FANG - Diamondback Energy: 8% Distribution Yield At $80 WTI I Expect Strong Upside

2024-01-16 07:15:00 ET

Summary

- The market is expected to see a rotation to "value" stocks, making energy stocks a good investment choice.

- Diamondback Energy is a strong energy stock with deep reserves, a top-tier balance sheet, and a commitment to distributing free cash flow to shareholders.

- Diamondback has outperformed growth stocks and is expected to continue to do so, especially if oil prices remain strong.

Introduction

A short while ago, I wrote an article titled "SCHD: A Buffett-Style ETF For 2024 And Beyond." In that article, I explained why I believe that the market will likely see a rotation to "value" stocks based on factors like valuation and economic developments, including sticky inflation.

In order to beat the market, I believe it is enough to focus on a few key things:

- Buying stocks with strong balance sheets and wide-moat business models to withstand economic headwinds.

- Buying stocks with good valuations and/or decent yields, as we'll likely see a rotation from growth to value, with a bigger part of total returns in the future coming from dividends.

Buying energy is a part of this strategy.

Currently, my largest energy holding is Canadian Natural Resources ( CNQ ), followed by Antero Midstream ( AM ), which is a midstream company I bought in the first trading days of this year.

One of the upstream energy plays I like in the United States is Diamondback Energy ( FANG ) , with the perfect ticker to make catchy titles.

Just like Canadian Natural, Diamondback has a few characteristics that are very appealing to energy investors like myself:

- It has deep reserves, which means it won't be forced into risky M&A deals anytime soon.

- It has a top-tier balance sheet and low breakeven prices, paving the road for strong free cash flow.

- It is dedicated to distributing almost all of its free cash flow to shareholders through a regular dividend, special dividends, and buybacks.

As a result, it is not only a stock that I expect to outperform its peers but also a company that could be a great pick to beat the FANG stocks. By that, I mean the high-flying growth stocks of the past few years.

{kind=link}

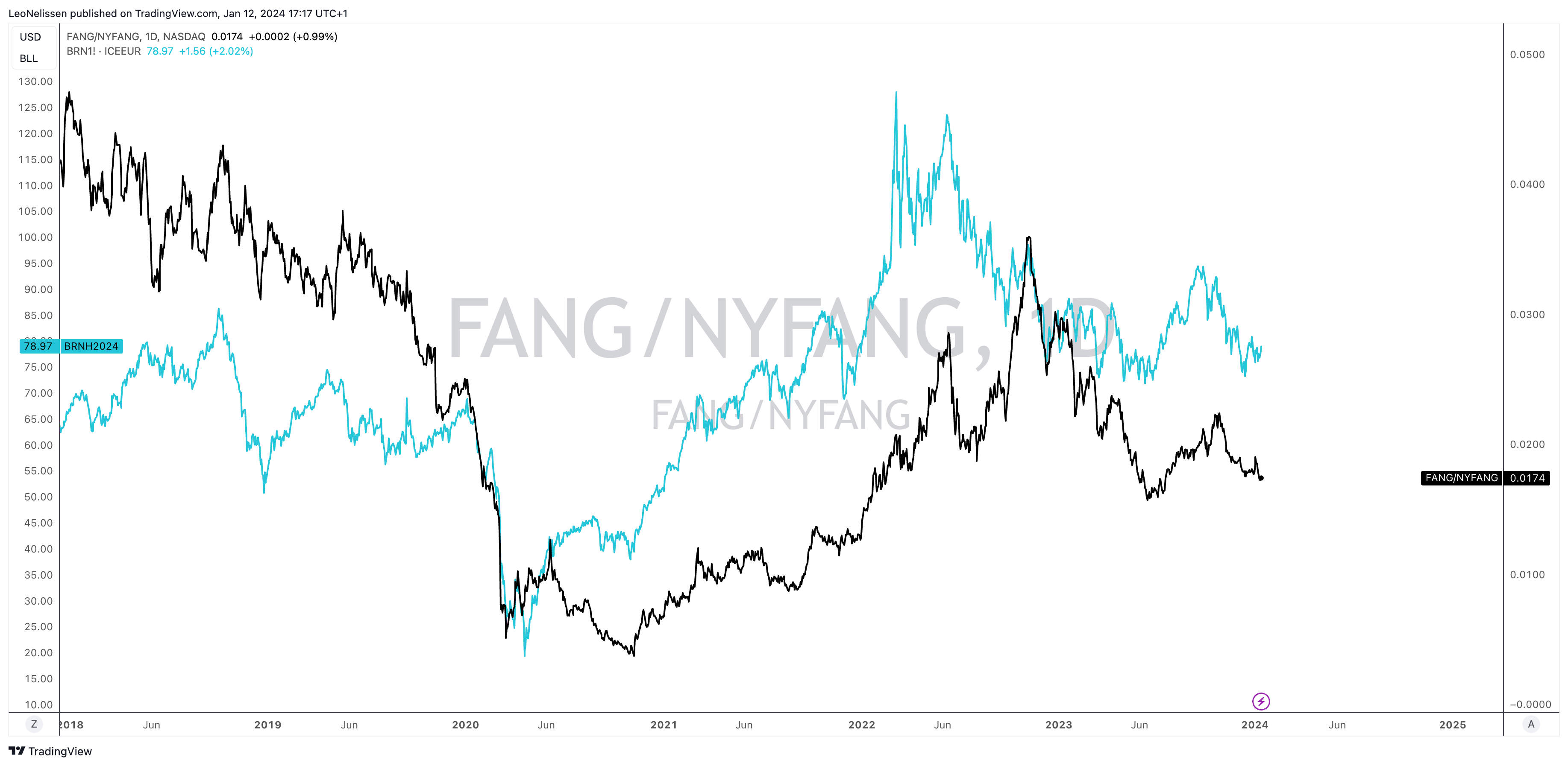

The chart below shows the ratio between Diamondback Energy and the ICE NYSE FANG+ index, which covers the aforementioned growth stocks.

Since 2021, Diamondback has outperformed these stocks. Especially if oil prices remain strong or climb higher (the blue line), I expect that Diamondback will be a better play than tech stocks going forward.

TradingView (FANG/ICE NYSE FANG+ Ratio)

{kind=link}

With all of this said, let's dive into the details!

Bullish On Oil

Generally speaking, I'm bullish on oil for two reasons:

- I expect long-term demand to remain strong.

- Supply growth is weakening, as the supply drivers of the past 15 years (U.S. shale operations) are losing momentum due to weaker Tier 1 reserves and a general focus on free cash flow over growth CapEx.

Going into this year, Wall Street seemed to agree.

According to Bloomberg , analysts foresee a potential recovery in oil prices this year, though not a substantial rally.

Projections from major banks suggest an average of $85 a barrel for global benchmark Brent in 2024. Citigroup's conservative estimate stands at $75, while Goldman Sachs is more optimistic at $92.

Projections anticipate further growth in global oil demand in 2024, mainly driven by China.

However, analysts remain divided on the magnitude of this expansion and how easily it can be satisfied by increasing supplies.

Overall sentiment is cautious compared to earlier predictions of a return to $100 a barrel, pressured by robust output from countries like the U.S., Guyana, and Iran.

While production in the U.S. has risen, I need to add that official numbers are a bit "manipulated," as the Energy Information Administration has started to include natural gas liquids into oil production, which caused official data to show a 1 million barrels per day production increase.

Bloomberg (Via Modern Investing)

However, natural gas liquids are different from crude oil.

Hence, I tend to agree with the view of StanChart , which I highlighted below:

Not only has StanChart predicted a much smaller global oil surplus in the early part of the year but sees demand growth remaining at elevated levels . Indeed, StanChart has forecast that global oil demand growth in 2024 and 2025 will remain above the longer-term average. The experts have predicted that oil demand growth in 2024 will clock in at a robust 1.54 mb/d before slowing down slightly to 1.41 mb/d in 2025. StanChart says that slowing non-OPEC supply, including from the U.S., and strong demand will support prices at higher levels .

On top of that, we're now dealing with more turmoil in the Middle East, including a war with the Houthis in Yemen.

While I expect that this will be bullish for oil, I cannot yet assess how bad things could get as I am not a Middle East geopolitical expert.

However, what I do know/expect is that the bull thesis on oil I maintain since 2020 will remain a strong foundation for oil stocks like Diamondback.

Why I Like Diamondback Energy So Much

With a $27 billion market cap, Diamondback Energy is one of North America's largest oil and gas producers.

Even more important, the company has very deep reserves, as I highly dislike companies that may be forced to engage in M&A projects soon to maintain healthy production reserves.

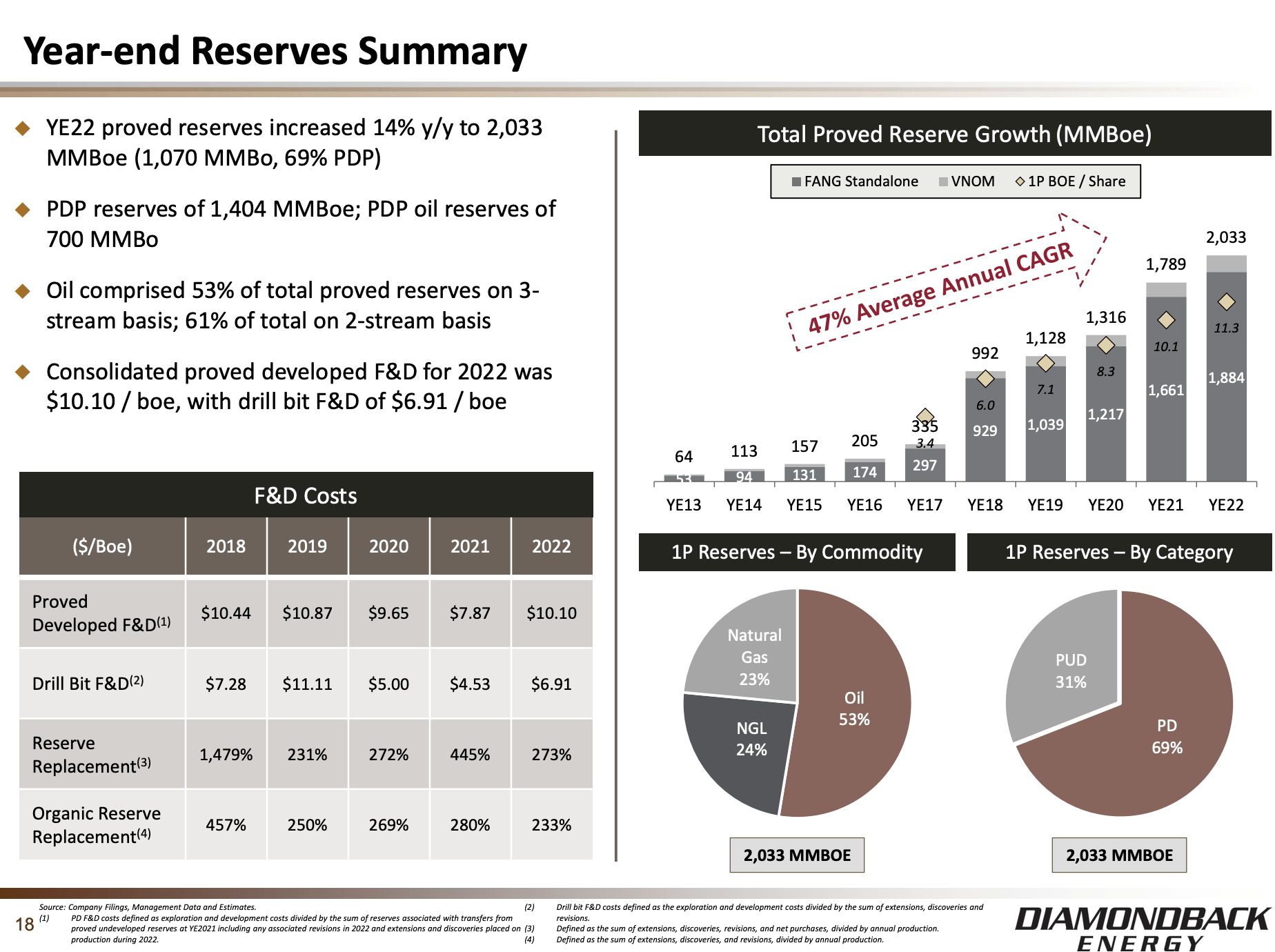

Going into 2023, the company had 2.0 billion barrels of oil equivalent ("BOE") in reserves. As full-year 2023 production is expected to be roughly 447 thousand BOE per day, this translates to a reserve life of 12 years. This excludes new discoveries.

On a side note, 58% of its 2023E production guidance is expected to be crude oil, which makes FANG an oil-focused oil and gas producer. That's another thing I like about this company.

Going back to its reserves, the company has grown its proved reserves by 47% per year since 2013. These numbers also exclude probable reserves, which means there's a lot more oil that's not included in these numbers.

{kind=link}

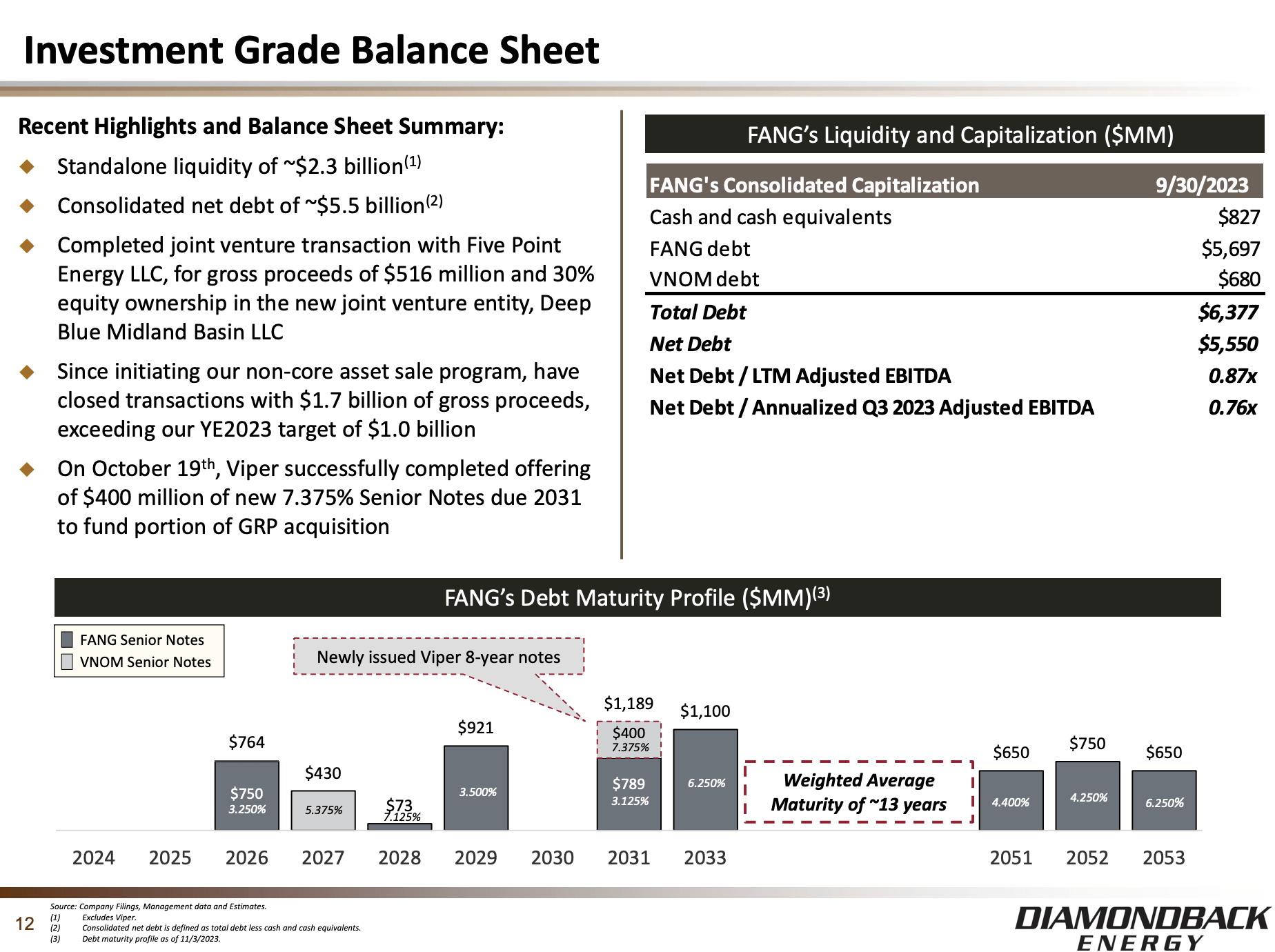

It also has a very healthy balance sheet, reflected in the total debt and net debt figures, which decreased by over $300 million and $1 billion in the third quarter, respectively, primarily attributed to the successful closure of non-core asset sales.

The company announced and closed non-core asset sales, generating gross proceeds of approximately $1.7 billion.

Moreover, in September, the company entered into a joint venture ("JV") with Five Point Energy LLC to form Deep Blue Midland Basin LLC. This JV, where Diamondback retained a 30% ownership stake, emerged as the largest independent water business in the Midland Basin. The transaction brought in proceeds of approximately $500 million.

As of September 30, the company has a net leverage ratio of less than 1x EBITDA.

The company has an investment grade credit rating of BBB-.

{kind=link}

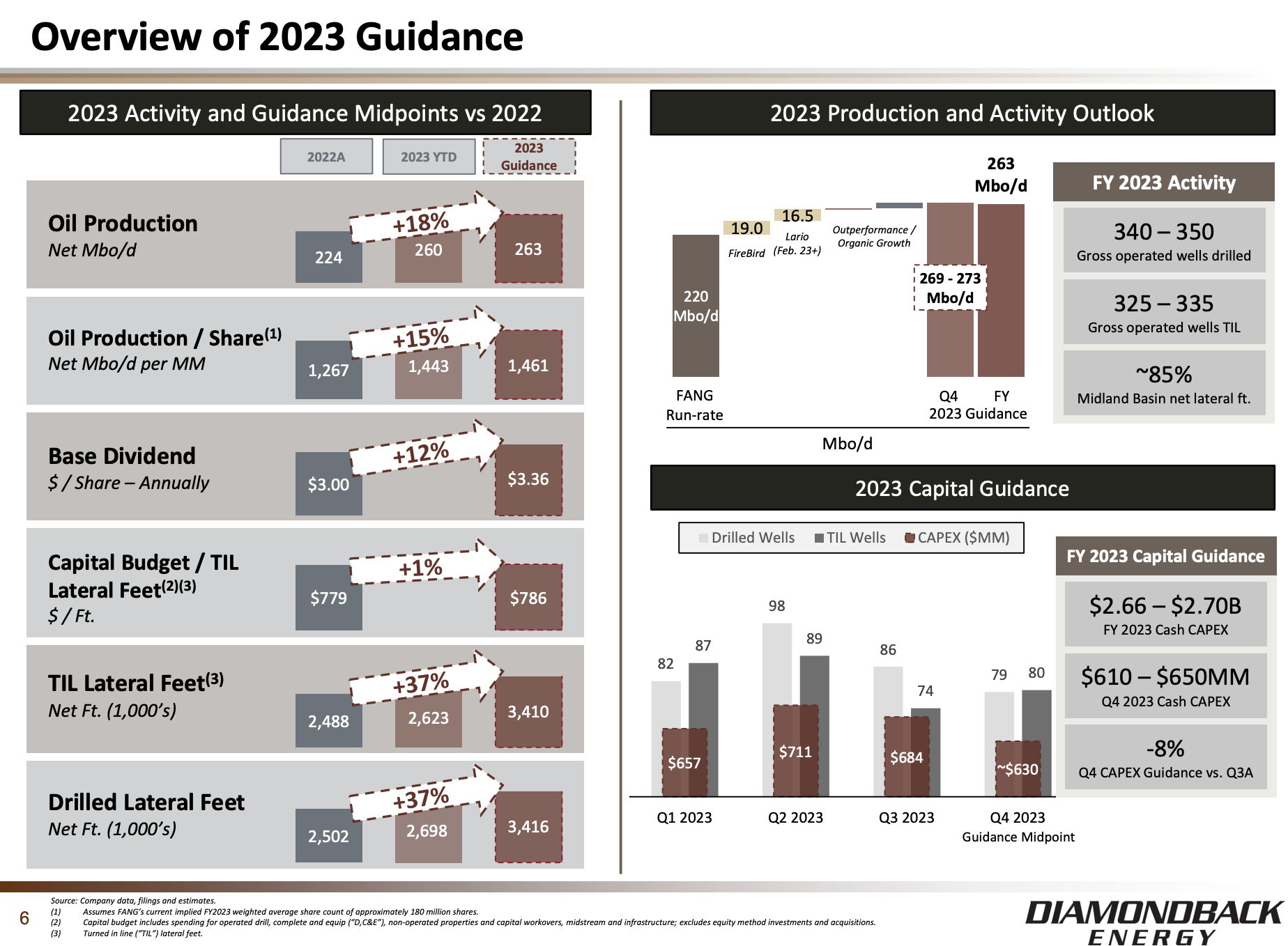

The company is also extremely efficient.

For example, cash capital expenditures for the third quarter came in at $684 million. While this is in the upper half of the quarterly guidance range, the company foresees a 5% to 10% decline in cash capex in the fourth quarter, ranging between $610 million and $650 million.

This projection is grounded in expectations of lower well costs, reduced drilling activity, and a slightly slower completion cadence.

Importantly, the midpoint of the fourth quarter capex is positioned as a reasonable baseline for the 2024 plan, assuming prevailing commodity prices.

This strategy aims to support organic production growth with lower capital expenditure, ultimately generating more free cash flow and FCF per share.

{kind=link}

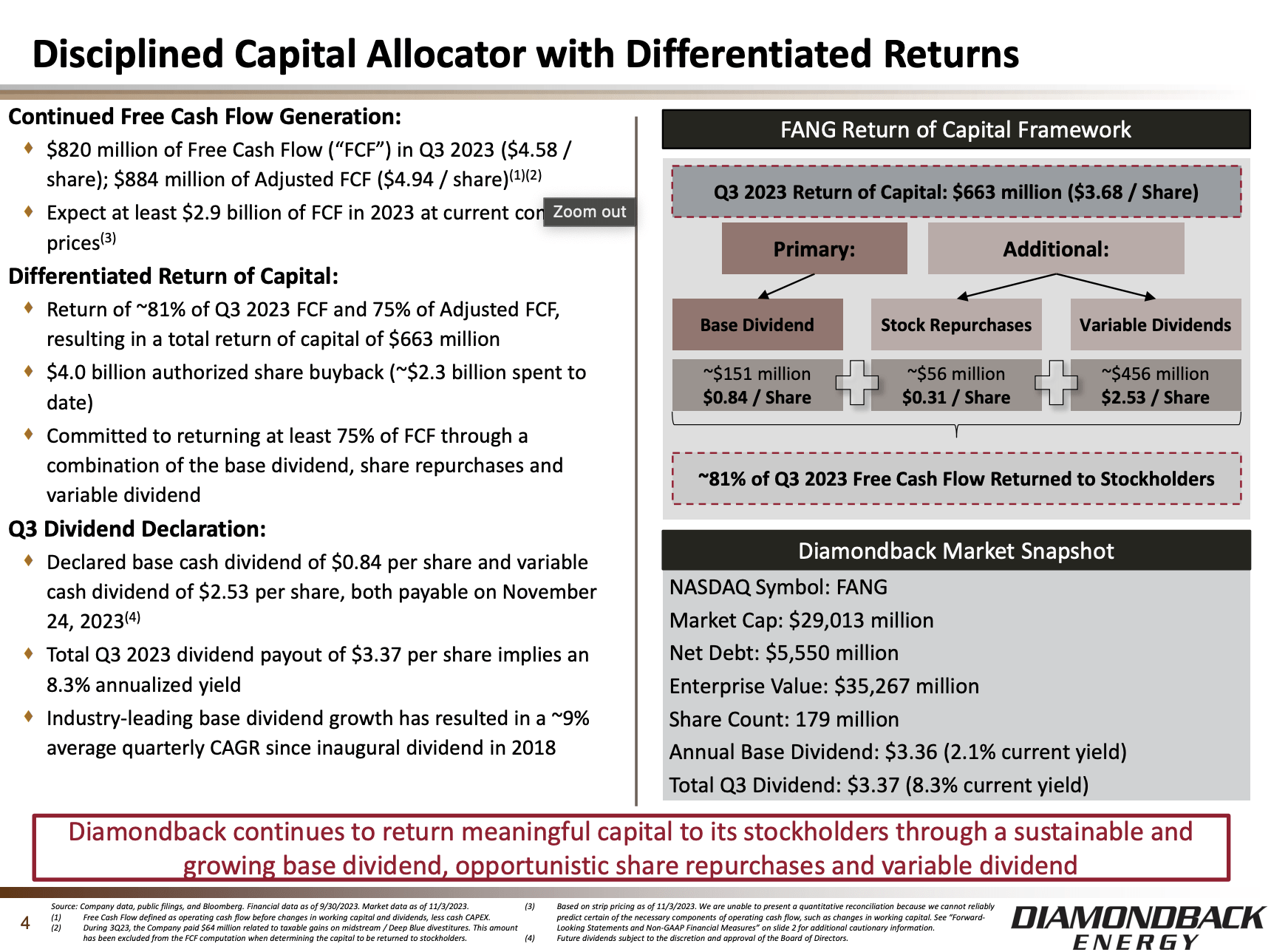

Before I continue to discuss how efficient FANG is, it has a strong focus on shareholder distributions.

- In Q3, Diamondback repurchased 406,700 shares at a cost of $56 million, with an eye on generating a low-teens rate of return.

- Repurchase opportunities were limited due to significant rallies in commodity prices and the company's stock.

- The dividend payout in the fourth quarter includes a base dividend of $0.84 per share and a variable dividend of $2.53 per share, amounting to a total cash dividend of $3.37 per share.

- The 4Q23 dividend translates to an annualized yield of 8.8% .

{kind=link}

As we can see below, the company is dedicated to returning more than 75% of its free cash flow to shareholders. This consists of a base dividend, protected at roughly $40 WTI, buybacks, and variable dividends.

Being able to sustain a 2.2% base dividend (using its current $153 stock price) at $40 WTI shows just how efficiently FANG is able to operate.

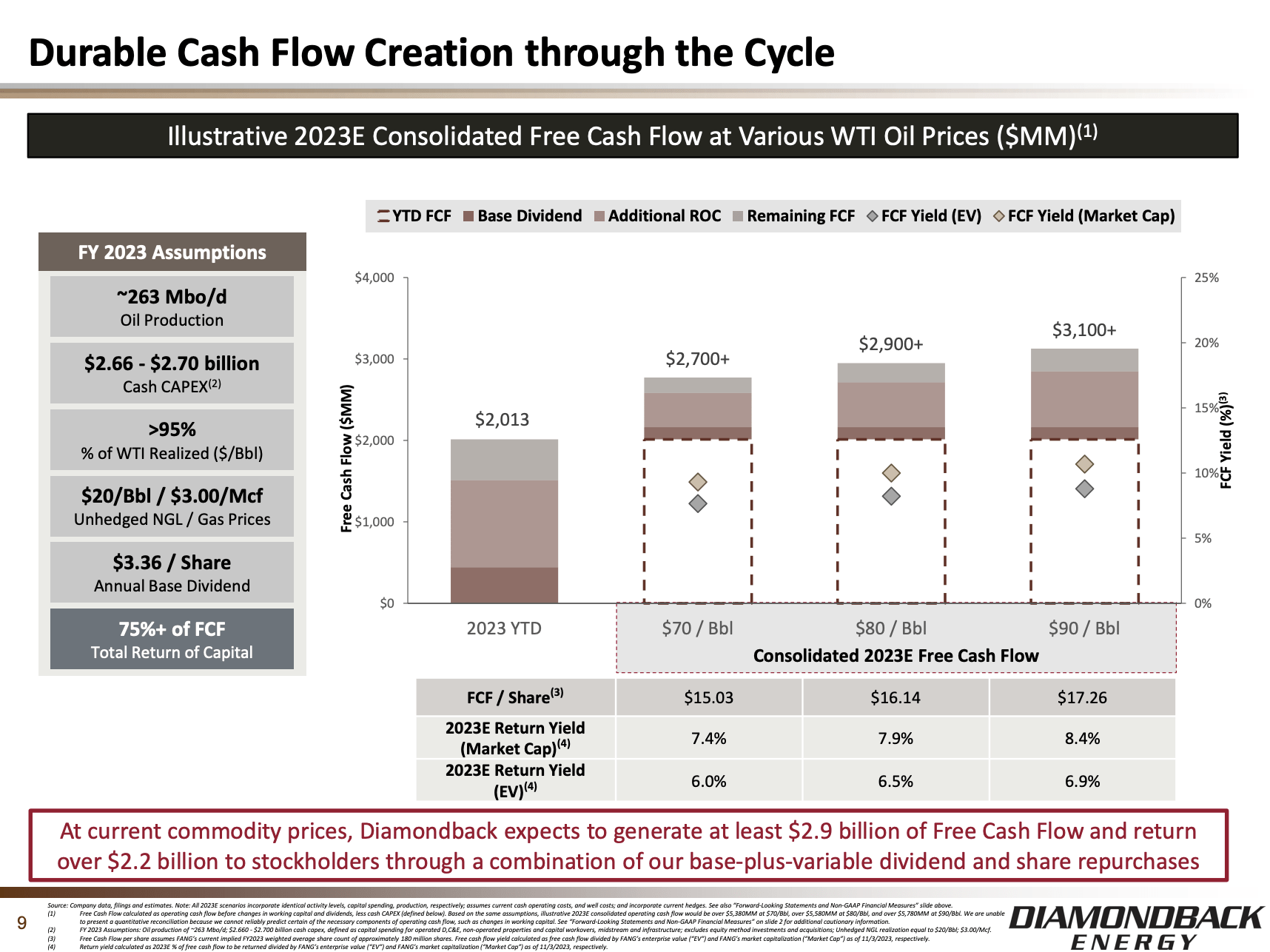

To show you how much distribution power this company has, we can use the overview below. Please note that the company's market was roughly 2% higher at the time this graph was made by the company, which means we can still use these numbers without having to do the math ourselves.

{kind=link}

Using the numbers above:

- At $70 WTI, the company has a distribution yield of 7.4%.

- At $80 WTI, the company has a distribution yield of 7.9%.

- At $90 WTI, the distribution yield exceeds 8.4%.

This bodes well for its valuation.

Not only can investors expect to receive juicy dividends at elevated oil prices, but the market never gave FANG the valuation it deserved.

Valuation

The most important part of the valuation is that I expect oil prices to remain at above-average levels on a long-term basis, with room to see triple-digit dollar oil prices once global economic growth improves.

This will likely unlock tremendous dividend flows.

The second point is that the stock never got the valuation it deserved.

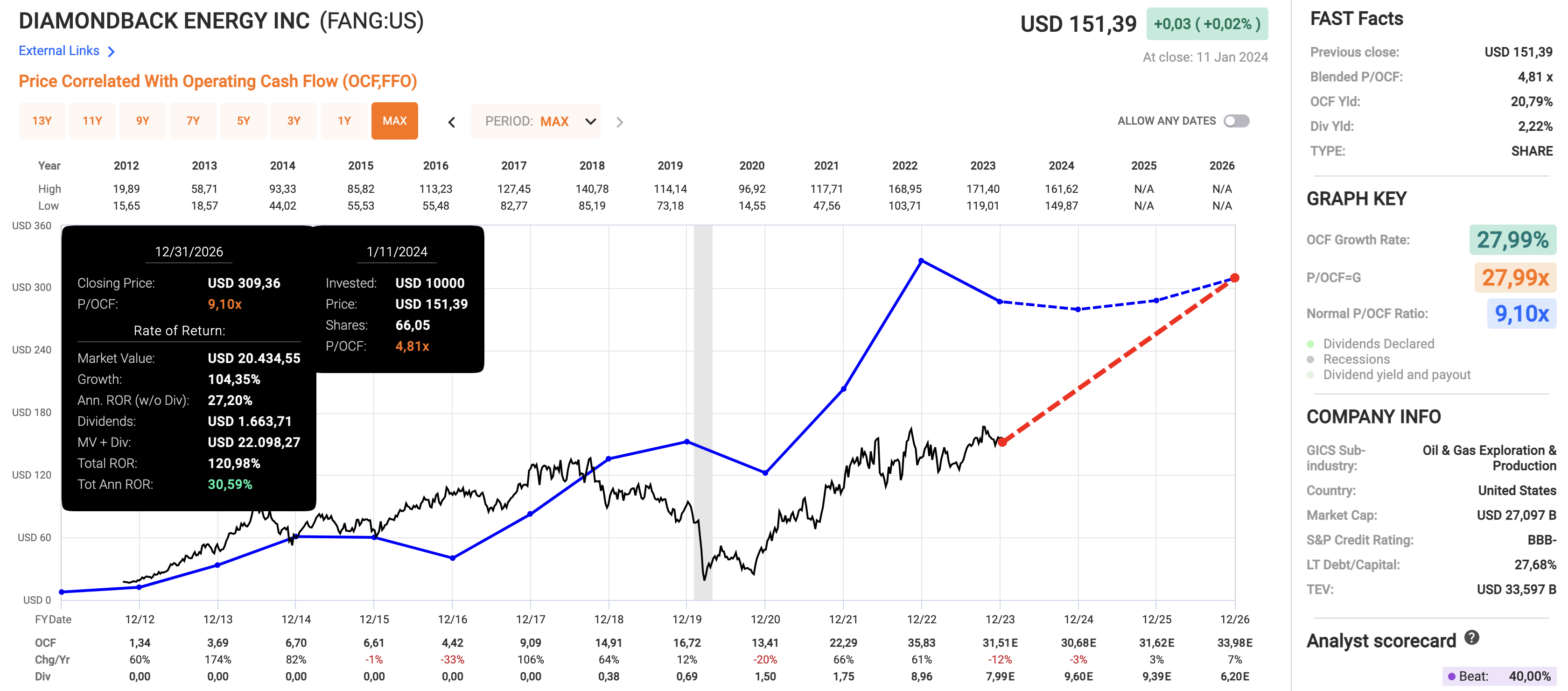

Using the data in the chat below:

- FANG is trading at a blended price-to-operating cash flow ratio of 4.8x.

- Historically, the stock has traded at roughly 9.0x OCF, which is in line with giants like Exxon Mobil ( XOM ).

- Technically speaking, a return to this valuation would give the stock a fair price target of $310, which is roughly twice its current price.

{kind=link}

I am not making the case that FANG will double this year, but it certainly trades at a very attractive valuation.

The moment global economic growth improves, I expect that investors will recognize how attractive oil equities are, which could push FANG toward $300 per share.

As I have significant energy exposure already, I am figuring out if and how FANG can fit into my portfolio.

However, the odds are I'll start buying FANG this year, as I really like the value this company brings to the table.

Takeaway

In a market poised for a shift towards value stocks, my focus on robust balance sheets and strategic investments led me to Diamondback Energy.

This North American energy giant, with a $27 billion market cap, boasts deep reserves, a stellar balance sheet, and efficient operations.

As I anticipate a bullish trend in oil, Diamondback's dedication to shareholder returns stands out.

With a strong dividend yield, buybacks, and efficient capital allocation, FANG's current undervaluation offers an enticing investment opportunity.

Positioned to outperform in the evolving energy landscape, Diamondback Energy remains a cornerstone in my portfolio for 2024.

For further details see:

Diamondback Energy: 8% Distribution Yield At $80 WTI, I Expect Strong Upside