DSX - Diana Shipping: Good Company And High Dividend Yields Sometimes Are Not Enough

2023-12-25 09:21:19 ET

Summary

- Diana Shipping is a bulk shipping company. It has 42 vessels with a 10.5-year average age. Only 2% of the fleet has scrubbers.

- The company has $173 million in cash, $657 million in total debt, and 135% total debt to equity.

- DSX delivers excellent profit margins and returns due to an efficient cost profile. DSX pays dividends with an impressive yield, 21.27% TTM. NTM yield is 12.9%.

- DSX trades at fair multiples compared to similar-sized bulkershipping companies. Conversely, the company seems cheaper, considering its 5Y average and 10Y peak multiples.

- I give DSX a hold rating due to the lack of scrubber-equipped vessels and slightly higher leverage.

Introduction

Diana Shipping ( DSX ) is a shipping company that owns and operates bulkers. It has 42 vessels with a 10.5-year average age. The fleet utilization has been 99-100% over the last two years. Only 2% of the fleet has scrubbers. The primary focus is iron ore and coal transport, meaning DSX revenues depend heavily on the Chinese economy. The company has $173 million in cash, $657 million in total debt, and 135% total debt to equity. Such figures are adequate but not excellent compared to similar-sized shipping companies. DSX has been profitable and maintains high-profit margins and returns. The company pays dividends with an impressive yield of 21.27% TTM. NTM yield is 12.9%. The slightly higher leverage and lack of scrubber-equipped vessels are the reasons to give DSX a hold rating.

Drybulk market snapshot

The current bulker cycle shares more similarities than differences with the tanker cycle. The supply-side drivers are global fleet age, low order book figures, and limited shipyard capacity. The demand side is pushed by higher iron ore, coal, and agricultural commodities demand by developing countries, especially China and India.

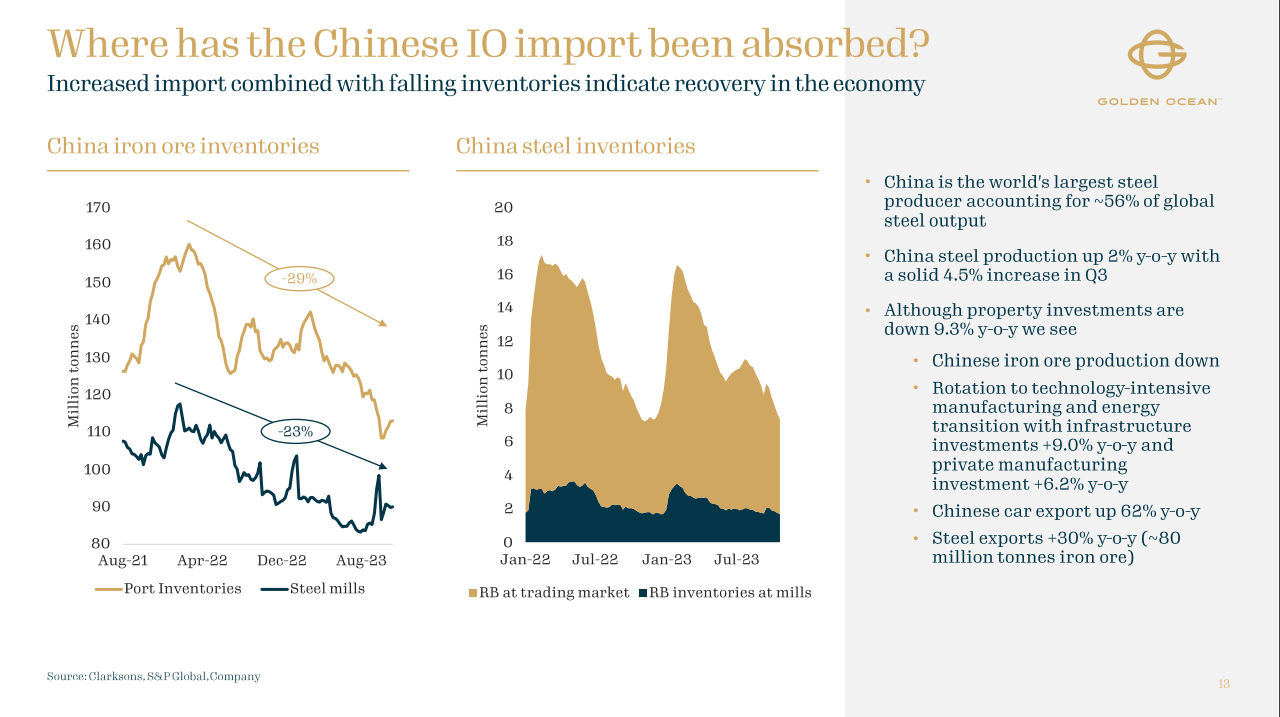

The inventory rebuilding trend drives the demand side for bulkers. Chinese iron ore inventory has declined 29% over the last two years. Besides that, China's steel production is up by 2% YoY, and steel exports are up by 30% YoY. The chart below from the Golden Ocean ( GOGL ) presentation shows Chinese iron ore import trends.

{kind=link}

Despite the declining property investments in China, the abovementioned dynamics compensate for the missing iron ore demand.

The Chinese government plans to keep fiscal stimulus for the economy, boosting productivity and resulting in a growing demand for metals. In the coming quarters, we might see a recovery in the Chinese economy, pushing the development of new projects across industries. That means enhanced demand for iron ore, coal, and aluminum in the coming quarters.

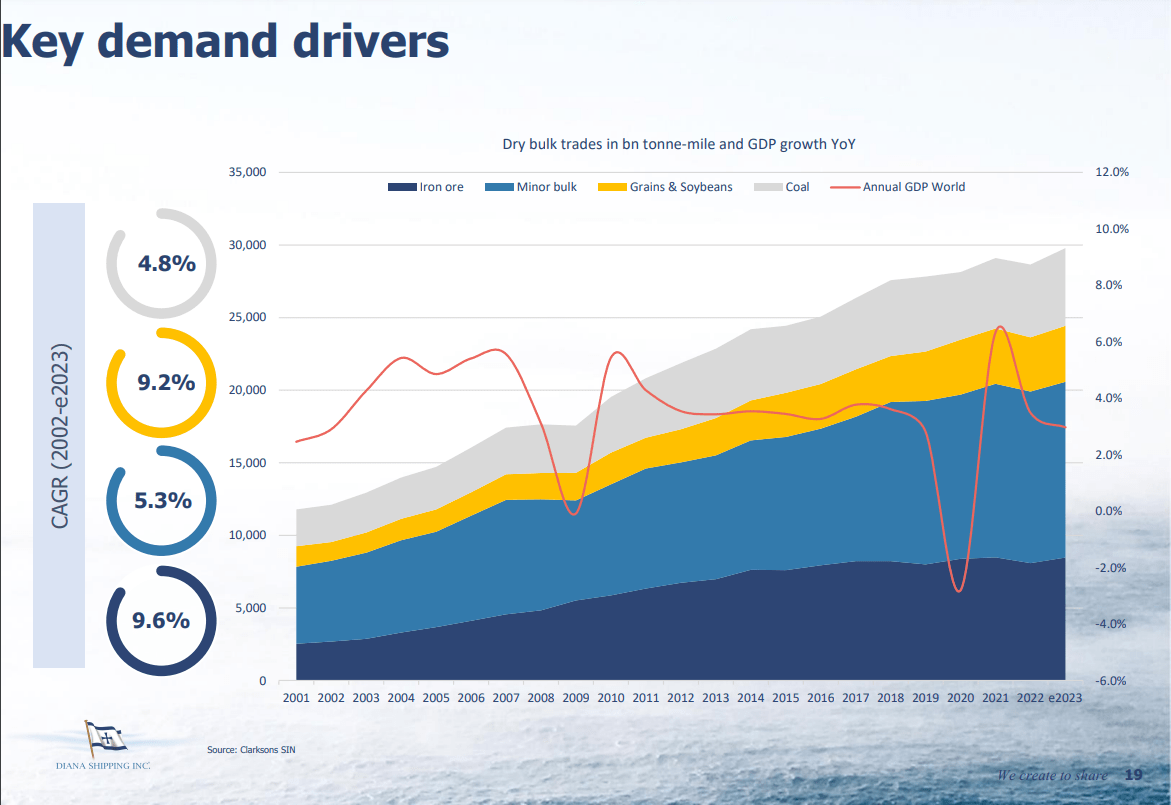

Following global GDP changes, the ton per mile grew over the last decades across all bulk trades.

{kind=link}

Iron ore ton-mile grew by 9.6% CAGR and grain and soybeans by 9.2%. The coal ton-mile has increased by 4.8%.

In the long term, I expect the demand for iron to continue to grow, especially in India and China, the largest steel makers globally; apart from that, the demand for metallurgical coal used in steel production will continue to rise, too.

The thermal coal used in power plants will remain one of the primary commodities for bulk trade. The reason is simple: Global South will not give up its coal plants to be replaced by questionable renewable energy projects with prohibitive costs and embarrassing EROI (return on invested energy). A month ago, India announced its plans to keep coal plants longer and invest in new projects.

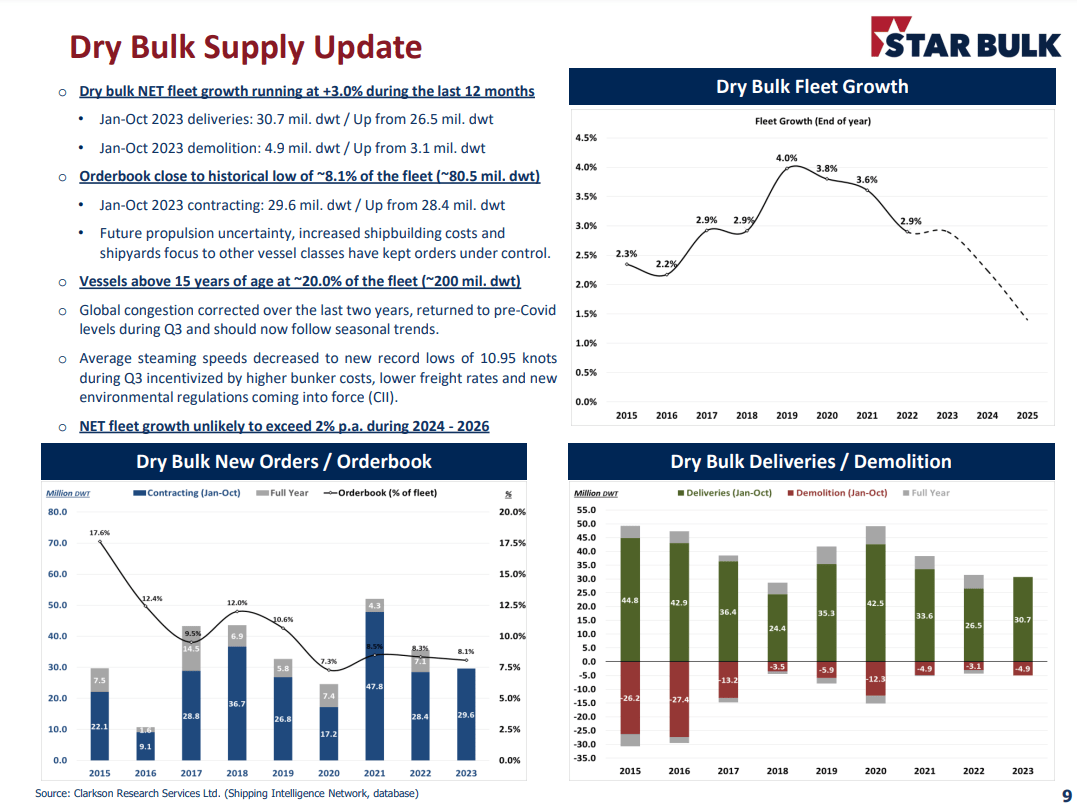

The supply side suffers from symptoms like the tanker segment: old ships, single-digit order books, and constrained shipyard capacity. The chart below from Star Bulk's ( SBLK ) presentation gives a glimpse into the supply side of bulkers.

{kind=link}

The charts above paint a negative picture of a future dry bulk supply; however, they are positive for enterprising investors. Order book is 8.1%, is 20 years record low. Only crude tankers and offshore support vessels have a lower order book, 2.8% and 2.5%, respectively. Twenty years old ships represent 20% of the current fleet. A bulker's average economic life span is 20-25 years, meaning two of every ten ships soon must be replaced. However, we have orders for 0.8 of every ten vessels. A low order book and an aging fleet will stagnate net fleet growth below 3% per annum.

The bottom right chart shows the new ship deliveries and the demolition sales over the last eight years. The ship owners are aware of the current fleet age. However, they are not keen to scrap the vessels before they are confined. New ones are coming.

The demolition figures are incredibly high, typical for cycle thought when the companies are desperate for cash due to TC rates below the breakeven costs. Thus, the ship owner cannot meet its debt obligations and must liquidate some assets to raise funds. No one is willing to scrap vessels at cycle peaks due to the expectation of ever-growing ship demand far exceeding the current vessel supply. I believe we are far away from that situation, too. In conclusion, I think we're in the middle of the cycle, and more profits have to be harvested.

Company Overview

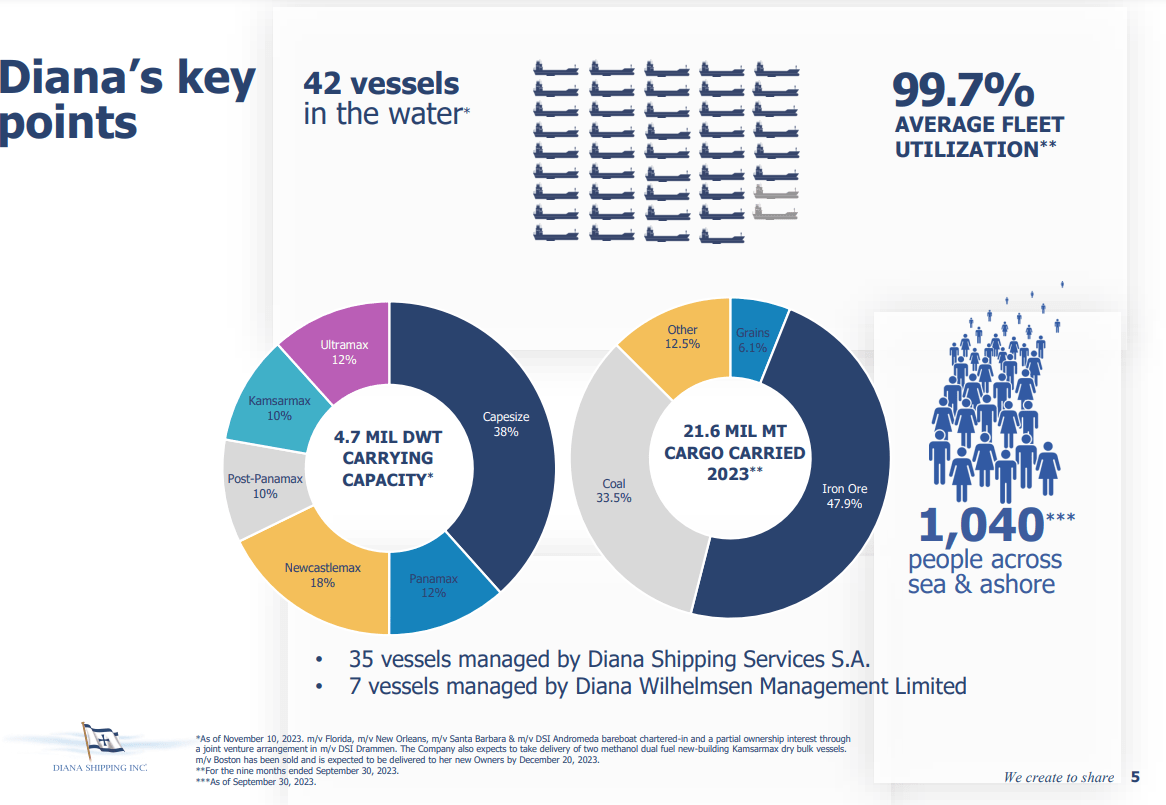

DSX has 42 vessels in its fleet with an average age of 10.5 years. The chart below from the last company presentation shows DSX fleet key points.

{kind=link}

The company has a diversified fleet of vessels. However, Capsize and Newcastle max represents the larger percentage of the fleet. Looking at the composition of the cargo carried, it is understandable: 38% of the cargo is iron ore, while 33.5% is coal. The former is carried primarily by Capsizes. A curious exception is Valemax bulkers or very large ore carriers ((VLOR)). These are ships designed to carry iron ore from Brazil (extracted by Vale) to China. Newcastlemax carries coal. As the name suggests, the ships are designed mainly to take coal in Newcastle, Australia.

The utilization of the fleet is impressive; it has been 99-100% over the last two years. 3Q23 company ships were operational for 3,720 days from 3772 total ownership days.

One thing I dislike is the lack of scrubber-equipped vessels. They are 2% of the total fleet. However, the company makes efforts in that direction, ordering two methanol dual-fuel Kamsarmax vessels. The deliveries are expected in 2027/2028.

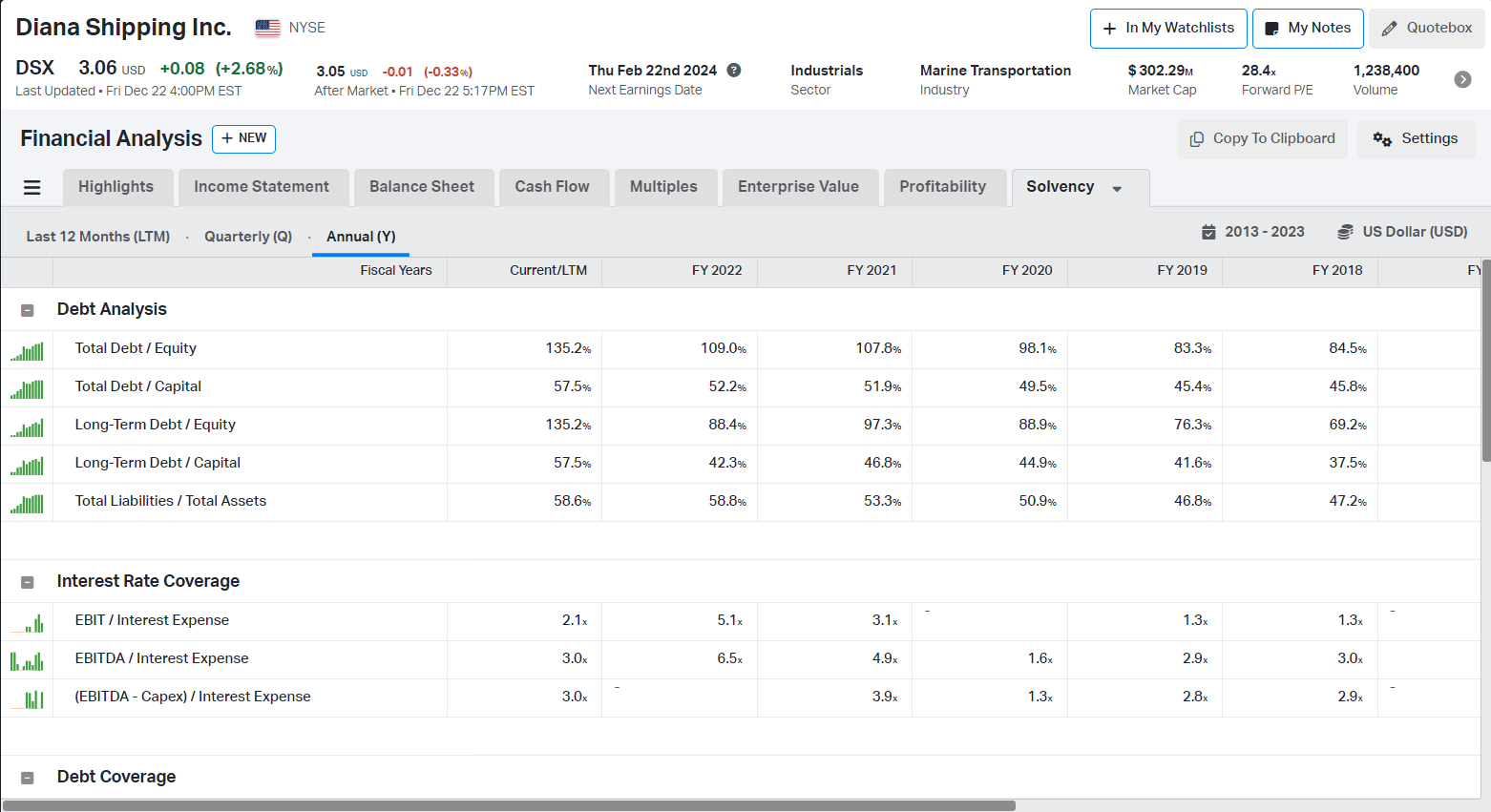

DSX balance sheet

DSX maintains an adequate level of leverage with 135% Total debt to Equity and 58.6% Total Liabilities to Total Assets. Let`s compare how DSX fares against similar sized bakeries companies:

- Diana Shipping $173 million cash; $657 million total debt; 0.26 cash to total debt ratio, total debt to equity 135%

- Pangaea Logistics ( PANL ) $87 million cash; $275 million total debt; 0.31 cash to total debt ratio, total debt to equity 73%

- Grindrod Shipping ( GRIN ) $71 million cash; $168 million total debt; 0.42 cash to total debt ratio, total debt to equity 60%

- Safe Bulkers ( SB ) $74 million cash; $440 million total debt; 0.17 cash to total debt ratio, total debt to equity 57%

- Genco Shipping ( GNK ) $48 million cash; $141 million total debt; 0.33 cash to total debt ratio, total debt to equity 15%

As I said, DSX figures are adequate but far from excellent. GNK has the best debt profile among the group, with a 0.33 cash-to-total debt ratio and 15% total debt and equity.

The table below shows DSX's debt profile and interest rate coverage.

{kind=link}

Over the years, the debt level has increased. 2022 was a strong year for the shipping industry; however, DSX management did not choose to deleverage. On the positive side is the strong liquidity position evident by the stable EBITDA/Interest Expense above 3.0 for the last five years. Interest expenses ((LTM)) are $46 million, while operational income is $98 million.

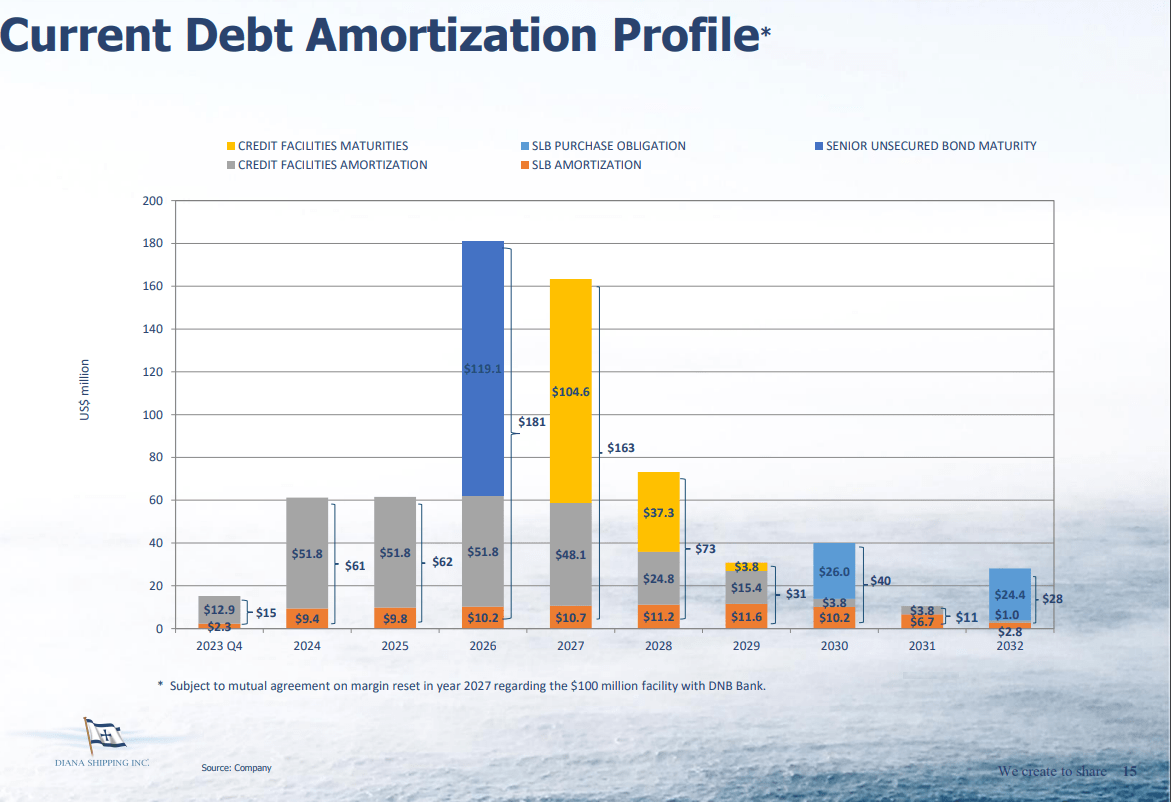

DSX debt maturities are well distributed in the coming years, as seen in the table below.

{kind=link}

In June 2027, a $104 million credit facility matures. In 2026, $119 million unsecured bonds with 8.375% interest come into maturity. The debt obligations for the next two years are $60.2 million in debt amortization on credit facilities per annum.

DSX profitability

Let`s compare how DSX performs against similar sized bakeries companies:

- Diana Shipping 65% gross margin, 49% EBITDA margin, 14.4% ROE, 6.0% ROTC

- Pangaea Logistics ((PANL)) 21% gross margin, 17% EBITDA margin, 11.4% ROE, 5.2% ROTC

- Grindrod Shipping ((GRIN)) 29% gross margin, 7.8% EBITDA margin, (3.5)% ROE, 1.0% ROTC

- Safe Bulkers ((SB)) 62% gross margin, 52% EBITDA margin, 11.1% ROE, 5.1% ROTC

- Genco Shipping ((GNK)) 36.5% gross margin, 26.3% EBITDA margin, 1.2% ROE, 3.71% ROTC

DSX leads the pack in looking at company margins. The reason for that is the efficient cost structure. Company OPEX per day is $5,621. For reference, the largest bulker company, Star Bulk ((SBLK)), has $4,851 daily OPEX. SBLK has 118 ships, and 94% are equipped with scrubbers. SBLK benefits from economy of scale and lower OPEX in the long term due to a scrubber-equipped fleet.

GNK has a similar fleet composition: 45 vessels (18 Capsize and 27 Ultramax/Panamax). 37% of the ships are with scrubbers. Despite that, GNK has $6000 daily OPEX.

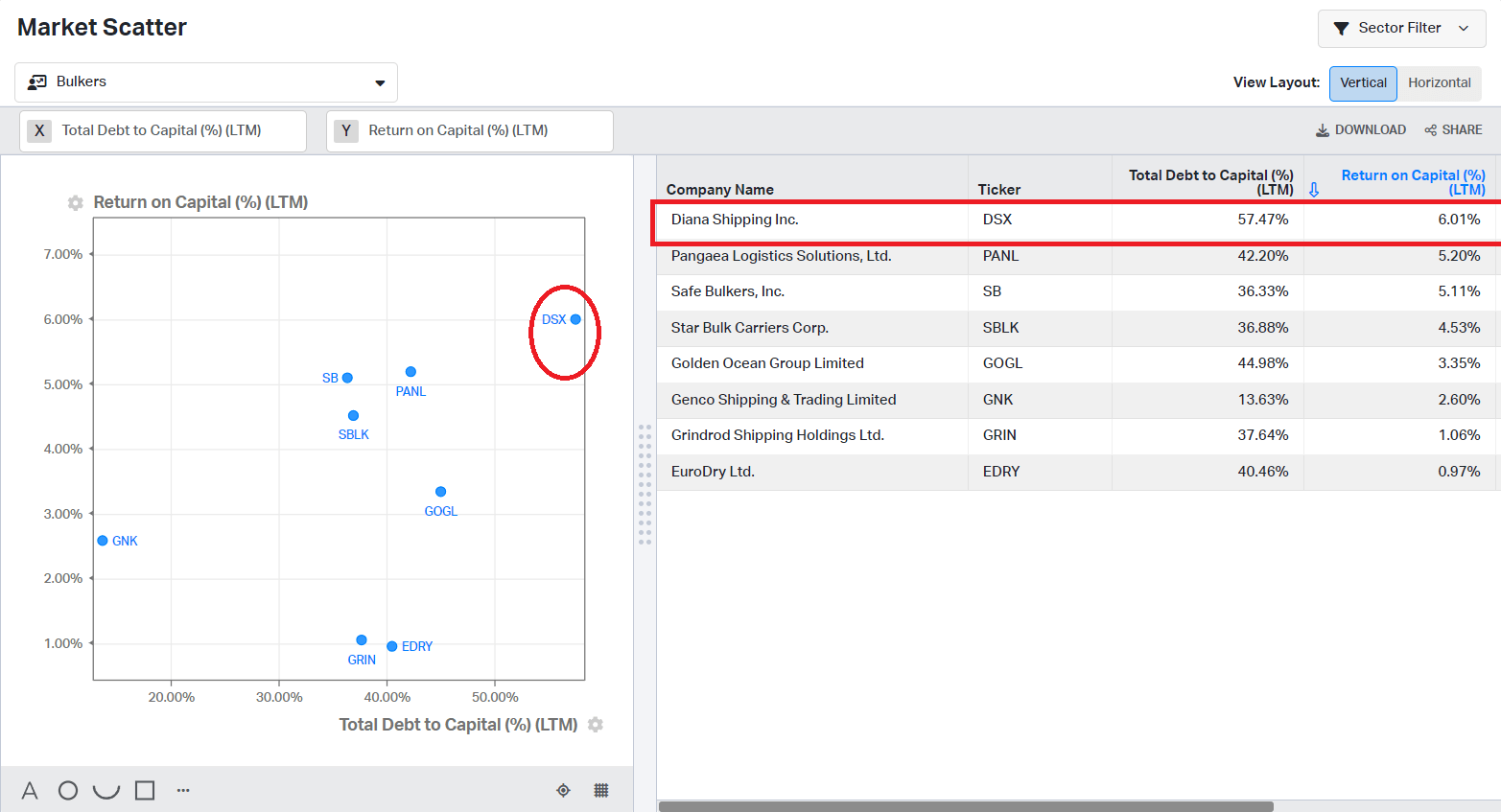

In the chart below, I scattered the ROTC and Total debt/Total capital multiples of several dry bulk carriers to estimate the most capable capital allocator.

{kind=link}

DSX is among the top three in the group, with 6.01% ROTC and 52.47% Total Debt/Total Equity.

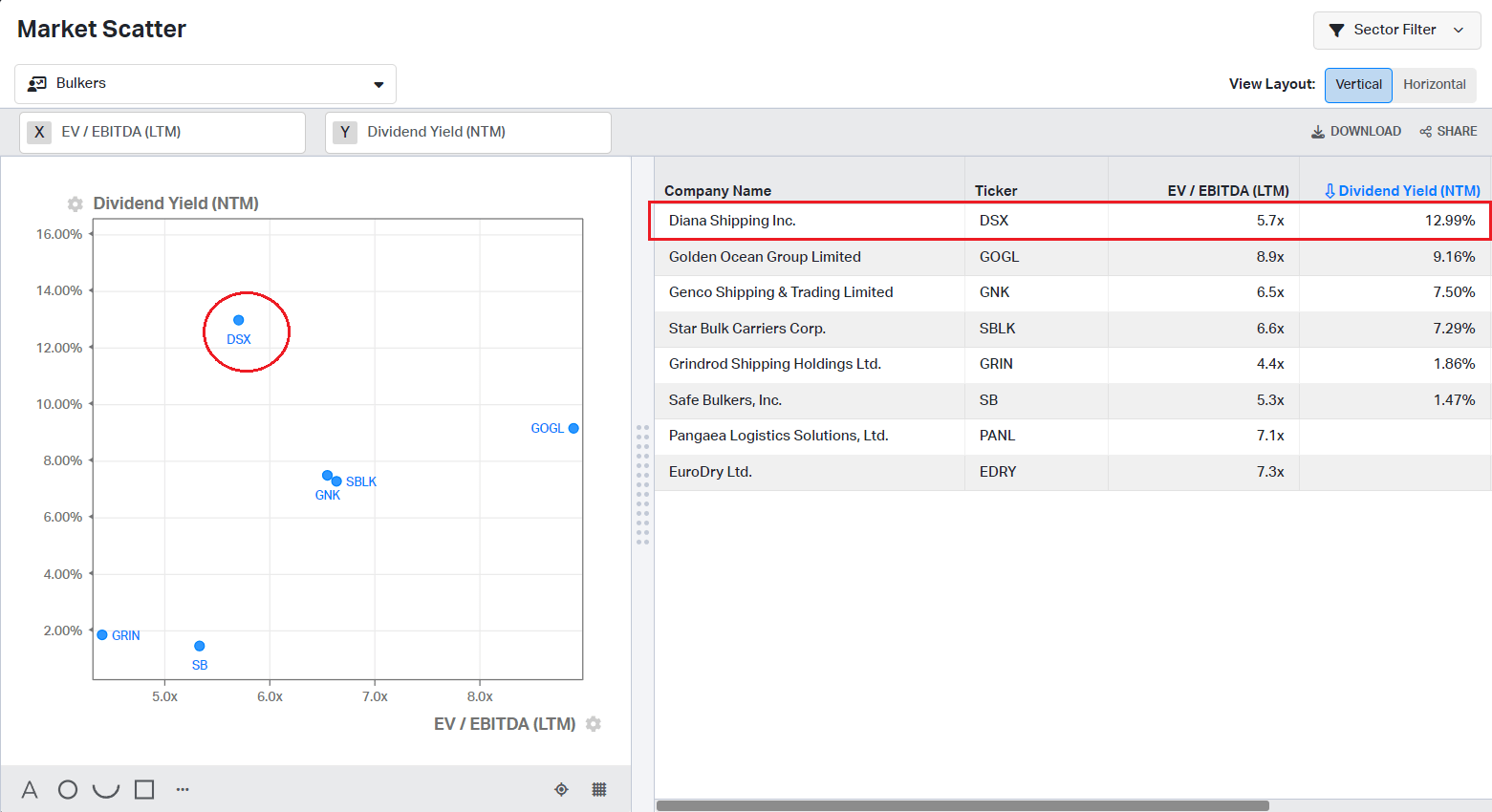

The chart below compares the same companies on dividends and EV/EBITDA.

{kind=link}

DSX has the highest NTM dividend yield while trading at fair EV/EBITDA compared to the other companies. To obtain a 12.99% yield, we have to pay 5.7 EV/EBITDA. Given the other peers in the group, DSX offers the most value for its price. With that conclusion, let`s move to the DSX relative valuation.

DSX Valuation

First, I will compare DSX against the same companies from previous chapters:

- Diana Shipping 2.83 EV/Sales, 5.72 EV/EBITDA, 0.62 P/BV

- Pangaea Logistics ((PANL)) 1.22 Ev/Sales, 7.15 EV/EBITDA, 1.12 P/BV

- Grindrod Shipping ((GRIN)) 0.73 EV/Sales, 9.34 EV/EBITDA, 0.57 P/BV

- Safe Bulkers ((SB)) 2.8 EV/Sales, 5.38 EV/EBITDA, 0.57 P/BV

- Genco Shipping ((GNK)) 1.99 EV/Sales, 7.56 EV/EBITDA, 1.02 P/BV

DSX trades at the highest EV/Sales but at the second lowest EV/EBITDA in the group. Except for PANL, all companies trade at a Price-to-book value below 1. PANL has ice-class vessels in its fleet; I assume this is the reason for higher multiples.

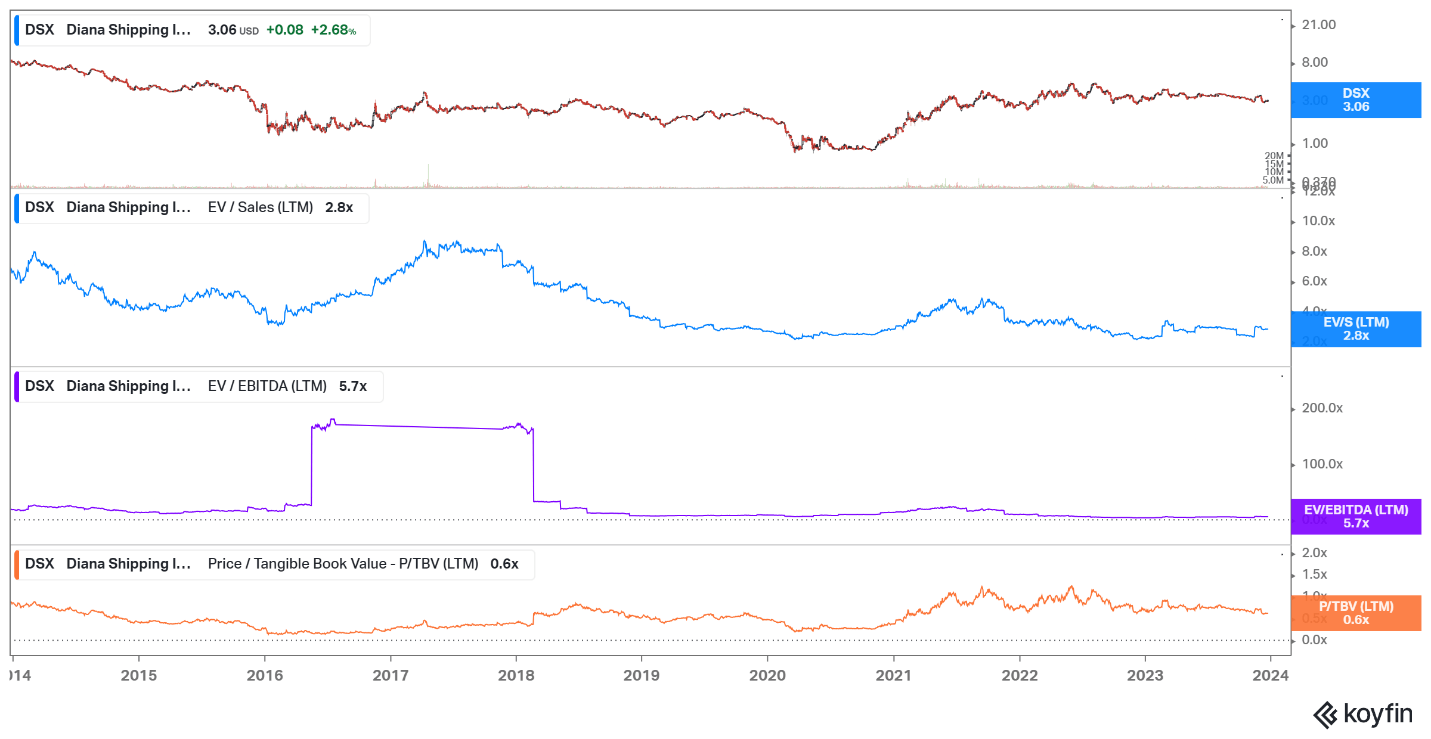

I compare the DSX current multiples in the chart below with its past figures.

{kind=link}

DSX multiples are below their peaks (8.1 EV/Sales, 170 EV/EBITDA, 1.4 P/TBV) and below its five-year average (3.04 EV/Sales, 9.09 EV/EBITDA, 1.02 P/TBV). DSX trades at fair multiples compared to similar-sized bulker shipping companies. Conversely, the company seems cheaper, considering its 5Y average and 10Y peak multiples.

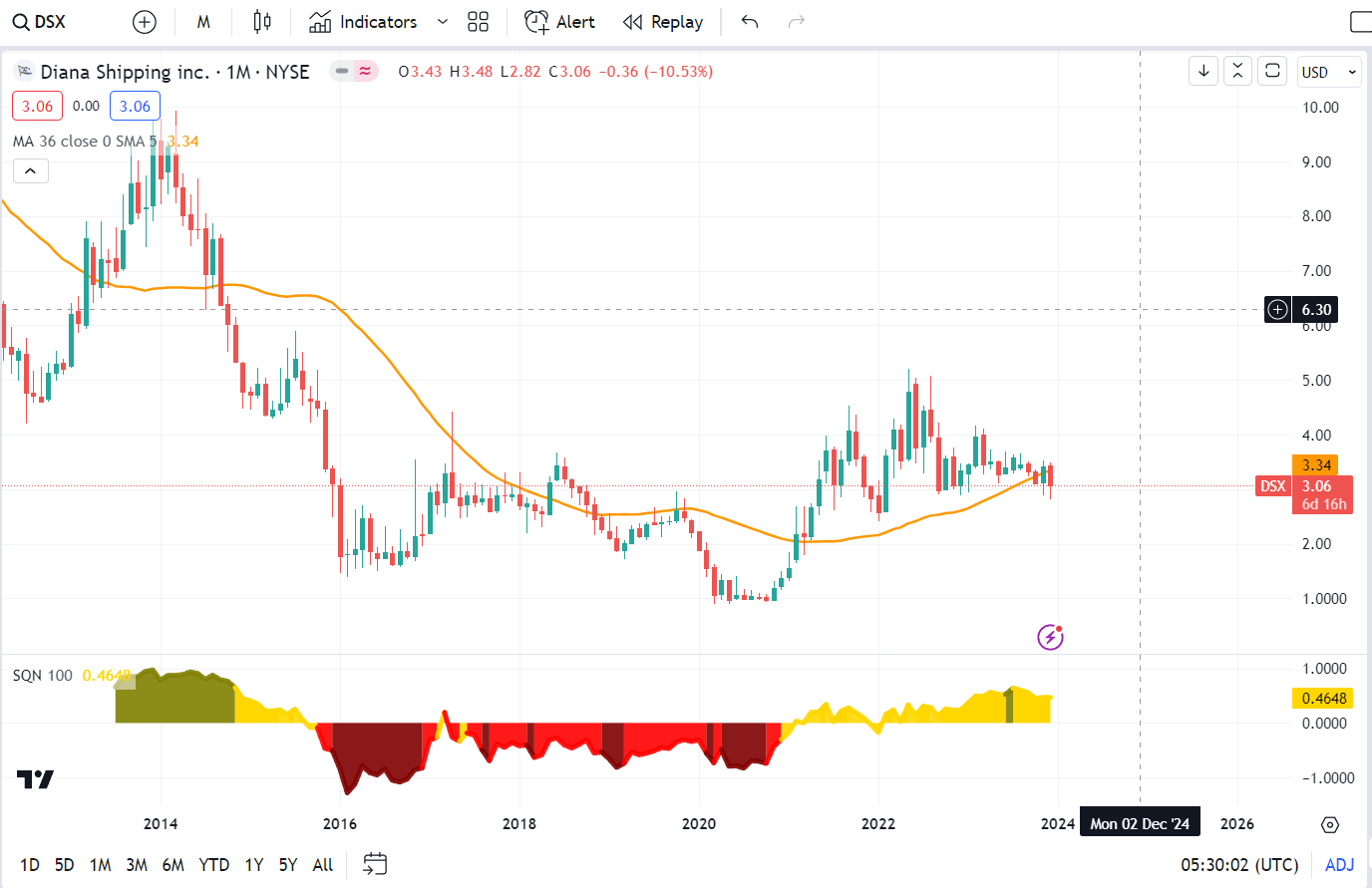

Price Action

DSX price action is not yet supportive. However, this might change.

{kind=link}

The price on the verge to breakout above 36 monthly moving average and significant price level $3.0-$3.5. SQN indicator is in a neutral regime. If the monthly candle closes above $3.5, it will give a good point for initial entry. Till then, I prefer to wait. The market rewards patience, not activity, and I prefer to stick to that maxim.

Risks

The primary risk is China. If its economy enters a recession, the demand for iron ore will decline, adversely impacting the demand for bulkers. The situation with metallurgical and thermal coal is similar. The fiscal stimulus , I believe, will suppress the issues and boost economic activity, at least for a while.

Financially, DSX is sound. It has enough liquidity to face its debt obligations and to carry out its operations. Significant maturities are coming in the 2026-2027 period. Given the company’s cash position and profitability, I do not expect any issues paying its debts.

The higher the geopolitical risk, the higher the shipping companies’ profits. However, not all ships are equal. I think the vessels that benefit most from the Red Sea crisis are product tankers and containers. The former connects European customers with Asian and Middle Eastern oil refineries. The containers passing via the Red Sea carry goods from China, Malaysia, and Vietnam to Europe.

The bulkers follow different routes due to the scattered location of their cargo: iron ore from Brazil, coal from Australia, and bauxite from Guinea. To carry the coal and the iron ore to China, India, or the US (the largest consumers of both), the vessels follow different routes, not including the Red Sea. That does not mean the bulkers will not be affected by the reduced capacity of Suez/Bab el Mandeb but to a lesser degree.

Investors takeaway

DSX is a good shipping company with profitable operations. It has 42 vessels with an average age of 10.5 years. The fleet utilization has been 99-100% over the last two years. Only 2% of the fleet has scrubbers. The company expects delivery of two methanol dual fuel vessels in 2027/2028. DSX has a healthy balance sheet with enough liquidity to cover its debts. The company has excellent margins and returns compared to similar-sized companies. DSX pays dividends with an impressive yield, 21.27% TTM. NTM yield is 12.9%. DSX trades at fair multiples compared to similar-sized bulker shipping companies. Conversely, the company seems cheaper, considering its 5Y average and 10Y peak multiples. I give DSX a hold rating.

For further details see:

Diana Shipping: Good Company And High Dividend Yields Sometimes Are Not Enough