DSX - Diana Shipping: A Solid Business But Too Much Debt

2023-06-05 10:56:53 ET

Summary

- The company has strong profitability with a solid net profit margin of 29.3%.

- The forward-looking dividend yield is strong at 15.4%.

- A heavy debt burden creates too much uncertainty in a high-interest-rate environment.

Introduction

Diana Shipping ( DSX ) is a shipping company operating in the dry-bulk ocean cargo market. In this article, I will introduce the company and its operation, analyze the company's financial position, look into the dry-bulk market's status, analyze the current market value for the company's stock, and discuss risks related to the stock.

Investment Thesis

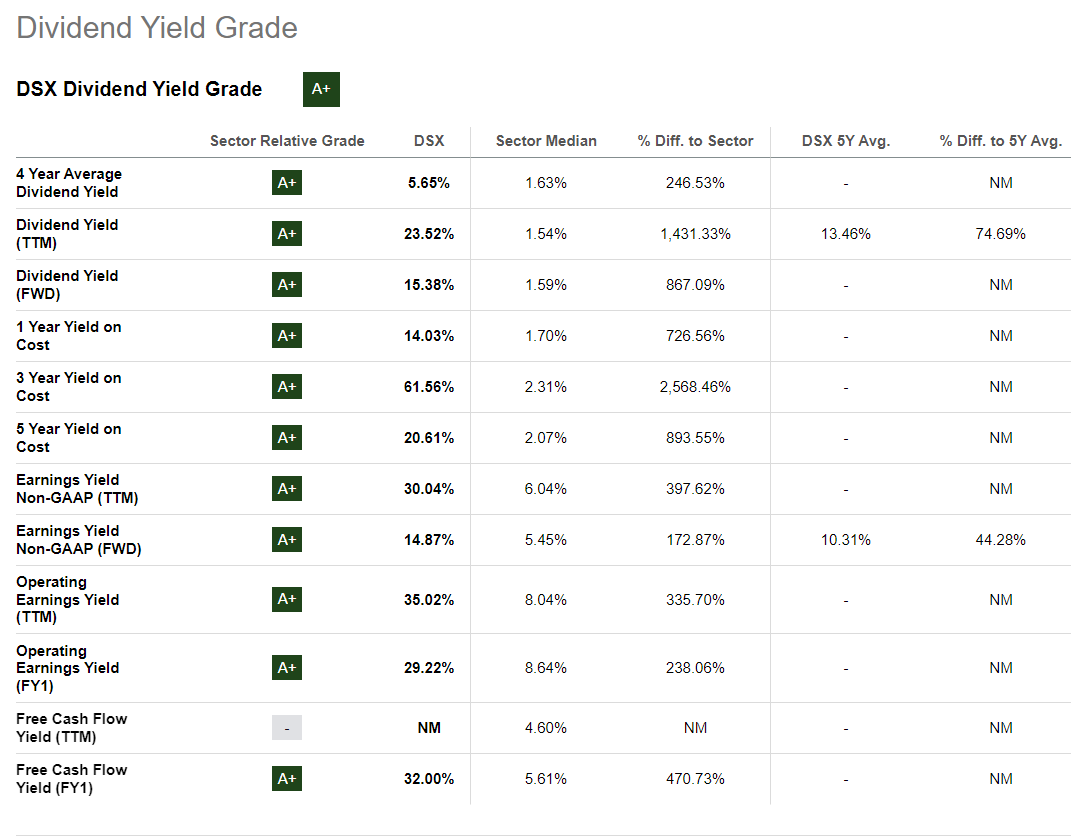

Dividend Yield Grade (Seeking Alpha)

{kind=link}

Diana Shipping is a clear dividend stock, a 4-year average dividend yield stands at 5.65% which indicates a strong ability to pay dividends to shareholders in a volatile market. Diana Shipping pays dividends on a quarterly basis which improves investors' cash flow. Investors must take into account that the last 4 years have been turbulent times in the dry bulk shipping market with a heavy fluctuation in the cargo rates (see Baltic Dry Index under market overview headline), and still, Diana has been able to pay consistent dividends. Diana's trailing 12-month dividend stands at 23.52% which is extremely strong. However, with Diana (and other dry bulk shippers) TTM dividend yield must be taken with a grain of salt due to the fact that 2022 was one of the strongest years for dry bulk ship owners in the last few decades. For an investor considering purchasing DSX right now, future dividends are important. If the company is able to pay a dividend of $0.15 per share (the latest dividend), on a quarterly basis, DSX's forward-looking dividend will stand at 15.38%. A major risk related to Diana Shipping is the relatively high-debt burden which is discussed more in detail below in the Risks section.

Diana Shipping In A Nutshell

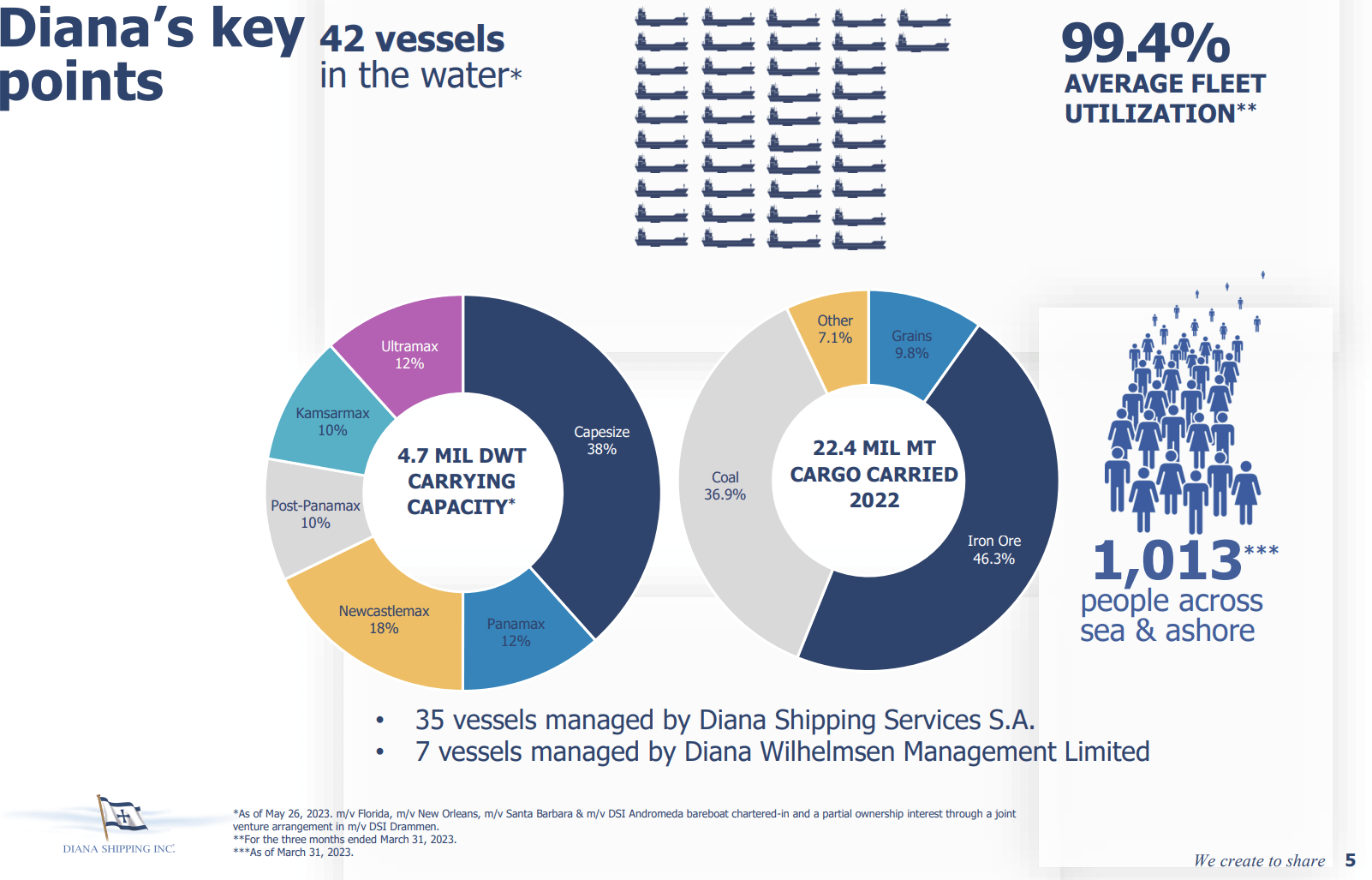

Diana Shipping corporate presentation

{kind=link}

Diana Shipping is an NYSE-listed shipping company with headquarters in Athens, Greece. The company operates a fleet of 42 vessels diversified within all major dry-bulk vessel categories. Capesize class vessels represent the largest share (38%) of Diana's total fleet. Diana's fleet's average age is approximately 10 years . The company has been actively selling its older vessels in order to decrease risks related to older vessels. Major cargoes Diana's fleet carries are iron ore and coal. In 2022 iron ore represented 46.3% of total cargo carried and coal 36.9% respectively. In total, iron ore and coal represented 83.2% of all cargo the company carried in 2022.

Financials

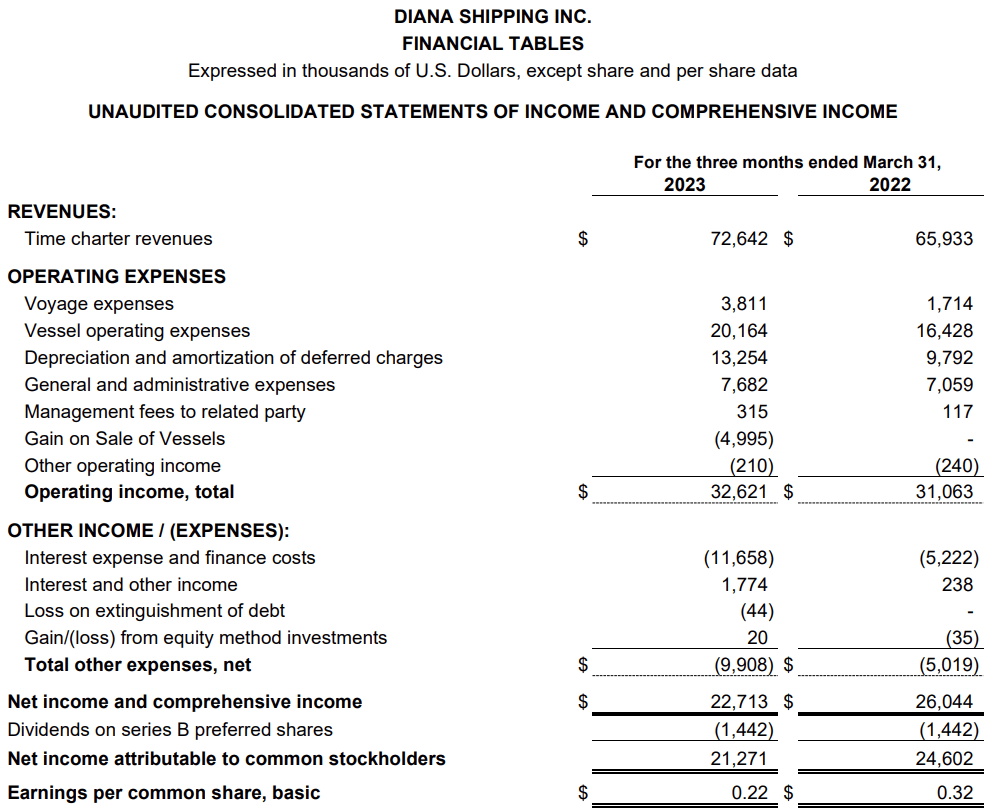

Diana Shipping Q1 2023 Income Statement (Diana Shipping Quarterly Report Q1 2023)

{kind=link}

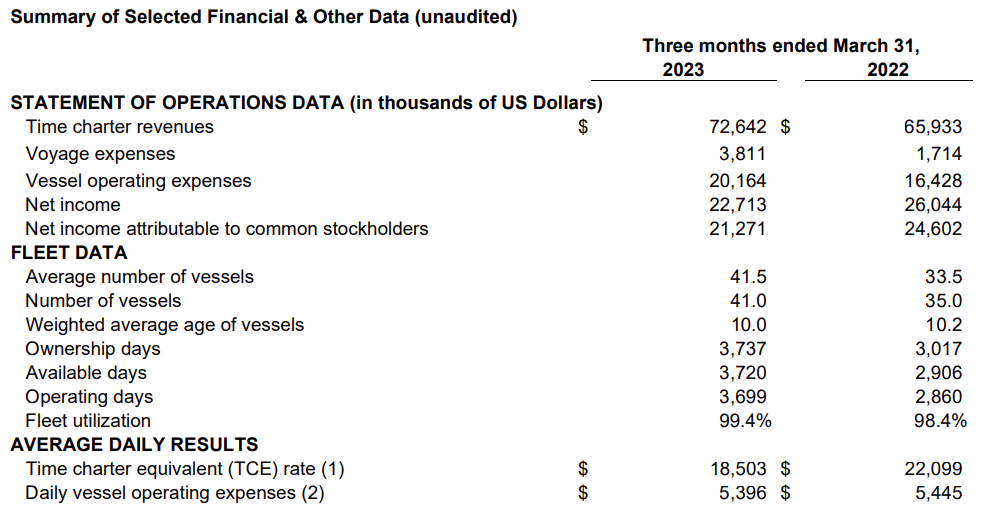

Diana Shipping's Q1 2023 was surprisingly strong. The revenue increased by 10.2% to $72.6 million from $65.9 million in Q1 2022. The company was able to achieve strong revenue due to a relatively high TCE rate (time charter equivalent rate) of $18,503. In comparison, Diana's competitor Genco Shipping (NYSE: GNK ) was able to achieve a TCE rate of $13,947 in Q1 2023, which is 24.6% lower than Diana's TCE. TCE rates between the two companies are not fully comparable due to the different size vessels in the fleet, but in the big picture, both companies carry mainly the same freight (coal & iron ore) with similar vessels.

Diana Shipping Quarterly Report Q1 2023

{kind=link}

The net income decreased by 12.8% to $22.7 million from $26.0 million in Q1 2022. The decrease in net income indicates that the heavy inflationary environment affects also the cost structure of Diana Shipping. In total, the vessel operating expenses have increased by 22.7% from Q1 2022. In the same period, the fleet size increased by 17.1%. This means that the operating expenses have increased at a higher rate than the fleet size, indicating that either the underlying prices have increased, or the company is not able to operate a larger fleet with a similar efficiency as a smaller fleet. Even when the net income has decreased, the net margin is still 31.2%, which is a strong performance for a company operating in the dry bulk shipping sector.

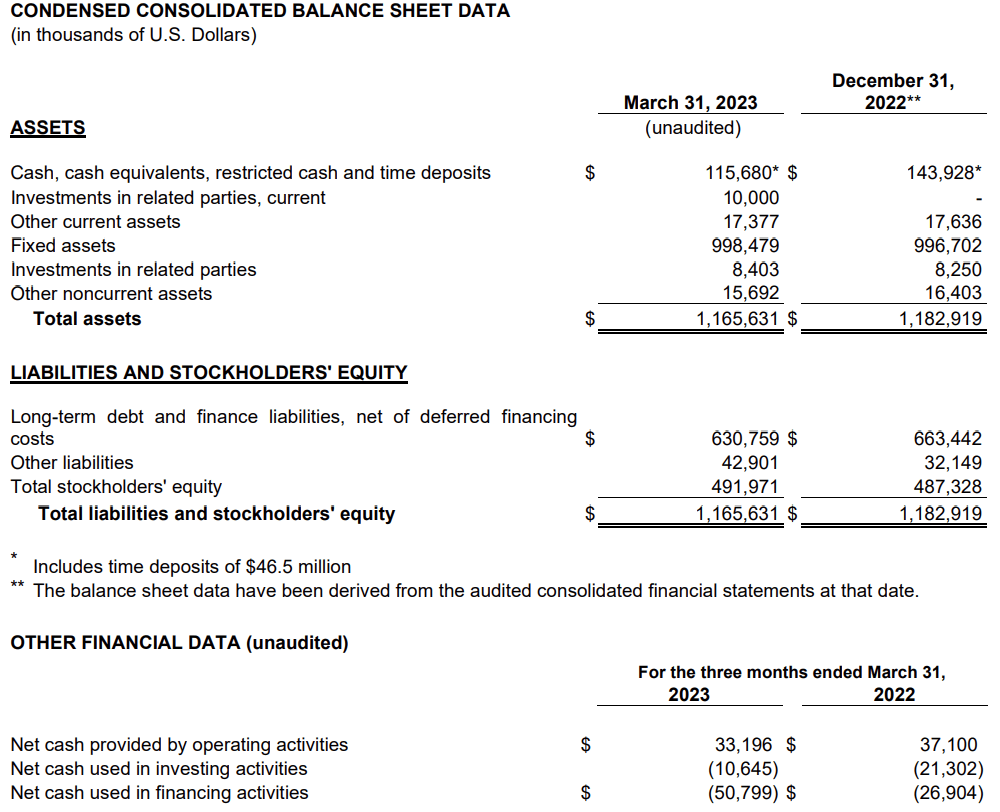

Balance Sheet March 31, 2023 (Diana Shipping Quarterly Report Q1 2023)

{kind=link}

From a balance sheet perspective, I focus on cash and debt. The cash level of $115.68 million on March 31, 2023, is a healthy level when taking into account the announced dividend payments. Diana has announced a $0.15 per share dividend from Q1 2023, which means a total cash outflow of roughly $16.0 million. The company pays dividends quarterly (on a historical basis), meaning that the annual cash outflow from dividends is roughly $61 million. Diana's cash balance seems to be viable to enable the company to continue similar dividend payments also in the future.

On the liability side of the balance sheet lies the problem for Diana Shipping. Long-term debt stands at $630.8 million while the total balance sheet value is $1,165.6 million, this translates the debt-to-assets ratio to 54%. In a high-interest rate environment high debt-to-assets ratio means increased risk in the cost of refinancing that may negatively impact Diana's ability to pay dividends to shareholders. Find more about risks related to high debt below in the Risks section.

Valuation

{kind=link}

{kind=link}

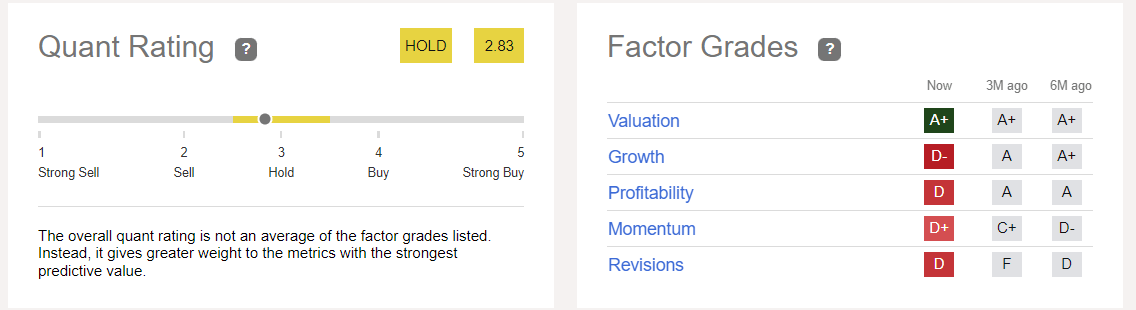

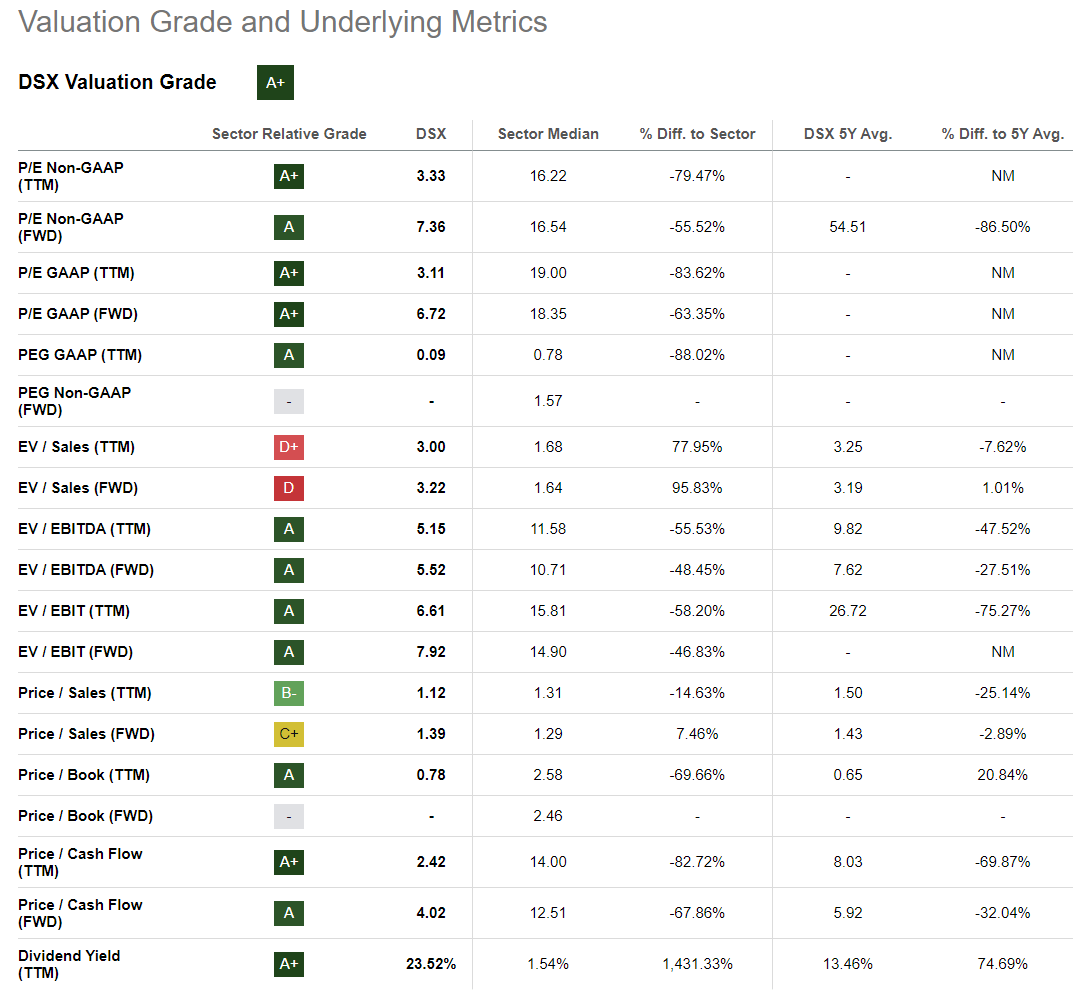

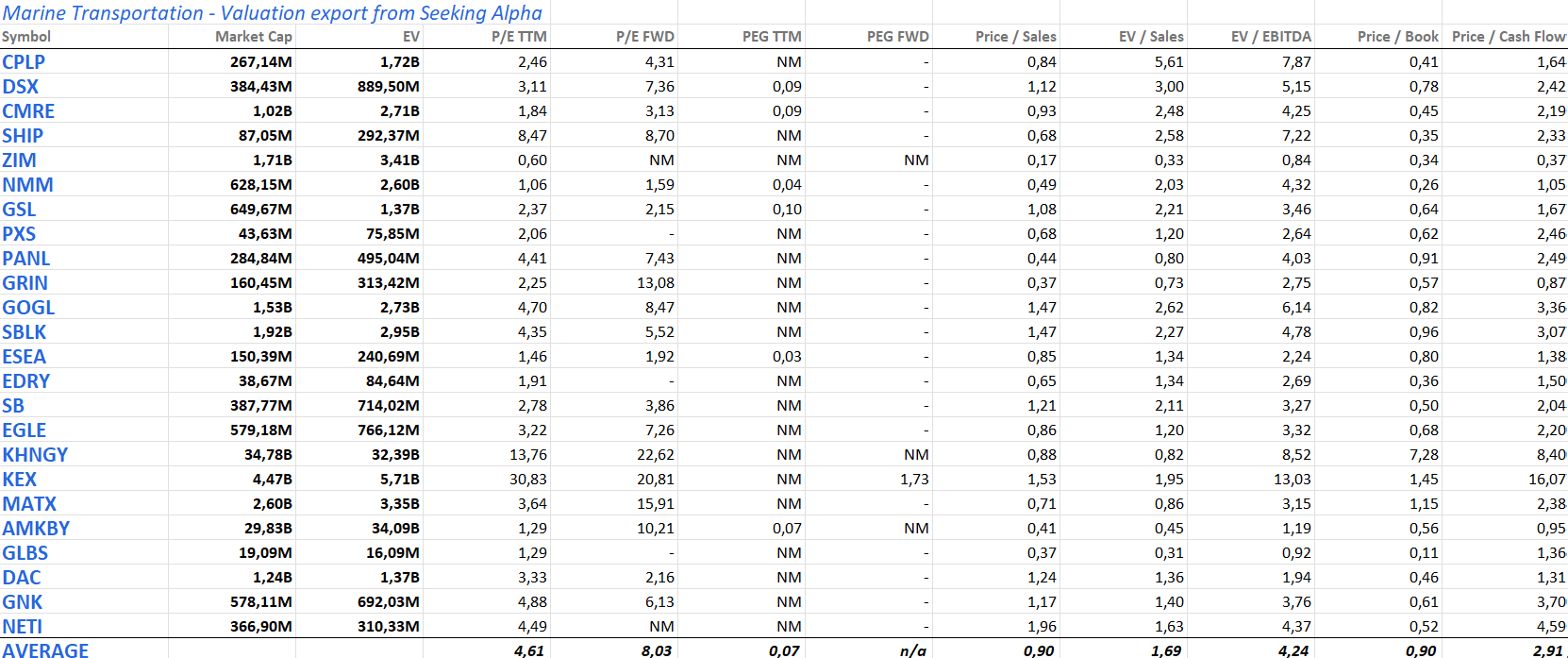

Seeking Alpha's Quant Rating gives Hold recommendation for Diana's stock. The best factor grade in Quant is Valuation standing at A+. On traditional valuation measures, Diana's stock seems to be cheap. P/E (price-to-earnings) calculated with a 12-month trailing earnings stands at 3.33 which is lower than the marine transportation sector median of 4.61.

Marine transportation sector valuation ratios (Seeking Alpha (average calculated by the Author))

{kind=link}

P/B (price-to-book) ratio for Diana stands at 0.78, meaning that the market value for the company is only 78% of the total assets on its balance sheet. This is a really low P/B value indicating that the stock is cheap, but as the company is operating in the dry bulk shipping sector, low P/B values are typical for a whole sector. The average P/B for the marine transportation sector is 0.9, this means that Diana can be considered cheap in comparison to its competitors.

Overall for an income-seeking investor, Diana seems to be a reasonably priced stock. When taking into account the forward-looking dividend yield of 15.38%, the stock has a strong potential to provide a decent return in my view.

Market Overview

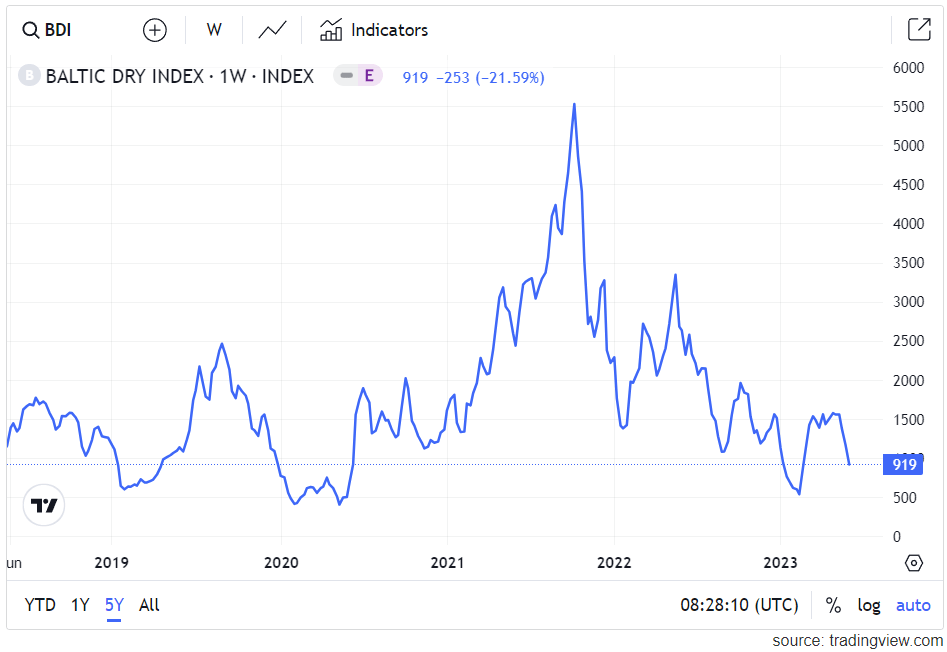

Baltic Dry Index (TradingView)

{kind=link}

The dry bulk shipping market is a cyclical sector and freight rates vary strongly. 2021 and 2022 were one of the strongest years for dry bulk shipping companies in decades due to extremely high freight rates. The Baltic Dry Index (commonly used price reference for dry bulk cargoes) peaked at 5,500 points in late 2021 and has gradually declined to the current value of 919. If the Baltic Dry Index continues its downward trend, dry bulk shippers face decreasing revenues that translate to a lower absolute profitability that affects the ability to pay dividends.

IMF (International Monetary Fund)

The demand for dry bulk shipping is closely correlated with the development of global GDP. International Monetary Fund estimates that the global GDP growth will decrease from 3.4 percent in 2022 to 2.8 percent in 2023. This means that the dry bulk shippers will likely face less demand for charters during 2023, which may lead to a decrease in prices. However, what is positive for dry bulk shippers operating with a fleet focusing on major bulk cargoes (coal & iron ore), is that the growth projection for emerging & developing Asia is higher than the overall global estimates. Asian trade is an important part of the iron ore & coal shippers business.

Risks

The main risks investors need to take into account while evaluating opportunities with Diana Shipping are market risks, risks related to inflation, and interest rate risks.

If the global GDP development is slower than anticipated, market rates and overall demand for dry bulk shipping may decrease. This might lead to the negative development of Diana Shipping's business and its ability to pay dividends might be endangered.

Inflationary risks affect the cost structure of Diana Shipping. If inflation stays strong, the operating expenses for Diana Shipping may increase at a faster rate than freight rates. This might negatively affect the profitability of the company and in the worst case, the company may not be able to pay dividends. Positively the inflation rates have been trending downwards, potentially easing the rate of increase in operating expenses.

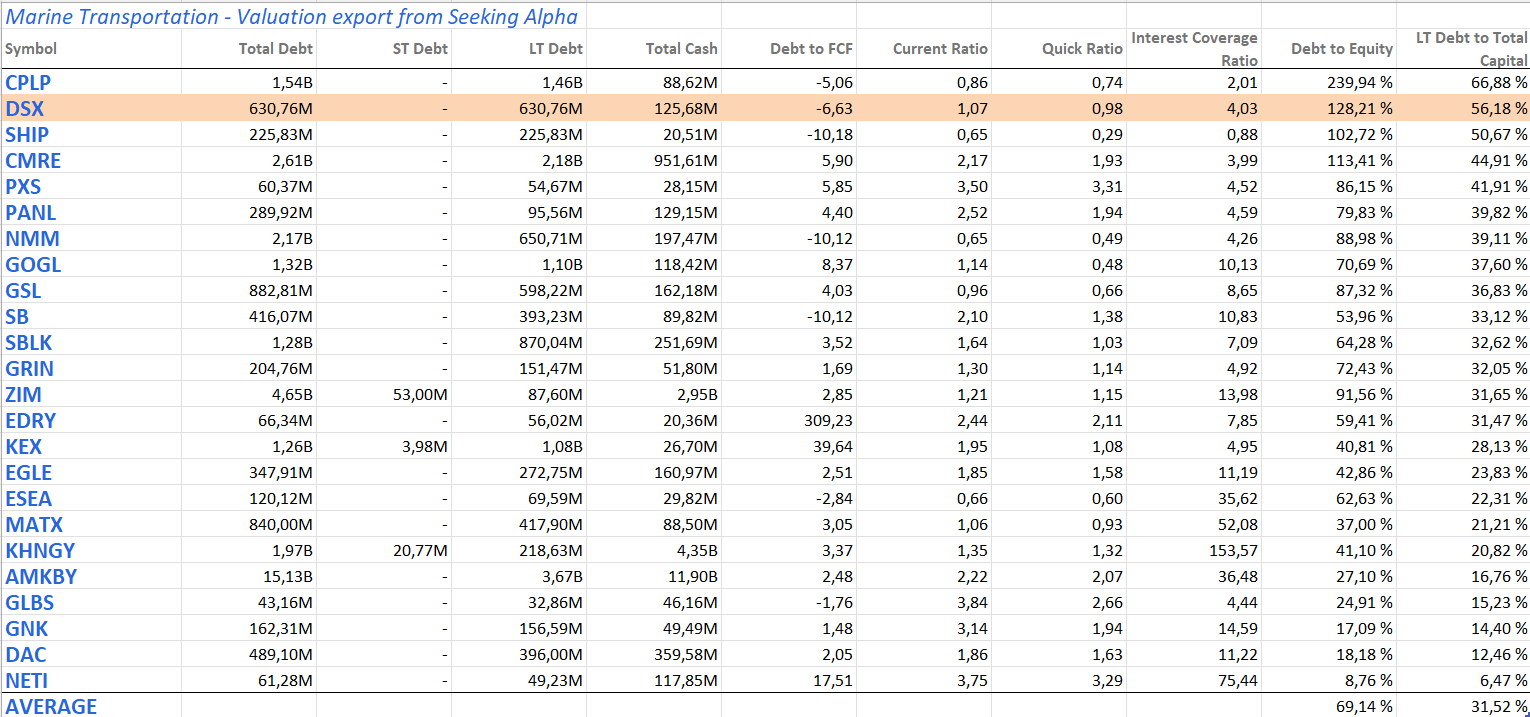

Marine transportation sector debt (Seeking Alpha (average calculated by the author))

{kind=link}

The major risk related to Diana Shipping is the company's heavy debt burden. The debt-to-equity ratio is 128.21% and the long-term debt-to-total capital is 56.18%. In comparison to Diana's competitors, the debt burden is high. On average the companies operating in the marine transportation sector have a debt-to-equity ratio of 69.14% and long-term debt-to-total capital of 31.52%. The heavy debt burden is challenging in the rising interest rate environment. The refinancing of debt with favorable terms may be challenging and the cost of debt financing may increase significantly. According to Diana's annual report for 2022, the increase of 1 percentage point in the interest rate would increase the company's interest expenses by $3 million. If interest rates keep rising, the company may be incapable to pay dividends. An investor must consider very carefully the willingness to carry Diana's risk related to high debt.

Conclusion

In conclusion, Diana Shipping is a dry bulk shipping stock with a strong business operation and the ability to run the business profitably. High debt levels in a high interest-rate environment create risks that might materially affect the company's ability to pay dividends. Due to high debt, I give a hold recommendation for the stock.

For further details see:

Diana Shipping: A Solid Business But Too Much Debt