DRH - DiamondRock Hospitality: Undervalued Thanks To Room Pricing Strategies And Hotel Enhancements

2023-08-16 03:38:47 ET

Summary

- DiamondRock Hospitality is an American company that operates as a REIT and is focused specifically on temporary accommodation properties.

- In 2023 and 2024, DiamondRock is expected to benefit from the capital expenditures made in the Hilton Boston Downtown/Faneuil Hall, Salt Lake City Marriott, and the Hilton Burlington Lake Champlain.

- I believe that further inflationary effects in the United States would most likely not affect the company as DiamondRock periodically changes the room prices to reflect the effects of inflation.

I believe that DiamondRock Hospitality ( DRH ) could, in 2023 and 2024, benefit from the capital expenditures made recently in the Salt Lake City Marriott and the Hilton Burlington Lake Champlain. Besides, recent FCF margin improvements seem to indicate that management knows well how to deal with inflationary pressures. Clients seem to accept room price increases. Moreover, I believe that market expectations are quite beneficial for DiamondRock. In my view, even considering the risks from franchise agreements or a decrease in the demand for accommodation in some regions, DiamondRock stock does look undervalued.

DiamondRock

Founded in 2004 and with uninterrupted activities to date, DiamondRock Hospitality is an American company that operates as a REIT and is focused specifically on temporary accommodation properties.

By the end of 2022, the company had in its portfolio 35 premium hotels and resorts with around 9,600 rooms located in 24 different markets within the United States.

The main business of this company involves the research, acquisition, ownership, and renovation of hotel facilities at the domestic level, in highly concentrated urban areas and with rapid turnover of transitory population segments. All its operations are managed under the representatives or brands of the hotels, among which we can highlight Marriott ( MAR ), one of the most recognized hotel chains globally.

The operations are carried out via a single segment that covers the administrative and financial treatment of its subsidiaries. DiamondRock generates its complete operating income through these subsidiaries, and the maximum annual income for the company comes from the hotel facilities of Marriott Chicago, which represented 9%, 10%, and 11% of the annual margins in recent 3 years respectively.

The search for acquisitions is dedicated to properties that generate quick returns on capital, and serve to make the operating costs of the company sustainable. The purchase strategy about properties that are already in operation, where this company is only dedicated to remodeling spaces, allows the company to meet the objective of obtaining direct margins. The experience in this sense enables the company to reduce operating costs and increase profit margins per rented room.

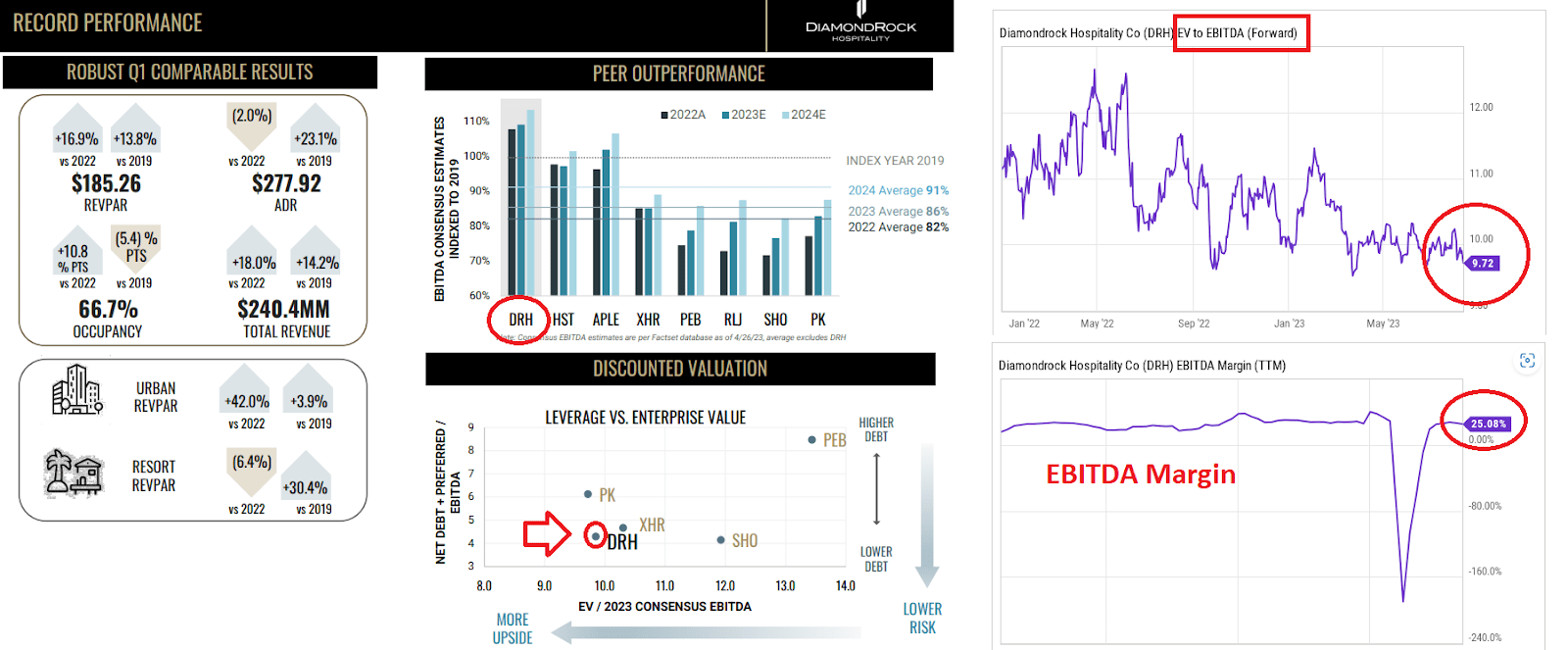

It is worth showing the valuation of DiamondRock. It is one of the most interesting features of DiamondRock. The company appears to be trading at a large discount as compared to peers, at close to 9.75x Forward EBITDA with an EBITDA margin close to 24%-25%.

{kind=link}

Good Track Record Of FCF Generation

Market expectations include net sales growth, EBITDA margin growth, net margin growth, and FCF growth. I believe that market analysts out there are quite optimistic about the future of DiamondRock.

More in particular, estimates include 2025 net sales close to $1131 million, with 2025 EBIT close to $297 million, 2025 EBITDA of $177 million, and operating margin close to 15%. Besides, 2025 net income would stand at about $109 million, with EPS close to $0.39 per share.

Source: S&P

Increase In Assets And A Decrease In Liabilities

In 2023, management reported a small increase in the total amount of assets, a decrease in the total amount of liabilities, and an enhancement in the asset/liability ratio. The increase in total assets was driven by a significant increase in the total amount of cash, attributed partially to increases in cash flow from operations.

Source: Ycharts

As of June 30, 2023, property and equipment stood at $2.740 billion, with right-of-use assets close to $97 million, restricted cash worth $37 million, due from hotel managers close to $164 million, and cash and cash equivalents of about $98 million. In sum, total assets were equal to $3.224 billion.

Source: 10-Q

In 2023, it is quite appealing that the total amount of liabilities decreased. Mortgage and other debt decreased accompanied by the decreases in accounts payable, due to hotel managers, and deferred income related to key money.

More in particular, the company reported total debt of $11.81 billion, with lease liabilities worth $111 million, due to hotel managers of about $119 million, deferred rent close to $67 million, accounts payable and accrued expenses of about $39 million, and total liabilities worth $1.594 billion.

Source: 10-Q

Valuation

I believe that further implementation of aggressive acquisition strategy, with low debt spreads and rapid returns on properties in urban and high-traffic areas within the United States, will most likely bring FCF growth.

I would also expect that further diversification of hotel properties that are not located in urban centers may improve FCF margin stability in the long term.

Considering the CFO currently generated, I would also expect prudent leverage, so investors would most likely not dump their shares because of financial risks. Besides, the WACC would most likely not increase beyond reasonable levels. In the last quarter, management promised to maintain a low level of debt. I assumed the same in the coming years.

As of June 30, 2023, we had $1.2 billion of debt outstanding with a weighted average interest rate of 4.88% and a weighted average maturity date of approximately 2.9 years. We have limited near-term mortgage debt maturities and 31 of our 35 hotels are unencumbered by mortgage debt. We remain committed to our core strategy of prudent leverage. Source: 10-Q

I would also expect that further accumulation of know-how, and digital capabilities will most likely continue to improve the occupancy. As a result, I believe that it is fair to assume further FCF margin growth. In this regard, I believe that there is room for optimism as occupancy increased in the last quarter, and total revenue in the first half of 2023 also increased by close to 11%.

Source: 10-Q

{kind=link}

Even including risks of macroeconomic decline in the United States for the second half of the current year, I believe that the balance sheet is in a good position to help meet the demands of corporate and tourist travel, supporting its financial strength. Besides, I believe that the recent capital expenditures to enhance the offering of the Hilton Boston Downtown/Faneuil Hall, Salt Lake City Marriott, and the Hilton Burlington Lake Champlain, which are taking place in 2023 and 2024, may also have a beneficial effect on the revenue line.

Hilton Boston Downtown/Faneuil Hall: We completed a comprehensive renovation to rebrand the hotel as The Dagny, an independent lifestyle hotel. Source: 10-Q

Salt Lake City Marriott: We are in the process of completing a renovation of the guestrooms, which is expected to be completed in the third quarter of 2023. Source: 10-Q

Hilton Burlington Lake Champlain: We commenced a repositioning of the hotel to rebrand it as a Curio Collection hotel. The repositioning is expected to be completed in the first quarter of 2024 and includes a new restaurant concept by a well-known, award-winning chef. Source: 10-Q

Finally, I believe that further inflationary effects in the United States would most likely not affect the company as DiamondRock periodically changes the room prices to reflect the effects of inflation. In this regard, the company may serve as a refuge for investors looking to protect their investments against inflation. In this regard, considering the recent increase in the FCF/Sales margin, I believe that DiamondRock knows well how to implement pricing strategies.

Operators of hotels, in general, possess the ability to adjust room rates daily to reflect the effects of inflation. Generally, our management companies may adjust room rates daily, excluding previous contractually committed reservations. Source: 10-Q

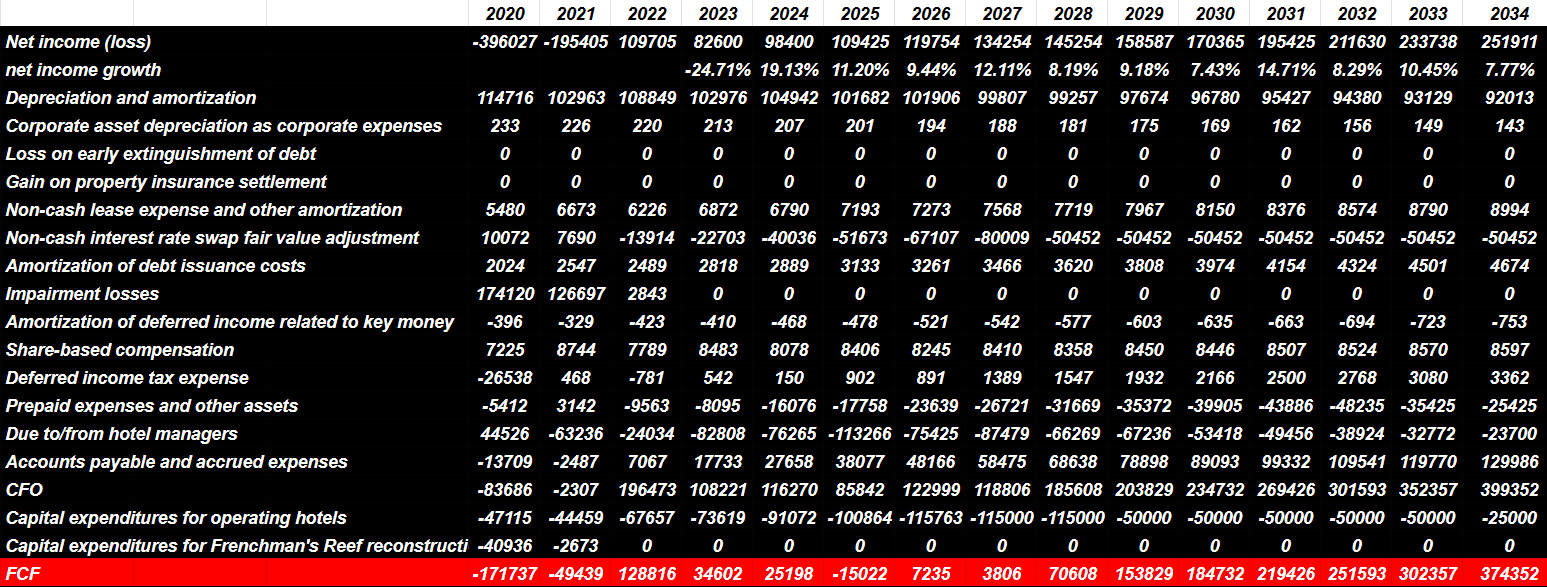

My numbers include 2034 net income close to $251 million, with net income growth of about 7.55%, and 2034 depreciation and amortization worth $92 million. Also, with 2034 non-cash lease expense and other amortization worth $8 million and non-cash interest rate swap fair value adjustments worth -$51 million, I assumed 2034 amortization of debt issuance costs of close to $4.05 million.

Besides, taking into account 2034 share-based compensation of $8.055 million, deferred income tax expense worth $3.055 million, and prepaid expenses and other assets of -$26.055 million, I also included due to hotel managers worth -$24.055 million. Finally, with changes in accounts payable and accrued expenses of $129 million, 2034 CFO would be close to $399 million. If we assume capital expenditures for operating hotels of -$25.055 million, 2034 FCF would be $374.55 million.

{kind=link}

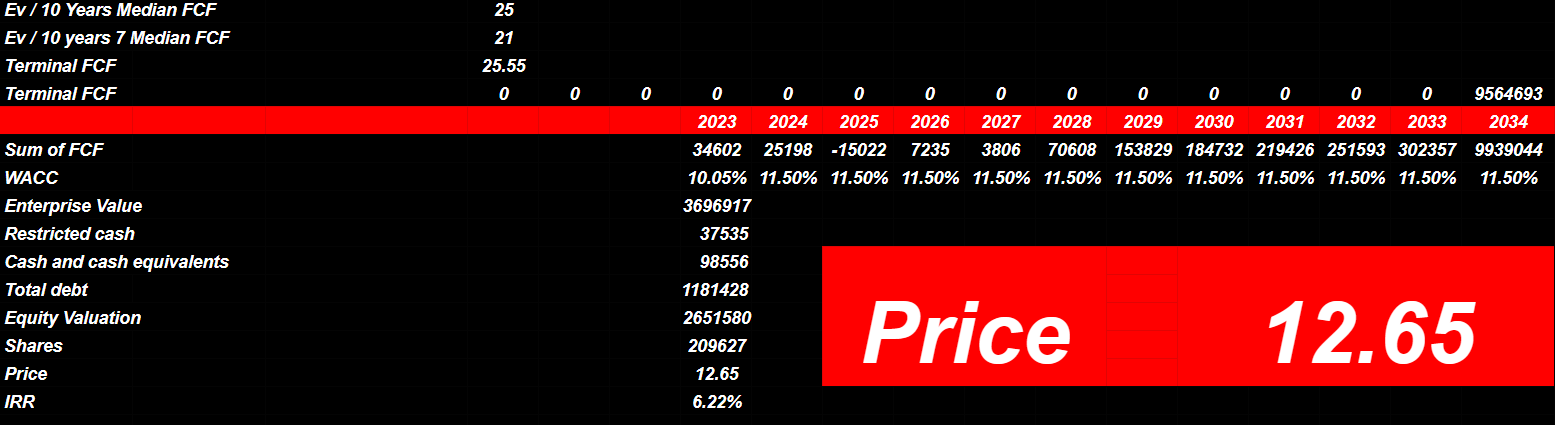

Taking into account that the EV/10 years Median FCF stands at close to 25x, I assumed a terminal EV/FCF of close to 25x, which implied a 2034 terminal FCF close to $9.5 billion.

Source: Ycharts

Now, with a conservative WACC of 10.055%, the implied enterprise value would be close to $3.6955 billion. Adding restricted cash of $37 million and cash and cash equivalents worth $98 million, and subtracting total debt of close to $1.181 billion, the implied equity valuation would be $2.65 billion. Finally, the implied price would be about $12.65 per share, with an IRR close to 6.25%.

{kind=link}

Competitors

The hotel industry is highly competitive, and is clearly segmented based on price, type of hotel, and location. The hotels owned by this company are top-of-the-line, and compete within that segment of categories. In this sense, competitive advantages are directly applied to hotels under the Marriott, InterContinental ( IHG ), or Hilton ( HLT ) brands, which have historical and international recognition. Due to the management systems they have developed, the operating costs of these subsidiaries tend to be significantly lower than those of smaller or independent hotels.

When it comes to property acquisition and competition in that sense, other companies that operate as REITs, investment funds, and hotel companies, find themselves in the same way that Diamond Rock focuses on urban properties with a high demographic concentration. This competition can of course reduce the opportunities available in the market as well as increase the costs for transactions.

Risks

The growing competition, the volatility of the economy, the demand that exists for accommodation in urban centers, and the growth of non-conventional accommodation options provided by internet platforms are risk factors that coexist with the operations of the subsidiaries of this company.

In addition, DiamondRock's properties are operated by subsidiaries, and they have a high concentration - 16 of their 35 properties - in the Marriott and Hilton franchises. This concentration means a risk in itself, and in addition to the properties operated under these franchises, the management skills the company maintains directly influence the financial conditions of the company. The relationship that the management maintains with the subsidiaries is of high value in terms of the fluidity and continuity of operations.

Conclusion

In 2023 and 2024, DiamondRock is expected to benefit from the capital expenditures made in the Hilton Boston Downtown/Faneuil Hall, Salt Lake City Marriott, and the Hilton Burlington Lake Champlain. I also think that the recent increase in the FCF margin proves that DiamondRock knows well how to implement correct pricing strategies to fight the effects of inflation. Most analysts already delivered beneficial expectations for the coming years, and I agree with their optimistic free cash flow figures. Even considering the risks from franchise agreements or less demand for accommodation in urban centers, I think that the stock could trade at a higher mark.

For further details see:

DiamondRock Hospitality: Undervalued Thanks To Room Pricing Strategies And Hotel Enhancements