REI - Diamondback Energy: Navigating The Fine Print

Summary

- Management is growing through acquisitions that have historically been accretive.

- Now management is also divesting noncore assets.

- Per share growth of earnings and cash flow is likely to continue despite the management's announced intention to maintain production (rather than grow it).

- The oil percentage of production is increasing as management expands into a less costly area.

- The Midland Basin offers competitive results with some of the more expensive Permian acreages but at less than half of some of those prices.

Diamondback Energy (FANG) has long had a growth history. But when the market demanded a return of capital, then management had to get creative to show growth. What has happened since fiscal year 2020 has been growth by acquisition. Diamondback has a very long history of making accretive acquisitions. Those acquisitions have long played a material part in the growth of the company. Therefore, it was only natural that management would turn to growth by acquisition when the market demanded a significant return of capital.

That has led to some benefits the market probably never saw coming. For as much as the market has demanded a return of capital, that same market loves a growth story. Those managements that cater to the short-term dividend demand while ignoring the long-term growth demand are likely to find their valuations reduced. But now the growth of Diamondback per share will come by divesting noncore parcels while acquiring good fit parcels. Production during this kind of activity may not change much, but this management will end up with a better grip on core acreage.

Unexpected Benefit

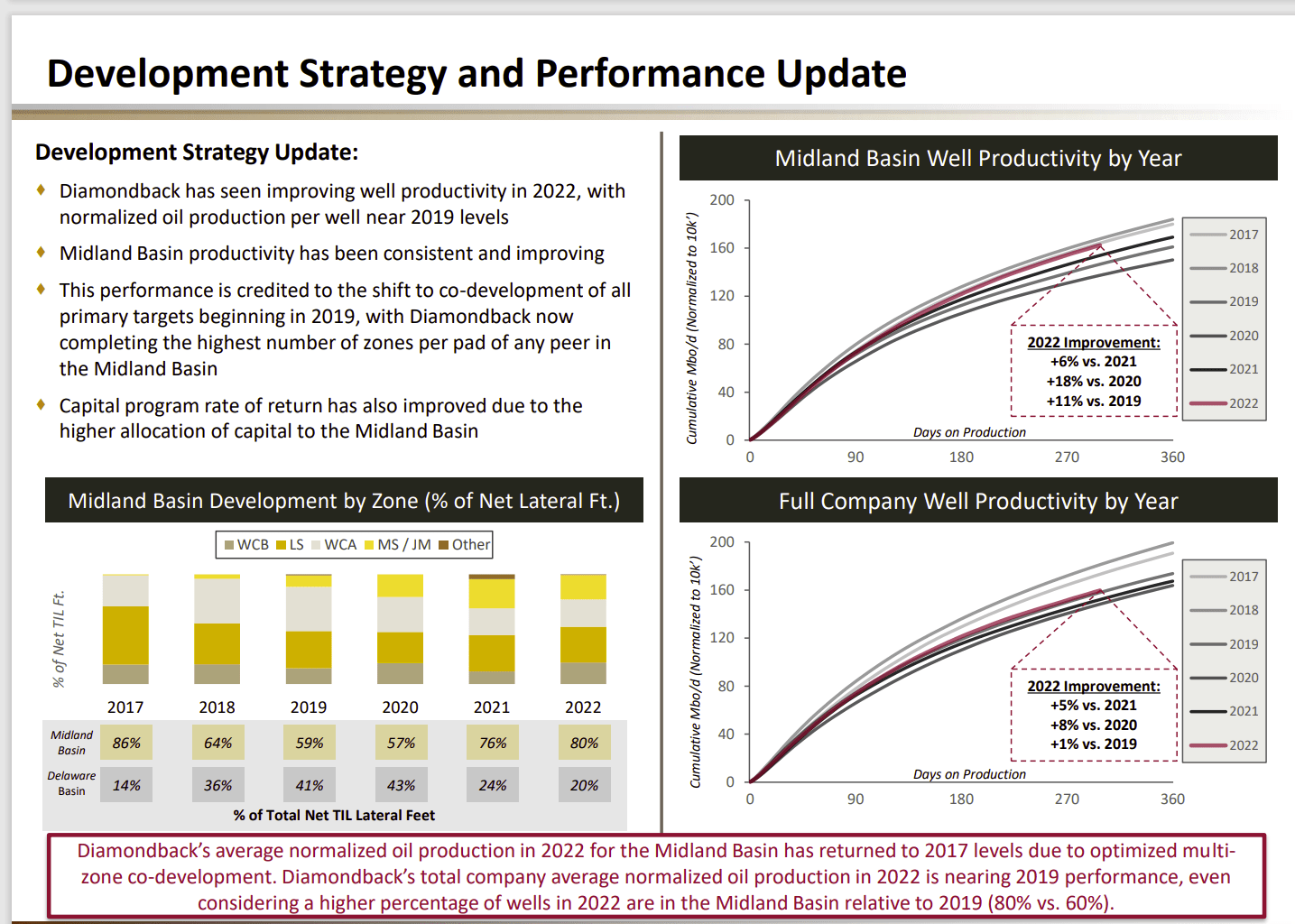

Management happened to mention that the percentage of oil production was rising. Since the Permian operators habitually decide whether or not to drill often by looking at the potential oil production with other liquids (and natural gas) as "icing on the cake", the results are often a surplus (and weak pricing) of "everything else". That means that a rising oil percentage of production probably has a long-term profit advantage.

Diamondback Energy Oil Percentage Of Production Progress (Diamondback Energy Corporate Presentation November 2022)

{kind=link}

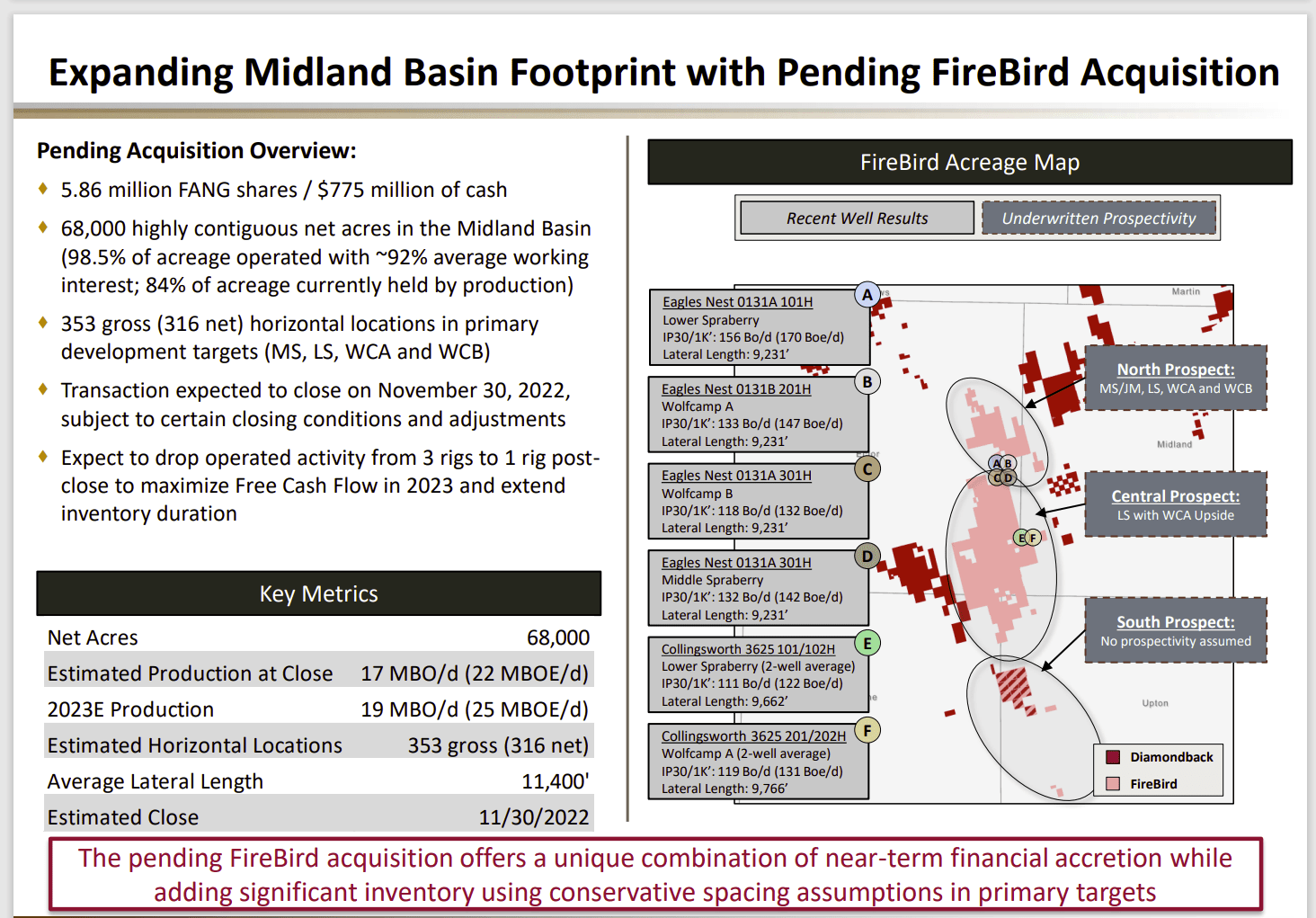

The move to the Midland Basin began a few years back with the usual notice of an acquisition. Now what is happening is a positive production mix variance due to that move. The Midland Basin has every bit as good a production history as the rest of the company acreage. But the acquisition costs are often lower (so far).

Diamondback Energy Presentation Of Midland Basin Acquisition (Diamondback Energy Corporate Presentation November 2022)

{kind=link}

Using a value of $160 per share, the total cost of the deal works out to about $1.7 billion (which is close to the company estimate). The rough price per acre is around $25,000. That is less than half of the price that acreage typically goes for in hot places like Reeves County (where prices in the past sometime got as high as $66,000 an acre). The stock price has since declined which makes the deal even better.

I follow a bunch of managements that operate in the Midland Basin. Some, like Laredo Petroleum ( LPI ), only recently acquired acreage in Howard County. There has been some concern with Laredo about production interference due to the neighboring drilling and completion activities. But that concern may change towards the value of the acreage when companies like Diamondback move into the area.

Others like Ring Energy ( REI ) have been in the Central Basin since inception. Ring Energy is yet another company that has found very profitable production in an interval that has largely been ignored. Diamondback Energy management is probably eyeing some of those results when the decision to expand in this direction was made. It is not unusual for a smaller company to "take the risks" before a larger company moves in to take advantage of "the rewards". These managements discovered that the acreage was relatively cheap. But the results were comparable with some far more expensive acreage.

Diamondback has long had some of the best acreage in the business. The only question was the cost to get it. Therefore, the expansion into lower cost acreage makes perfect sense when the results actually improve the production mix while the acreage appears to cost less than others were paying for "premium acreage".

Back in 2021, Pioneer Resources ( PXD ) was one of those competitors that paid "full price" for premium acreage. It also sold Midland Basin acreage to Laredo ( LPI ) for a fraction of the acreage price it paid in the acquisition. In this case, the acreage had a higher ratio of natural gas production than the primary Pioneer Resources acreage. But for Laredo Petroleum, that acreage was far more profitable to produce than was its legacy acreage.

The key to all of this is the location cost that is never shown to investors when a well breakeven is calculated. Anyone paying $60,000 per acre adds $6 million in costs to a well breakeven calculation when using 100-acre spacing. On the other hand, Laredo paid closer to $10,000 an acre for a larger percentage of natural gas production. That same 100-acre spacing would add a location cost of $1 million to the well-breakeven calculation. That lower amount can be surmounted by most wells to assure a decent corporate profitability.

The $6 million addition can only be surmounted by the most profitable wells in the industry. Usually what happens when companies pay that price is lower company returns on shareholder equity because the acreage is good but not that good. Then when the next cyclical downturn forces a revaluation due to the lower of cost or market calculation, there is often a big impairment to "clear the decks" and erase that high purchase price from future earnings.

Reserves

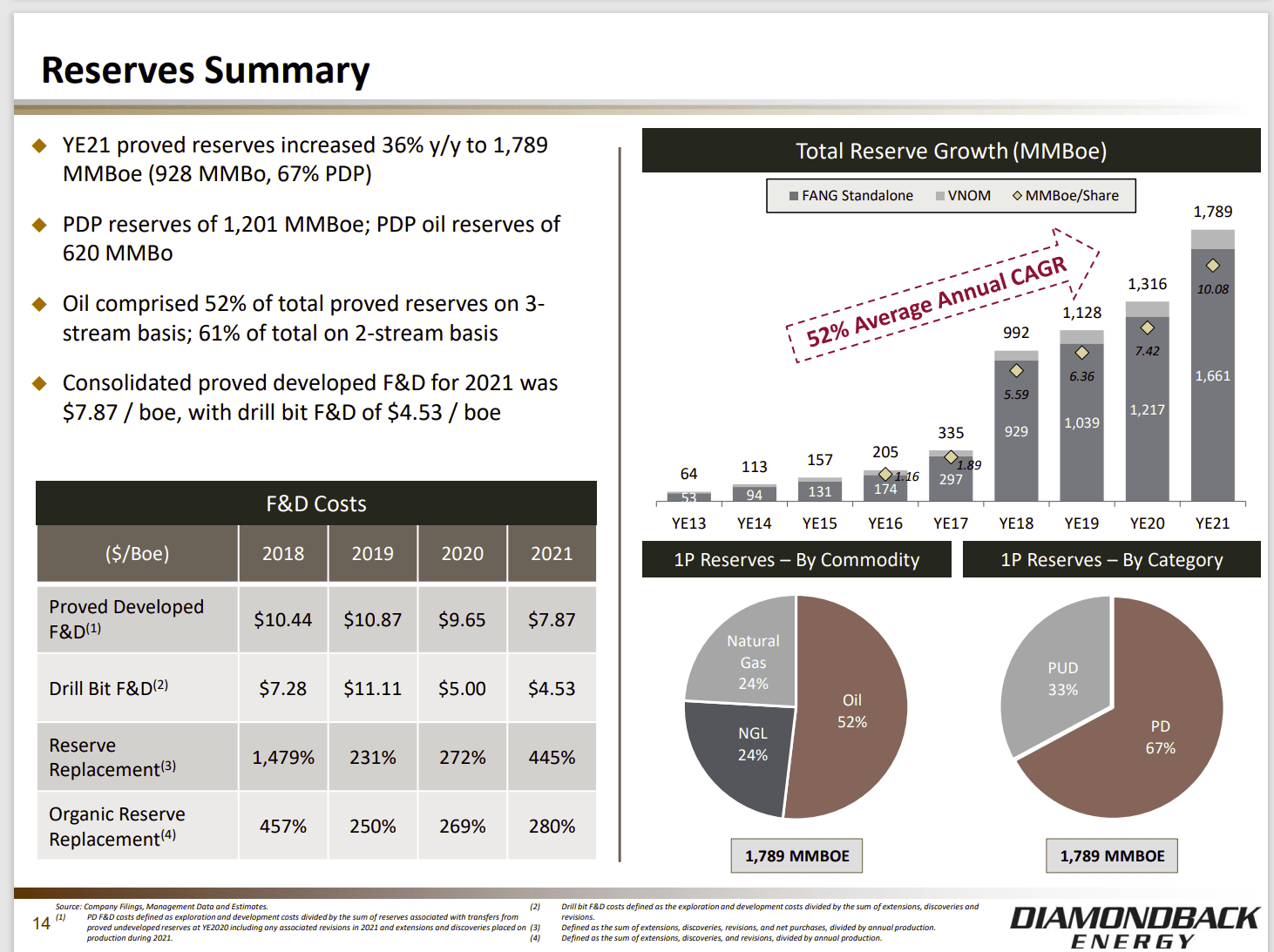

The effect of all the activity is that reserves are increasing right along with earnings and cash flow.

Diamondback Energy History Of Reserve Increases (Diamondback Energy Corporate Presentation November 2022)

{kind=link}

I have followed a lot of companies with great reserves and no cash flow. That is not usually a successful combination. Here, this company has grown earnings, cash flow, and reserves in tandem. Now the increasing reserves per share is a very believable story because earnings and cash flow per share are growing as well.

The growth story is easy to keep alive in the current situation because higher commodity prices assure a positive earnings comparison every quarter that Mr. Market just loves.

But clearly, management is looking ahead by divesting noncore assets (as in higher cost assets) while acquiring acreage that is likely to produce profit growth in the future. Management has a long record of doing this successfully. Therefore, earnings per share growth without the accompanying production growth is a likely outcome.

The Future

Management has had quarterly earnings that are multiples of the earnings in the previous quarter all year. Cash flow is now at a record. The company has achieved investment-grade ratings.

Now management needs to continue to navigate this market successfully. Clearly, the stock price approves of the actions of management. The acquisition program will make sure there is a growth story in the future that the market approves of. Clearly, the current stock price has baked in some management expectations that are not present in other competitor stock prices.

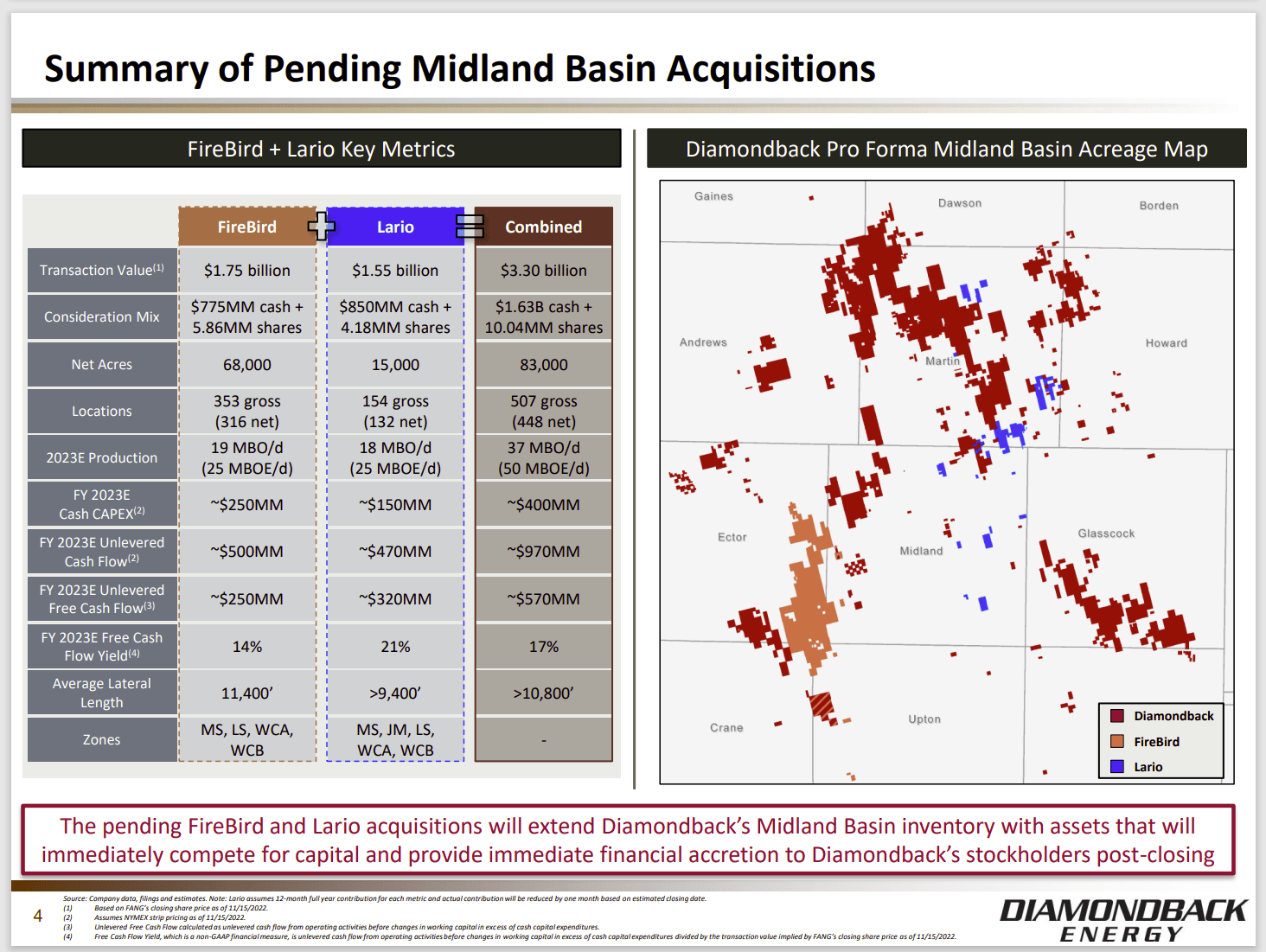

Diamondback Energy Summary OF Pending Acquisitions Towards The Central And Midland Areas Of Texas (Diamondback Energy November 2022, Acquisition Corporate Presentation)

{kind=link}

Clearly, management is moving into areas that some smaller companies I follow have long maintained are very profitable areas. Both Ring Energy and Laredo Petroleum are likely to become acquisition candidates if this trend continues. It should be no surprise that areas like this are more profitable. Location costs are getting to be far too high in prime areas to make acquisitions in those areas worth the effort. Good managements find cheap acreage that is likely to outperform market expectations. Clearly that is happening here.

This management has always outperformed much of the industry throughout company's existence. The lease operating costs are among the lowest I follow in the industry. The improvement in oil production will lead to wider margins in the future.

The expansion of Diamondback into more Central Basin acreage could be followed by others enough to push prices too high as was the case in other parts of the Permian. But for now, management is acquiring acreage at a good price. The strategy by management appears to have fairly low risk to shareholders with potential upside should this part of Texas become the next "hot spot".

There is always the risk of a bad acquisition or the risk of a sudden downturn in commodity prices that turns a bargain acquisition into an expensive one. But this management has a good enough record to interest a wide variety of potential investors. The stock is not as cheap as it once was. But given the tendency of management to grow per-share earnings, it still appears to be worth a look by potential investors.

For further details see:

Diamondback Energy: Navigating The Fine Print