DSX - Diana Shipping: Navigating Troubled Waters

2023-10-18 21:15:00 ET

Summary

- Diana Shipping Inc. faces significant financial challenges with a 71% decline in net income and a drop in EPS in Q2 2023.

- The company's time charter revenues fell by 9.6%, despite increasing its fleet size, and vessel operating expenses increased by 23%.

- External factors like slow economic growth forecasts and challenging market indicators further compound the risks.

Investment Thesis

Diana Shipping Inc. (DSX) presents a complex investment case that requires a nuanced evaluation. On the one hand, the company's robust cash position of $197.6 million provides a financial cushion, backed by a net debt of $671.9 million, which is balanced against this strong cash reserve. The sale of its "Boston" vessel for $18 million and the acquisition of new technologically advanced vessels for $92 million indicate strategic asset management aimed at long-term growth. With a fleet utilization rate of 99.6% and a workforce of 1,024 employees, operational efficiency appears to be a strong suit. Refinancing existing loans extends debt maturity to 2025, adding financial stability.

However, there are red flags. A 71% YoY decline in net income and a 9.6% reduction in Time Charter Revenues, despite an increase in fleet size from 35 to 41 vessels, raise questions about profitability and operational efficacy. Operating expenses have surged, and liquidity is impacted with a YoY decline in operating income from $40.4 million to $19.5 million.

Baltic Indices and IMF projections suggest headwinds for the dry bulk carrier industry, and slow economic growth forecasts for the U.S. and China add external risks. Given these multifaceted factors, the investment strategy leans towards a 'Hold' recommendation, suitable for a conservative investor with a long-term view.

Overview

In Q2 2023, Diana Shipping Inc. saw a significant drop in its financial numbers compared to the previous year. The company announced a dividend payout of $0.15 per share, demonstrating its commitment to rewarding shareholders. This payout is backed by a solid cash position of $197.6 million, offering a financial cushion for operations and potential investments. The financial health is further emphasized by the company's net debt of $671.9 million, which might seem like a large number but is well-balanced against the strong cash position.

The company announced the sale of its "Boston" vessel for a solid $18 million. This isn't just about getting rid of an asset; it's about immediate liquidity. With $18 million cash in hand, the company can allocate this capital to other strategic areas to maximize returns. For instance, Diana Shipping has already committed to investing in new technology by buying two 81,200 DWT methanol dual fuel new-building Kamsarmax dry bulk vessels for $46 million each, totaling a substantial investment of $92 million. These new vessels are expected by the second half of 2027 and the first half of 2028. This is pivotal because these new vessels are equipped with advanced methanol dual fuel technology, which aligns with the shipping industry's move toward sustainability and could give Diana Shipping an edge in future regulatory scenarios.

Besides these acquisitions, Diana Shipping has also strategically entered into multiple time charter contracts that are going to bring in a steady cash flow. These charter contracts have gross rates ranging between $11,250 and $14,250 per day. When you add it up, these charters are expected to generate at least $8.91 million in gross revenue. This is a crucial revenue stream, especially when you consider that they've extended some of their existing charter contracts, like the one with Reachy Shipping, thereby ensuring that their vessels won't be sitting idle and will continue to generate revenue. This is particularly important because idle ships can become a financial drain.

In terms of industry outlook, the global shipping business is leaning more towards sustainable solutions. Diana Shipping's investment in advanced fuel technology puts it in a favorable position both for regulatory approvals and for long-term sustainable operations. The $92 million commitment to new vessels is not just an expenditure; it's a long-term investment aimed at positioning the company for sustainable growth in an industry that's becoming increasingly eco-conscious. But investments like these aren't without risks. There's market volatility that can affect shipping rates and long-term contracts. And then there are future environmental regulations that the company will need to comply with.

One standout metric is the company's fleet utilization rate of 99.6%. This is a vital sign of operational efficiency. The company is nearly using its entire fleet to generate revenue, which is uncommon in an industry plagued with inefficiencies. This high utilization rate also sets the company above industry averages, making it a strong player in a challenging environment. The workforce behind this high utilization rate is robust, with 1,024 employees ensuring smooth operations.

The company has refinanced its existing loans and secured new term loans from Danish Ship Finance and Nordea Bank. Refinancing is a strategic move here; it's not just about swapping out old debt for new. It improves the company's financial flexibility, allowing it to adapt to a volatile market. Importantly, the company has no debt maturing until the end of 2025, offering a stable financial future and making it an attractive long-term investment.

The company acquired the DSI Drammen vessel for $27.9 million, indicating a proactive approach to expanding its revenue-generating assets. It's also diversifying through joint ventures, like the one for an Ultramax vessel, broadening its operational scope and revenue streams.

However, market indicators like the Baltic Indices and IMF projections suggest a challenging environment for dry bulk carriers, impacting the long-term sustainability of the company. Additionally, slow economic growth forecasts for the U.S. and China, major players in shipping, could negatively impact the company. Even though Diana Shipping has secured 80% of its 2023 revenue and 31% for 2024, the challenging market conditions make long-term investment in the company risky.

To sum it all up, the company’s focus on high fleet utilization, strategic refinancing, and a strong workforce makes it a stable bet for long-term investment, albeit not entirely devoid of market risks.

Revenue Analysis

{kind=link}

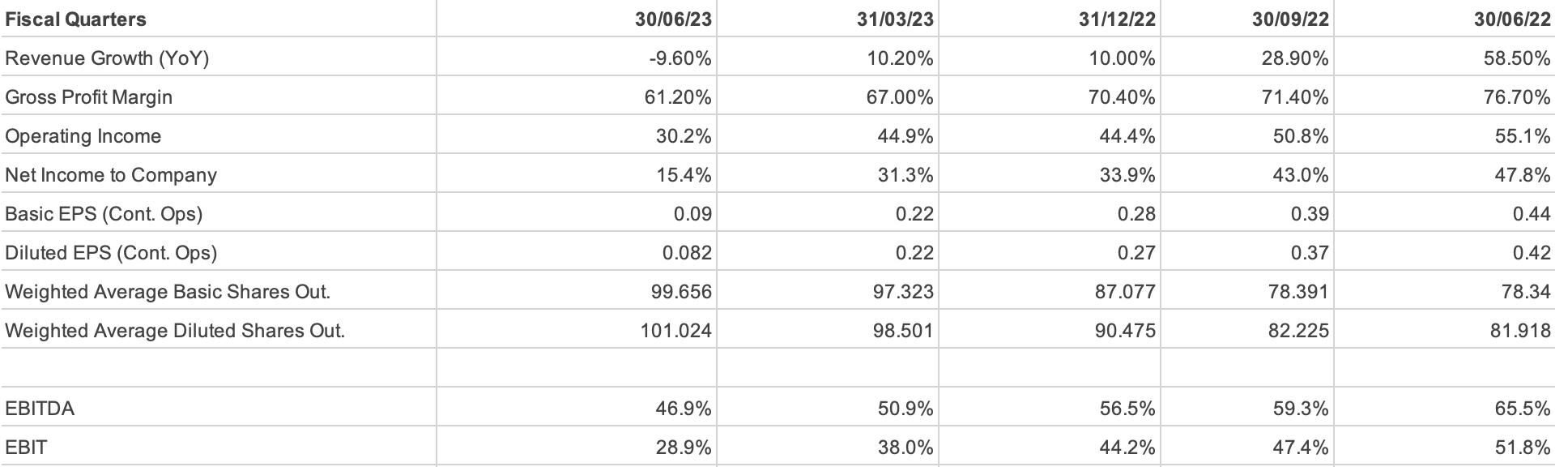

In Q2 2023, the company's Net Income decreased to $10.364 million from $35.606 million in Q2 2022, marking a 71% decline. This trend is also reflected in a six-month view, where the Net Income fell from $61.649 million to $33.077 million. Alongside this, Time Charter Revenues, the core revenue stream, saw a 9.6% reduction, dropping from $74.522 million to $67.379 million, despite the number of vessels in the fleet growing from 35 to 41 over the same period. The company experienced a quarter-over-quarter (QoQ) decline of 9.59%, implying a reduction in chartering activities and a fall in rates charged. For the half-year comparison, revenues remained relatively stable, falling only by a marginal 0.31%, indicating some resiliency in this revenue stream over a longer period.

Voyage Expenses, the costs incurred during a ship's voyage, increased by 438.06% QoQ and 1,010.71% HY. These numbers could result from resuming halted voyages and embarking on new ones, indicating a significant ramp-up in activities.

Another worrying signal is the increase in Vessel Operating Expenses by 23% from $18.4 million to $22.6 million in the same period. These consistent increases could point to higher maintenance costs.

The biggest red flag, however, comes from the Net Income metrics. The company’s net income plummeted by 70.89% QoQ and 46.35% HY. This significant decline and the surge in operating expenses raise serious concerns about the company’s current profitability and future financial stability. These factors have had a negative impact on the EPS, dropping it from $0.44 to $0.09, making the stock less appealing to individual investors.

The sharp drop in net income and increase in operational costs do bring into question the quality of earnings and the potential for one-time events or manipulations.

Projecting forward, if these declining trends continue, the company could face a Net Income of around $5 million and Time Charter Revenues close to $60 million by Q2 2024. Given these indicators, the immediate focus should be closely monitoring Net Income and Time Charter Revenues in upcoming quarterly reports.

The company's strength lies in the relatively stable half-year revenues, while the weaknesses and threats are predominantly from increasing operational costs and plummeting net income. Based on the available data, the investment recommendation is to 'HOLD' the stock.

Balance Sheet Analysis

Starting with liquidity, the company has a robust Current Ratio of 4.83, calculated by dividing its current assets of $215,314k by its current liabilities of $44,561k. This high ratio means the company has ample short-term assets to meet its immediate obligations, making it financially stable in the short run.

However, when we look at solvency through the Debt to Equity Ratio, which is 1.38, things become a bit concerning. This ratio is derived by dividing the company's total debt of $671,934k by its total stockholders' equity of $487,388k. Given these figures, it's prudent to predict that if current trends continue, the company could face further declines in fixed assets and increases in long-term debt, which may lead to using its cash reserves to service these rising liabilities.

Stockholders' equity has remained almost static, from $487.3 in 2022 million to $487.38 million in 2023, suggesting neither significant dilution of shares nor a fresh inflow of capital. This static equity position could signal that Diana Shipping is not generating enough retained earnings, limiting its internal funding options and possibly pushing it towards more debt financing in the long run.

The cash and cash equivalents have increased from $143.9 million at the end of 2022 to $197.6 million as of June 2023, boosting liquidity. It hints at positive cash flow generation, probably from its core business activities. However, there's an increase in long-term debt from $663.4 million to $671.9 million, and a decrease in fixed assets from $996.7 million to $958.6 million. These shifts indicate that the company is taking on more debt without investing in its growth or assets, raising questions about its long-term financial strategy.

Now, projecting into the future, if the existing trend of incrementally rising assets and debts continues, Diana Shipping could face both liquidity and solvency issues. It urgently needs to improve its profitability and curtail its burgeoning debt to avoid future financial instability.

Free Cash Flow Analysis

{kind=link}

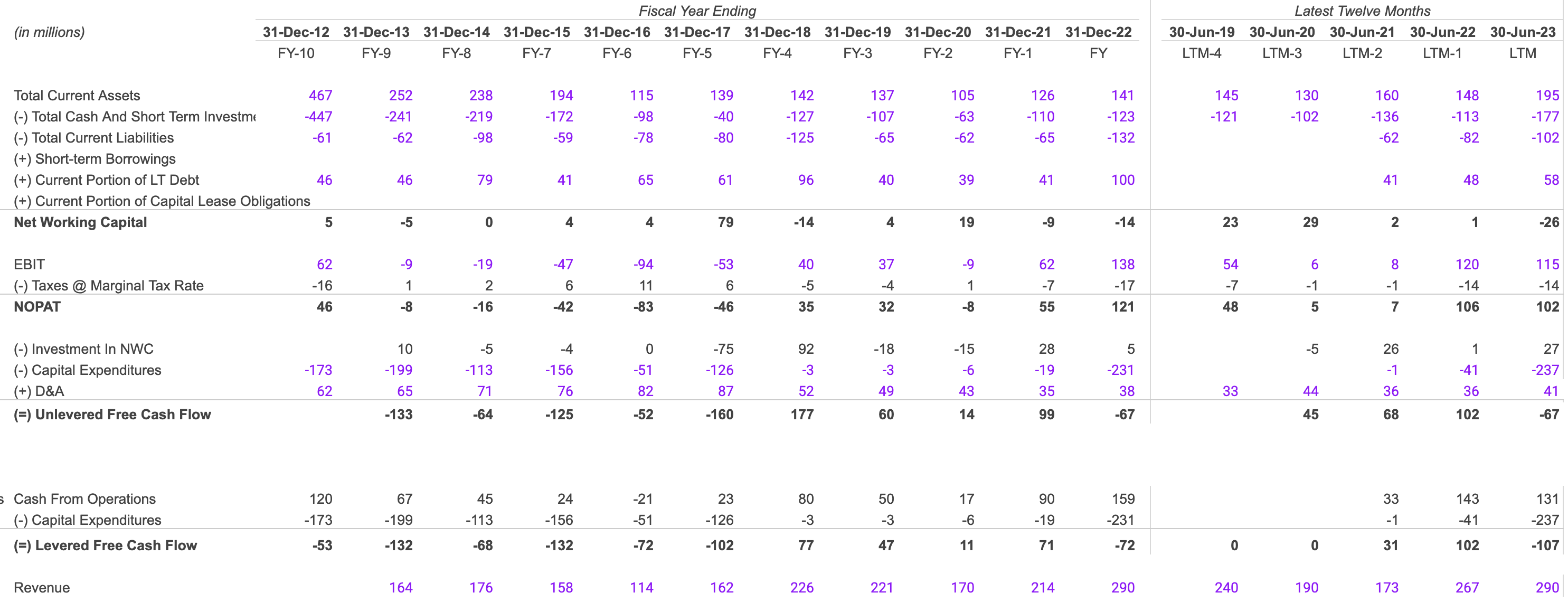

On the operating front, cash from operations surged from $33M in 2021 to $143M in 2022, indicating robust growth in sales and operational efficiency. However, this dropped slightly to $131M in 2023, signaling potential stagnation. In terms of investing, the company increased its capital expenditures from -$1M in 2021 to -$237M in 2023, which suggests aggressive investment in long-term assets but also locks up a significant amount of cash. On the financing side, short-term debts, including the current portion of long-term debt, rose steadily from $41M in 2021 to $58M in 2023. This escalating debt can pose a risk if not covered by operational cash flow, which already shows signs of slowing down.

The Unlevered Free Cash Flow plummeted from $68M in 2021 to a negative $67M in 2023, primarily due to increased capital expenditures. This could be a calculated risk if these investments generate higher returns in the future. But as of now, it's a warning sign. Levered Free Cash Flow also swung into the negative at -$107M in 2023, indicating possible liquidity issues. Coupled with increasing debts, the company might need to secure additional financing or improve its operational efficiency to avoid liquidity issues.

EBIT rose from $8M in 2021 to $120M in 2022, demonstrating robust operational health, although it dipped to $115M in 2023. NOPAT grew from $7M in 2021 to $106M in 2022 but slightly decreased to $102M in 2023, suggesting a strong core business. Meanwhile, revenue has been consistently rising from $173M in 2021 to $290M in 2023, showing strong market demand. However, Net Working Capital dropped to a negative $26M in 2023, a red flag indicating the company may struggle to meet its short-term liabilities, thus questioning the quality of its earnings.

The one-year forecast suggests these cash flows could rebound, but that's contingent on the ROI generated by these new capital investments, which need to be closely monitored. Due to these factors, the immediate investment recommendation is to hold, while keeping a close eye on ROI from capital expenditures and the NOPAT figures.

Cash Conversion Cycle

{kind=link}

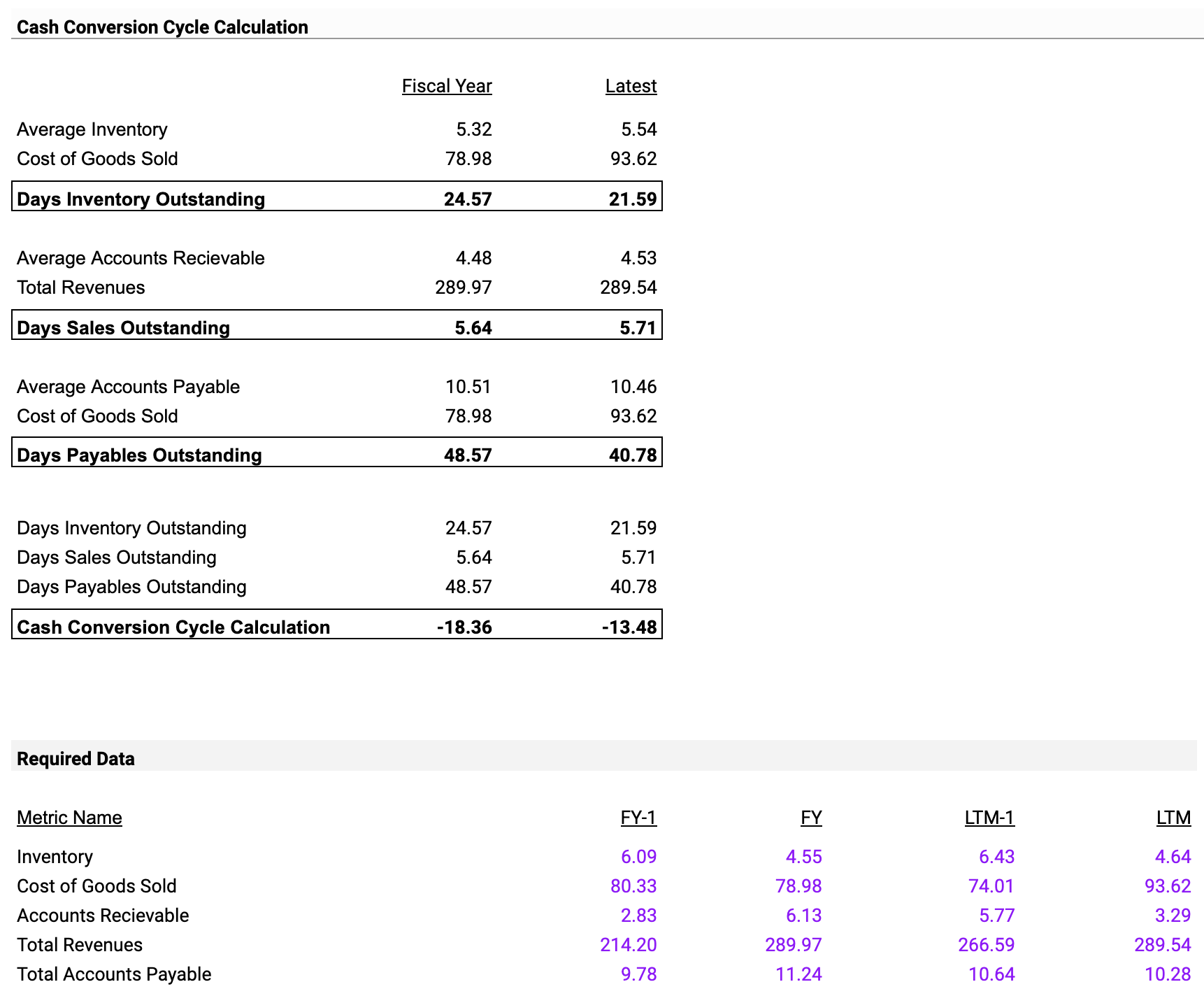

Between December 2022 and June 2023, the company saw an 18.6% rise in its Cost of Goods Sold (COGS) from $78.98M to $93.62M, without a matching increase in revenue, which stayed nearly flat at around $289.5M. This raises a red flag about potentially increasing operational costs and shrinking profit margins. Average inventory and accounts receivable also increased by 4.1% and 1.1%, respectively, hinting at potential liquidity issues.

At the same time, Days Inventory Outstanding dropped from 24.57 to 21.59 days, signaling faster inventory turnover. Conversely, Days Sales Outstanding ((DSO)) edged up from 5.64 to 5.71 days, while Days Payables Outstanding ((DPO)) decreased from 48.57 to 40.78 days, meaning the company is paying its suppliers more quickly. These changes led to a Cash Conversion Cycle ((CCC)) shift from -18.36 days to -13.48 days, pointing to less efficiency in converting resources into cash.

Given these metrics, the immediate focus should be on the rising COGS and the less efficient cash conversion cycle. If these trends persist, the company could face profitability challenges.

Shareholder Yield

{kind=link}

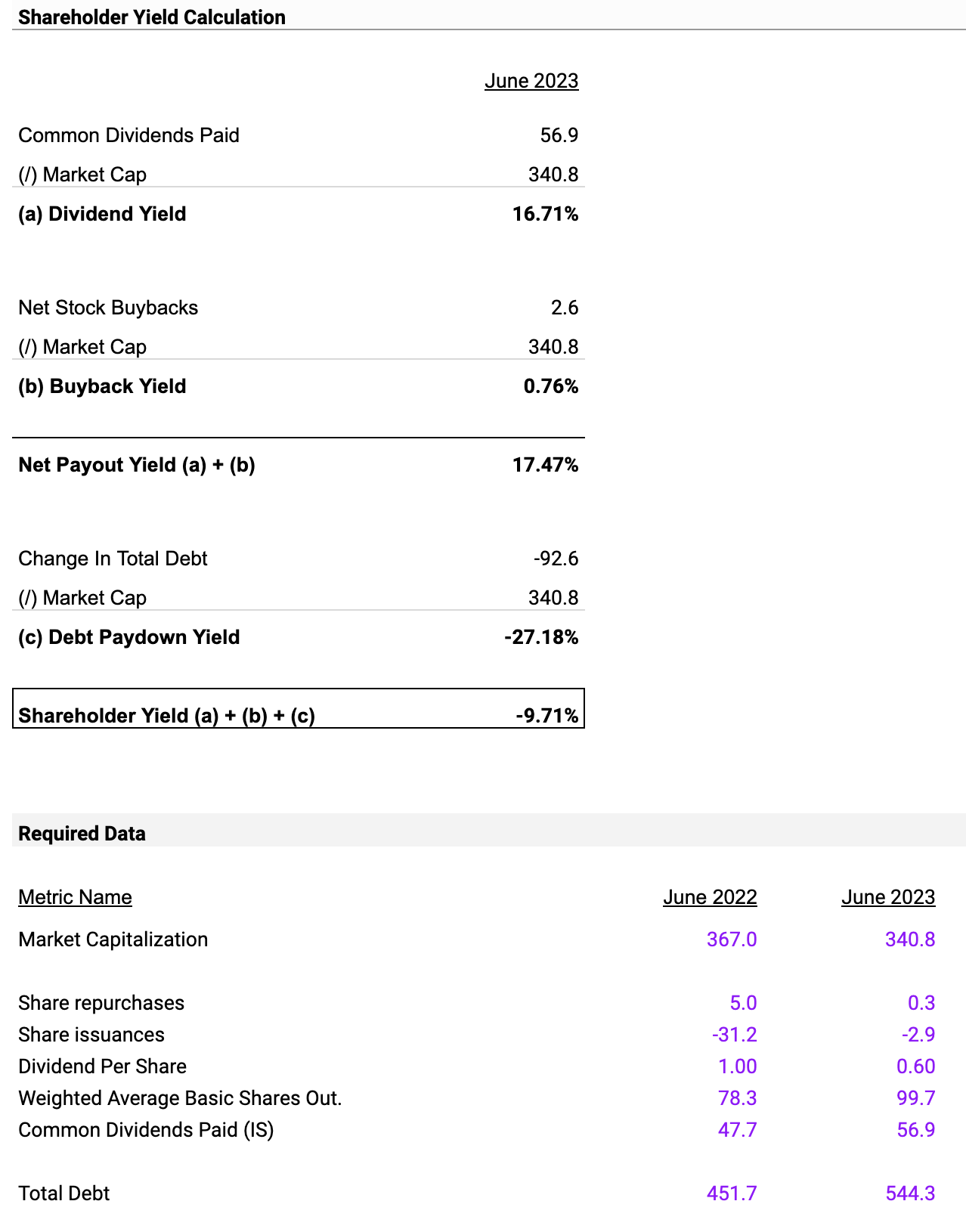

The company has a high Dividend Yield of 16.71%, calculated from its Common Dividends of $56.9M and a Market Cap of $340.8M, which could be a positive sign of investor confidence and a red flag if unsustainable. Its Buyback Yield stands at 0.76%, based on Net Stock Buybacks of $2.6M, indicating that share buybacks aren't aggressive. Adding these, the Net Payout Yield is 17.47%, which is worrying as the company doesn't have strong cash flows to support it. Simultaneously, the Debt Paydown Yield is -27.18%, showing the company reduced its Total Debt by $92.6M, marking an aggressive stance on debt reduction.

As a result, the overall Shareholder Yield is negative at -9.71%, suggesting a decrease in shareholder value. Given these metrics, immediate attention is needed to scrutinize the high Dividend Yield and negative Shareholder Yield. If the trend of debt reduction continues while maintaining a high Dividend Yield, the company might face liquidity issues.

In terms of investment, the best course right now is to 'Hold' while monitoring these critical financial metrics and the company's strategies behind them.

Valuation

I do an EV/EBITDA comparable valuation analysis for Diana Shipping.

Benchmark Companies:

{kind=link}

The companies selected for benchmarking include Euroseas Ltd. (ESEA), Safe Bulkers, Inc. (SB), Seanergy Maritime Holdings Corp. (SHIP), Eagle Bulk Shipping Inc. (EGLE), and Star Bulk Carriers Corp. (SBLK). These companies operate within the same industry as Diana Shipping Inc. and exhibit similar business models, thereby making the comparison relevant and credible.

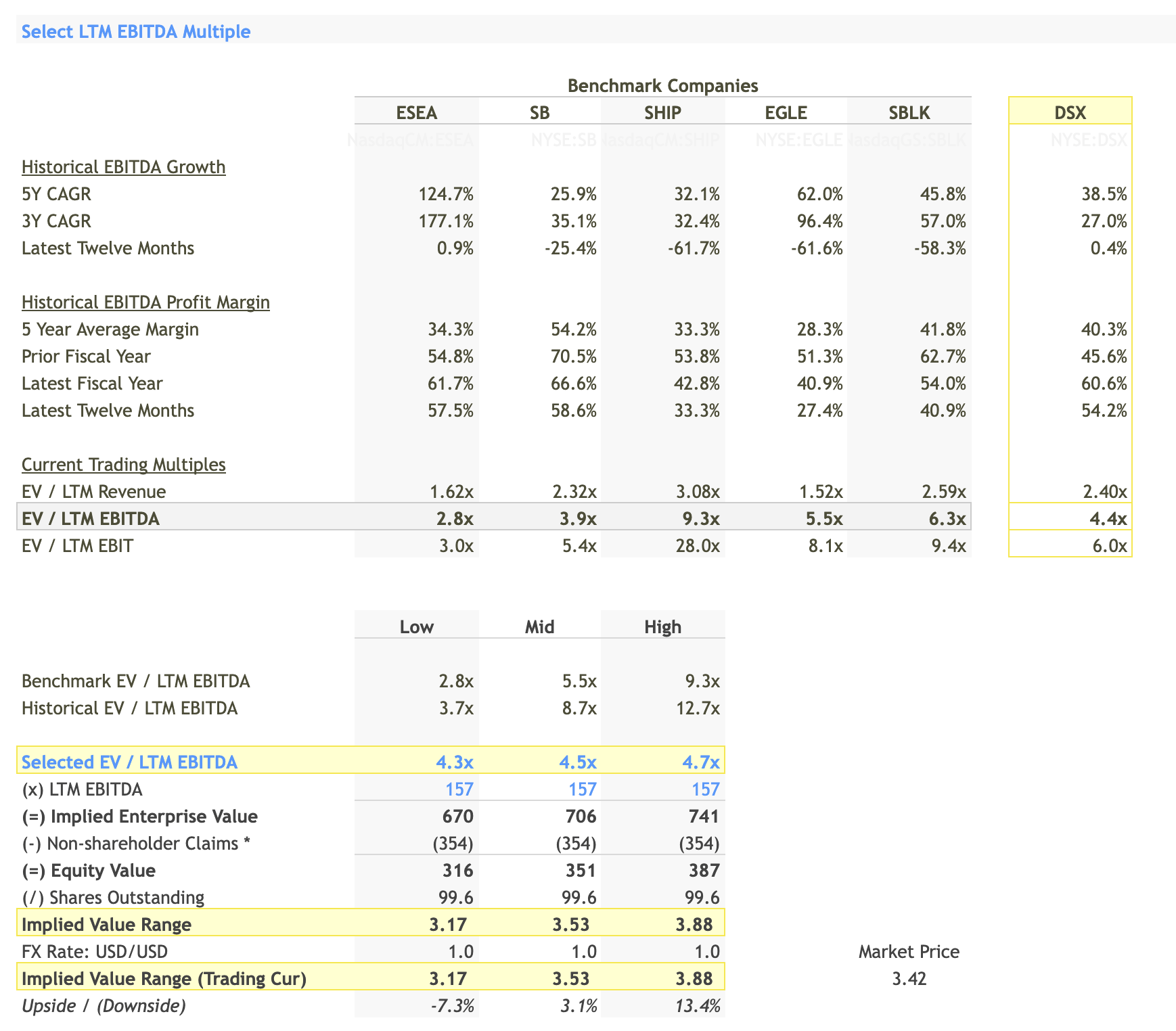

Select LTM EBITDA Multiple:

{kind=link}

The LTM (Last Twelve Months) EBITDA multiples for the benchmark companies range from a low of 2.8x ( ESEA ) to a high of 9.3x (SHIP). Diana Shipping Inc. itself has an LTM EBITDA multiple of 4.4x. The selected LTM EBITDA multiple range for Diana Shipping is 4.3x to 4.7x, which is within the industry range and reflects its 0.4% LTM EBITDA growth and 54.2% LTM EBITDA margin. These numbers substantiate that Diana Shipping is moderately positioned in terms of profitability and growth compared to its peers.

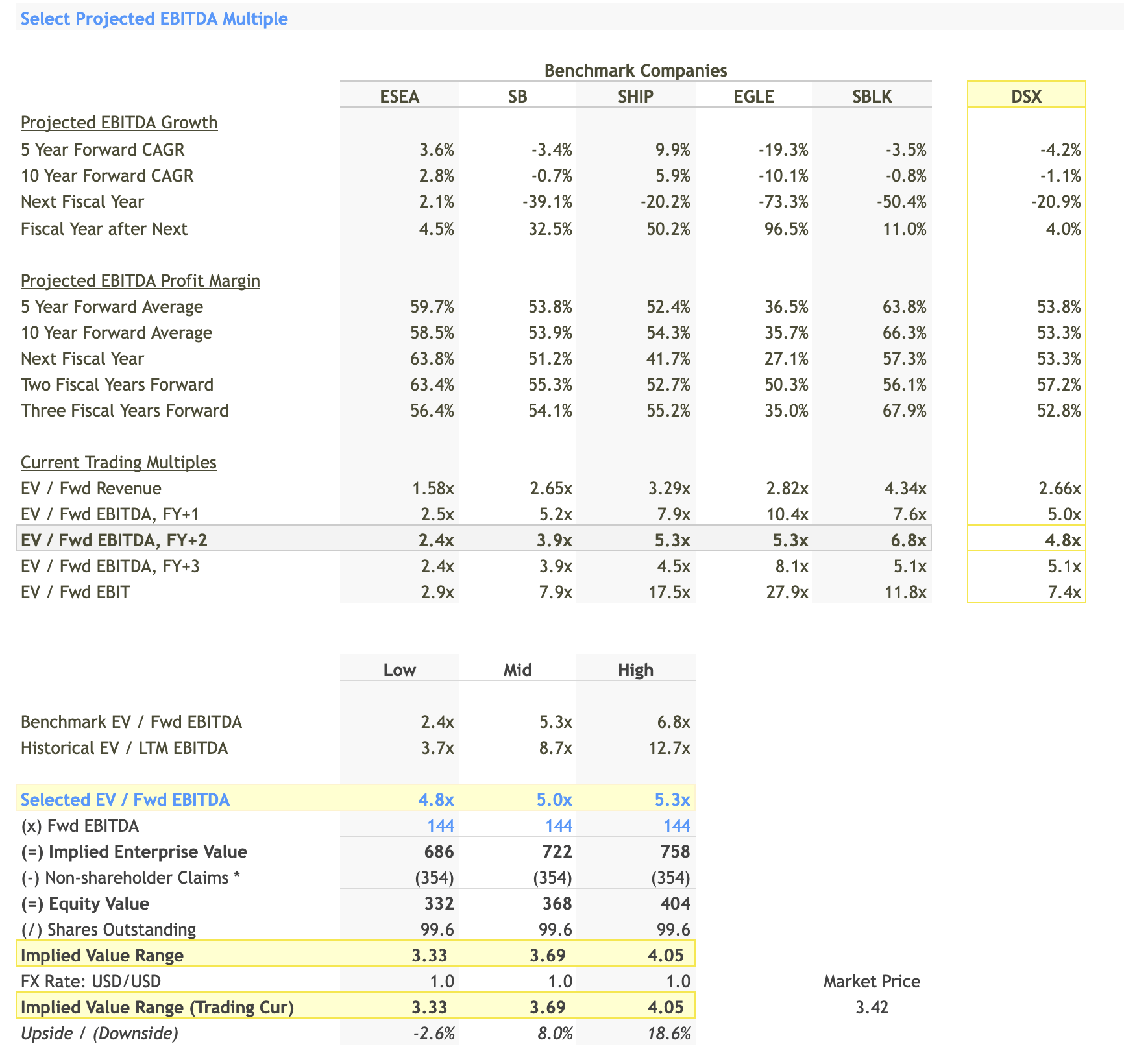

Select Projected EBITDA Multiple:

{kind=link}

The projected EBITDA multiples for the benchmark companies in the next fiscal year (FY+1) range from 2.5x ( ESEA ) to 10.4x (EGLE). The selected projected EBITDA multiple for Diana Shipping is between 4.8x and 5.3x. This is consistent with its projected EBITDA growth rate of -20.9% for the next fiscal year and a margin of 53.3%. These forward-looking multiples indicate that while Diana Shipping may experience a contraction in EBITDA growth, it is likely to maintain a relatively stable EBITDA margin, justifying the selected multiple range.

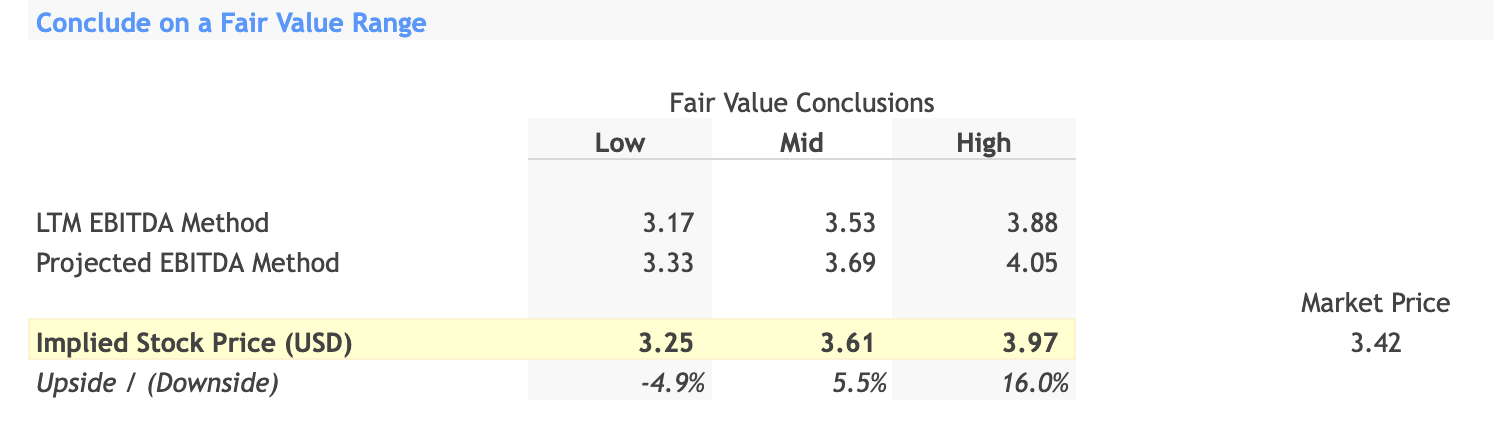

Fair Value Range:

{kind=link}

Based on the LTM EBITDA method, the implied stock value range is between $3.17 and $3.88. According to the projected EBITDA method, the implied stock value is between $3.33 and $4.05. Combining these two methods provides a comprehensive fair value range for Diana Shipping from $3.25 to $3.97. This range is derived by averaging the low, mid, and high values from both LTM and projected EBITDA methods.

Investment Decision:

The current market price of Diana Shipping's stock is $3.42. The fair value range suggests an implied stock price between $3.25 and $3.97. The downside risk is about -4.9%, and the upside potential is approximately 16.0%.

Given this range and the current market price, the investment recommendation for Diana Shipping is a 'Hold'. The company shows moderate EBITDA growth and profitability compared to its peers but also faces forward-looking contraction in EBITDA.

This mixed outlook validates a 'Hold' position, as the stock is fairly valued with limited downside and moderate upside potential. Therefore, at the current market price, the stock neither offers a substantial discount nor is it overly expensive, making 'Hold' the most prudent recommendation.

For further details see:

Diana Shipping: Navigating Troubled Waters