DGEAF - Diageo Vs. Constellation Brands - One Is The Better Dividend Stock (With A Caveat)

2023-03-24 10:26:30 ET

Summary

- Diageo and Constellation Brands share a lot of similarities but are still quite different companies. The article gives a good overview of their business models.

- Diageo does a great job of maintaining its top position through strong marketing spend. Constellation's management delivers surprisingly strong performance in an otherwise difficult segment thanks to its important niche.

- Both show disciplined growth through acquisitions, but Diageo's approach strikes me as more promising in the long run. Still, Constellation's management may have a surprise or two up its sleeve.

- Besides a discussion of their business models, the article compares past growth, future prospects, profitability, balance sheet quality, and the suitability of STZ and DEO/DGEAF as dividend investments.

- A discounted cash flow and earnings-based valuation are also included.

Introduction

In times of increased volatility and growing perceived uncertainty of bank deposits, it is quite understandable that many would want to put part of their savings in a "bank" that covers its liabilities (in the sense of deposits) with assets other than loans or equity and bond investments. While I don't question the systemic importance of our financial system, I do think that investing in companies that manufacture everyday products has its own appeal. Granted, invested money should never be confused with an emergency fund or other short-term cash needs, but I think it's important to recognize that excess cash is best invested in productive capital over the long term. Of course, in a diversified portfolio, it may make sense to invest in common stocks of banks - after all, banks are an integral part of our economy - but the bulk of personal wealth, in my opinion, is best invested in stocks of largely non-cyclical or moderately cyclical companies such as consumer staples or health care firms.

My regular readers probably remember my January 2022 comparative analysis of the world's largest Scotch whiskey company Diageo plc ( DEO , DGEAF ) with the company behind the world-famous Jack Daniels Tennessee whiskey - Brown-Forman Corporation ( BF.A , BF.B ). In this article, I want to take a look at another U.S.-based player in the alcoholic beverage market and compare it with my all-time favorite Diageo - Constellation Brands Inc. ( STZ ). The company caught my attention because of its strong performance in an otherwise difficult segment thanks to its important niche, and because it is still largely family-owned and quite conservatively managed.

A Comparison Of The Business Models Of Diageo And Constellation Brands

I will only very briefly discuss Diageo's business, as I have already covered it in the abovementioned article and a company-specific analysis in early 2022. Diageo has an estimated market share of almost 40% in the Scotch whisky segment and owns brands such as Johnnie Walker, Oban, Talisker, Singleton, Lagavulin, J&B, and Bell's. The company also owns Guinness, the world's leading Irish stout brand, as well as several rum, gin, vodka and mezcal brands. However, Diageo should not be viewed as a spirits-only company, as it is also leveraging its brand strength by offering increasingly popular ready-to-drink versions of some of its brands.

Constellation Brands is much more focused on beer and wine, which accounted for nearly 77% and 21% of net sales in fiscal 2022, respectively. In addition, Constellation Brands operates almost exclusively in the U.S. (>97% of net sales in fiscal 2022). In contrast, Diageo generated only about 40% of its fiscal 2022 net sales in the United States. This of course has advantages such as simpler operations, better predictability and almost no currency risk, but also disadvantages such as limited growth prospects (Diageo is growing strongly in Asia and has the ability to leverage regional trends)

Diageo has always had a focus on premium brands, while Constellation Brands is premiumizing its portfolio by divesting low-margin businesses and acquiring premium brands. Already the leading player in the U.S. imported Mexican beer market, Constellation Brands owns exclusive U.S. import, marketing and distribution rights for Corona, Modelo, Pacifico and Victoria (p. 3, fiscal 2022 10-K ). Corona Hard Seltzer and Corona Refresca, as well as Modelo's Chelada variants , enable the company to capitalize on the increasingly important trend toward low-alcohol mix drinks and beer-based beverages with unique ingredient compositions. In total, nine of the top 15 U.S. import beer brands trace back to Constellation, through which the company continues to benefit from the entrenchment of the Hispanics/Latinos demography in the United States. In partnership with The Coca-Cola Company ( KO ), STZ launched mixed drinks under the FRESCA Mixed brand (e.g., RTD vodka spritz and tequila-paloma cocktails).

Constellation Brands is a largely U.S.- and beer-focused company. However, the company also owns wine brands such as 7 Moons, Meiomi, Kim Crawford, Ruffino, Crafters Union, Cooper & Thief, and Cook's California Champagne. It also owns tequila, whiskey, brandy and vodka brands (e.g., Casa Noble, High West, Mi CAMPO, Nelson's Green Brier, SVEDKA and Cooper & Kings), but with only around 2% contribution to net sales, the segment is still very small. In 2021, the company divested lower-margin, lower-growth wine and spirits businesses for approximately $540 million plus a possible additional $250 million in contingent consideration. Also in 2021, STZ acquired the remaining interest in My Favorite Neighbor, a company focused on direct-to-consumer ((DTC)) sales of premium wines. The company's growing focus on DTC is further highlighted by the acquisition of Empathy Wines in 2020. In spirits, Constellation acquired the remaining ownership interest in Cooper & Kings in 2020. A complete summary of the company's acquisitions and divestitures can be found on page 74 et seq. in the fiscal 2022 10-K . Recently, STZ announced the divestitures of Cooper & Thief, Crafters Union, The Dreaming Tree, Monkey Bay, 7 Moons and Charles Smith Wines. Constellation Brands also holds a 36.1% stake in Canadian cannabis company Canopy Growth Corp ( CGC ). STZ has the right to nominate four board members but does not actively control Canopy's business or operations.

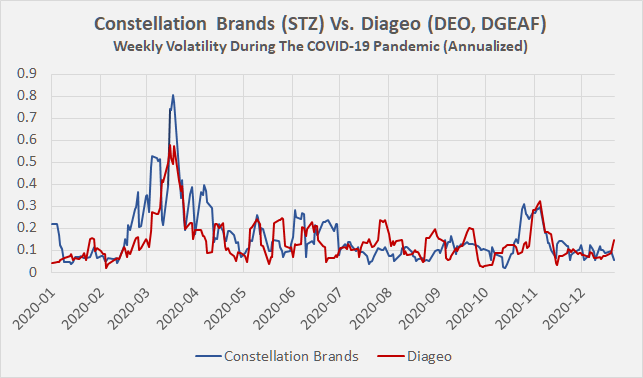

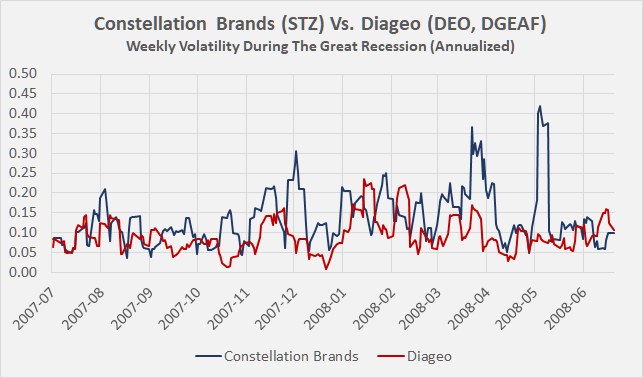

In direct comparison, Constellation Brands is definitely on the right track in terms of premiumizing its portfolio (the company's CAGNY 2023 presentation gives a good overview), but Diageo is obviously a much more mature and more settled company in this context. The U.K.-based business is increasingly leveraging the brand power of its well-rounded portfolio for ready-to-drink cocktails, which are in strong demand among younger consumers. Because of its focus on beer and wine, Constellation has a stronger presence in nightlife venues such as bars and restaurants. This is well illustrated by the comparatively higher volatility of its shares in the early months of the COVID-19 pandemic (Figure 1), but Constellation Brands' stock was also comparatively volatile during the Great Recession (Figure 2).

Figure 1: Volatility of Constellation Brands' stock [STZ] and Diageo's stock [DEO, DGEAF] during the COVID-19 pandemic, computed on the basis of daily LOG returns (own work, based on STZ's and Diageo's daily closing share price in USD and GBP, respectively) Figure 2: Volatility of Constellation Brands' stock [STZ] and Diageo's stock [DEO, DGEAF] during the Great Recession, computed on the basis of daily LOG returns (own work, based on STZ's and Diageo's daily closing share price in USD and GBP, respectively)

{kind=link}

{kind=link}

Growth And Profitability Of Constellation Brands And Diageo

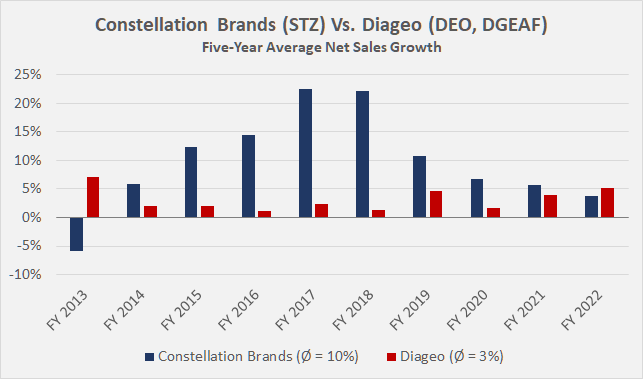

Constellation is only about 40% the size of Diageo ($40 billion vs. $101 billion market cap). Both companies are growing organically and through acquisitions. Goodwill is a rough proxy for how much a company relies on acquisitions - Constellation's goodwill has tripled over the past decade, while Diageo's has increased only 1.7 times (data from fiscal 2012 and 2022 balance sheets). In relative terms, goodwill represents about 30% and 6% of the total assets of STZ and DEO, respectively. It is not difficult to understand that both companies rely heavily on brands - when goodwill, trademarks, and other intangible assets are added together, they represent about 41% and 33% of the two companies' total assets at year-end 2022, respectively. Constellation Brands acquisitions have contributed quite a bit to net sales, as shown in Figure 3, which compares net sales growth based on five-year average data. The same trend can be seen in the two companies' operating profit growth, which has averaged 19% for STZ and 4% for DEO over the past decade, based on rolling five-year average data. The lower net sales growth underscores the maturity of Diageo's portfolio.

Figure 3: Net sales growth of Constellation Brands [STZ] and Diageo [DEO, DGEAF] (own work, based on data supplied by Morningstar)

{kind=link}

Constellation's increasing focus on premium products is also reflected in its margins. While Diageo maintains a very high gross margin of over 60%, Constellation's management has been able to increase this from around 40% to over 50% in recent years. STZ's operating margin has also caught up very well over the years, even surpassing Diageo's profitability in recent years. For a beer-focused company, I think this are phenomenal results. In terms of return on invested capital ((ROIC)), both companies generally (i.e., excluding the pandemic) generate solid returns above their cost of capital. As an aside, online resources such as Morningstar and GuruFocus show a near-zero ROIC for STZ in fiscal 2022, due to an impairment charge related to the suspended Mexicali Brewery construction project.

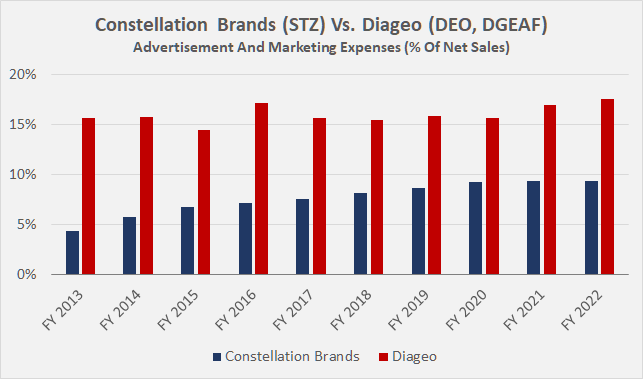

U.K.-based Diageo is spending significantly more on advertising to successfully defend the economic moat of its intangible brand assets (Figure 4). In this context, the increase in advertising spending at STZ confirms the company's growing emphasis on premium products.

Figure 4: Advertisement and marketing expenses of Constellation Brands [STZ] and Diageo [DEO, DGEAF] (own work, based on the companies' fiscal 2013 to fiscal 2022 annual reports)

{kind=link}

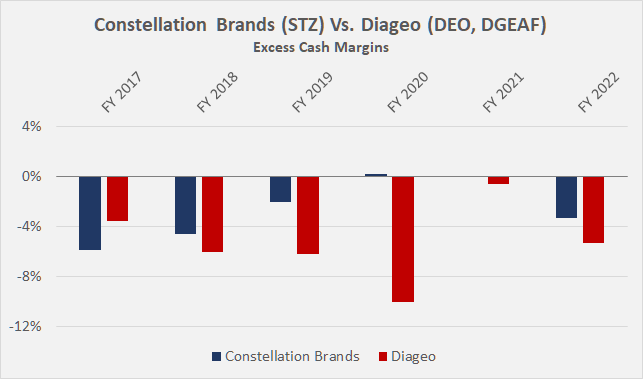

Looking at actual cash earnings, STZ's operational improvement is also evident. Over the last six years, STZ's excess cash margin (ECM, a metric I explain in this article ) has been more stable than Diageo's and typically less negative, meaning STZ has a better cash profitability (leaving capital expenditures aside). While it is important to keep in mind that the companies have different fiscal year ends (Diageo in June, Constellation in February), I don't think that is the reason for the divergence. STZ is considerably smaller than Diageo, and as companies get larger, it generally becomes more difficult to maintain a consistently high level of cash profitability. In any case, STZ's solid performance is a clear sign that management is properly integrating the acquired businesses. Taking capital expenditures into account, both companies typically convert 20% of each dollar/pound of net sales into free cash flow, also taking into account normalization of working capital movements and adjustments for share-based compensation (normalized free cash flow, nFCF). Because of the difference in ECM (Figure 5), one might expect Constellation to have a higher free cash flow margin, but because of their consistently much larger investments in the business (in addition to acquisitions), the two companies are similarly profitable.

Figure 5: Excess cash margins of Constellation Brands [STZ] and Diageo [DEO, DGEAF] (own work, based on the companies' fiscal 2016 to fiscal 2022 annual reports)

{kind=link}

Constellation Brands is quite a bit smaller than Diageo and is at an earlier stage in terms of growth. I like the way management is balancing growth through internal reinvestment in the business and growth through acquisitions. That's not to say Diageo is inferior to Constellation, of course - management is doing a great job of maintaining its top position, and its relentless focus on premium brands is a solid foundation for reliable profitability. However, by buying up relatively small companies and leveraging its own international distribution and marketing capabilities, Diageo also has a very solid growth plan. Going forward, I believe both companies are well positioned. Diageo will benefit from the growing middle class in Asia, while Constellation continues to benefit from the entrenchment of the Hispanics/Latinos demography in the United States through its position as the exclusive distributor of Grupo Modelo S.A. de C.V.'s leading Mexican beer brands. That relationship, however, is why Constellation Brands' beer portfolio will likely remain confined to the U.S., but of course the company may consider expanding into international markets through its wine and spirits business or acquiring other beer brands - with all the pros and cons that entails.

Assessing The Quality Of Diageo's And Constellation Brands' Balance Sheet

Both Diageo and Constellation Brands have, in principle, solid balance sheets. The comparatively high proportion of goodwill at STZ has already been discussed, and as with all companies that grow through acquisitions, a large goodwill position carries the risk of write-downs. While I have already positively highlighted the company's hybrid growth through acquisitions and internal reinvestments, I like the strategy of Diageo's international development of small brands better. Of course, the company's global footprint puts it in an advantageous position.

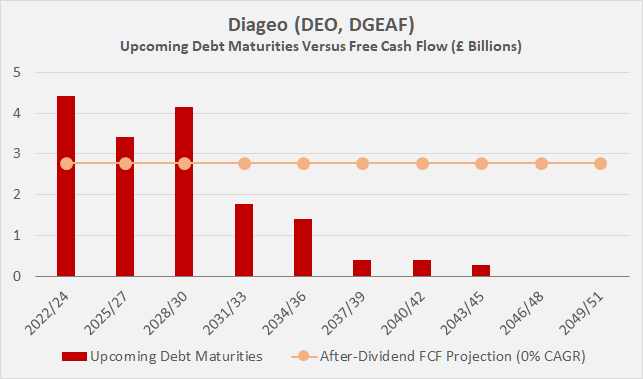

At the end of fiscal 2022 (ended June 30, 2022), Diageo reported net debt of £13.7 billion. This is undoubtedly significant, but should be viewed in the context of the company's relatively low cyclicality. Demand for Diageo's products is relatively constant, but during a severe recession, demand for high-priced alcoholic beverages can of course be expected to decline temporarily. Diageo currently generates normalized free cash flow of around £2.6 billion per year (average for fiscal years 2020 to 2022), which would allow the company to repay all of its outstanding debt in the hypothetical event of a dividend suspension within five to six years. An interest coverage ratio of more than seven times pre-interest nFCF is also very acceptable for this type of company.

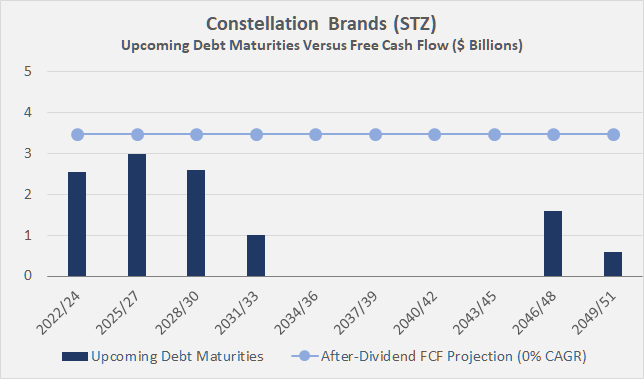

Constellation's net debt at the end of fiscal 2022 (ended February 28, 2022) was 5.9 times three-year average nFCF. Between then and the end of the third quarter of fiscal 2023 (ended November 30, 2022), net debt increased by $1.8 billion, largely due to the distribution paid to holders of Class B shares. The conversion of Class B shares , which were primarily owned by the Sands family and controlled entities, resulted in a reduction in voting concentration (Class A and Class B shares had 1 and 10 votes per share, respectively), operational cost savings, and changes to the company's board (see press release announcing the agreement with the Sands family). However, the significant family ownership - now in the form of Class A shares - remains. As a result of the transaction, Constellation's net debt increased to 6.9 times the three-year average nFCF. STZ's interest coverage ratio is expected to decline from 5.9 times to 5.3 times nFCF before interest. I do not see these levels as worrisome, nor do I believe that the increase in debt significantly limits STZ's leeway for further acquisitions, largely due to the company's still balanced maturity profile (Figure 6). Even after the dividend is paid ($573 million in fiscal 2022), nearly two-thirds of free cash flow remains for other purposes such as debt repayment or acquisitions. With the help of term loans, Constellation could actually pay off its debt at maturity, but this is of course a very unrealistic scenario and is only meant to demonstrate the manageability of the debt.

Figure 6: Debt maturity profile of Constellation Brands [STZ] in three-year buckets as of fiscal 2022 year-end, including the recently assumed debt in an approximative manner and compared to its three-year average normalized free cash flow after dividends (own work)

{kind=link}

Things look slightly worse for Diageo as more debt needs to be refinanced over the coming years (Figure 7, Diageo's dividend payout ratio is around 2/3 of nFCF) - likely at less favorable interest rates due to the current environment. However, the upcoming maturities should be considered in the context of Diageo's very low weighted average interest rate of just 2.3% at the end of fiscal 2022. Granted, the interest coverage ratio will decline, but the impact of refinancing at higher rates will not be too great, and I do not expect it to affect the company's ability to pay its growing dividend and continue its inorganic expansion. STZ's weighted average interest rate of 3.8% (based on fiscal 2022 data) is significantly higher, but should be viewed in the context of the company's U.S.-focused operations. Long-term refinancing of the three-year term loan, which was used to partially fund the recent conversion of Class B shares, will most likely increase Constellation's weighted average interest rate slightly (p. 20, FQ3 10-Q ).

Figure 7: Debt maturity profile of Diageo [DEO, DGEAF] in three-year buckets as of fiscal 2022 year-end, compared to its three-year average normalized free cash flow after dividends (own work)

{kind=link}

Moody's last affirmed Diageo's long-term rating of A3 (S&P equivalent of A-) in November 2019 with a stable outlook. Constellation's long-term rating of Baa3 (S&P equivalent of BBB-) was affirmed in May 2022, also with a stable outlook. The agency highlighted STZ's elimination of its Class B shares and decision to distance itself from Canopy Growth as credit positive, as well as its announced lower leverage target.

Which Is The Better Dividend Stock - Constellation Brands Or Diageo?

Given the stable business models and solid balance sheets, I believe the shares of both companies are fundamentally solid income-generating assets. However, given the comparatively low starting yields of 2.25% (Diageo) and 1.49% (Constellation Brands), the shares should be viewed as long-term investments with only insignificant near-term cash flow. The low dividend yields also indicate - other things being equal - that the shares are not exactly cheap.

In my view, Diageo is the better dividend pick because of its global diversification, its strong focus on premium products, and its comparatively lower exposure to restaurants and bars. At the same time, putting myself in the shoes of a U.S.-based investor, it should be kept in mind that the company reports its earnings and declares its dividend in pounds sterling. From that perspective, STZ seems to be the better choice, but of course the company's U.S. focus carries its own risks. As an aside, I discussed the main risks to companies in the alcohol business in detail in my previous article. For the sake of brevity, I will not repeat them in this analysis.

Both companies are shareholder-friendly, which is underlined by fairly regular dividend increases and occasional share buybacks. Between fiscal 2013 and fiscal 2022, Constellation and Diageo reduced the number of diluted weighted average shares by 11% and 8%, respectively. Constellation paid its first dividend in 2015, and its seven-year compound annual growth rate of 15% certainly sounds very enticing. However, it should be kept in mind that the company increased its dividend quite aggressively between 2016 and 2018, and its payout to shareholders has grown at a fairly moderate pace (0%-5%) since then. STZ did not increase its dividend in 2020. Given the company's exposure to beer and its comparatively small size, I think this was a prudent move and speaks to management's prudence. This is also reflected in the very conservative dividend payout ratio of about 35% of normalized free cash flow. The latest increase of over 5% was certainly meaningful and a good sign of management's confidence in the business. Diageo, due to its global footprint, much better diversification, and less reliance on beer sales (Guinness), was able to offer shareholders a modest 1.9% dividend increase in 2020. Over the longer term, the company typically increases its dividend by about 5% per year. However, it should be borne in mind that the company generally distributes around two-thirds of its free cash flow to shareholders in the form of dividends.

Investors who value companies that can comfortably weather periods of above-average inflation should definitely take a closer look at Diageo, as the company is currently proving that it has very strong pricing power. Reported operating margin declined 92 basis points in the first half of fiscal 2023 , primarily due to special items and foreign exchange. On an adjusted basis, Diageo reported margin expansion of 9 basis points. For the most recent quarter, Constellation reported a 380 basis point decline in operating margin in its beer segment due to increased raw material costs, brewery capacity expansions and higher marketing expenses due to timing issues. Therefore, it seems unfair to directly compare the performance of the two companies, but Constellation is definitely in a comparatively weaker position than Diageo. However, I think the strong FQ3 results of Modelo, Casa Noble, Mi CAMPO and High West confirm the company's intact growth progress, which should help stabilize margins in the long run.

Valuation Of STZ And DEO/DGEAF Stock

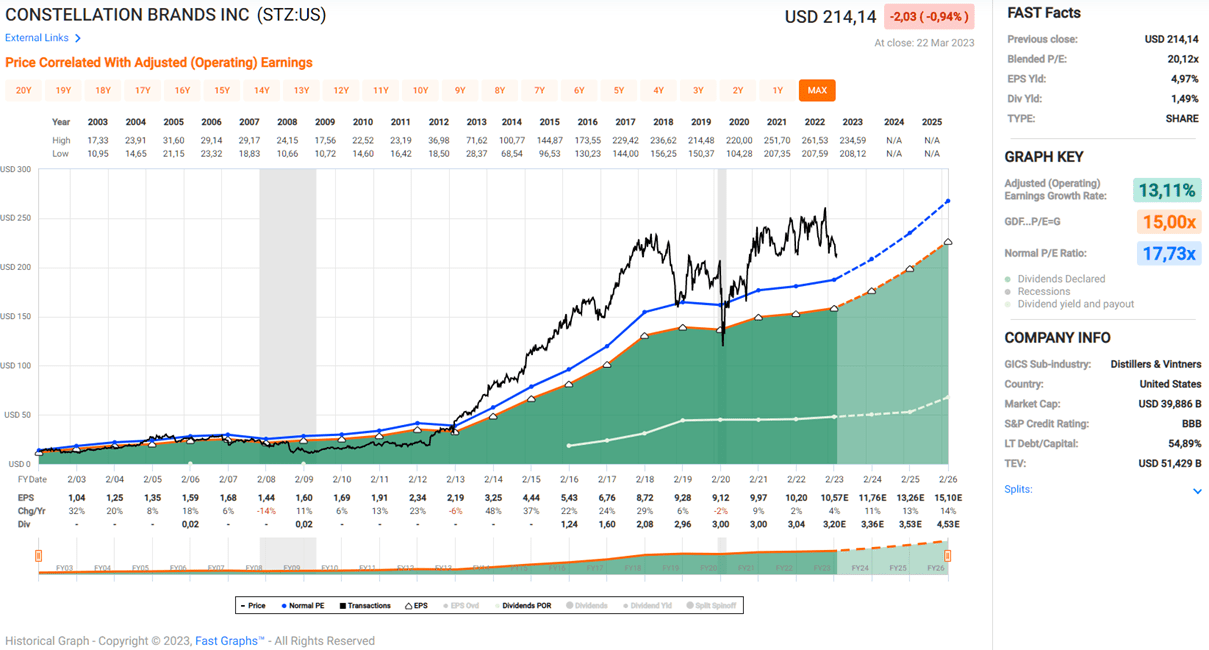

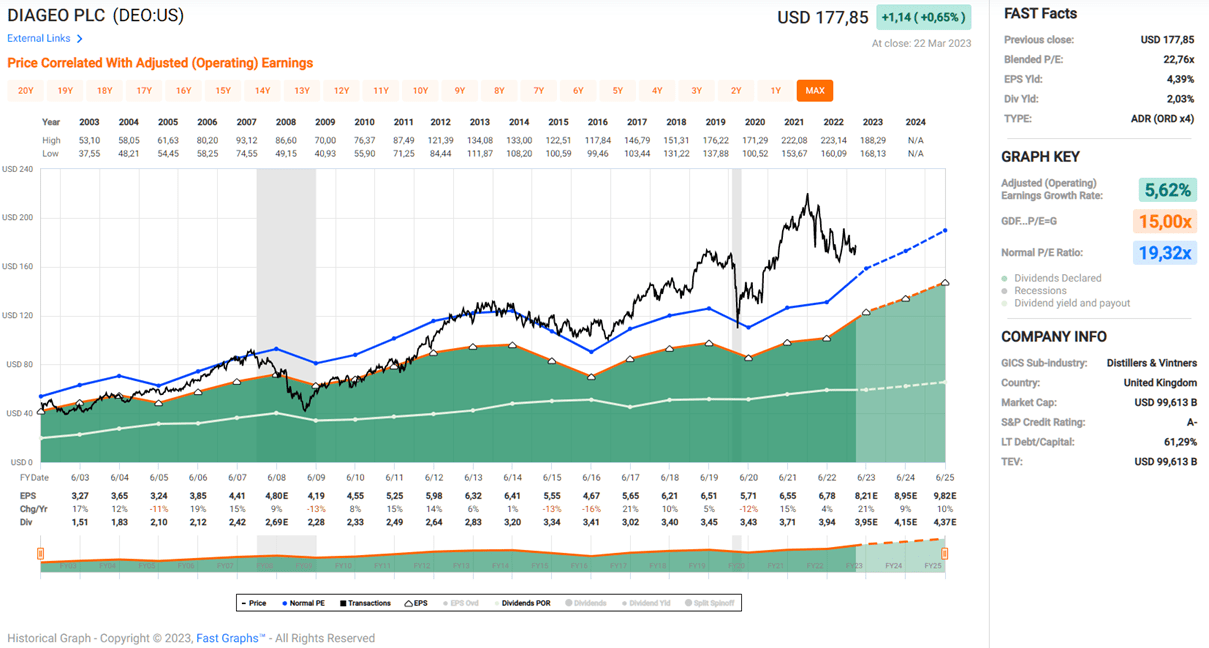

Because of their reliable earnings and cash flows, both companies can be valued based on price-to-earnings ratios and discounted cash flow analysis. Constellation's strong earnings growth is nicely illustrated by the FAST Graphs chart in Figure 8. In my opinion, this is a strong testament to the qualities of management - it takes a lot for a relatively small, beer-focused company to achieve such reliable earnings growth. Of course, results have been much more volatile on an unadjusted diluted earnings basis, but at the same time, looking at Constellation's historical free cash flow is very reassuring. Nevertheless, a price-to-earnings ratio of around 20 seems relatively high for this company, but I think it reflects our current market environment well - quality trades at a premium, and long-term investors in such companies are not easily scared out of their holdings. This is also true of Diageo stock. The ADRs (4:1, issued by Citibank ) are currently trading at over 22 times adjusted operating earnings (Figure 9). Clearly, investors are currently willing to pay a substantial premium for a stake in this well-diversified and well-managed company.

Figure 8: FAST Graphs chart of Constellation Brands stock [STZ], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com) Figure 9: FAST Graphs chart of Diageo's 4:1 ADRs [DEO], based on adjusted operating earnings per share (obtained with permission from www.fastgraphs.com)

{kind=link}

{kind=link}

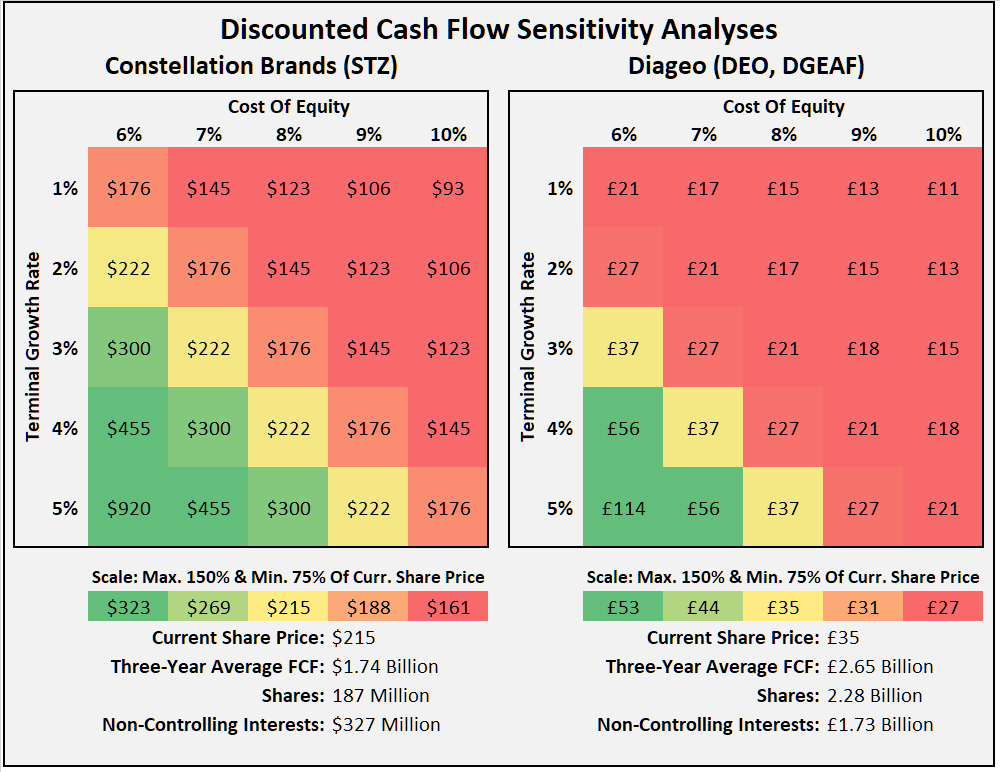

The high price that the market has set for these - admittedly top-quality - companies also becomes clear from the discounted cash flow sensitivity analyses (Figure 10). Assuming a cost of equity of 8%, the free cash flow of STZ and DEO would have to grow by 4% and 5%, respectively, in perpetuity, to justify the current share prices. While this does not sound like overly aggressive growth, it is important to understand the leverage of terminal value in a discounted cash flow analysis. These are significant growth assumptions, and I think the market currently is very confident that Diageo will be able to continue its successful expansion trajectory into new markets through its growth strategy of scaling up previously acquired smaller brands. STZ's valuation is a little less optimistic, but I still think the company needs to consider international expansion through wines, spirits, or newly acquired premium beer brands (STZ's marketing and distribution rights for Grupo Modelo beer brands are confined to the U.S.) to justify its valuation.

Figure 10: Discounted cash flow sensitivity analysis of Constellation Brands [STZ] and Diageo [DEO, DGEAF] (own work)

{kind=link}

Conclusion

Both Diageo and Constellation Brands are formidable companies with forward-looking management teams. Diageo is a more mature company with a balanced portfolio, and its growth story depends largely on expansion into Asian markets, as well as further acquisitions and international development of more or less unknown brands with potential. Diageo's management has a knack for profitable acquisitions. Income-oriented investors from the U.S. probably dislike the company being headquartered in the U.K., but I personally do not mind owning it in a diversified portfolio. Granted, if the pound sterling depreciates, the dividend payout to foreign investors declines accordingly. At the same time, however, the company's earnings benefit from a currency tailwind, which, assuming appropriate capital allocation, can form the basis for stronger organic or inorganic growth in the future. The positive impact on earnings is quite notable in the fiscal 2023 half-year results which were reported in January. In my view, Diageo's growth prospects are favorable, but the stock is priced accordingly. Investors are also willing to pay a premium for its global diversification and high-quality brand portfolio, which plays to its strengths in this inflationary environment.

Conversely, Constellation's focus on beer is at first glance a disadvantage, but the company is doing a very good job of premiumizing its portfolio. As a result, it is increasingly benefiting from intangible switching cost effects, which are a key factor in Diageo's success. Of course, with a beer-focused portfolio, this benefit is somewhat limited, so Constellation's margin expansion in recent years should be seen as particularly positive. As the market leader in U.S.-imported Mexican beer, the company is benefiting from the significant Hispanics/Latinos demographic, and it is also pulling the right levers to offer the kind of low-alcohol but distinct-tasting beverages that are currently in vogue among younger consumers. Modelo's Chelada selection and the Corona Hard Seltzer category are good examples. Of course, Diageo is also benefiting from this trend by leveraging the strength of its internationally recognized spirits brands.

Both companies are well managed and have solid balance sheets. The Sands family's significant ownership is reflected in the conservative nature of STZ's management, which only began paying a dividend in 2015 and skipped a dividend increase in 2020 due to pandemic-related uncertainties. While the elimination of Class B "super-voting-shares" could be viewed as a negative, it is important to remember that the Sands family and controlled entities are still significant holders of Constellation stock. While I am not usually a fan of concentrated ownership in smaller companies due to the buyout risk at low valuations, I think the simplification of the share structure, and the significant consideration paid to former Class B stockholders is a good sign that there are no plans for a take-private transaction that could be detrimental to minority shareholders. Still, it is risk worth considering in one's due diligence.

My regular readers know that I focus on income-generating stocks in my diversified portfolio. From this perspective, and taking into account the current environment, the starting yields of 2.25% (Diageo) and 1.49% (Constellation Brands) are rather uninspiring. However, I think it is wrong to view the two stocks as pure dividend growth stocks - STZ's shareholder returns over the past decade in particular have been largely due to capital gains. DEO and STZ are total return investments. While I think investor patience may be tested in this choppy and sidelining market, the reliable dividends should be considered a small consolation. As a conservative investor, capital preservation is an important objective, and both Constellation Brands and Diageo fit very well into that category. However, even though the shares of both companies rightly demand a premium valuation, I do not consider them a buy at current levels. At the same time, I don't think there's much downside either - these are quality companies, and long-term investors are well aware of the fact and aren't easily scared out of their holdings.

For my own internationally diversified portfolio, I'm a happy long-term owner of Diageo. The company offers the best of both worlds - world-leading brands with growth prospects in ready-to-drink cocktails and throughout the world. Constellation Brands' investment case has appeal, no doubt about it, but I do not think it adds meaningful diversification to my own stock portfolio. If I put myself in the shoes of a U.S.-based investor and disregard valuation, I would probably consider building a position in Brown-Forman and Constellation Brands instead of Diageo. Brown-Forman offers international diversification and a high-margin spirits portfolio of leading brands, and Constellation offers U.S.-focused exposure to growing premium beer brands.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my article. Whether you agree or disagree with my conclusions, I always welcome your opinions and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Diageo Vs. Constellation Brands - One Is The Better Dividend Stock (With A Caveat)