DRH - DiamondRock Hospitality: Low LTV Ratio Makes 7.6% Yielding Preferreds Appealing

Summary

- DiamondRock Hospitality REIT will likely post a full-year AFFO per share of in excess of $0.90, indicating the stock trades at just 9X AFFO.

- While that's cheap, it may get even cheaper as DiamondRock has started to buy back its own shares.

- I like the preferred shares as the preferred dividend is very well-covered and the balance sheet appears strong.

- Wait for weaker days and pick up the preferred shares closer to par.

Introduction

While I'm not necessarily a big fan of REITs in the hospitality sector, there are some REITs and preferred shares issued by hospitality REITs that I do like. Sunstone Hotel's ( SHO ) preferred shares for instance, which I discussed here . But since this summer, I have also been keeping an eye on DiamondRock Hospitality ( DRH ). Not for the common units, but for the preferred shares. When my last update was published in September, the preferred shares actually offered an 8.8% yield to call as the preferred shares were trading below the par value.

The third quarter was very strong for DiamondRock, and FY2022 should be a good year

A lot has happened since my previous update and the Q3 results of DiamondRock once again showed the hotel REIT is getting back on track. While I'm not expecting a lot from the fourth quarter, the REIT's performance in the first nine months of the year already paves the way for a very decent financial year. And as I'm mainly interested in the preferred shares, I will explain how those preferred shares have actually gotten 'safer' since the beginning of this year.

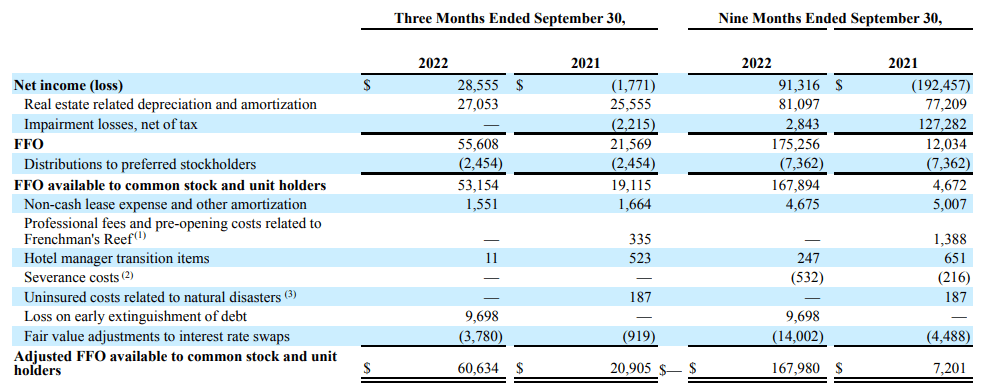

DiamondRock clearly performed pretty well during the third quarter. The REIT reported a net income of $28.6M and after adding back the $27.1M in depreciation and amortization expenses, the FFO was $55.6M .

{kind=link}

As you can see in the image above, this also means the preferred dividends were very well covered as DiamondRock needed less than 5% of its FFO to cover the dividend payments.

Additionally, DiamondRock's Adjusted FFO was even higher than the FFO due to the positive impact from the non-cash lease expense amortization and adding back the loss on the extinguishment of debt, partially offset by a $3/8M fair value adjustment to interest rate swaps.

This means the AFFO during the third quarter was $60.6M which already included the $2.5M in preferred dividend payments. Adding those preferred dividends back to the equation, DiamondRock generated about $63M in AFFO during the third quarter and needed less than 4% of its AFFO to cover the preferred dividends.

The relatively strong third quarter obviously also had a positive impact on the YTD results as the AFFO came in at just under $168M during the first nine months of this year (including $7.4M in preferred dividend payments). That's approximately $0.80 per share ( $0.78 per diluted share was the result reported by DiamondRock, but the REIT has since repurchased about 1% of its share count, while I also use the current share count rather than the diluted share count).

While DiamondRock has not published an official outlook for the fourth quarter of this year, I don't think DiamondRock will do worse than its $0.09 AFFO per share in Q4 2021 . This means we can likely look forward to DiamondRock generating $0.90 in AFFO this year and perhaps even well into the 90s although investors are warned the fourth quarter is traditionally pretty weak.

DiamondRock pays a quarterly dividend of $0.03 per share but has recently started a share buyback program. Between October 1 and the publication of the quarterly report in early November, DiamondRock spent in excess of $12M on buying back 1.6M shares .

{kind=link}

The preferred shares are still attractive

The series A preferred shares ( DRH.PA ) are cumulative issue, offering an annual preferred dividend of $2.0625 per preferred share paid in four quarterly installments. The securities can be called from Aug. 31, 2025 on.

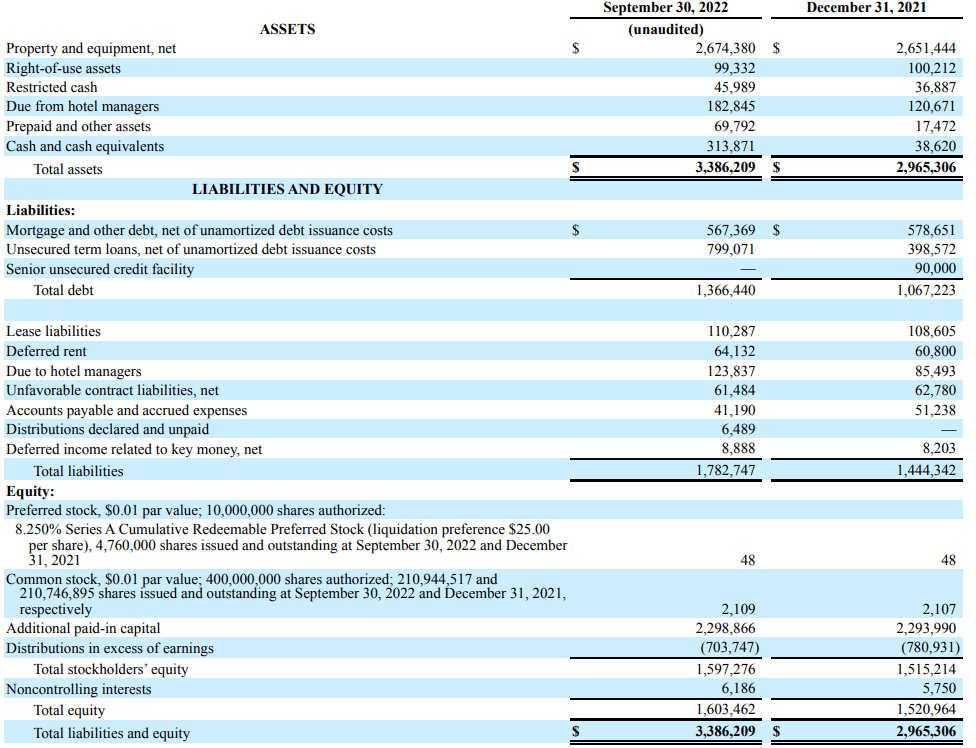

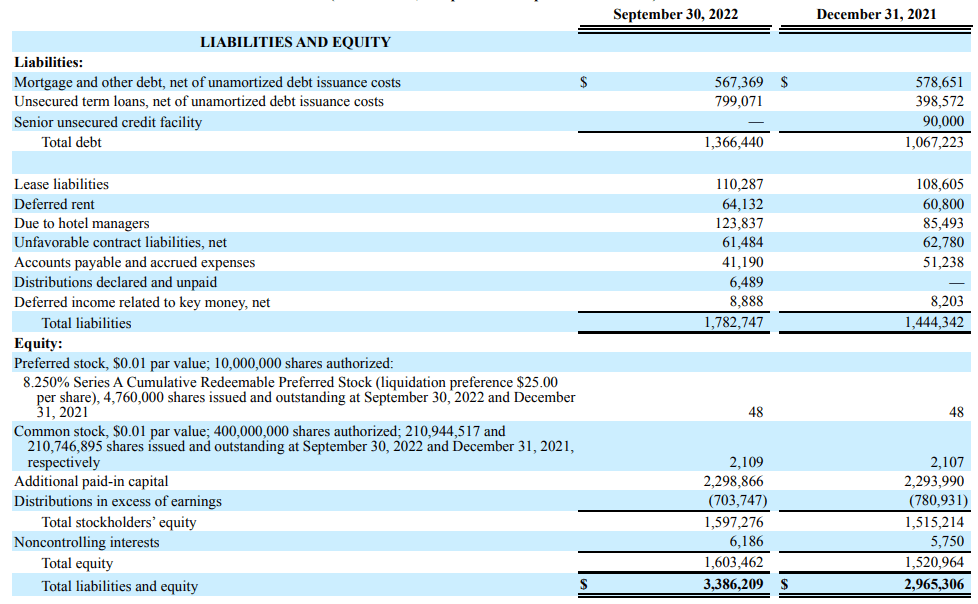

Earlier in this article I already established the preferred dividends are very well-covered but I also like to keep an eye on the asset coverage ratio. The balance sheet provides an excellent look under the hood. We see the total amount of assets as of the end of September was just under $3.4B, of which $2.67B were real estate assets.

{kind=link}

The cash position of $314M also was a big help as it means the net financial debt (defined as financial debt minus cash) was just $1.05B. That's an LTV ratio of just under 40% of the book value of the assets.

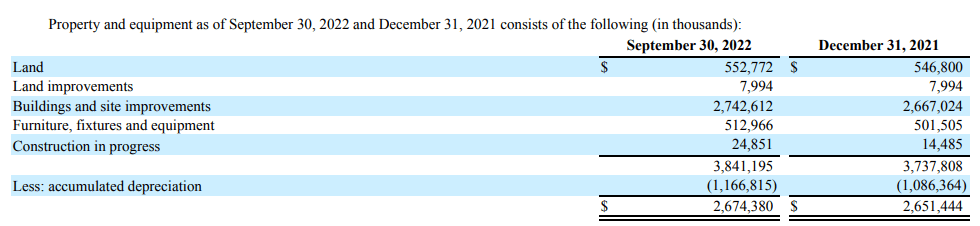

However, that aforementioned $2.67B in real estate assets already includes a substantial amount of depreciation. According to the footnotes to the financial statement, the total accumulated depreciation was approximately $1.17B which means the acquisition value of the assets was substantially higher than the current book value.

{kind=link}

Based on the acquisition value of the assets, the LTV ratio is less than 30% which makes the balance sheet pretty safe. Additionally, if we zoom in on the liabilities side of the balance sheet, we see there's plenty of common equity, which ranks junior to the preferred equity.

{kind=link}

There are 4.76 million preferred shares outstanding which means the total amount of preferred equity is approximately $119M. This means there's about $1.48B in equity ranked junior to the preferred shares. And that's based on the book value and completely ignores the in excess of $1.1B in accumulated depreciation.

Investment thesis

There will for sure be weaker days and it is quite likely the preferred shares of DiamondRock will dip below their par value of $25 per share, and that would make them a strong buy as I think the odds of DiamondRock calling these preferred shares in 2025 are growing . Based on Friday's closing price of $25.38 per share, the yield to call is approximately 7.61%. Lower than what it used to be in September, but I remain convinced there will be days this preferred share issue will fall below par.

I like the very strong dividend coverage ratio and asset coverage ratio and while I still think my Sunstone preferred shares are my favorite in the hospitality REIT sector, DiamondRock's balance sheet is rapidly improving making the preferred shares rather attractive for income-focused investors. DiamondRock's preferred shares are very high on my short list and I'm still kicking myself for having missed the opportunity to purchase the shares below par.

For further details see:

DiamondRock Hospitality: Low LTV Ratio Makes 7.6% Yielding Preferreds Appealing