VNOM - Diamondback Energy: Permian Pure Play Looks Well Positioned

2023-05-19 12:56:34 ET

Summary

- FANG is a pure play on the best oil basin in the U.S.

- With low leverage, the company has a very shareholder-friendly capital allocation plan.

- The stock valuation looks attractive at current levels.

As a Permian pureplay, Diamondback Energy ( FANG ) looks well-positioned to benefit from the medium-term positives in the oil market, while its shareholder-friendly policies are a nice bonus for investors.

Company Profile

FANG is an oil and natural gas E&P focused on the Permian Basin in West Texas. Within the Permian, it is primarily focused on horizontal drilling in the Spraberry and Wolfcamp formations in the Midland Basin and the Wolfcamp and Bone spring formations in the Delaware Basin.

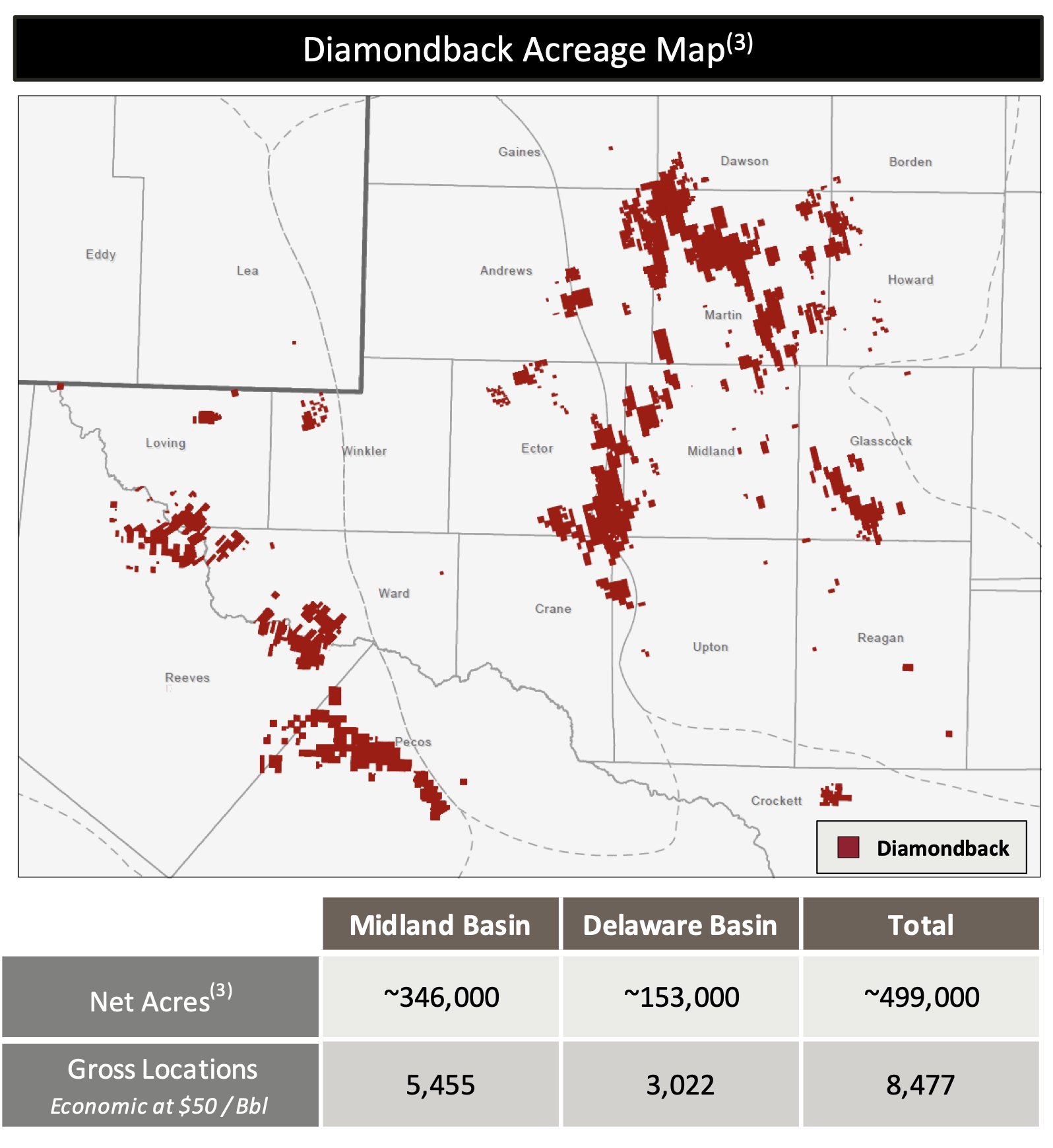

At the end of March, the company had approximately 499,000 net acres. About 346,000 were in the Midland Basin and ~153,000 in the Delaware Basin. It said it has identified 5,455 gross locations that are economic at $50 a barrel WTI in the Midland Basin, and 3,022 gross locations in the Delaware.

At the end of 2022, it had proved reserves of 2,033 MMBoe. 53% of its 1P reserves are oil, 24% NGLs, and 23% natural gas. 69% of its reserves are proved developed.

FANG also owns 56% of Viper Energy Partners ( VNOM ), as well as its GP. VNOM owns mineral interests in the Permian, of which nearly 60% are operated by FANG.

The company bought back its midstream operator, Rattler, last year. Its midstream assets now consist of 770 miles of crude gathering pipelines as well as an integrated water system. It also owns interests in numerous midstream JVs.

{kind=link}

Opportunities and Risks

Energy prices are not surprisingly the biggest driver for an E&P such as FANG. Oil prices play the largest role in its results, as the company's oil hedges are mostly to minimize extreme downside while not limiting any upside.

The company also produces associated natural gas. The Permian can often see very low natural gas prices, especially given natural gas takeaway constraints. In fact, Waha natural gas prices turned negative earlier this month.

However, FANG has hedged about 65% on its 2023 and 70% of its expected 2024 natural gas production using Waha basis swaps, which it says 100% protects it from Waha basis blowouts in 2023. The company expects continued price weakness at Waha through 2024. It expects to get Gulf Coast Pricing on about 33% of its natural gas production. It also has 60% of its 2023 gas production hedged with a floor of $3.17 in Q1 and $3.18 in the second half.

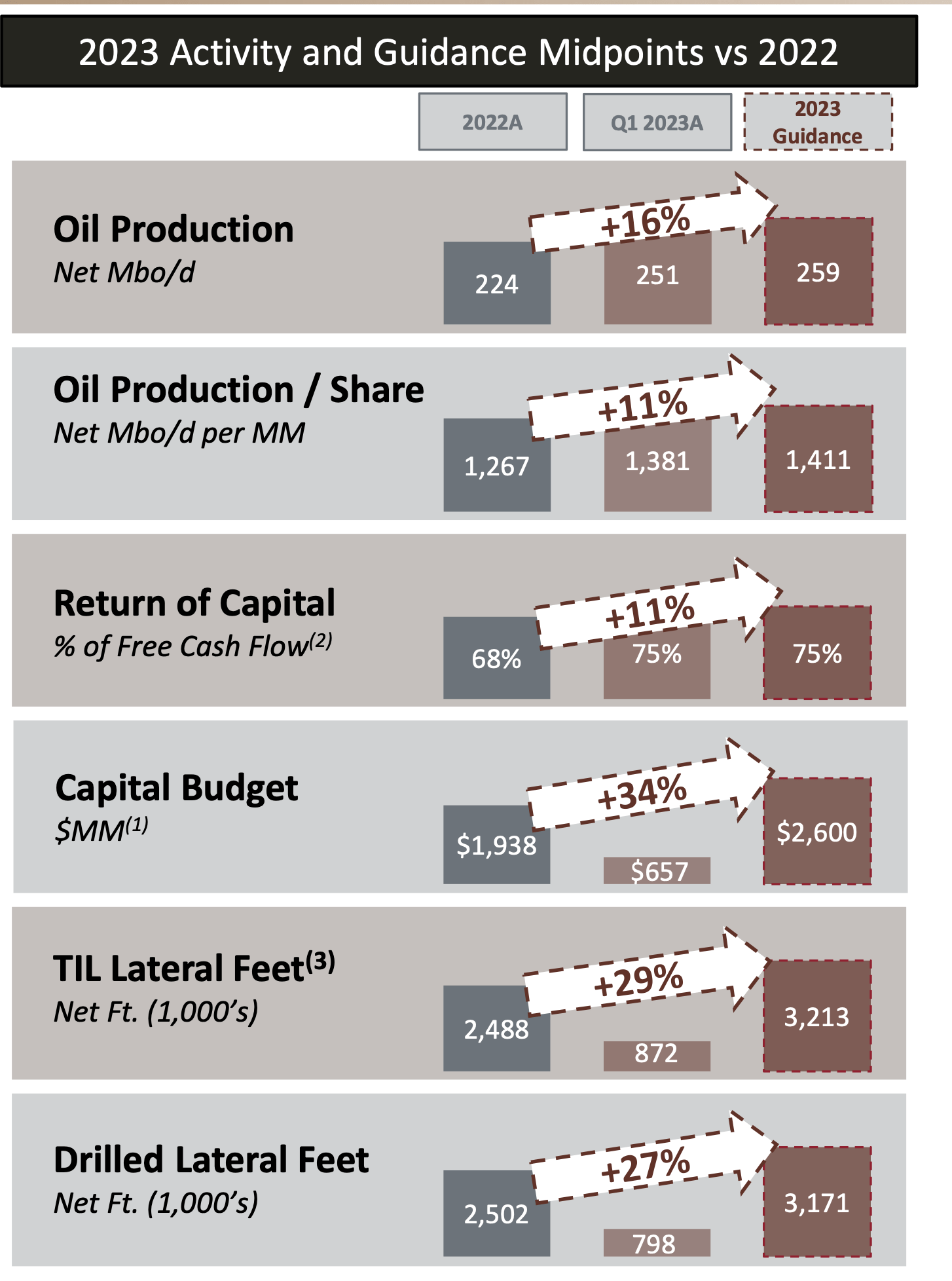

Notably, the Permian is considered the best oil basin in North America, with most of the U.S.'s oil production increases expected to come from the basin. For its part, FANG is mostly a Permian pure play. It is projecting its oil production to increase 16% this year, mostly coming from its recent acquisitions of Firebird and Lario, which combined adds production of 37 MBbls/d (or 50 MBoe/d).

{kind=link}

In addition, FANG and other operators are beginning to see service costs and other expenses start to flatten and, in some cases, come down.

Discussing its cost outlook on its Q1 call , CEO Travis Stice said:

"The read through to that question is kind of what the CapEx is going to look like in the back half of the year. .. But when we talk about deflation, that's from raw materials, it's diesel, it's sand, steel, particularly on steel because we're buying our steel needs multiple quarters in advance. So we know what that steel cost is. And it's already down for the future purposes $20, $25 a foot. And then we've also got the rigs, we talked about dropping, we are going to drop a couple of rigs and that allows us to look at our entire rig fleet and the costs associated with those rigs and we see rig costs are coming down as well. And then lastly, while it's not necessarily a CapEx issue, we're seeing improved efficiencies as we've got the second e-fleet that started last week. And we've also got rid of our 2 spot frac crews and replace them with 1 simul-frac crew. So we're seeing $10 to $20 a foot efficiency gains there as well.

So regardless of what's going on with CapEx, our commitment has always been to be the low-cost leaders when it comes to [executing] our development plan out here."

A bit unique to FANG is also the opportunity to divest its interests in a number of midstream projects, which it acquired when it bought Rattler. It expects to sell at least $1 billion in non-core assets by the end of 2023. It's already sold its 10% interest in the Gray Oak crude pipeline, as well as some non-core acreage.

FANG is also a very shareholder-friendly company, which is looking to use its prolific free cash flow to buy back stock, pay a base and variable dividend, and keep a low level of debt. The company ended the quarter with trailing twelve month leverage of 1.0x. While its net debt crept up a bit in Q2 due to the Lario deal, it expects net debt to decrease in Q2.

The E&P repurchased $332 million in shares at a weighted average price of $131.34 in Q1, and at the start of May, it had also bought back another $72 million in shares thus far in Q2. Since the initiation of its buyback program, the company has spent nearly $2 billion buying back almost 16 million shares.

The company also declared an 80-cent quarterly base dividend and a 3-cent variable dividend. The current yield based on its base dividend is about 2.5%.

Outside of energy prices, which can be influenced by the economy, supply-demand, global, and political factors, basin risk is probably FANG's biggest risk. When it comes to the Permian, the biggest issue is a lack of natural gas takeaway, which can impact drilling activity. New long-haul projects coming online this year are expected to help relieve this issue, but it is something that has plagued the basin for a while.

Valuation

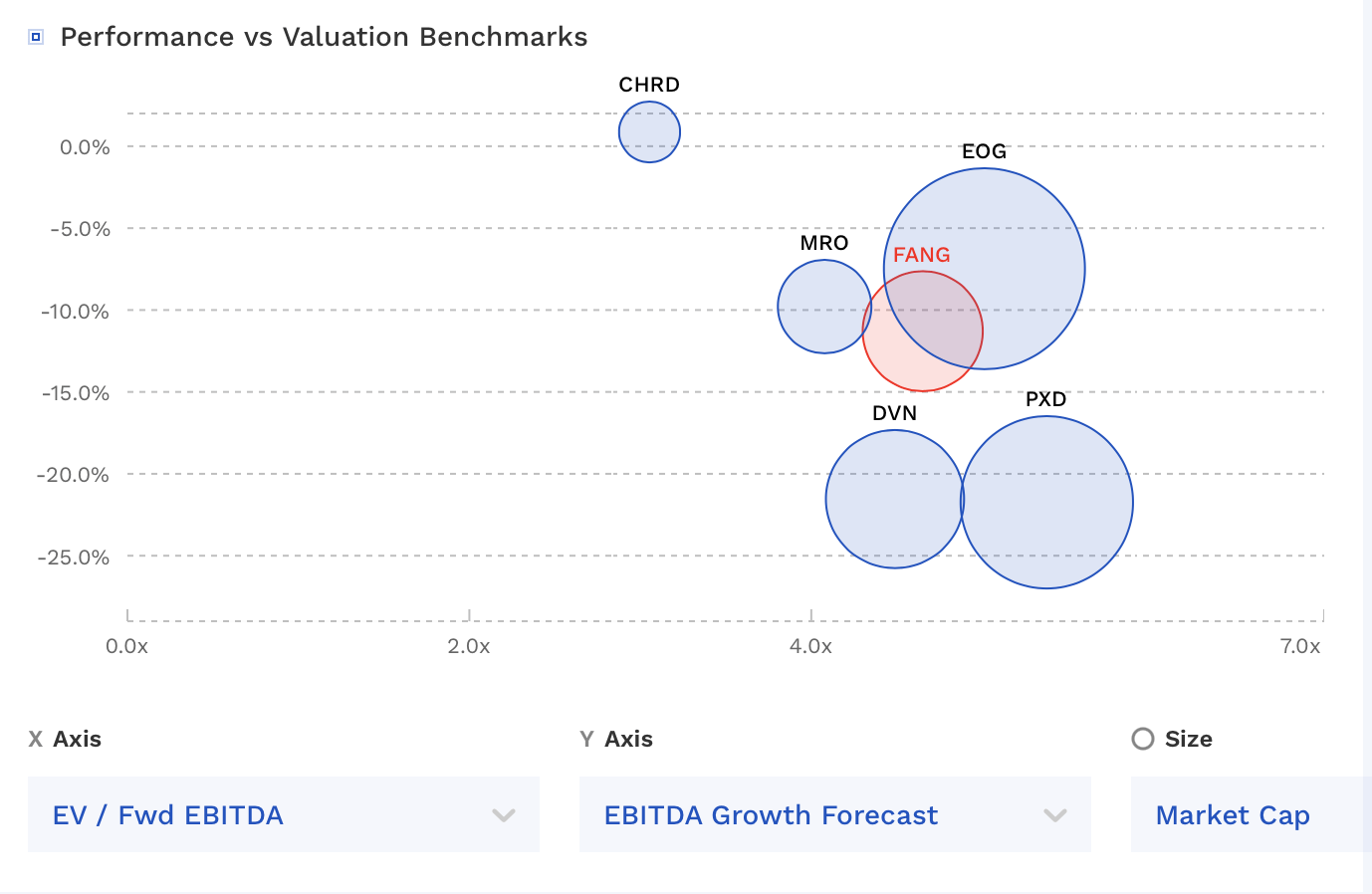

FANG trades at 4.7x EBITDA based on 2023 analyst estimates of $6.4 billion. Consolidated EBITDA in 2022 was around $7.2 billion, reflecting higher energy prices.

Based on the 2024 consensus of $6.9 billion, the stock trades at a 4.4x multiple. Of course, the price of oil and natural gas can change the actual results immensely.

FANG is valued in the middle of the pack compared to other independent E&Ps, despite its strong asset position in the Permian.

{kind=link}

Its stake in VNOM is worth about $1 billion.

Conclusion

I continue to be an oil bull in the medium term, as I think a more forceful OPEC, re-opening China, depleted U.S. strategic reserve, and current geopolitical climate all bode well for the commodity, along with underinvestment in the industry by oil majors. A bad global recession is a risk, although at this point I'm expecting a more moderate recession.

For FANG specifically, I like the stock as a Permian pure play, as well as its solid balance sheet and shareholder-friendly capital allocation policies. Meanwhile, the company has hedged out one of its bigger risks with Waha natural gas prices.

Once Permian natural gas takeaway constraints are alleviated, the Permian is set to be the major growth driver for U.S. oil production over the next decade. That puts FANG in an enviable position as a Permian pure play. As such, I think the stock is a buy at current levels.

For further details see:

Diamondback Energy: Permian Pure Play Looks Well Positioned