OXY - Diamondback Energy Went Midland Before Midland Was Cool

2023-12-12 07:46:38 ET

Summary

- Occidental Petroleum wins bid for midland properties, following the strategy executed by Diamondback Energy and Vital Energy.

- Midland Basin attracts attention due to lower prices for acreage compared to the Delaware Basin while producing as profitable results.

- Diamondback Energy was the first to pursue accretive acreage in less focused areas, resulting in less buying competition, better prices, and now more profitability.

- The Diamondback location cost will likely be the lowest cost unless a company pursues the Vital Energy small company strategy.

- All three companies win by staying in their own lane.

It is often stated that imitation is the sincerest form of flattery. If that is the case, then in the business world, that flattery is likely to result in a cost advantage to the company that went first. Today, Occidental Petroleum (OXY) made the headlines by grabbing the winning bid for some midland properties. But Diamondback Energy (FANG) and Vital Energy (VTLE) were executing this idea a few years before this and likely were using considerably lower energy price assumptions to make it work as a result. The strategy that Vital Energy used (as you will see) was likely too small to have an impact on a company the size of Occidental. But Diamondback did far larger deals that paved the way for a lot of activity that followed.

General Midland Basin Attraction

The Midland basin, as I have covered for a few years now, has every bit as good, reported results for the far more expensive Reeves County and Delaware Basin. The result is that companies looking for acreage likely overpaid for those great results or were priced out of the area. It even got to the point where the very fast growth led to takeaway issues to the point that the product was discounted significantly below posted prices to get it to the market.

This led to perceived basins like the Eagle Ford outperforming operators without the takeaway capacity available. When that happens, then operators start looking elsewhere for good profits to both grow and diversify. No one wants to be the one that "came too late to the party" to make a decent profit. Commodity markets forever have shifting areas that make "the most profits". But that often depends upon who got there first before prices rose.

True profits get complicated by the fact that operators almost never report the location cost in the well breakeven calculations. That makes it hard for investors to get from well profitability to corporate profitability. There is a link between those two, but other factors cloud the relationship for most investors.

The result is that the Midland Basin, with what has been lower prices for acreage, has been attracting more attention than the Delaware Basin. If anything, this will likely bring Delaware Basin prices such as Reeves County locations down to reality.

For investors, the expectation of rotation of locations to new "hot areas" will continue as it has in the past. Technology keeps advancing which geology and area is the most profitable.

Diamondback Was First

Diamondback Energy has long grown by acquisition. The key difference is that the company rarely considers acquisitions in the current market because the prices are a good deal higher than the company was willing to pay.

Therefore, Diamondback keeps looking for accretive acreage in places where the market is not focused upon. That results in better prices and accretive acquisitions at those lower prices. Oftentimes, the corporate breakeven is lower and the profitability is higher.

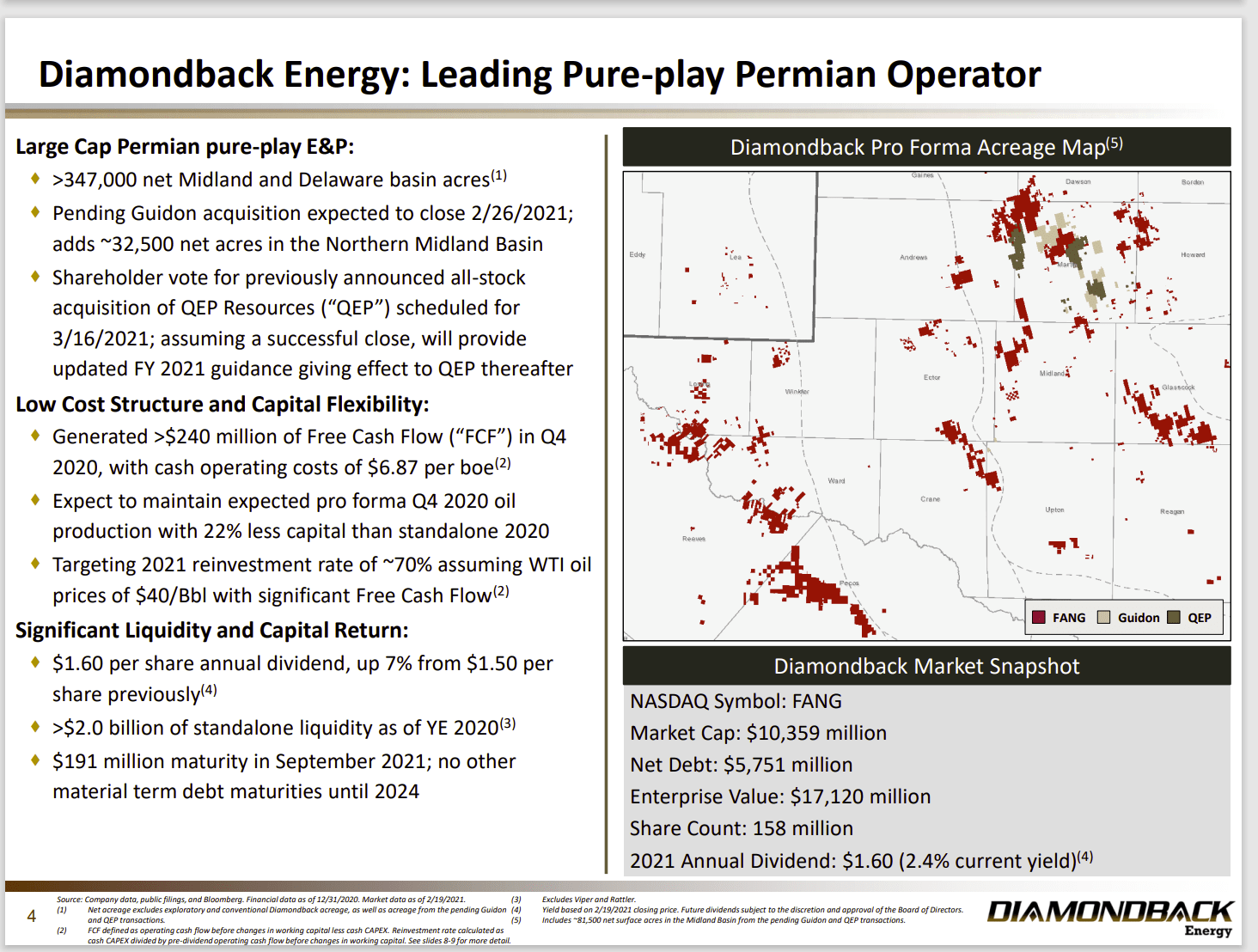

Diamondback Energy Pending Guidon Acquisition With Map Of Guidon and QEP Acquisition Acreage (Diamondback Energy February 2021, Investor Presentation)

{kind=link}

This is a sample of one of several presentations for acquisitions made back around 2021 involving Midland acreage. Diamondback Energy actually ended up with significantly more acreage before the commodity price peak in early fiscal year 2022.

Investors can just bet that those great commodity prices in fiscal year 2022 raised the return on that series of acquisitions above what many figured the returns would be.

The other idea is that acquisitions announced in 2020 and 2021 were done with much more conservative thinking (or parameters) than is the case now. Diamondback was one of very few "shoppers" at the time. On the other hand, there were a whole lot of sellers that were "fed up" with the industry and ready to "move on".

Even more importantly, Diamondback management was far more unlikely to get caught in bidding situations. Instead, the management was "in the catbird seat" of having a lot of sellers trying to unload acreage with very few buyers because of all the financial damage done to the industry by the challenges of fiscal year 2020. Management was in the position of being able to bargain hard for sales prices as sellers competed with one another.

Admittedly, Diamondback Energy used stock to keep leverage at safe levels (and keep that investment grade rating) because no one knew that fiscal year 2022, particularly the second quarter, would arrive with sky-high commodity prices. But then again, a lot of very good managements build companies by betting on operational leverage rather than financial leverage. That is the exact opposite of many investor comments I receive.

Vital Energy

Vital Energy was likewise shopping in the midland area.

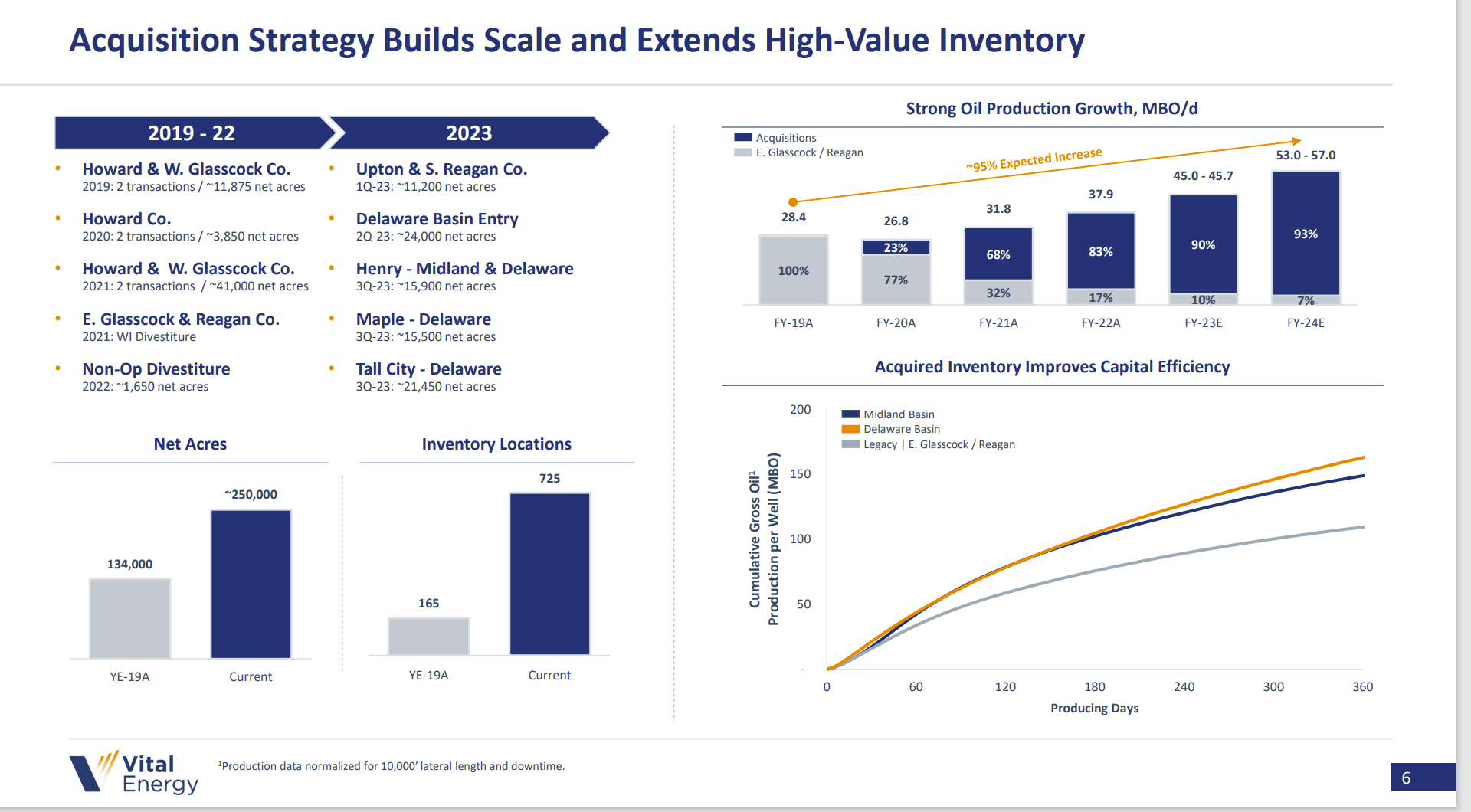

Vital Energy Acquisition History (Vital Energy Corporate Presentation November 2023)

{kind=link}

Vital Energy began purchasing subpar holdings for a big discount from an already cheap market. Vital also targeted distressed or unnatural sellers. This is a very small that executed the Diamondback Energy strategy in a way suitable to a much smaller company with far less buying power.

The Howard County acquisitions in the beginning, for example, had to be small and the prices were less than $10K an acre in many cases if you go back to my older articles on this. Then came a significant purchase that was likewise small, but it was "bolt-on" in that it made a decent roughly 30K acreage position in very profitable Howard County which made all those little pieces far more valuable than they were to the sellers.

Vital has continued to "stay out of the way of the big boys" to purchase smaller positions as it enters new counties while consolidating what it has into more profitable holdings. The result of this is a far more profitable company going forward with far more cash flow than was the case in the past.

Occidental Petroleum Follows

Now comes Occidental Petroleum with a deal to purchas e Crownrock for roughly $12 billion. Occidental can make this deal work because of its size that builds efficiencies not necessarily available to the first two companies discussed here. For example, this is way out of consideration for Vital and it would be crazy for management to even try.

Diamondback would likely be in the bidding for this acreage except for the fact that the company management has a contrarian strategy to purchase acreage either when no one else is buying or what no one else is buying. That likely means that Diamondback would easily be outbid in a situation like this because they have better offers in places Mr. Market is not focused upon . By the time Mr. Market thinks about it, Diamondback is closing up shop and moving on to the next unpopular location.

In the meantime:

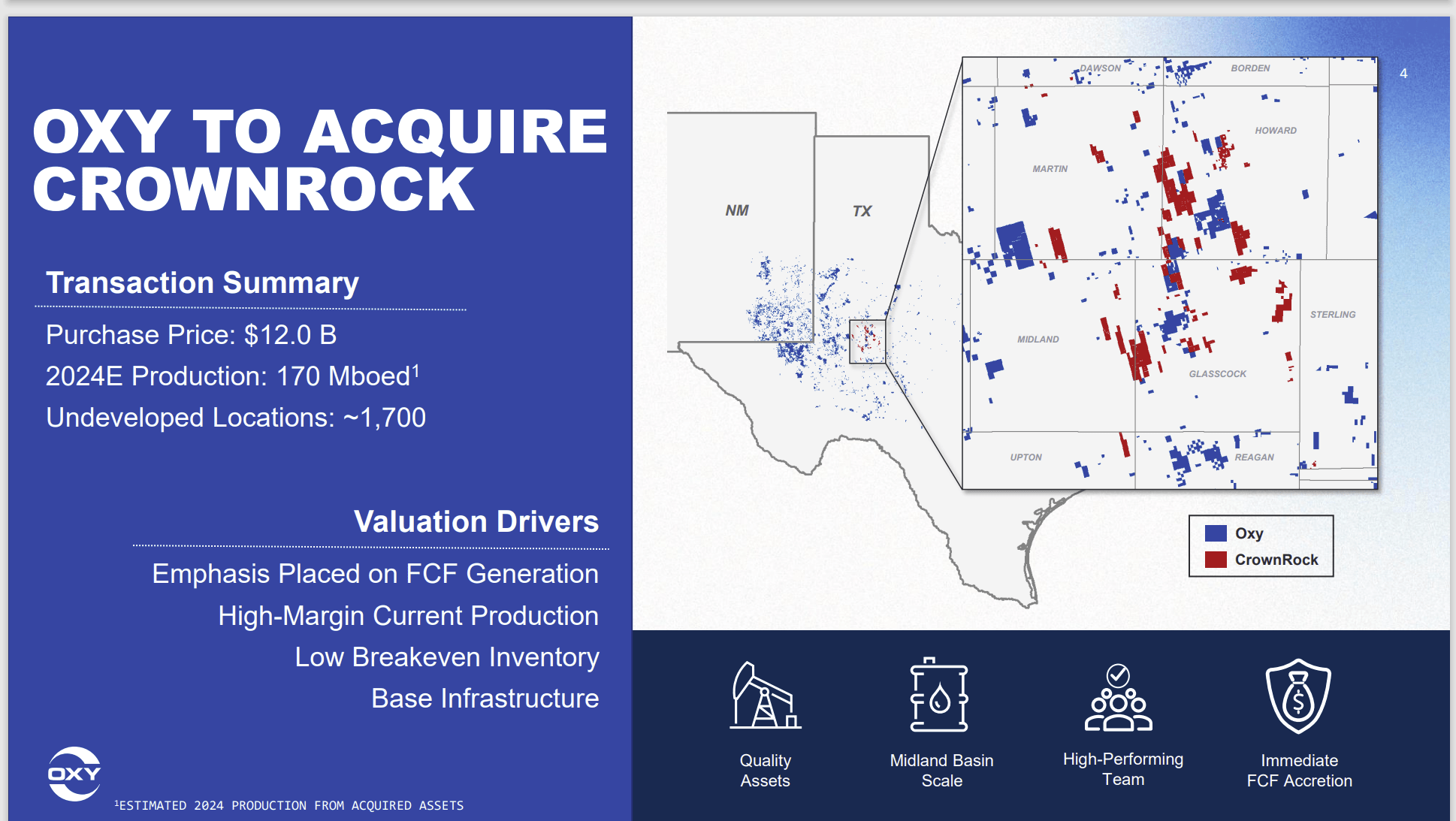

Occidental Summary Of Crownrock Acquisition (Occidental Petroleum Presentation Of Crownrock Acquisition)

{kind=link}

Oftentimes, the large companies get the best acreage because they have the resources to bid on the best acreage and win the bidding process. This acreage is every bit as good as the acreage that the first two companies bid upon. But the first two companies paid far less.

This deal is going to top $120K an acre. The other two companies paid roughly one-fifth of that price or less on their deals (with some exceptions of course). Admittedly you have current production and infrastructure. But so did the other deals.

The problem Occidental has is the sheer size demands big deals to "move the needle". I honestly think this deal will move the needle in the right direction for Occidental.

But you can bet that management had to use higher assumed oil prices for this deal to work than was the case for the other two companies.

Conclusion

Diamondback Energy "got there first". Diamondback had the best balance sheet at the time and could shop when "no one could shop" in one of the best buyers' markets in recent memory. Not only were sales conservative, but there were buyers ready to "give up and move on". Diamondback management likely got its choice of deals. In fact, management probably bargained a lot of sellers down to pick the best deal at prices today's buyers could only dream about.

Vital Energy did even better by beginning with subpar holdings that "no one wanted" and piecing them together into what is now a viable (if small) profitable Howard County holding while going on to build other profitable acreage holdings while this buyers' market lasts.

Occidental wins by purchasing the best acreage and then making it perform better than anyone else can. Occidental needs big deals to make a material improvement to its outlook and this is a "big deal".

All three companies will swap acreage to improve contiguous holdings. This is most significant for Vital Energy where just a few acres can still make a big difference. Diamondback needs to do a whole lot more swapping (and they appear to be doing it too).

Diamondback Energy has the size and the NYSE listing to benefit the most from the acreage it acquired before the whole industry went on a shopping spree. The market may have forgotten the acquisitions because they were a few years back. But it will not forget the profitability benefits from those lower prices (for good acreage) as the profits roll in. That makes Diamondback a very strong buy with exclamation points.

Vital Energy is smaller and so could stay underpriced for a while. But it now has very good acreage with which to grow production. For patient investors, this one is likewise a strong buy.

Occidental clearly grabbed a big win here. But it did so at a higher price than either of the first two companies. Investors are beginning to see why Warren Buffett is so interested in this company and its management. This one is likely a strong buy as well. It is also likely to be one of the first companies to reach historical valuations due to its size and the backing of Warren Buffett.

For further details see:

Diamondback Energy Went Midland Before Midland Was Cool