DKS - DICK'S Sporting Goods: Back-To-School Results Impress In Q3 Shares Remain Attractive

2023-11-21 10:06:01 ET

Summary

- Investors cheered Q3 results reported by DICK’S Sporting Goods on Tuesday.

- Shares climbed about 8% in the pre-market trading hours on a comfortable beat on both the top and bottom lines, as well as a raised full-year outlook.

- A strong back-to-school season powered sales to a quarterly record in Q3. DKS also continued to gain market share during the reportable period.

- While shares have been on a run in recent periods, I believe the stock could rise even further in the months ahead.

DICK’S Sporting Goods ( DKS ) was already up nearly 6% since my last update following its Q2 earnings release, which badly disappointed investors. At the time, I noted that the selloff was overdone and that it presented investors with an attractive entry point to an industry leader with favorable demand drivers. The share price appreciation since then has been nearly double that of the broader markets over the same period.

Investors provided shares in DKS a further boost following Q3 results that showed off record quarterly sales and a topper on both the top and bottom lines. Propelling results was a combination of a stronger-than-expected back-to-school season and continued market share gains. And the quarterly momentum ultimately enabled a raise in the full-year outlook.

The positive outlook sent shares higher by about 8% in the pre-market trading hours on Tuesday. In my view, I can see the stock returning to the upper-end of its 52-week range in the periods ahead supported in part by the continued consumer preference for DKS in meeting their team- and gear-based spending needs.

DKS Stock Key Metrics

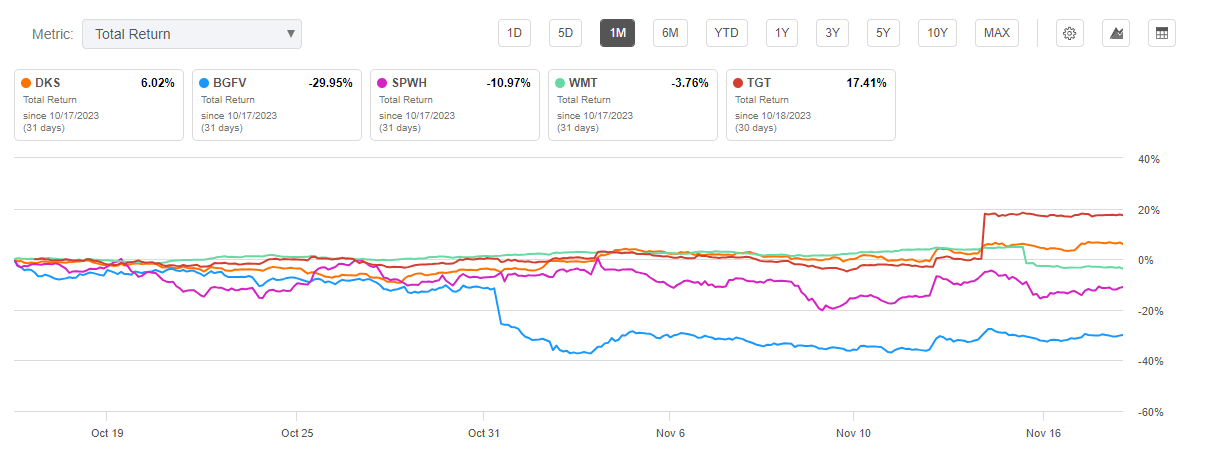

Shares in DKS have had a strong month, up about 6.5%. This is in-line with the broader S&P ( SPY ) but compares favorably to others within the retail space. Its smaller peers, Big 5 Sporting Goods ( BGFV ) and Sportsman’s Warehouse ( SPWH ) are each down double-digits over the same time span.

Walmart ( WMT ) is also sitting on losses due primarily to its post-release earnings selloff , while Target ( TGT ) moved in the other direction due to investor enthusiasm over its positive results.

{kind=link}

Seeking Alpha - 1M Total Returns Of DKS Compared To Peers

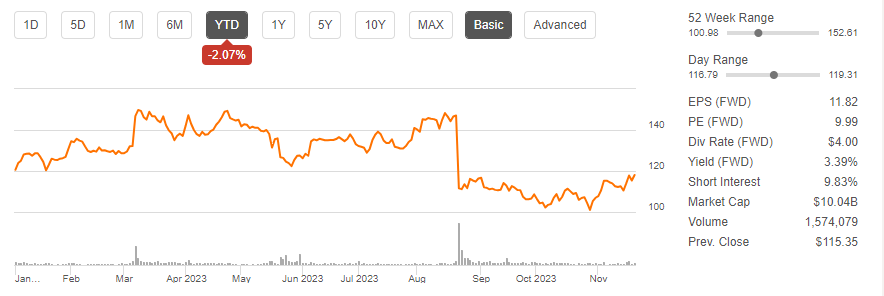

Despite the recovery over the past month, shares are still in the negative on a YTD basis. This is due mostly to the share price pressure faced following the release of its Q2 results.

{kind=link}

Seeking Alpha - YTD Returns Of DKS

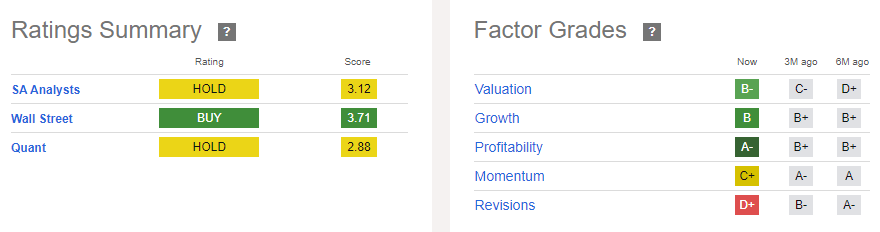

DKS trades at a reasonable forward multiple below historical averages. While this stacks favorably in Seeking Alpha’s quant system, negative momentum in the share price, as well as negative revisions in the earnings estimate offset the discount in valuation, resulting in a net rating of “hold.” Wall Street is more bullish, with a “buy” rating and an assessed estimated fair value of $130/share, which is a mark shares have just reached in the pre-market trading hours on Tuesday.

{kind=link}

Seeking Alpha - DKS Ratings Summary

What Did DKS Expect Heading Into Q3?

DKS disappointed investors in Q2 with weak results and downward revisions in its full-year guidance. On the day of the release, shares fell about 25%. The losses then continued the next day following multiple downgrades from Wall Street.

While DKS kept its full-year comparable sales expectations intact at flat to 2% growth, it reduced its EPS guidance to a midpoint of $11.73/share, down significantly from the prior midpoint of $13.35/share. Margin weakness was the primary driver for the decline.

Instead of EBT margins of 11.6%, as originally expected, DKS guided for a margin rate of 10.2%. The notable haircut was due mostly to expectations of higher shrink, which was expected to reduce full-year gross margins by 50 basis points (“bps”).

In addition, increased investments in their growth strategy was expected to drive SG&A higher, resulting in a 200bps YOY headwind. The comparable, however, to last year was expected to moderate towards the back half of the fiscal year.

On a similar note, despite the moderating expectations for its margin rate, DKS was expecting meaningful improvements later in Q4 due to the lapping of the effects of clearance activity incurred last year, as well as through the added benefits of a more favorable freight environment.

DKS Q3 Earnings Recap

A strong back-to-school season and continued market share gains powered quarterly sales to a record +$3.04B, up just under 3% YOY and comfortably ahead of consensus estimates of +$2.94B in sales. On a comparable basis, sales were up a surprising 1.7%.

This stands at the high-end of their expected full-year average. The positive growth is also notably in contrast to other discretionary retailers who have reported declines in the metric in recent results.

Issues related to shrink may have also subsided, as gross profit improved during the quarter, with a profit rate of 34.89%. Not only was this an uplift from Q2’s 34.42%, but it was also up from the 34.22% reported in the same period last year. This was due in part to the more favorable comparable environment, in which DKS lapped the clearance activity seen last year.

Elsewhere, non-GAAP EBT margins increased to 10.6%, up from 10.3% reported last year and a 50 basis point sequential increase from last quarter. The increase was well-ahead of the full-year margin rate of 10.2% that the management team had guided for previously.

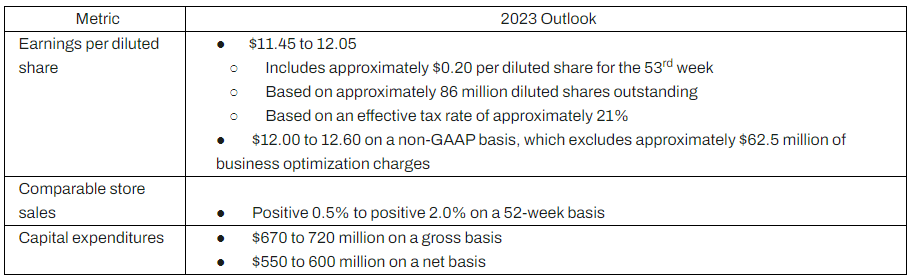

The successful back-to-school season provided CEO, Lauren Hobart, the confidence to announce a raise in the company’s full-year outlook. EPS is now seen at a midpoint of $11.75/share. While this is still well-below the prior midpoint set forth at the beginning of the year, the more optimistic view is a positive for investors heading into the holiday season.

DKS also firmed up their outlook for comparable store sales growth, with a nudge higher to a 0.5% growth rate at the low end of the range, up from the flat growth seen previously.

{kind=link}

DKS Q3 Earnings Release - Summary Of Full-Year Guidance

Is DKS Stock A Buy, Sell, Or Hold?

In my view, the long-term prospects for DKS remain favorable. The omni-channel sports retailer continues to gain market share in an addressable market estimated at about +$140B according to company presentations .

The share gains have also come on categories including footwear and athletic apparel and gear. The latter could very well be viewed as essential spending, since the gear often needs to be recycled every season.

In the pre-market hours on Tuesday, investors were cheering quarterly results that comfortably beat expectations on both the top and bottom lines. The beat on earnings was especially notable given the issues related to retail theft seen earlier in the year.

A strong back-to-school season also propelled sales to a quarterly record. This then enabled the management team to raise full-year guidance. While the earnings estimate is still below what was guided at the beginning of the year, the raise nevertheless should provide optimism heading into the crucial holiday season.

Despite the earnings spike, shares still command an earnings multiple below their five-year historical average of about 13.80x. Consensus price targets do, however, peg the stock at around the $130/share level. And today’s run-up brings trading values near this target.

Investors may feel compelled to hold off on any new or further positioning in the stock. Or they may even choose to sell into the gains. In my view, DKS still presents investors with an attractive buying opportunity.

The strong back-to-school season validates the favorable demand drivers underlying DKS’ business, and results continue to indicate that consumers view the product offerings as essential spending, as evidenced by the positive comparable sales growth, a refreshing contrast to the declines seen at other retailers who have reported thus far. I can see the positive momentum returning shares to the upper-end of its 52-week range or to about $150/share. This would suggest about 15% upside from the $130 mark and would imply a forward multiple of 12.8x. Following a strong Q3, I continue to view shares as a “buy.”

For further details see:

DICK'S Sporting Goods: Back-To-School Results Impress In Q3, Shares Remain Attractive