DEO - Diageo Stock: Good Business But Outside The Buy Zone

2023-07-24 23:31:16 ET

Summary

- Diageo, a global leader in the alcoholic drinks industry underpinned by prominent brands.

- The firm operates in a fragmented market, enabling the company to grow through acquisitions.

- I assign a hold because my current valuation suggests the company is currently fairly valued.

Thesis

Diageo ( DEO ) is a leading premium drinks company underpinned by high-quality and well-known brands. The firm operates in a resilient and growing market with high barriers to entry. I believe DEO benefits from strong pricing power and a cost advantage as a result of its intangible assets. In my opinion, These two factors will serve the company as long-term tailwinds for margin enhancement. I assign a hold because the stock seems fairly valued. I will explain my thesis's key points below.

Company Overview

Diageo was created in 1997 following a merger between Grand Metropolitan and Guinness. With over 200 brands and sales in 180 countries, the firm is a prominent leader in the beverage alcohol industry with an outstanding collection of brands across spirits and beer. The company owns brands such as Johnnie Walker, Tanqueray, Smirnoff, Guinness, Bailey's, and more. Its portfolio includes tequila, gin, Cognac, Liqueurs, Rum, Vodka, and more. In 2022, 81% of sales came from spirits, 14% from beer, and 5% from ready-to-drink beverages.

39% of revenue is derived from N.A., 21% from Europe, 19% from Asia, 11% from Africa, and 10% from Latin America. Diageo owns 34% of Moet Hennessy, a subsidiary of LVMH Moet Hennessy-Louis Vuitton, and almost 56% of India's United Spirits. According to the company's website , they have the best-selling Scotch whiskey brand in the world (Johnnie Walker).

As I said in my thesis, I believe the company has pricing power due to its intangible assets. In 2021, DEO posted organic growth of 16% and 21.6% in 2022. The firm has said that 58% of organic growth over the past two years came from price/mix, resulting in annual growth of 11%, which is way above the inflation rate (average global inflation over the past two years stood at 6.7%). Regardless of the price increases, Organic volume growth was up by 10% in 2022. Revenue also grew by 21%, reaching an all-time high. This is significant because, despite the price hikes, consumers are still buying the company's products, demonstrating the strength of their brands.

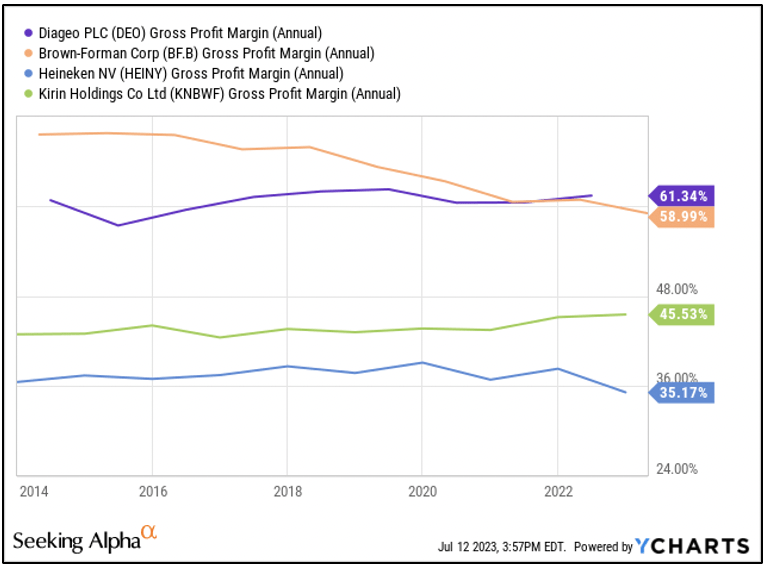

Being the #1 player in the spirits market with a 27% global volume market share DEO benefits from a cost advantage. What I mean by that is that the company can negotiate a low price point for the materials needed for its products, such as grapes, barley, and other things. This allows the firm to have access to the same materials as competitors but at a much lower price, which will help DEO make its goods at a much lower cost than its peers. As a result of the company's pricing power and cost advantage. DEO's gross margin has outperformed its peers and sector. The sector median is 31%, and DEO's is almost double that. These two elements, I believe, will serve as long-term tailwinds for margin expansion.

{kind=link}

Market Overview

The alcoholic drinks market is highly regulated and isn't very easy to penetrate because it requires a lot of capital to build your brand, find distribution channels, and create trust with the consumer. Unlike other consumer products, it's hard to sell alcoholic drinks online because of age verification. This is important because e-commerce has made it easy for new companies to disrupt other markets. In the U.S., 3.5% of alcoholic drink sales were made online. I believe all of these elements enable the alcoholic drinks market to have high barriers to entry.

Historically, the alcoholic drinks market has outperformed its peers because of rising demand, status, strong pricing power, and being less exposed to the macroeconomic environment. According to Statista, the alcoholic drinks market is expected to grow at an annual rate of 5.42% from 2023 to 2027. Beer accounts for most of the market's revenue (38%).

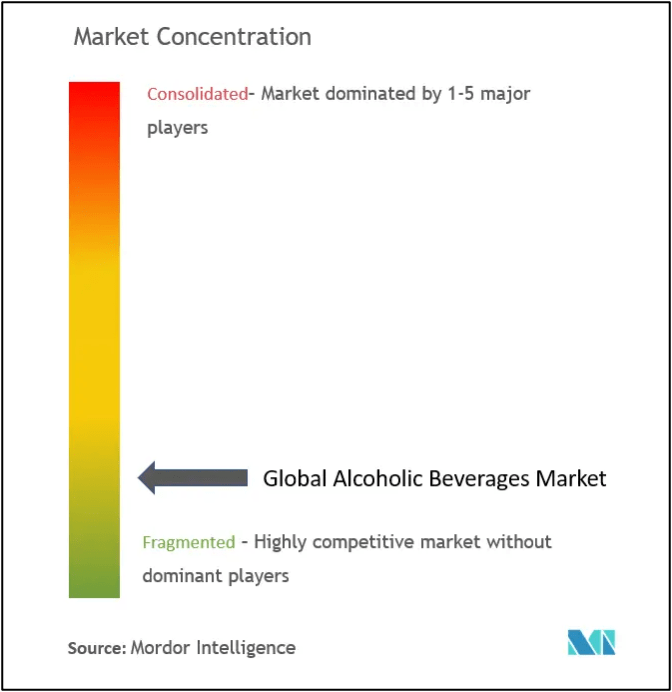

The alcoholic beverage market is also highly fragmented . This presents dominant companies such as DEO with M&A opportunities. With more than 20 acquisitions, The firm has a history of creating value through acquisitions, enabling them to be one of the top five firms in the industry.

{kind=link}

Valuation

DEO is currently trading at a FWD P/E ratio of 22.07x and an EV/EBITDA ratio of 16.08x. I forecast revenue to compound at an annual growth rate of 6.61% from 2023 to 2027 due to price increases, industry growth, and future M&As. Perhaps price increases won't be at the same pace as for the past two years because inflation isn't climbing at the same pace it did post-pandemic, but as I said before, I believe cost advantage and pricing power will serve as long-term tailwinds for margin expansion. Using a discount rate of 7.5%, I discounted the future cash flows and Terminal value. I arrived at an equity value of $100 billion, which translates to a value of $180 per share, representing a 1% upside. I assign a hold because my current valuation suggests the company is fairly valued at $177 a share.

Risks

Competition is another risk. The alcoholic beverage industry is highly fragmented. Just as this offers DEO M&A opportunities, the same opportunities are available to competitors. So far, the company's acquisition strategy has helped them create value, and I don't think that will change anytime soon.

Regulation can serve as a double-edged sword for the alcoholic drinks industry as a whole, not just DEO. Out of all alcoholic drinks, distilled spirits have the highest tax rate. Considering that 80% of DEO's revenue is derived from spirits, Future changes to how much tax is charged on alcoholic drinks can further dilute the company's profits. Over the past three years, DEO has averaged a tax rate of 25%.

Takeaway

In conclusion, DEO is a global leader in a substantial and growing market. The company's high-quality brands have helped them benefit from strong pricing power and a cost advantage. These factors have helped the firm maintain above-average gross margins, and I don't expect that to stop. The firm's industry offers a lot of M&A opportunities, and with DEO's disciplined acquisition strategy, I expect them to take full advantage of the opportunity. I assign a hold because the current valuation of $177 seems fair

For further details see:

Diageo Stock: Good Business But Outside The Buy Zone