FANG - Diamondback Energy: Strong Q3 Free Cash Flow Makes Shares Attractive

2023-11-07 06:58:03 ET

Summary

- Diamondback Energy has strong assets in the Permian Basin and delivered strong results in Q3, and despite recent industry M&A, I view a deal as unlikely.

- The company's production has increased, with oil production expected to rise further in Q4.

- Diamondback has a strong balance sheet, generates solid cash flow, and has a powerful capital return policy, making it an attractive investment.

Shares of Diamondback Energy (FANG) have been a mixed performer over the past year, essentially treading water. The company does have premiere assets in the Permian Basin, which delivered strong results in Q3. For this reason, its name is bound to get speculation amidst the recent wave of energy M&A activity. With a pristine balance sheet and strong capital return policy, I see further upside in shares, even though I do not expect it to be acquired in this current wave of M&A.

{kind=link}

In the company's third quarter , Diamondback earned $5.49 in adjusted EPS. Production has risen strongly, aided by asset optimization activity, at 266mbo/d from 224mbo/d last year. Oil production will be up 18% this year at 263mbo/d, up from 260-262mbo/d previously, even as management kept cap-ex guidance steady, thanks to greater well productivity. Oil production per share was up 16% from last year.

In a world of elevated inflation, it is noteworthy that Diamondback is actually bringing operating expenses down. Cash operating costs were down by $0.15 in the quarter at $10.51, down from $11.97 last year. This contributes to industry-leading cash margins and solid cash flow, even as oil prices fell in the quarter to $81.57 from $89.79.

In the fourth quarter, oil production should be 269-274mbo/d even with cap-ex down about 8% from Q3's $684 million level. This is aided by the fact that in Q3, FANG drilled 75 wells but only completed 71, adding to its inventory of drilled and uncompleted wells, which are now relatively inexpensive to bring online. As they come online, we will see the production benefit from this quarter's capital spending.

FANG delivered strong production, which is allowing it to raise guidance, and production will rise further in Q4. It also has brought down cash costs while its cap-ex program continues to generate gains, drilling more lateral feet, and getting more oil out of wells more quickly. It is controlling what it can well, and while commodity prices have fallen, they remain at favorable levels, with management guiding to $2.9 billion of full year free cash flow if current commodity prices hold.

This is critical because Diamondback is really a free cash flow and capital return story. The company generated $884 million of adjusted free cash flow, or $4.94 per share. This was $1.17 billion last year as oil prices and natural gas prices have fallen, with natural gas down over 65%. If you recall, last year, natural gas prices surged as Europe scrambled for LNG to fill up inventories as it turned away from Russian oil. As some of these pressures have faded, prices have normalized.

While free cash flow has fallen, it remains at a healthy level. FANG maintains a simple and powerful capital allocation policy. First, it buys puts to hedge downside commodity risks at $55/barrel while retaining upside as oil prices rise. It aims to have about 60% of current production hedged. It does this to ensure its primary dividends is sacrosanct. This base dividend is set to be sustainable even at $40 oil, and it runs at $0.84/quarter. This provides investors with a 2.1% yield they can "count on" through upturns and downturns. It is set quite conservative, just to ensure management does not ever have to go back on this commitment.

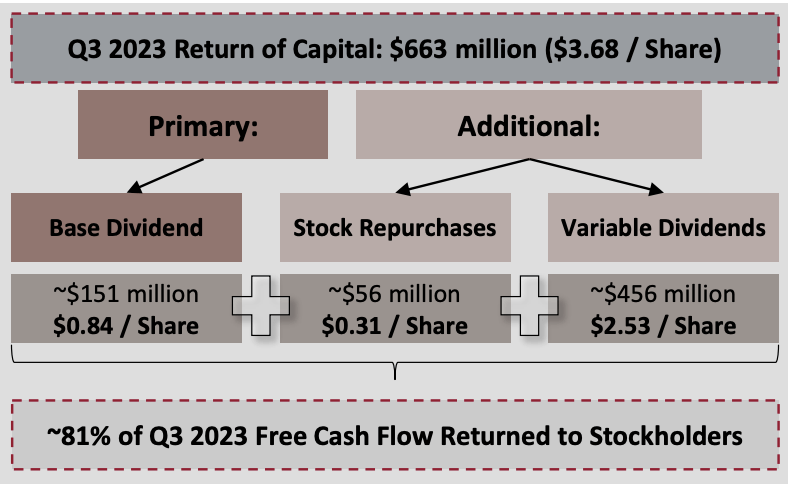

Beyond that, FANG seeks to return 75% of its free cash flow to investors. With oil prices well above $40, that leaves a lot of extra cash flow for buybacks and special dividends. This quarter Diamondback will pay out 81% of this to shareholders. As you can see below, beyond the base dividend, it declared a special dividend of $2.53 and also bought back $56 million of stock. It has $2.3 billion remaining on its buyback authorization. The combined dividend yield is 8.3%, annualized.

{kind=link}

This year, FANG has done $741 million of buybacks, so this quarter was notably lighter on buybacks in favor of dividends, which coincides with shares having steadily risen. Management frames its buybacks as "opportunistic," so in share price downturns, you will likely see variable payments shift towards repurchases and vice versa during rallies. I view it as a positive that management maintains flexibility in its payout structure to try to deliver the most accretive capital returns for investors.

With full year and Q4 run-rate free cash flow both running about $2.9 billion, FANG has an about 10% free cash flow yield at its current share price. I view this as an attractive level for this company. First, Diamondback has a strong balance sheet. Net debt is $5.5 billion, down $1 billion in the quarter. Net leverage is just 0.9x based on trailing 12 months EBITDA, and 0.8x on Q3 annualized. Given the cyclicality of this industry, I like to see leverage at or below 1-1.5x. FANG has achieved this, which is why it can focus its free cash flow on reward shareholders.

It also must be emphasized that Diamondback is generating this much free cash flow while spending enough on cap-ex to sustain and grow its oil production. As such, even if oil prices stay constant, free cash flow should rise over time. Of course, if you expect prices to fall significantly, you likely should avoid FANG (and E&P companies more broadly) as its free cash flow will move with oil prices. Personally, I expect prices to at least maintain around current levels, if not rise over time, given the fact oil consumption is still rising and cap-ex spending has been low for several years , which will restrain production growth.

With strong cash returns, production growth, and a favorable commodity setup, I view a 10% free cash flow yield as attractive and likely to produce double-digit returns for investors, just through dividends and buybacks. When thinking about upside scenarios, M&A naturally comes to mind. Pioneer Natural Resources (PXD), another firm with stellar Permian assets, is being acquired by Exxon Mobil (XOM), and this year it should generate about $4 billion in free cash flow based on year to date results, giving its stock a below 7% free cash flow yield at the deal price.

At Pioneer's valuation, FANG would have 43% upside. Now, that is upside unlikely to be achieved through public markets alone-it would require M&A. The problem is with Exxon and Chevron (CVX) having announced deals. It is unclear who is big enough to afford the $40 billion FANG would command. ConocoPhillips (COP) is likely the only US player large enough and has a " high bar" for M&A. While Devon Energy (DVN) may be looking at M&A, it is smaller than FANG. Ultimately, in a few years, Chevron or Exxon may once again do a deal and look at FANG, but with them sidelined, I do not see a natural buyer for the company.

I view fair value on the public markets as being about an 8% free cash flow yield. That would provide a 6% capital return yield, which combined with modest production growth and oil price appreciation over time, should lead to mid-single digit cash flow growth and 10+% returns over time. That gives shares about 25% upside to $192. In the oil sector, strong capital returns are crucial, and FANG meets this test clearly, making the stock a buy.

For further details see:

Diamondback Energy: Strong Q3 Free Cash Flow Makes Shares Attractive