BORR - Diamond Offshore: Expectations For Earnings Inflection Shifting Into Next Year

Summary

- Diamond Offshore Drilling, Inc. reports fourth quarter and full-year 2022 results largely in line with expectations provided in November.

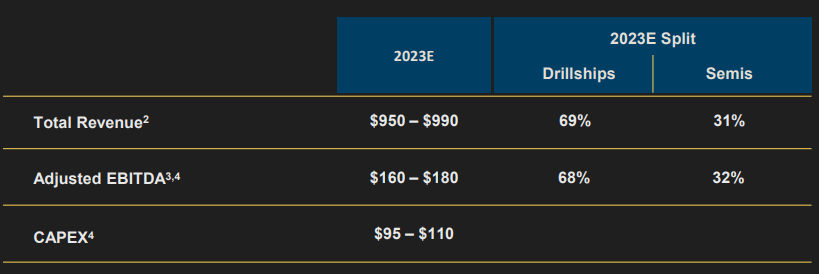

- On the conference call, management projected significant increases in revenue and Adjusted EBITDA for this year but free cash flow is expected to remain negative.

- Backlog at the end of December was stated at approximately $1.8 billion but this number includes more than $300 million related to managed drillships "Auriga" and "Vela".

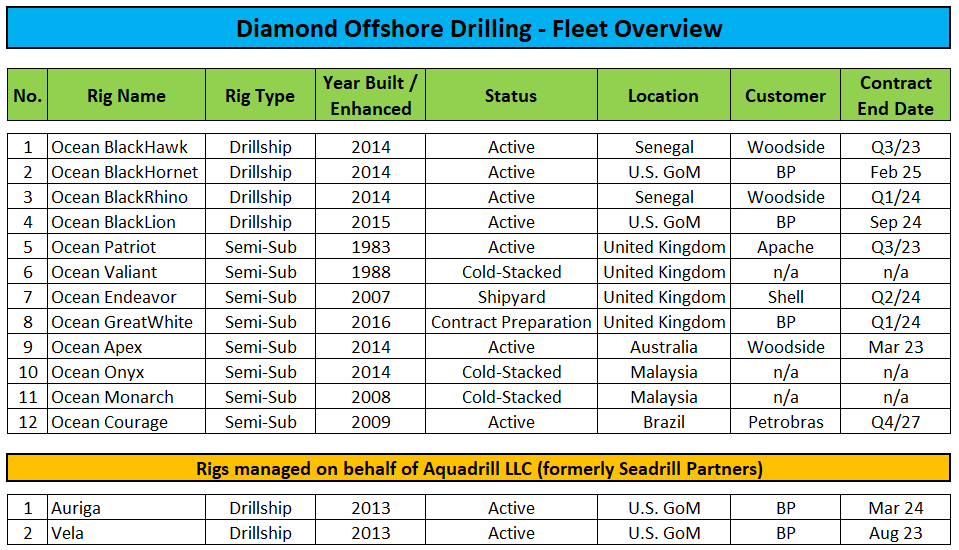

- Based on some of the company's highest-specification rigs still working on legacy contracts at painfully low rates, ongoing weakness in the North Sea market and three units remaining cold-stacked, investors will have to look forward to 2024 as a likely inflection point.

- With Diamond Offshore Drilling, Inc. stock up by almost 65% since I initiated coverage of the restructured company 11 months ago and expectations for an earnings inflection having shifted into next year, I am downgrading my rating from "Strong Buy" to "Buy" but would advise investors to initiate or add to existing positions on any major weakness.

Note:

I have previously covered Diamond Offshore Drilling, Inc. ( DO ), so investors should view this as an update to my earlier articles on the company.

After the close of Monday's regular session, leading offshore driller Diamond Offshore Drilling ("Diamond Offshore") reported fourth quarter and full-year 2022 results largely in line with expectations provided in November.

For the full year, the company recorded Adjusted EBITDA of $35 million and negative free cash flow of slightly above $50 million.

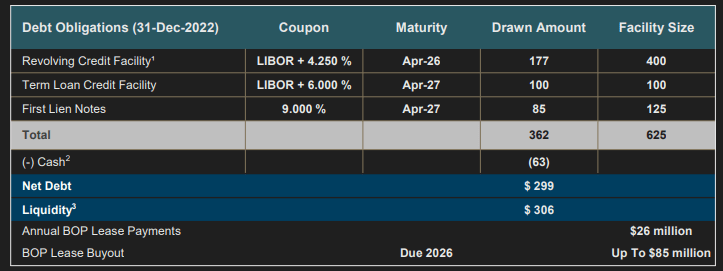

Diamond Offshore finished the year with $63 million in unrestricted cash on the balance sheet and $306 million in total liquidity. Net debt excluding restricted cash calculated to $299 million:

{kind=link}

On the conference call , management projected significant increases in revenue and Adjusted EBITDA for this year, but free cash flow is expected to remain negative:

{kind=link}

With some of the company's highest-specification rigs still working on legacy contracts at painfully low rates, ongoing weakness in the North Sea market and three units remaining cold-stacked, investors will have to look forward to 2024 as a likely inflection point for Diamond Offshore.

In addition, the company's focus on the moored semi-submersible rig market doesn't help things either as rates for this niche asset class continue to lag substantially behind the drillship segment.

Lastly, the company recently suffered a surprise contract termination for the semi-submersible rig Ocean Patriot, but on the conference call , management was confident in securing new work for the rig in the second half of this year.

{kind=link}

Backlog at the end of December was stated at approximately $1.8 billion but this number includes more than $300 million related to managed drillships " Auriga " and " Vela. " With rig owner Aquadrill LLC currently in the process of being acquired by former parent Seadrill ( SDRL ), both management contracts are likely to be terminated later this year.

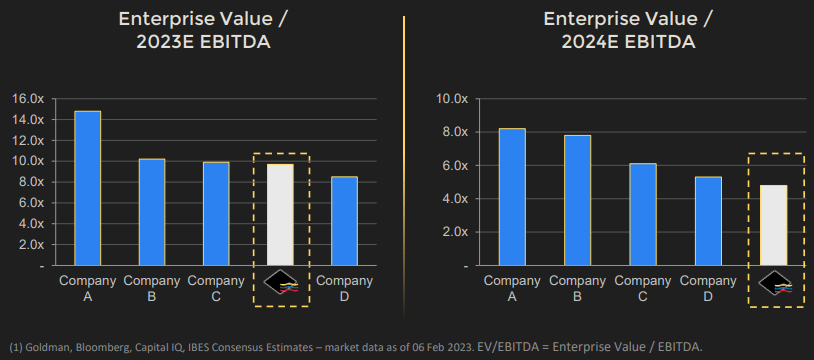

During the question-and-answer session of the conference call, management stated that the company continues to evaluate potential business combination opportunities and pointed to Diamond Offshore's low 2024 consensus EV/EBITDA multiple relative to peers:

{kind=link}

Bottom Line:

Very similar to larger competitor Valaris Limited ( VAL ), it will take more time for Diamond Offshore to fully participate in the ongoing industry recovery.

That said, even after the recent rally, Diamond Offshore Drilling, Inc. shares look inexpensive relative to peers based on consensus EV/EBITDA estimates.

In addition, odds remain in favor of the company being acquired by a larger competitor in the not-too-distant future.

With Diamond Offshore Drilling, Inc. stock up by almost 65% since I initiated coverage of the restructured company 11 months ago and expectations for an earnings inflection having shifted into next year, I am downgrading my rating from " Strong Buy " to " Buy " but would advise investors to initiate or add to existing positions on any major weakness.

At this point, I remain positive on the entire industry, including leading U.S. exchange-listed players Seadrill, Valaris, Borr Drilling ( BORR ), Transocean ( RIG ), Noble Corporation ( NE ), Helix Energy Solutions ( HLX ) and particularly offshore drilling support providers like Tidewater ( TDW ) and SEACOR Marine Holdings ( SMHI ).

For further details see:

Diamond Offshore: Expectations For Earnings Inflection Shifting Into Next Year