DKS - DICK'S Is Impressive - But Is It Enough?

2023-09-24 04:39:58 ET

Summary

- DICK'S Sporting Goods excels with strong sales, rising dividends, and a robust market strategy.

- The company's success lies in in-store expertise, a diverse product range, and efficient distribution methods.

- While DKS performs well, its stock's volatility and economic uncertainties suggest cautious consideration, especially given current inflation concerns.

Introduction

It's fall. Football season has started. Baseball playoffs are about to start, and the start of the NBA regular season is just one month away.

One might say it's the best time of the year!

What better way to start an article covering one of America's go-to places for sports equipment?

DICK'S Sporting Goods ( DKS ) is a 3.6% yielding retail giant catering to a wide variety of sports equipment needs. The company has consistently outperformed the S&P 500 and adopted a policy of consistently rising dividends, buybacks, and special dividends that have paid off handsomely.

In this article, we'll discuss all of that, in addition to the challenging macroeconomic environment and the company's mildly unfavorable volatility profile, which requires the ability to somewhat time one's entry.

So, without further ado, let's get to it!

About DICK'S And Its Dividend

Generally speaking, I'm not a huge fan of the consumer cyclical industry. While it is home to some fantastic companies, it's competitive, prone to (online) disruptions, and volatile consumer sentiment.

I own just one consumer stock, which is Home Depot ( HD ). One of the reasons why I own it is its wide moat in a competitive industry and the fact that it has become a go-to place for things that people usually do not buy online. It also has ways to order online and pick it up at the store.

DICK'S is different yet similar. Although people buy shoes and related equipment online, most people prefer to test things before buying - especially when making higher-ticker purchases. In-store expertise is key.

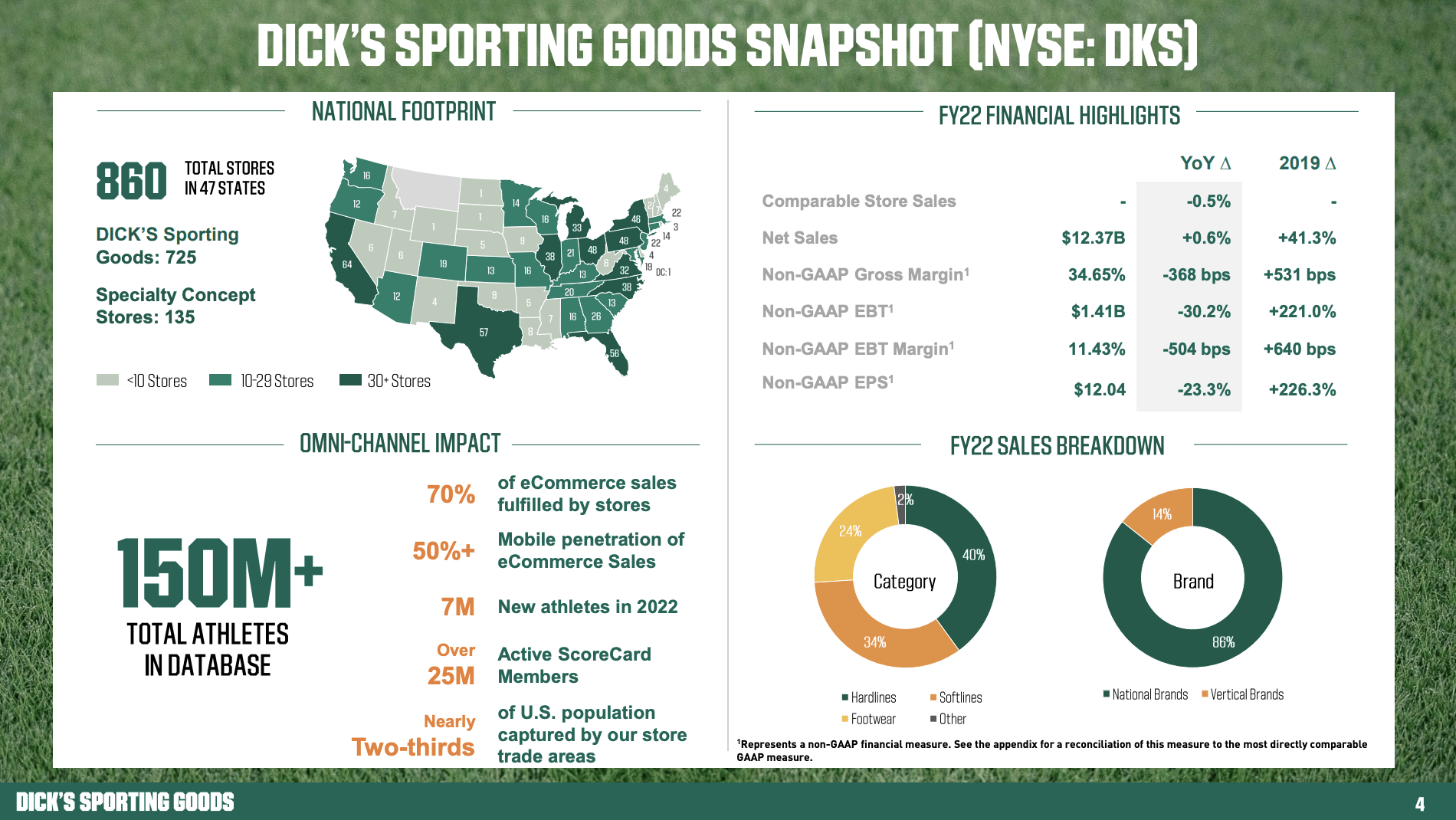

Founded just three years after the Second World War, DICK'S has grown into a giant with roughly 860 stores in 47 states.

{kind=link}

Paraphrasing the company's 10-K, DICK'S has formulated a comprehensive business strategy that centers around its core belief in the transformative power of sports in people's lives.

This belief fuels their drive to offer an unparalleled athlete experience, engaging brand interactions, a diverse product range, and, most importantly, a dedicated team of employees referred to as teammates.

In other words, the company has obviously realized that brick-and-mortar stores have tough competition from online stores. Thriving means excelling at offering great service.

This is based on a number of pillars, including the ones below.

- Optimizing Assortment : DKS is offering a broad range of products within each category, catering to different athlete segments and promoting both national and proprietary brands to diversify the product portfolio.

- Omni-channel Platform and Fulfillment : To ensure a seamless experience across retail stores and online platforms, the company is leveraging its extensive store network for efficient distribution and fulfillment.

- Merchandising : The key is focusing on the right mix of hardlines, apparel, and footwear to drive sales and adapt the product assortment to changing market dynamics.

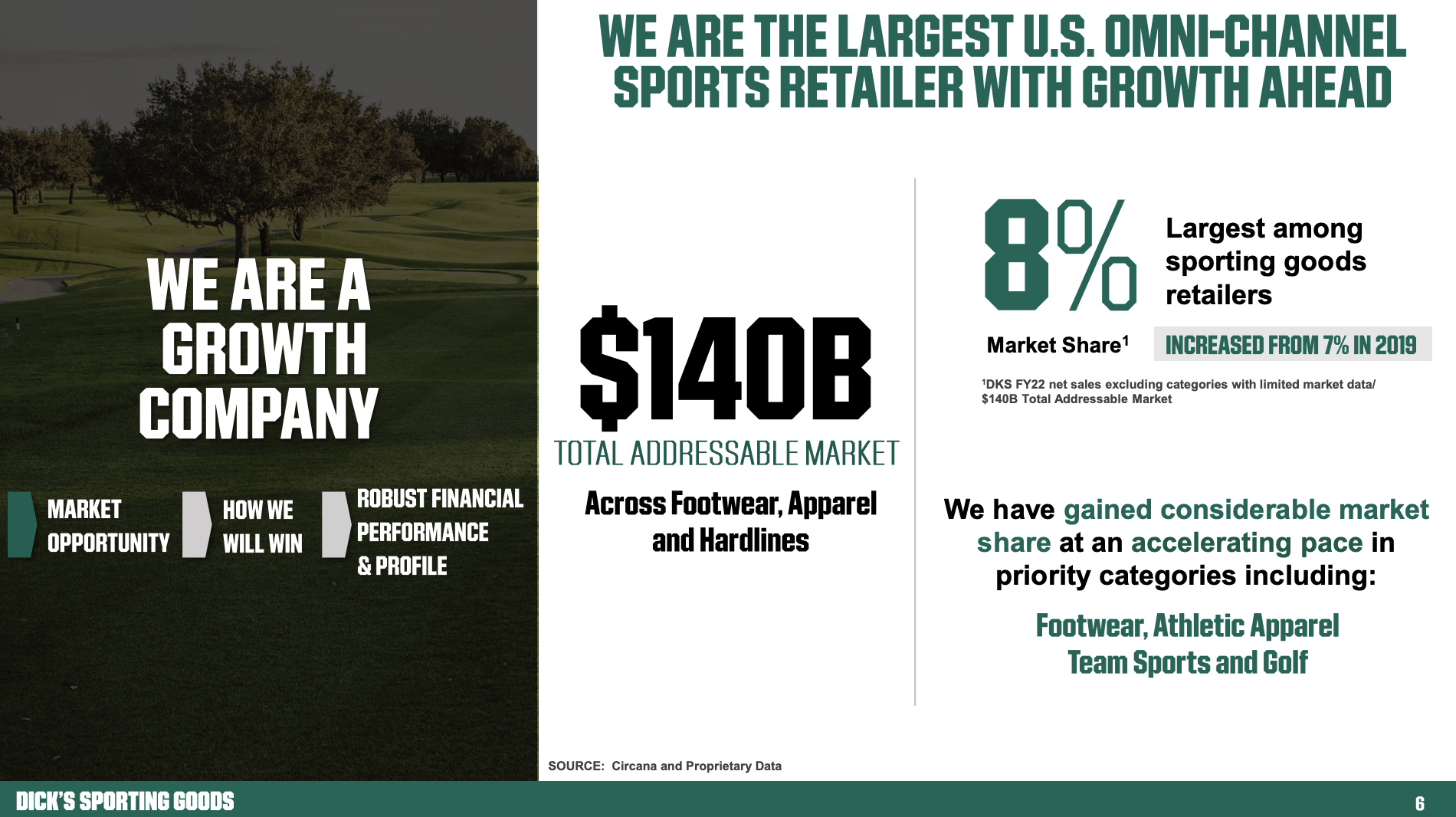

So far, this has been a highly efficient strategy, allowing the company to grow its market share from 7% in 2019 to 8% in 2022. 1% may not sound like much, but it definitely is, given that the total addressable market is $140 billion.

{kind=link}

In addition to that, the company is committed to returning capital to shareholders.

The company currently pays a $1.00 per share per quarter dividend. This translates to a yield of 3.6%.

The dividend is protected by a 25% net income payout ratio.

Over the past five years, the average annual dividend growth rate was 33%, mainly boosted by a 105.1% hike announced on March 7.

As the chart above shows, the company also pays special dividends.

In 2021, the company paid a special dividend of $5.50 per share.

The dividend is also protected by a healthy balance sheet. Analysts expect DKS to end this year with $480 million in net cash, which means the company will have $480 million more in cash than gross debt.

This year, the company is expected to generate $560 million in free cash flow, which translates to an implied free cash flow yield of 6.0%. This number protects its 3.6% dividend. Next year, free cash flow is expected to rise to $910 million, which would imply a 9.7% free cash flow yield.

Furthermore, over the past ten years, the company has bought back more than 30% of its shares.

Having said that, let's dive into the company's numbers, as it's in a very tricky spot, given the unpleasant headwinds consisting of elevated inflation and weakening economic growth.

DICK'S Remains Strong

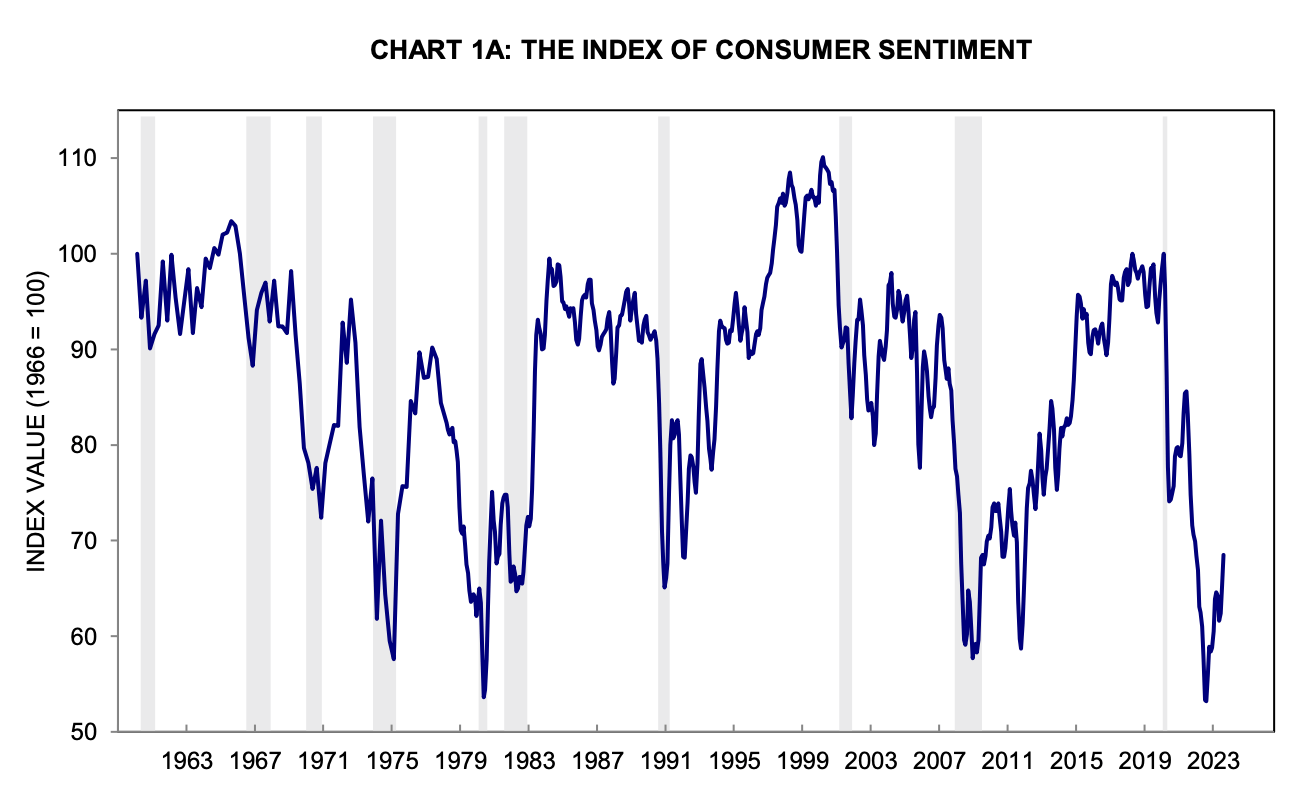

Although consumer confidence has rebounded, it remains at extremely subdued levels.

{kind=link}

Even worse is that oil prices have rebounded, pushing inflation up for two straight months. This is likely to keep a lid on consumer confidence.

The good news is that DICK'S has been doing quite well so far.

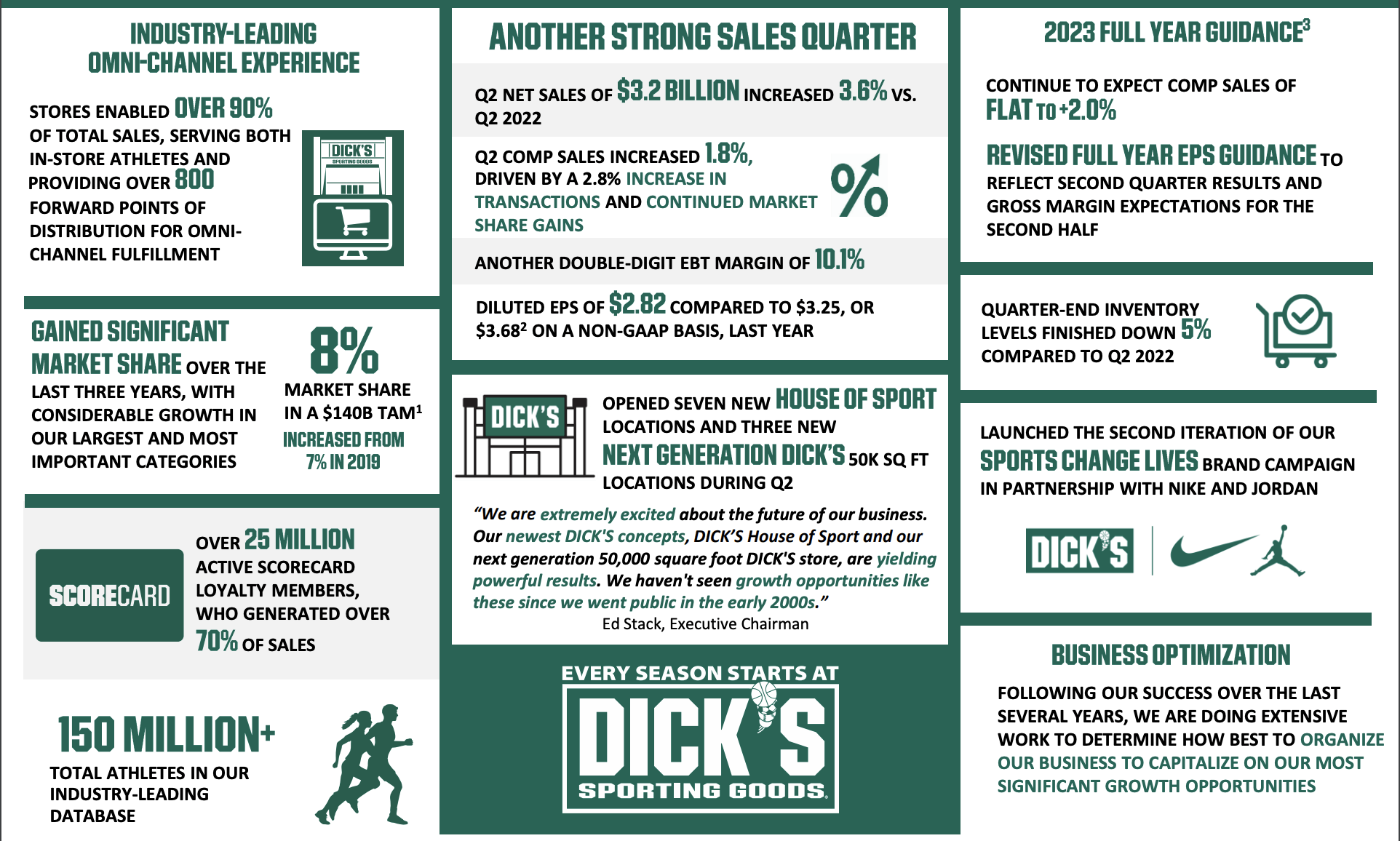

In the second quarter, total sales saw a notable 3.6% increase, reaching $3.22 billion. The key driver behind this surge was a 1.8% rise in comparable sales, propelled by robust transaction growth of 2.8%. The average ticket value was down 1%.

According to the company, this surge in sales and transactions shows a growing reliance on DICK'S Sporting Goods among athletes nationwide.

Notably, within the quarter, sales demonstrated a significant acceleration in July, coinciding with the start of the back-to-school season and the inauguration of the latest House of Sport location.

{kind=link}

Especially the footwear and team sports categories stood out in terms of performance.

Unfortunately, despite the overall sales increase, gross profit for the quarter came in at $1.11 billion, representing 34.42% of net sales, which is a decline of 161 basis points compared to the previous year.

This decrease was primarily due to a drop in merchandise margin by 254 basis points.

According to the company, actions were taken to manage excess products, especially in the outdoor category, aiming to maintain optimal inventory levels.

However, the company faced challenges due to higher-than-expected shrink, accounting for a notable portion of the merchandise margin decline. This was partly offset by lower supply chain costs.

Shrink means people are stealing stuff. This is getting out of hand lately and doing a number on the profitability of many companies.

When they reported second-quarter results, some companies like Target and Dick’s Sporting Goods offered clues into how much shrink is costing them and squarely blamed theft. Target lost about $219.5 million more to shrink during the three months ended July 29 than it did during the year-ago period. Dick’s lost about $27.1 million during the same three months, according to a CNBC analysis.

Meanwhile, Ulta and Foot Locker, which both blamed “organized retail crime” for losses in May, did not mention theft during their most recent results. They only used the term “shrink” when discussing how it squeezed margins.

Lowe’s has some of the highest shrink numbers among the companies analyzed by CNBC. It has blamed a range of factors for the losses. Sometimes it has said organized retail crime cut into profits, but in other cases, it blamed weather-related damages. - CNBC

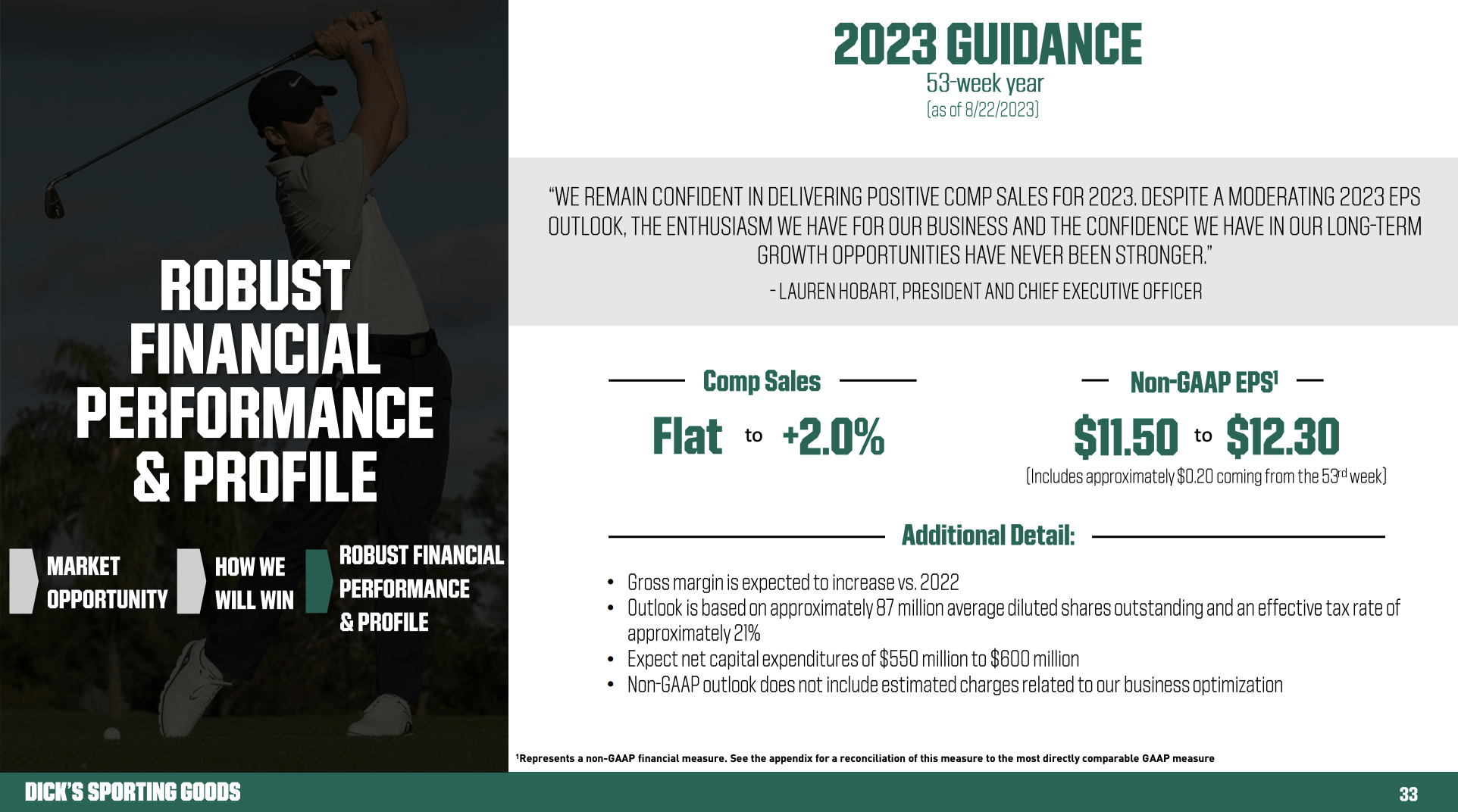

Despite these issues, DICK'S reaffirmed its expectations for comparable store sales to be in the range of flat to plus 2%.

Furthermore, management commented on macroeconomic uncertainties, including the resumption of student loan repayments, which are incorporated in its outlook.

For the full year, the company anticipates roughly 250 basis points of non-comp sales growth, including the 53rd week.

After adjusting its outlook based on the 2Q23 performance and gross margin projections, the company now expects non-GAAP earnings per diluted share to be in the range of $11.50 to $12.30. This includes expectations of improving gross margins, although impacted by higher shrink affecting the full-year gross margins.

{kind=link}

With that said, there's another thing I want to bring up, which is related to the cyclical nature of the industry DICK'S serves.

Unfavorable Volatility & Valuation

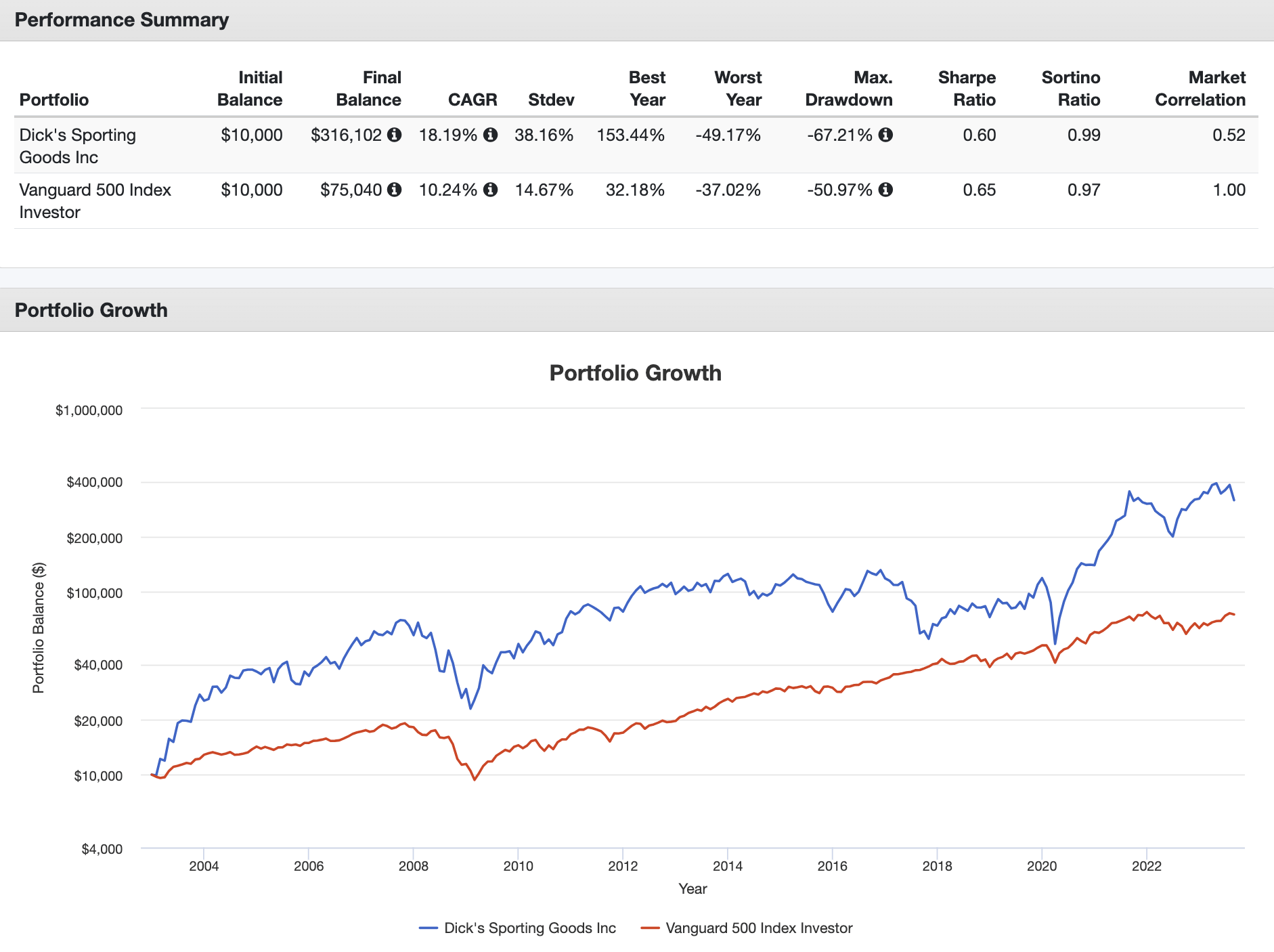

Since December 31, 2002, DKS shares have returned 18.2% per year, turning a $10,000 investment into $316,102. This beat the S&P 500 by almost 800 basis points per year.

The problem is that these returns aren't very consistent with elevated volatility. The standard deviation of DKS is 38%, which is well above the 14.7% standard deviation of the S&P 500. Most returns came from the 2002-2008, 2009-2012, and 2020-2023 periods.

{kind=link}

Over the past ten years, DKS shares have returned 12.3% per year. The S&P 500 has been compounded at 12.7% per year during this period.

This isn't a horrible result. However, DKS is a stock I would only buy on severe weakness.

Historically speaking, DKS investors have been through a lot. This also explains why its long-term standard deviation is elevated.

Currently, DKS shares are 26% below their all-time high.

Shares are trading at 5.4x forward EBITDA. That's neither undervalued nor overvalued. It's a bit in no man's land.

The current consensus price target is $133, which is 20% above the current price.

If we were in a normal economic environment of easing inflation and robust unemployment, I would make the case that DKS shares are a buy.

However, because I believe that inflation is likely to remain sticky, I cannot make the case that DKS is a buy. I will give the stock a Hold rating, as I am not very upbeat about the consumer.

Needless to say, please feel free to disagree with me in the comment section!

As much as I like how well DKS is managing its business in a very tough environment, I will have to see more stock price weakness before moving to a buy rating.

Takeaway

DICK'S stands as an impressive player in the sports equipment retail sector, offering a unique blend of in-store expertise and a diverse product range.

Its commitment to returning capital to shareholders through consistently rising dividends, buybacks, and special dividends has significantly contributed to a high long-term total return.

However, while DKS has navigated challenging macroeconomic conditions well and maintains a positive outlook, its industry's cyclicality and elevated volatility warrant caution.

The stock's historical performance has shown periods of significant growth but also volatility.

As an investor, I appreciate DKS's resilience and strategic approach but remain watchful due to uncertainties in the current economic landscape, particularly regarding inflation.

For further details see:

DICK'S Is Impressive - But Is It Enough?