UZF - Diamond Hill Long-Short Fund Q2 2023 Market Commentary

2023-08-23 11:30:00 ET

Summary

- Diamond Hill invests on behalf of clients through a shared commitment to its valuation-driven investment principles, long-term perspective, capacity discipline and client alignment.

- The portfolio trailed the Russell 1000 Index and the blended benchmark (60% Russell 1000 Index/40% Bloomberg US Treasury Bills 1-3 Month Index) in Q2.

- US stocks rose over 8% in Q2 2023, bringing YTD gains to roughly 16%.

- Large-cap stocks outperformed mid-cap and small-cap stocks in Q2.

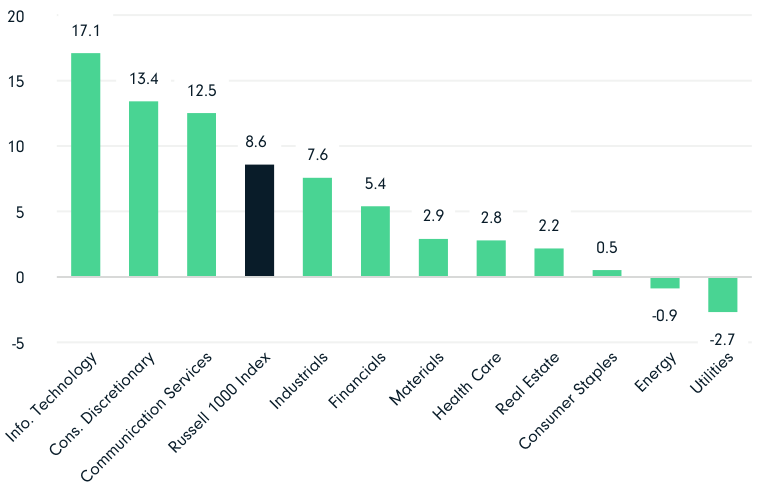

- Technology, consumer discretionary, and communication services sectors performed well, while energy and utilities sectors struggled.

Market Commentary

Markets were positive in Q2 2023, with US stocks rising over 8% (as measured by the Russell 3000 Index), bringing YTD gains to roughly 16%. Continuing the YTD trend, large-cap stocks led in Q2, rising almost 9%, while mid-cap stocks rose nearly 5% and small-cap stocks rose just over 5% (as measured by the Russell indices). Also continuing from Q1, growth stocks outperformed their value counterparts across the cap spectrum. The Russell 1000 Value Index rose 4%, while its growth counterpart rose nearly 13%; the Russell Midcap Value Index advanced close to 4%, while the Russell Midcap Growth Index rose over 6%. The Russell 2000 Value Index added a little over 3%, and the Russell 2000 Growth Index rose just over 7%.

From a sector perspective, technology continued its strong YTD performance in Q2, rising north of 17%, while consumer discretionary (13%) and communication services (13%) were also nicely positive. Conversely, energy (-1%) and utilities (-3%) were in the red in Q2 as oil prices have defied expectations they would rise given the ongoing Russia Ukraine war. Relatively moderate winter temperatures combined with increased production (and, therefore, increased supply), helped rein prices in — but consequently pressured returns in the relevant energy and utilities sectors.

2Q23 Russell 1000 Index Sector Returns (%)

{kind=link}

The macro picture has also been consistent in 2023, with inflation, central bank policy and ongoing geopolitical tensions dominating headlines. In early May, JP Morgan agreed to acquire most of First Republic Bank’s operations after the failed institution was seized by regulators. It marked the second-largest bank failure in US history (after Washington Mutual’s 2008 collapse), followed by Silicon Valley Bank and Signature Bank, both of which failed late in Q1 2023. While we remain vigilant in assessing the fundamental health of all our portfolio holdings, we believe the worst is behind us on this front for the time being.

Many point to the recent failures as signs monetary policy has gotten sufficiently (if not overly) tight — and investors consequently anticipated a slowdown or pause in rate hikes. Indeed, though the Federal Reserve did raise the benchmark rate 25 basis points (bps) in May to a range of 5.00% - 5.25%, it also tentatively hinted the current rate hike cycle (which has included 10 hikes in just over a year) was nearing its conclusion and didn’t raise rates in June.

Outside the US, global monetary policy is a more mixed bag. The UK faces ongoing stubborn inflation, seemingly decreasing the likelihood it is as close to the end of its hiking cycle as the US may be. Similarly, the European Central Bank likely has a way to go as inflation has proven sticky in major economies like Germany’s. In contrast, many emerging markets economies seem on the cusp of considering pausing rate hikes, if not beginning to cut. For example, Hungary trimmed rates (which remain high) during the quarter as it struggles to rein in inflation while not hampering too much economic activity. A notable exception is Turkey, which significantly raised rates (650 bps) following President Erdogan’s May re-election — presumably in a bid to convince markets the country will begin seriously addressing its economic challenges. Whether investors find the effort credible naturally remains to be seen.

Meanwhile, markets seem to continue climbing the proverbial wall of worry — likely aided by relatively resilient economic data and corporate earnings in the US (and, selectively, beyond). Inflation, though effectively a global concern, has yet to meaningfully dampen hiring in the US. Stocks have rallied — especially growth stocks, where prices have increased significantly — which could be reflective of the fact that markets have discounted an impending recession several times over the last couple years, each time getting a little more comfortable with the economy’s and corporate earnings’ resilience.

That said, we don’t believe now is the time to get complacent about the environment. As we saw in March this year with the first of the aforementioned bank failures, unexpected events could rattle markets periodically — and that is particularly the case given all the macroeconomic headwinds we currently see. Further, there is still a possibility we see a recession in the next three to nine months, given the 10-year/3-month yield curve remains inverted and has historically been a decent predictor of recession.

However, we believe our philosophy and approach are well-suited to just such an environment — in which higher rates, higher inflation and possibly higher volatility than we’ve seen over the last decade or so are likely — as value stocks are likely to become more attractive to investors as they are well-positioned to produce attractive cash flows over time.

Performance Discussion

The portfolio trailed the Russell 1000 Index and the blended benchmark (60% Russell 1000 Index/40% Bloomberg US Treasury Bills 1-3 Month Index) in Q2. Our long book’s positive returns lagged the benchmark, tied primarily to our long technology holdings and our significantly below benchmark exposure, detracting from relative results. Our long consumer discretionary holdings were also a source of relative weakness. Conversely, our long consumer staples and communication services holdings were sources of relative strength in Q2. Our short book trailed the index, providing a relative tailwind to performance.

On an individual holdings’ basis, bottom contributors to return in Q2 included long positions in WNS (Holdings) Limited and Ciena ( CIEN ). India-based business process management (BPM) services company WNS declined as investors contemplated whether artificial intelligence ((AI)) could disrupt the company’s BPM solutions. However, we do not believe AI will be a major threat to the company’s value proposition given its BPM expertise — on the contrary, we anticipate AI may present opportunities for WNS to implement AI-related solutions on its clients’ and prospects’ behalf.

Networking systems company Ciena has faced a significant orders backlog given ongoing supply chain constraints. With those now easing, Ciena has begun fulfilling orders, generating strong fundamentals. However, two of its largest segments — telecommunications and web scale — have begun pushing out orders, leading to concerns those orders could ultimately be cancelled and weighing on shares. However, our long-term fundamental outlook on the company remains favorable, and we anticipate the company will work through these near-term issues.

Other bottom contributors were from our short book, including Teradata Corporation ( TDC ), e.l.f. Beauty ( ELF ) and Penumbra ( PEN ). Teradata provides a connected multi-cloud data platform for enterprise analytics. We initiated our short position given our conviction the market has been over-optimistic in assuming the company would successfully transition into a competitive cloud data warehouse provider. In contrast, we believe Teradata is overexposed to the legacy, on-premise data warehouse market and will struggle to compete with cloud native data warehouse peers. In Q1, though, the company made better progress than anticipated on its transition, giving shares a boost. We believe our thesis remains intact, and Teradata is likely to be challenged in the period ahead by superior offerings from competitors like Amazon, Google, Snowflake and Databricks.

Shares of mass market beauty company e.l.f. Beauty benefited in Q2 from robust consumer demand. We’ve maintained our short position despite the healthy fundamentals as the valuation has gotten even richer. While medical device manufacturer Penumbra has benefited from multiple product launches year to date, we believe it still faces headwinds from rising competition in its end markets and reputational and litigation risk from a defective product.

Top contributors to return in Q2 were all from our long book, including Microsoft ( MSFT ) and American International Group ( AIG ). Microsoft reported strong quarterly results and provided more favorable than expected commentary on near-term Azure (cloud platform) revenue growth. Investors had become concerned that Azure’s revenue growth could come under increased pressure in a weakening economy, but the combination of quarterly results and commentary about Azure’s future growth trajectory calmed concerns.

AIG reported solid quarterly results for its fiscal Q1, consistent with our thesis that the company is now in the middle stages of a successful turnaround in its P&C insurance business that we believe still has meaningful runway for improvement. AIG also announced the expected sale of Validus Re (property catastrophe reinsurance) to RenaissanceRe, a transaction we view as mutually beneficial as it transfers the assets to an entity that can create the most value with the intellectual property and customer relationships. The sale is also consistent with AIG’s longer-term path of reducing underwriting volatility. The proceeds from the sale, along with an additional share sale of its ownership stake in CRBG (the holding company for its life and retirement business), should generate a nice cash flow for the company, which it intends to use to repurchase stock.

Other top contributors included META Platforms, Alphabet ( GOOG , GOOGL ) and Parker-Hannifin ( PH ). Social media platform Meta rose alongside its mega-cap tech brethren as it has made progress cutting its expense base, contributing to better than-expected earnings in Q1. Alphabet launched several new products to respond to competition from ChatGPT and Microsoft, which was a comprehensive response by the company to showcase that it is a leader in the artificial intelligence space. Shares of global leader in motion and control technologies and solutions Parker Hannifin rose alongside improving investor sentiment about global industrial activity — a meaningful majority of Parker Hannifin’s revenues are derived from industrial businesses.

Portfolio Activity

New positions initiated in Q2 included a long position in Target Corporation ( TGT ) and shorts in Canada Goose Holdings ( GOOS ) and Choice Hotels International ( CHH ). Retailer Target Corporation has been pressured in recent quarters by the combination of traffic challenges and boycotts related to social issues — neither of which we think are likely to lead to long-term traffic deterioration. Further, we anticipate the company will be able to improve inventory management in the period ahead, which should contribute to improved operating margins. Given what we believe to be an attractive risk/ reward profile, we capitalized on the depressed share price to initiate a position in Q2.

Luxury apparel designer and marketer Canada Goose experienced tremendous popularity — especially for its designer parkas — a few years ago. As that popularity has largely peaked, the company has announced plans to launch product extensions into related aspects of apparel. While the market seems optimistic about Canada Goose’s ability to capitalize on these extensions to spur sales growth, we are less so and believe the current valuation is overly optimistic. Given this combination, we initiated a short position in Q2.

Hotel franchisor Choice Hotels similarly benefited from a favorable environment over the past couple years. However, it faces challenges from a unit growth standpoint — i.e., its ability to grow the number of rooms available. During COVID, Choice Hotels’ locations were a benefit to the company as they were easily reached via car during the pandemic — helping contribute to higher revenues per available room and possibly obscuring some of its impending growth challenges. We believe the market is too generously projecting Choice Hotel’s recent performance into the future and consequently capitalized on the opportunity to initiate a short position.

In Q2, we exited our long position in global basic apparel manufacturer Hanesbrands in favor of more compelling opportunities elsewhere. We also covered our short positions in Bank of Hawaii ( BOH ), Macy’s ( M ), US Cellular Corp ( USM ), Waters Corporation ( WAT ) and Westamerica Bancorporation ( WABC ) as our theses played out and the stock prices converged with our estimates of intrinsic value.

The Fund’s net exposure at the end of the quarter was 57%.

Market Outlook

Despite equity markets’ positive returns in Q2 and 2023 to date, it has been among the narrowest markets in history, with just seven stocks — Meta Platforms, Apple, NVIDIA, Alphabet, Microsoft, Amazon and Tesla — contributing a large majority of the market’s return. These stocks collectively have increased 61% year to date, although the other 493 stocks in the S&P 500 Index increased a respectable 6%.

Market participants have seemingly moved past the recent failures of SVB Financial, First Republic and Signature Bank; however, the full effects of these failures have not yet been felt. For example, if banks pull back on lending to improve their capital positions, it could negatively impact economic growth. Balancing the potential economic impact of higher interest rates with still-elevated inflation levels continues to complicate the Fed’s monetary policy decision-making process.

Corporate earnings growth is expected to slow in 2023, weighed down partly by a decline in energy sector earnings due to commodities prices well below their mid-2022 peaks. However, the decline in this year’s earnings estimates seems to have bottomed.

Given the very aggressive monetary policy and much higher interest rates, we have been surprised many of the more speculative growth stocks have been leading the market thus far in 2023. Growth stocks more broadly have regained a vast majority of their 2022 underperformance versus value stocks, with the Russell 1000 Growth Index outperforming the Russell 1000 Value Index by 24 percentage points year to date.

Meanwhile, equity markets are trading at elevated valuations compared to history; however, this is somewhat misleading given the market’s narrowness. While the S&P 500 Index trades around 20X earnings per share (EPS), the median stock trades at a more reasonable ~17X EPS. So, while it may be difficult for equity markets to generate returns that match historical averages over the next five years, there are still attractive opportunities with the potential to generate above-average returns over that period.

Our primary focus is always on adding value through stock selection by identifying both long and short opportunities. We believe investors who are willing to perform deep research and valuation work to identify individual businesses that are being mispriced by the market will be rewarded with favorable risk-adjusted returns over the long term.

| Period and Annualized Total Returns (%) |

| Since Inception (30 Jun 2000) |

| 20Y |

| 15Y |

| 10Y |

| 5Y |

| 3Y |

| 1Y |

| YTD |

| 2Q23 |

| Expense Ratio (%) |

| Class I ( DHLSX ) |

| 6.42 |

| 7.04 |

| 4.96 |

| 5.84 |

| 5.67 |

| 9.19 |

| 4.42 |

| 3.85 |

| 3.27 |

| 1.50 |

| Russell 1000 Index |

| 7.11 |

| 10.13 |

| 10.77 |

| 12.64 |

| 11.92 |

| 14.09 |

| 19.36 |

| 16.68 |

| 8.58 |

| — |

| 60%/40% Blended Index |

| 5.17 |

| 6.81 |

| 7.00 |

| 8.13 |

| 8.13 |

| 9.24 |

| 13.39 |

| 10.83 |

| 5.62 |

| — |

| Russell 1000 Value Index |

| 7.33 |

| 8.50 |

| 8.36 |

| 9.22 |

| 8.11 |

| 14.30 |

| 11.54 |

| 5.12 |

| 4.07 |

| — |

| Click here for holdings as of 30 June 2023. 1 Includes dividend expense relating to short sales. If dividend expenses relating to short sales were excluded, the Expense Ratio for the Long-Short Fund would have been 1.08% for Class I. Risk disclosure: The portfolio uses short selling which incurs significant additional risk. Theoretically, stocks sold short have the risk of unlimited losses. Overall equity market risks may affect the portfolio’s value. The views expressed are those of Diamond Hill as of 30 June 2023 and are subject to change without notice. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Investment returns and principal values will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The Fund’s current performance may be lower or higher than the performance quoted. For current to most recent month end performance, visit Diamond Hill. Performance assumes reinvestment of all distributions. Returns for periods less than one year are not annualized. Class I shares include Investor share performance achieved prior to the creation of Class I shares. Fund holdings subject to change without notice. Index data source: Bloomberg Index Services Limited. See Diamond Hill - Disclosures for a full copy of the disclaimer. Securities referenced may not be representative of all portfolio holdings. Contribution to return is not indicative of whether an investment was or will be profitable. To obtain contribution calculation methodology and a complete list of every holding’s contribution to return during the period, contact 855.255.8955 or info@diamond-hill.com. Carefully consider the Fund’s investment objectives, risks and expenses. This and other important information are contained in the Fund’s prospectus and summary prospectus, which are available at Diamond Hill or calling 888.226.5595. Read carefully before investing. The Diamond Hill Funds are distributed by Foreside Financial Services, LLC (Member FINRA). Diamond Hill Capital Management, Inc., a registered investment adviser, serves as Investment Adviser to the Diamond Hill Funds and is paid a fee for its services. Not FDIC insured | No bank guarantee | May lose value |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Diamond Hill Long-Short Fund Q2 2023 Market Commentary