DSX - Diana Shipping: Downgrading On Premium Valuation And Risk Of Dividend Cut

2023-08-02 20:55:13 ET

Summary

- Diana Shipping reported somewhat weaker than expected Q2 results but declared a generous $0.15 dividend per common share, payable in stock or cash at the election of shareholders.

- Average daily time charter equivalent ("TCE") rate was down by 6.5% sequentially and almost 30% year-over-year.

- Assuming the current charter rate environment to persist, free cash flow for the second half of 2023 would be just slightly above breakeven.

- While Diana Shipping has committed to another $0.15 dividend for the next quarter, payable in stock or cash at the election of shareholders, the generous distribution won't be supported by cash generation in the second half of the year.

- Considering the company's premium valuation and very real risk of a substantial dividend reduction later this year, I am downgrading Diana Shipping's common shares from "Hold" to "Sell".

Note:

I have covered Diana Shipping Inc. or "Diana Shipping" ( DSX , DSX.PB ) previously, so investors should view this as an update to my earlier articles on the company.

On Tuesday, leading dry bulk shipper Diana Shipping reported somewhat weaker than expected second quarter results and declared a $0.15 dividend per common share, payable in stock or cash at the election of shareholders.

{kind=link}

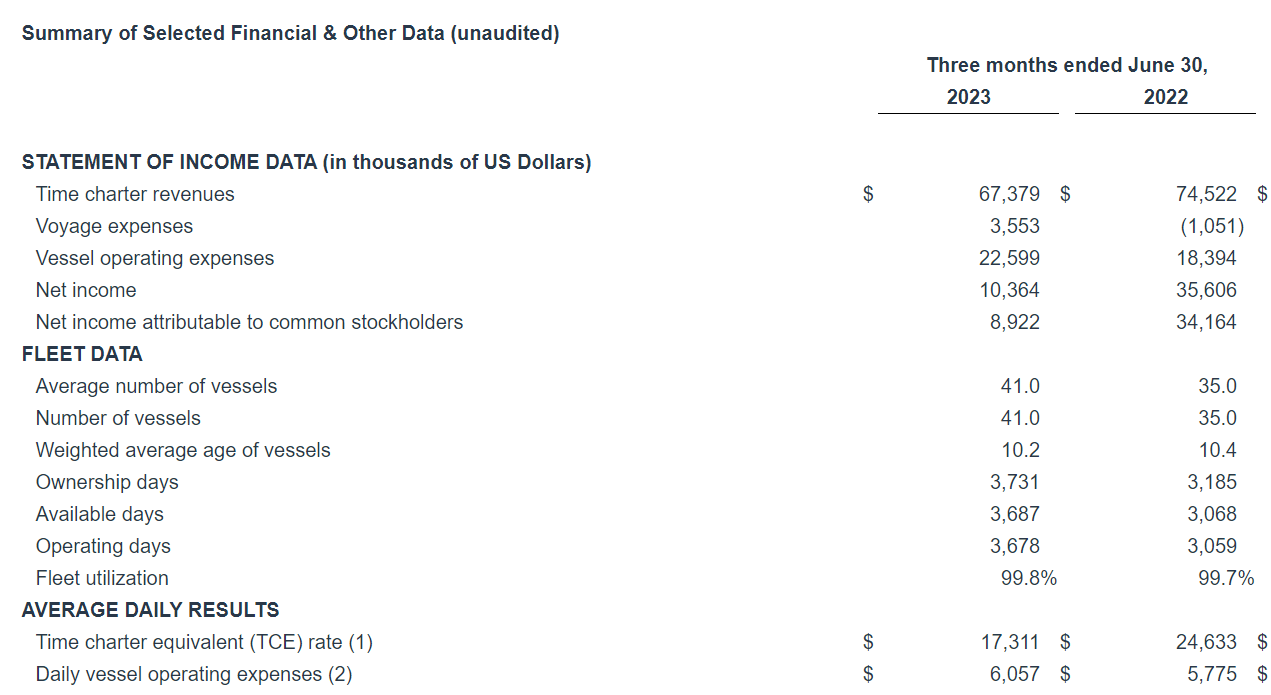

Despite the company operating a substantially higher number of vessels than twelve months ago, time charter revenue was actually down by almost 10% year-over-year as Diana Shipping's average daily time charter equivalent ("TCE") rate decreased by approximately 30% to $17,311.

Given the trajectory of dry bulk shipping markets in recent quarters, the material decrease in profitability is hardly a surprise:

{kind=link}

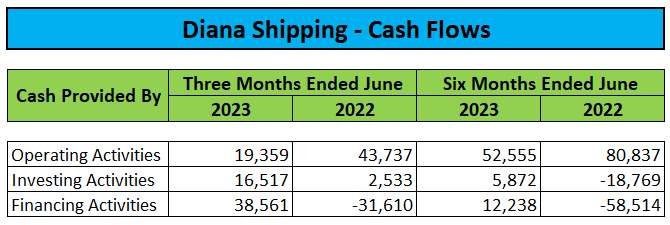

That said, the company still generated $19.4 million in cash flow from operating activities for the quarter but with 80% of remaining days for 2023 fixed at a TCE rate of $16,814, cash generation is likely to decrease even further in the second half of the year.

{kind=link}

In fact, current forward freight agreement ("FFA") rates are substantially below the company's free cash flow breakeven TCE rate of $15,602:

Company Presentation

Assuming the current charter rate environment to persist, free cash flow for the second half of 2023 would be just slightly above breakeven:

Company Presentation

While Diana Shipping has committed to another $0.15 dividend for the next quarter, payable in stock or cash at the election of shareholders, the generous distribution won't be supported by cash generation in the second half of the year.

Given this issue, I would expect the company to either move to a stock dividend or reduce payouts substantially in Q4.

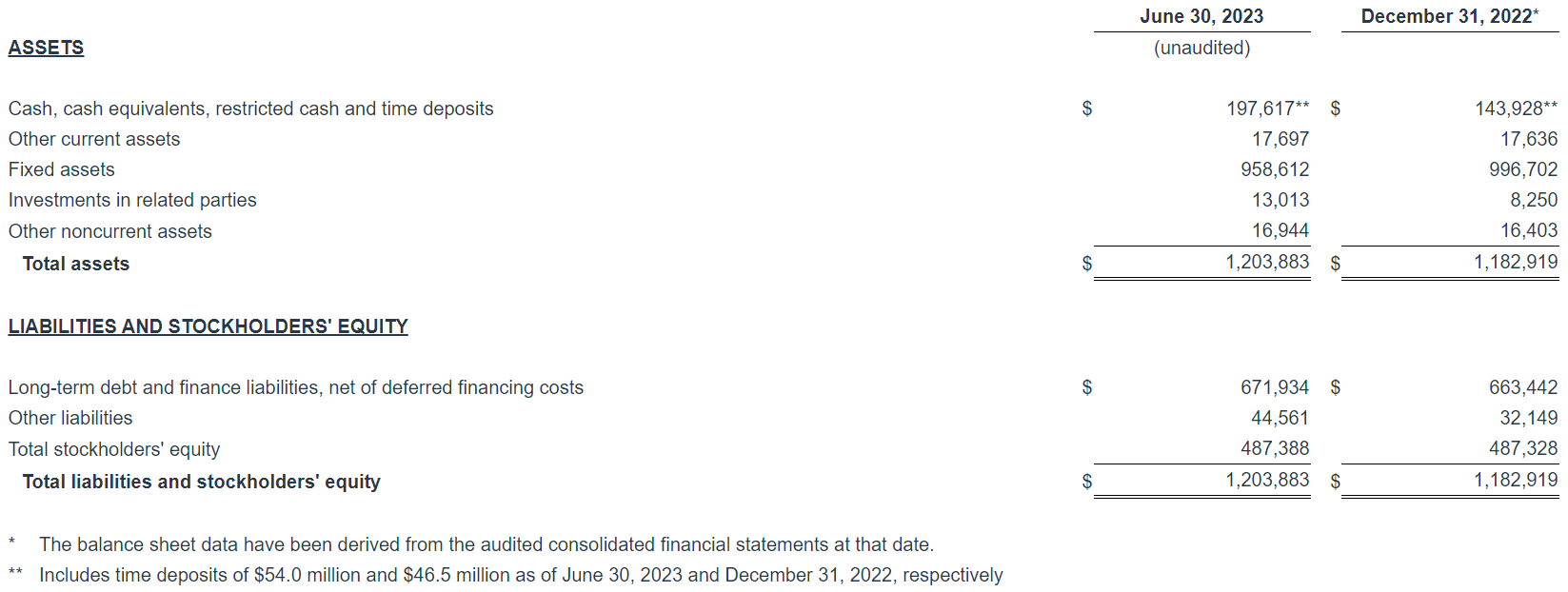

That said, with $197.6 million in cash, cash equivalents, restricted cash and time deposits, Diana Shipping won't experience liquidity issues anytime soon. On the flip side, the company needs to service $671.9 million in increasingly expensive debt:

{kind=link}

Challenging market conditions have resulted in some pressure on second hand vessel values which in combination with the company's generous payouts has impacted net asset value ("NAV") per share:

Regulatory Filings / MarineTraffic.com

On the conference call , management reiterated its commitment to a conservative chartering approach but wasn't exactly enthusiastic for the remainder of the year:

So what about the freight market conditions prevailing. Now according to Clarksons' demand improvements this year have been led by slightly firmer trends in China. But these were accompanied by weaker trends in key other regions, which have marginally prevailed thus far.

At the same time, lower levels of port congestion have added to active tonnage supply. For this year, we will most likely witness more moderate bulker markets overall, compared to the strong conditions experienced in 2021 and the first half of 2022.

In contrast to the common stock dividend, I would consider distributions for the company's 8.875% Series B Cumulative Redeemable Perpetual Preferred Shares ( DSX.PB ) to remain safe for the time being.

Bottom Line

With more and more of Diana Shipping's lucrative legacy charters rolling over to prevailing market rates, the company's cash flows are no longer shielded from current, weak market conditions.

Given this issue, I would expect the dividend to be reduced substantially in Q4 which could impact the stock price quite meaningfully.

With shares trading around net asset value, Diana Shipping commands a premium over the majority of its U.S.-exchange listed peers, which I would solely attribute to its generous distribution policy.

Considering the company's premium valuation and very real risk of a substantial dividend reduction later this year, I am downgrading Diana Shipping's common shares from " Hold " to " Sell ".

For further details see:

Diana Shipping: Downgrading On Premium Valuation And Risk Of Dividend Cut