currencies.

Against the backdrop of fairly obvious consumer restocking efforts in the first half of fiscal 2023, I think the company's poor inventory management is particularly noteworthy.

Management claims that it has far less insight into stock held by wholesalers and retailers than it does into stock held by distributors. This is of course understandable when considering that Diageo is largely pursuing a sell-out strategy, meaning that their marketing strategy is focused on their distribution partners and not directly on the end consumer.

However, I don't think that absolves them from keeping a very close eye on consumer trends. But that what's CEO Debra Crew's comment suggests: " it was just difficult to see what part was going on was true consumption growth versus inventory increases " (p. 4 of the transcript), and indeed management admitted that the channels below the distributors have purchased ahead of consumption.

I don't want to be misunderstood as oversimplifying Diageo's business and I recognize the highly volatile environment. However, the scale of sales and volume growth in the first half of fiscal 2023 (LAC was the only segment to report volume growth, and a strong one at that, p. 3, trading update ) in an already difficult year for the consumer should have told management that a one-off uplift effect must have played a big part. In this context, the organic volume growth of 13% in Brazil in the first half of fiscal 2023 compared to a volume decline of 1% for the full year is particularly noteworthy.

Can Diageo's Other Segments More Than Compensate For The Decline In LAC Sales?

While the sharp decline in net sales in the first half of fiscal 2024 is of course very disappointing, it seems worth noting that Diageo's management remains quite optimistic about the business as a whole - especially in the longer term.

In the short term, Diageo is facing difficulties not only in Latin America but understandably also in the Middle East, where trading has been suspended in key regions. However, investors should not over-interpret the (hopefully brief) trading halt due to the conflict in Israel, as the sub-segment is responsible for less than 10% of the Asia Pacific segment, which itself contributed 18.7% of Diageo's net sales in fiscal 2023. In addition, the Middle East sub-segment includes travel-related sales for the entire Asia region and it is therefore reasonable to conclude that the impact is likely to be well below 1% of consolidated net sales.

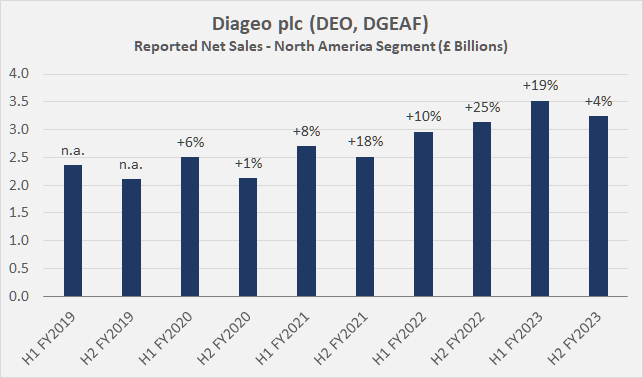

Diageo's North America segment shows a sequential improvement and, given its significance (39.5% of net sales in fiscal 2023), obviously helps to offset the weak performance of the LAC segment. However, looking at Figure 4, we can clearly see a seasonal pattern (with the exception of fiscal 2022), so sequential improvement does not appear to be anything out of the ordinary, and one wonders why management is emphasizing this. Given that Diageo's North America segment reported organic sales growth of 3% in the first half of the year (on a 4% volume decline) and flat sales for the full year on an accelerated volume decline (-5%), the expected sequential improvement for H1 of fiscal 2024 is not really a highlight in my view - after all, the comparison is quite an easy one.

Figure 4: Diageo plc (DEO, DGEAF): North America segment net sales (own work, based on company reports)

{kind=link}

However, management is probably highlighting this development positively due to the aforementioned inventory issues that are not only impacting the Latin America and Caribbean segment, and the readings for disposable income per capita (somewhat weaker in recent months) and consumer confidence (a weakening trend) are also not too positive. With regard to the outlook for the full year, management noted that the North America segment will definitely fall short of the company's medium-term growth forecast for sales and operating profit of 5-7% annually.

Against this backdrop - and this also applies to Diageo's Europe segment (21% of net sales in fiscal 2023) - the company sees pricing pressure easing, which should benefit performance in the second half of the financial year. Added to this is the fact that price increases were implemented at the beginning of 2023, so consumers are likely to have become accustomed to the adjusted level by now, in what is clearly the more important half of the year for the company due to the holiday season.

All in all, management now expects the first half of fiscal 2024 to be weaker or in line with the second half of fiscal 2023 (Figure 5), which is of course disappointing given the importance of the period and the inability of Diageo's other segments to offset the current weakness in the LAC segment. To be fair, however, investors should bear in mind that this is a challenging environment and that the recovery in China is also somewhat slower than anticipated. However, management expects a gradual improvement in the second half of the financial year, both in terms of sales and operating profit, given the difficult inventory situation. The long-term growth expectation for sales and operating profit of 5 to 7% annually has also been maintained. This does not seem to be an unrealistic expectation, considering that Diageo's global market share for alcoholic beverages is still only 4.7%.

Figure 5: Diageo plc (DEO, DGEAF): Consolidated net sales (own work, based on company reports)

{kind=link}

What To Make Of Warren Buffett's Position In Diageo?

In its Q1 13F-HR filing , Berkshire Hathaway reported ownership of 227,750 Diageo American Depositary Receipts, representing 911,000 ordinary shares ( 4:1 ADRs ), worth approximately $32.4 million at the time of writing. At the end of the second quarter of 2023 , Berkshire still held 227,750 ADRs.

This is, of course, a tiny position in Berkshire's portfolio, which currently generates $736m in annual pre-tax cash flow from its investment in The Coca-Cola Company ( KO ) (ownership of 400 million shares). Put another way, the size of Berkshire's Diageo position represents just 4.4% (!) of the annual dividend income derived from its position in Coca-Cola. Of course, the position is insignificant not only from this perspective but also in comparison to the $152 billion in cash, cash equivalents and short-term investments in U.S. Treasury Bills reported at the end of the third quarter of 2023 .

However, I would not completely ignore the position and keep an eye on Berkshire's Q3 13F-HR filing, which is expected in the next few days. Diageo shares performed rather poorly in Q3 and were trading well below the average price in Q1 2023 when Berkshire opened the position. Therefore, I wouldn't rule out Buffett and Co. having bought additional ADRs provided their view on the investment hasn't changed in the meantime. Such news could have a significant positive impact on the sentiment surrounding Diageo stock.

However, since the sharp drop was already in the fourth quarter, we will have to wait until February 2024 before we find out if Buffett (or whoever is responsible for the position) added to his position in reaction to the dip on November 10.

That being said, and while I wouldn't rule out the possibility that Berkshire increased its stake in Diageo, it's also worth keeping an eye on the comparatively low trading volume of currently around 530,000 ADRs per day (2.12 million ordinary shares), representing less than 0.1% of the diluted weighted-average shares outstanding at the end of fiscal 2023 (2.271 billion shares).

Conclusion – Is Diageo Stock A Buy Now After The Drop?

Diageo reported sobering news in relation to its Latin America and Caribbean segment, which is now expected to report an organic sales decline of more than 20% in the first half of fiscal 2024. Admittedly, the comparison with the strong first half of fiscal 2023 is difficult, but a closer look reveals that a significant part of the strong performance in this period was due to consumers stocking up on fears of further sharp price increases, the political situation in some countries and, of course, the use of high-quality spirits as a kind of hedge against currency devaluation.

Diageo's management apparently misinterpreted the anticipated demand and consequently greatly overestimated demand for the current period. This is largely due to Diageo practicing sell-out strategies, resulting in rather poor visibility on consumer-facing distribution channels. However, in my view, this is not an adequate excuse and I really hope that management improves its inventory planning, particularly in this segment, and improves communication and the quality of feedback with its distributors, the channels below its distributors, and between wholesales/retailers and distributors.

In addition to the poor outlook in the LAC segment, Diageo is also experiencing a weaker-than-expected recovery in China and is, of course, affected by the de facto trade halt in connection with the conflict in Israel. However, the impact of the latter conflict is - for the time being - insignificant in my view. All in all, the results for the first half of fiscal 2024 will likely be lower than in the second half of fiscal 2023, which is naturally disappointing given the seasonal nature of the business and the importance of the holiday season.

Longer term, however, management remains confident of returning to organic sales growth of 5% to 7% and, thanks to ongoing supply chain improvements, operating income (and also cash flow, see my previous articles on Diageo's excess cash margin) should grow at a similar rate.

Personally, I think the drop in share price is somewhat justified given the misinterpretation of local developments in Mexico and South America and the resulting poor inventory management. At the same time, I was disappointed with the way management communicated the sequential improvement in the North America segment (knowing the seasonality).

All that being said, I own Diageo for its strong brands, good profitability, and solid growth prospects (despite the short-term challenges). It is a stock that I believe warrants a premium valuation, albeit a modest one given the relatively low long-term average growth (5% adjusted earnings and free cash flow). Based on earnings per share for fiscal 2023 (165p), the stock currently trades (share price of £28.88 or $142.5 per ADR) at a price-to-earnings ratio of 17.5 - not bad compared to the historical average valuation . Similarly, a free cash flow yield of 4.3% strikes me as acceptable, but still a long way from what I would call deep value. And therein lies the issue - a stock like Diageo rarely, if ever, trades at rock-bottom valuations. Even in the midst of the pandemic - when Diageo's business model was obviously significantly impacted - the shares were still changing hands at a pretty solid valuation (P/E ratio of 19, based on fiscal 2019 EPS).

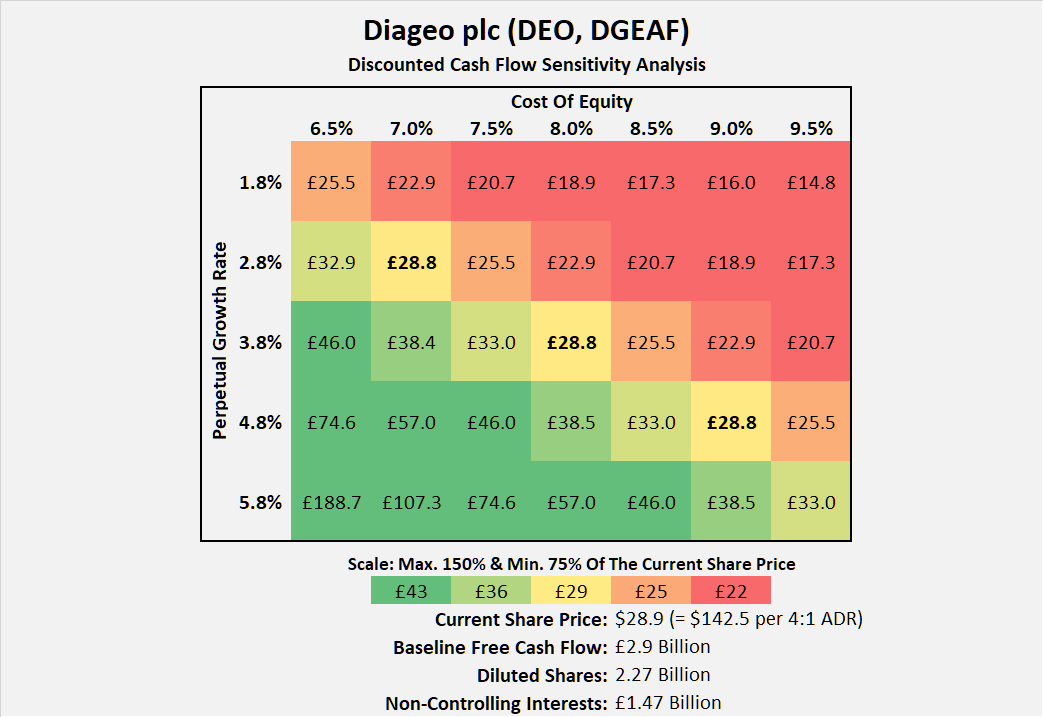

According to the discounted cash flow sensitivity analysis in Figure 6, DEO shares are currently approximately fairly valued at a cost of equity of 8.0% and a perpetual growth rate of 3.8%. Of course, caution is warranted with such high perpetual growth rates, especially given that Diageo's long-term growth rate has only been around 5% in a relatively low inflation environment. However, given its still small market share and strong brand portfolio with pricing power, I believe such growth is achievable. That said, with a company like Diageo that grows through acquisitions, it is always important to keep an eye on organic growth and the balance sheet.

Figure 6: Diageo plc (DEO, DGEAF): Discounted cash flow sensitivity analysis (own work, based on company reports and own calculations)

{kind=link}

Until recently, I still held a fairly modest position in Diageo's ordinary shares, which accounted for around 0.85% of my total portfolio value. For this reason, and because I currently consider the stock to be fairly valued, I have increased my position to 1.0% after the precipitous drop. I continue to monitor the company and expect to gain further insights from the upcoming 2023 Capital Markets Event , which will take place tomorrow, Wednesday, November 15. Depending on further developments and the share price performance, I can imagine increasing my position to a maximum of 1.5% of my portfolio value.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Diageo Stock: Finally A Buy Now After The Sharp Drop