VSTO - DICK'S Sporting Goods: A Solid Q1 That Justifies Optimism

2023-05-24 03:33:32 ET

Summary

- DICK'S Sporting Goods reported Q1 2023 revenue of $2.84 billion, a 5.3% YoY increase, and earnings per share of $3.40, significantly higher than the $2.47 reported one year earlier.

- The company's stock appears cheap on an absolute basis and fairly valued compared to similar firms, with management remaining optimistic about the current fiscal year.

- Despite some margin compression issues, the company's strong top-line growth and positive outlook warrant a soft 'buy' rating.

If I were paid a dollar for every time I saw a scenario where the market threw the baby out with the bathwater, I would be a very wealthy man by now. During uncertain times, when pessimism permeates the market, companies that otherwise should experience a nice move higher end up seeing nothing but pain. A really good example of this can be seen by looking at sporting goods retailer DICK'S Sporting Goods ( DKS ). On May 23rd, shares of the business initially moved higher early in the trading day, driven by financial results that exceeded analysts' expectations . This was great to see in and of itself. But as general market pessimism pushed stocks down for the day, shares of this firm followed suit. If the stock was expensive, I could understand why this gyration might occur. But relative to similar firms, shares look more or less fairly valued, while being cheap on an absolute basis. Management continues to post attractive growth on both the top and bottom lines for the business. Given these factors, and in spite of the fact that the market has gone from bullish to bearish on the enterprise rather quickly, I do believe that the firm offers some attractive upside and warrants a 'buy' rating for now.

Impressive performance

With the way the economy is moving, I would make the argument that investors should be wary of retailers in general. The retail space is highly commoditized, suffers from intense competition, and has to deal with low margins because of these issues. However, the financial performance achieved by DICK'S Sporting Goods lately has been encouraging enough to warrant optimism. Consider how the business performed during the first quarter of its 2023 fiscal year.

{kind=link}

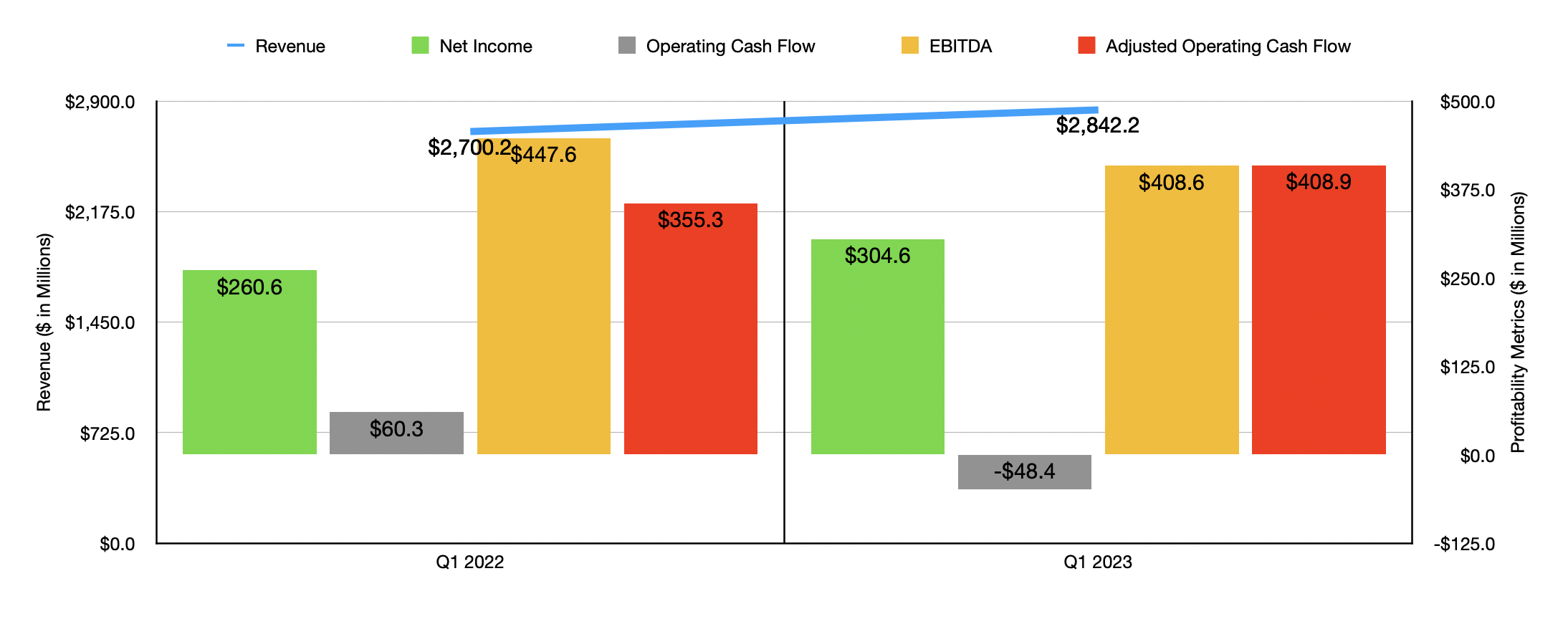

According to management, revenue during this time came in at $2.84 billion. That's 5.3% higher than the $2.70 billion the company reported one year earlier. This sales figure also came in $40 million higher than what analysts thought it would be. Part of this increase undoubtedly came from a rise in the number of stores the business has in operation. At the end of the first quarter of 2022, the retailer had 858 locations open. By the end of the first quarter of this year, that number had inched higher to 863. An even bigger driver of this increase, however, was the 3.4% rise in comparable store sales that management reported. This compares to the 8.4% decline in comparable store sales that the business reported for the first quarter of 2022 compared to the same time one year prior to that. The biggest contributor to the comparable store sales increase for the company was a 2.7% rise in the number of transactions at its locations. But the company did also benefit from an increase associated with the average ticket. This is essentially the average transaction size. So what this indicates is that, not only are more people buying more things from its locations, they are also paying more in the process.

On the bottom line, the picture for the company was also quite positive. Earnings per share came in at $3.40. That was significantly higher than the $2.47 reported one year earlier. Both earnings per share and adjusted earnings per share were $0.19 above what analysts thought they would be. This increase came even as certain core costs for the business worsened. The firm's gross profit margin, for instance, dropped from 36.47% to 36.19%. The bigger pain for the company came from an increase in its selling, general, and administrative costs from 22.79% of sales to 24.41%. This increase, on its own, translated to $46 million of missed potential on its bottom line on a pre-tax basis. It is possible that perhaps some of the shift in optimism tip pessimism that shares experienced came from the fact that these core costs did worsen year over year.

In fact, the only reason why the company saw profits increased from $260.6 million in the first quarter of 2022 to $304.6 million the same time this year, was because of a $47.7 million reduction in income tax expense and a $26.7 million improvement in other income and expenses. Changes when it comes to these items are much more likely to be temporary rather than indicators of long-term health. There were, of course, other profitability metrics that we should pay attention to here. Operating cash flow for the company actually worsened, dropping from $60.3 million to negative $48.4 million. But if we adjust for changes in working capital, we would have seen this metric climb from $355.3 million to $408.9 million. Unfortunately, one area where the company did experience some pain was when it came to EBITDA. This metric ultimately fell from $447.6 million to $408.6 million.

{kind=link}

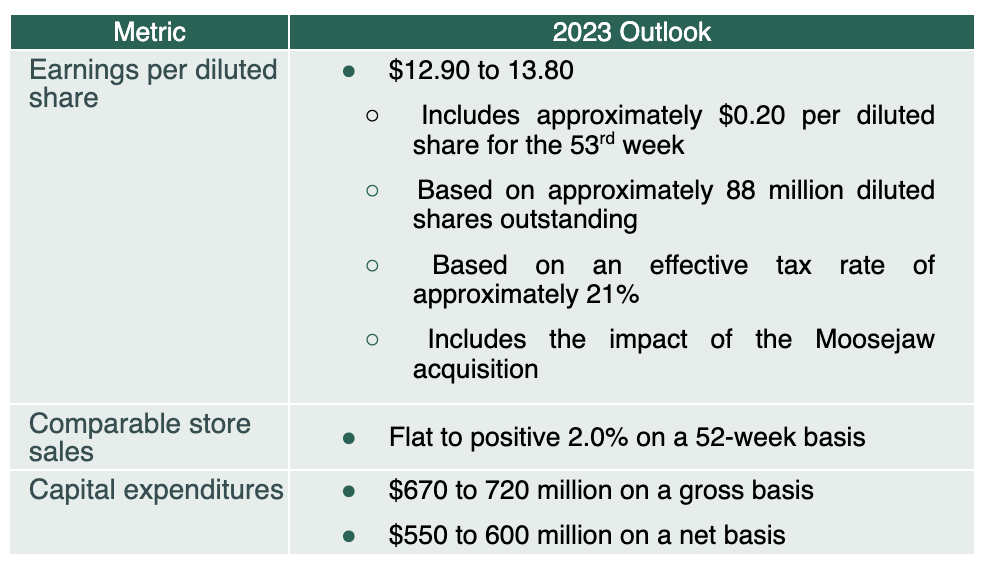

When it comes to the 2023 fiscal year in its entirety, management does have some positive expectations. Management did not provide guidance when it came to overall revenue. But they did say that comparable store sales should be somewhere between flat and up 2% year over year. Earnings per share, meanwhile, should be between $12.90 and $13.80. $0.20 per share of this is slated to be attributable to the fact that the company has an extra operating week this year. If we strip this out from the equation and use midpoint guidance provided by management, overall net income for the company should be around $1.16 billion for the year. This would represent a decent improvement over the $1.04 billion the company reported for 2022.

{kind=link}

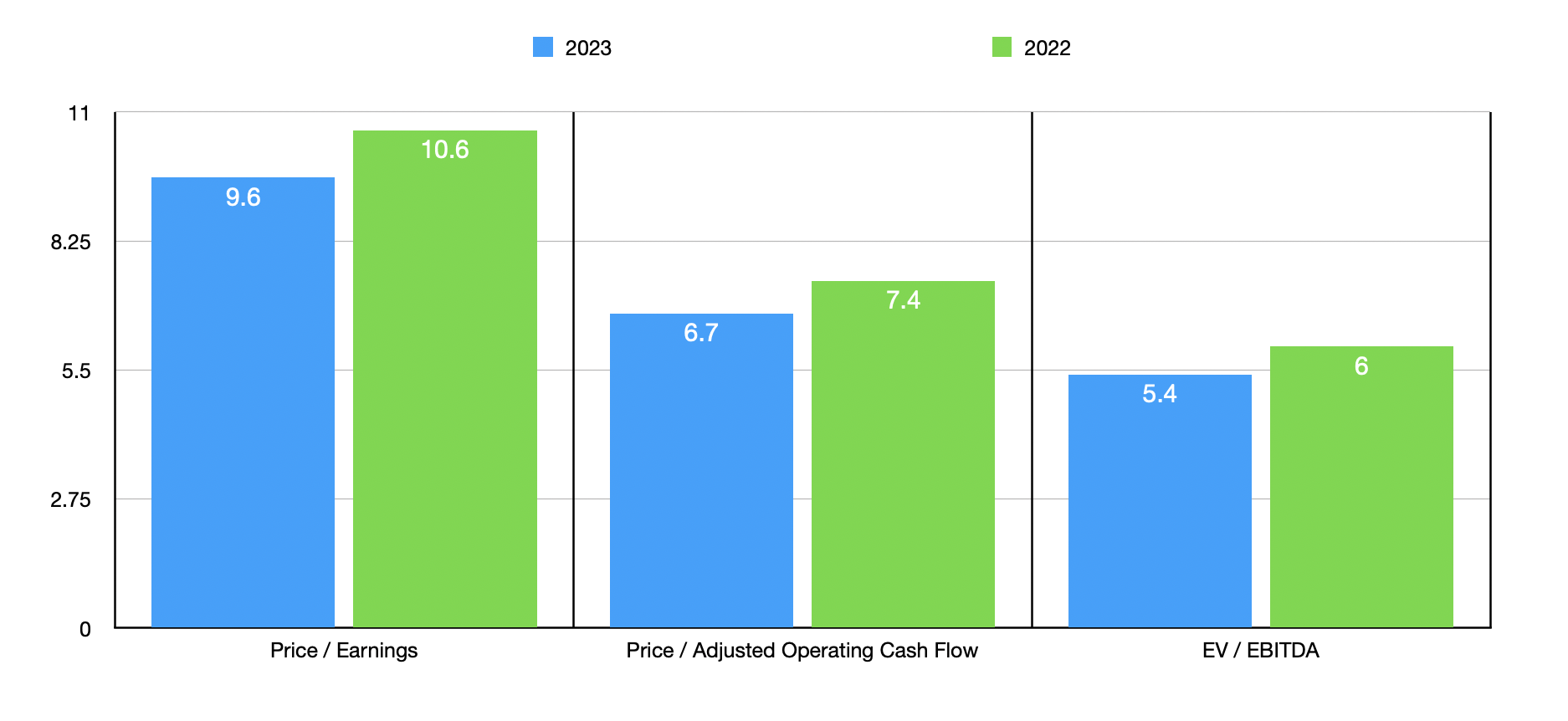

Management has not provided guidance when it comes to other profitability metrics. But if we assume that they will increase at the same rate that adjusted earnings are forecasted to, then we would expect adjusted operating cash flow, without the extra operating week, of $1.67 billion. Meanwhile, this would translate to EBITDA of around $2.03 billion. Taking these numbers, we can easily value the company. On a forward basis, as shown in the chart above, the business is trading at a price to earnings multiple of 9.6. The forward price to adjusted operating cash flow multiple is 6.7, while the forward EV to EBITDA multiple should be 5.4. The chart also shows how these all represent a nice improvement over what the company would be priced at using data from 2022. As part of my analysis, I also decided to compare the firm to five similar companies. As you can see in the table below, shares of DICK'S Sporting Goods are cheaper than three of its five competitors on both a price to earnings basis and on an EV to EBITDA basis. Meanwhile, using the price to operating cash flow approach, only one of the five companies was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| DICK'S Sporting Goods |

| 9.6 |

| 6.7 |

| 5.4 |

| Academy Sports and Outdoors ( ASO ) |

| 7.0 |

| 8.0 |

| 4.5 |

| Big 5 Sporting Goods ( BGFV ) |

| 9.9 |

| 22.8 |

| 3.4 |

| Hibbett ( HIBB ) |

| 4.8 |

| 8.0 |

| 2.8 |

| Vista Outdoor ( VSTO ) |

| 3.9 |

| 3.3 |

| 12.7 |

| Johnson Outdoors ( JOUT ) |

| 14.1 |

| 25.5 |

| 6.9 |

Takeaway

Operationally speaking, DICK'S Sporting Goods is doing quite well for itself. I do understand that, when you dig a bit deeper, you see some unfortunate margin compression where it actually matters. The company was essentially bailed out by some transitory factors. Some of the pessimism that developed regarding the business later in the day almost certainly came from the market digesting these facts. But on the positive side, you have a company that looks cheap on an absolute basis and fairly valued compared to similar firms, that happens to be growing its top line at a nice clip. Management remains optimistic about the current fiscal year, which is also a big bonus. All combined, I wouldn't say that the company makes for a grand slam or a home run. But it is attractive enough to warrant a soft 'buy' rating from here.

For further details see:

DICK'S Sporting Goods: A Solid Q1 That Justifies Optimism