DKS - DICK'S Sporting Goods Is Unbelievably Cheap

2023-08-29 09:32:01 ET

Summary

- DICK'S Sporting Goods is a full-line sporting goods retailer with a strong e-commerce business and a focus on building brand loyalty.

- The company is facing pressure from shrink and organized retail theft, but its valuation is heavily depressed.

- DICK'S Sporting Goods has a strong net cash position, generates significant free cash flow, and has a solid and growing dividend.

- We value shares of DICK'S Sporting Goods at $160 each, offering material upside potential to patient long-term investors.

By Valuentum Analysts

We last wrote on Seeking Alpha about DICK'S Sporting Goods (DKS) back in November of last year in this article . We thought shares offered a bargain back then, and we think DICK'S Sporting Goods' valuation remains heavily depressed today. The biggest change from November 2022 has been the greater prominence that shrink has had on its business. In this article, we want to provide a refresh of our take on the company as well as explain our updated valuation of the name.

The biggest risk to our thesis on DICK'S Sporting Goods in the near term remains the impact of shrink on its profit levels, while the proliferation of competing e-commerce plays such as Amazon (AMZN) and other competitors in sporting goods remains the key long-term threat. From a valuation standpoint, we've accounted for the company's considerable operating leases as rent expense in earnings before interest. Adjusting for this debt-like commitment could have an impact on our valuation, though we don't view such an impact as material enough to change our bullish take.

DICK'S Sporting Goods is a full-line sporting goods retailer offering a broad assortment of brand name sporting goods equipment, apparel, and footwear. The company also owns and operates Golf Galaxy, a golf specialty retailer, and Field & Stream, a hunting and fishing specialty retailer. The firm was founded in 1948 and is headquartered in Pennsylvania. It has an industry-leading omnichannel platform that serves athletes through in-store and online (curbside and home delivery) shopping options. The retailer continues to work on building brand loyalty and a seamless shopping experience.

DICK'S Sporting Goods' e-commerce business has been a source of strength in recent fiscal years. In November 2021, the retailer announced a strategic partnership with Nike (NKE) that involves both physical and digital platforms. DICK'S Sporting Goods is rolling out new store concepts such as DICK'S House of Sport and Public Lands. Athletes go to its stores to buy some of the top brands including adidas (ADDYY), Callaway (MODG), Columbia (COLM), Nike, The North Face, Titleist, Under Armour (UA) (UAA) and YETI (YETI), among others. It also has a number of private label offerings not available elsewhere such as Second Skin, DSG, and Top-Flite.

Though DICK'S Sporting Goods is succeeding in both e-commerce and brick-and-mortar, the retail sporting goods market is a tough one. For example, big names such as The Sports Authority and Gander Mountain have filed for Chapter 11 bankruptcy protection over the years. More recently, DICK'S Sporting Goods is facing pressure from shrink, perpetuated in part by organized retail theft. This has become a huge problem in the retail industry stemming from the onset of the COVID-19 pandemic, where many consumers while cocooning at home spent time buying most of their needs and wants online. This offered organized retail thieves an avenue to dispose of their goods quickly, and often anonymously.

DICK'S Sporting Goods ended its second quarter of fiscal 2023 with a modest net cash position, while free cash flow surged during the first half of this fiscal year (~$450 million versus -$65.9 million). Though free cash flow suffered a bit last fiscal year, we're forecasting that the firm will haul in nearly $1 billion in free cash flow this year during fiscal 2023. With a market capitalization less than $10 billion, that amounts to roughly a 10% free cash flow yield. DICK'S Sporting Goods does have operating lease liabilities to be aware of and short interest is comparatively elevated on the name, but the stock looks unbelievable cheap at present levels, trading for less than 10 times forward estimated earnings per share at last check .

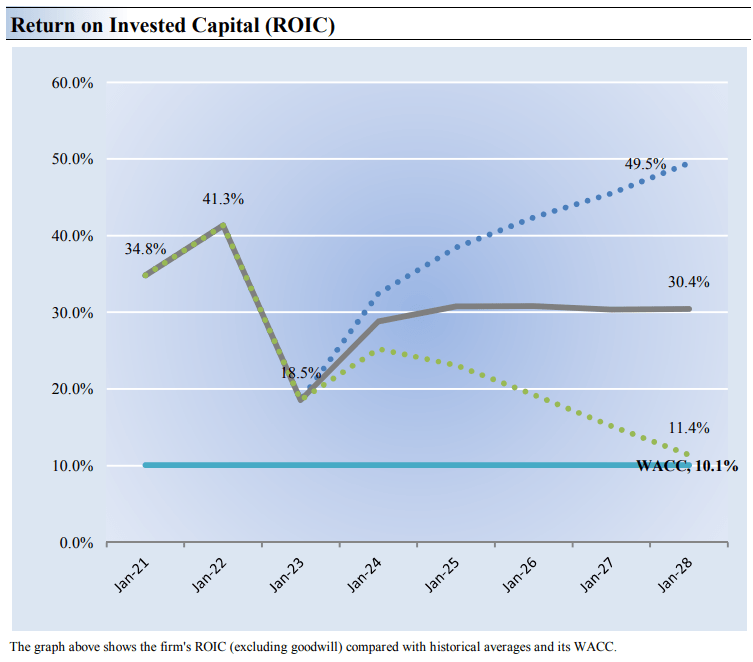

Our forecasts of DICK'S Sporting Goods' return on invested capital. (Valuentum)

{kind=link}

The best measure of a firm's ability to create value for shareholders is expressed by comparing its return on invested capital [ROIC] with its weighted average cost of capital ((WACC)). The gap or difference between ROIC and WACC is called the firm's economic profit spread. DICK'S Sporting's 3-year historical return on invested capital (without goodwill) is 31.6%, which is above the estimate of its cost of capital of 10.1%. As such, we assign the firm a ValueCreation rating of EXCELLENT. In the chart above, we show the probable path of ROIC in the years ahead based on our baseline forecasts and the estimated volatility of key drivers behind the measure. The solid grey line reflects the most likely outcome, in our opinion, and represents the scenario that results in our fair value estimate, which we'll discuss later in this note.

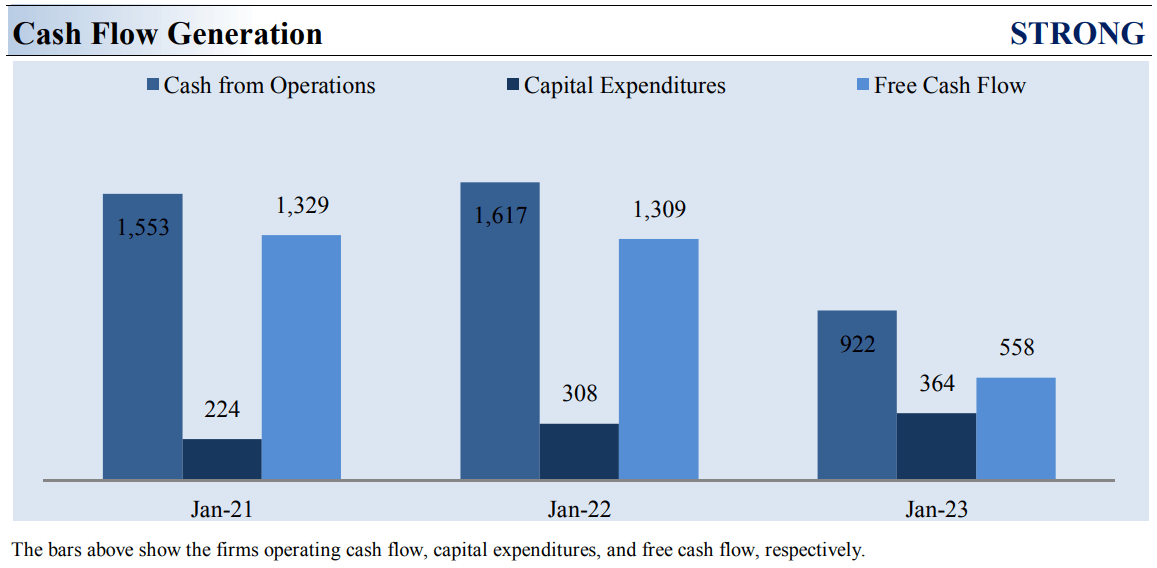

DICK'S Sporting Goods' historical free cash flow trends. (Valuentum)

{kind=link}

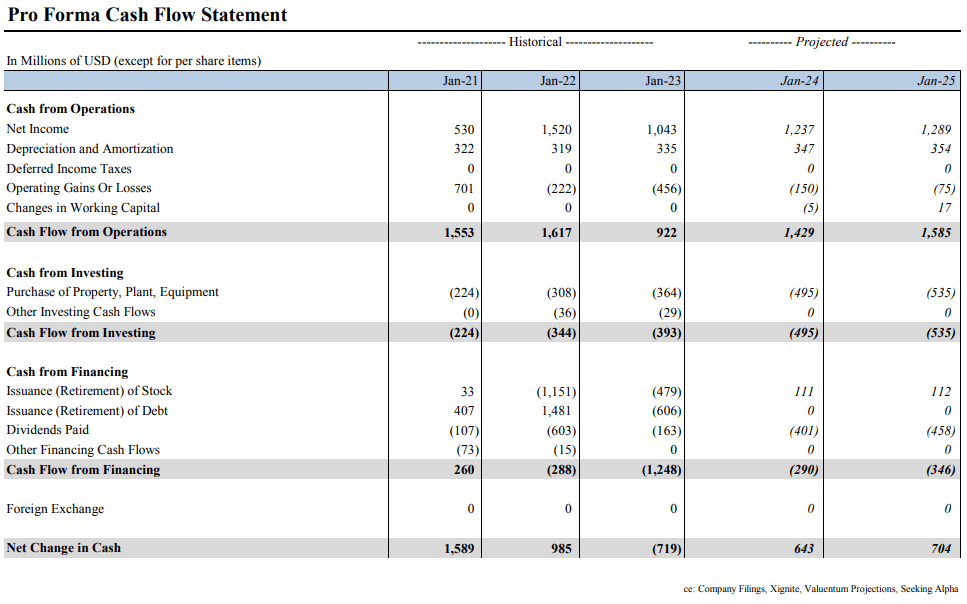

Firms that generate a free cash flow margin (free cash flow divided by total revenue) above 5% are usually considered cash cows. DICK'S Sporting's free cash flow margin has averaged about 9.7% during the past 3 years. As such, we think its cash flow generation is relatively STRONG. The free cash flow measure shown above is derived by taking cash flow from operations less capital expenditures and differs from enterprise free cash flow [FCFF], which we use in deriving our fair value estimate for the company. At DICK'S Sporting Goods, cash flow from operations has fallen from levels registered a couple years ago, while capital expenditures expanded over the same time period. We think free cash flow is on the mend, however, and we expect the firm to generate nearly $1 billion in free cash flow this year in fiscal 2023 (its pro forma cash flow statement is provided at the end of this article.

Our enterprise valuation summary of DICK'S Sporting Goods. (Valuentum)

{kind=link}

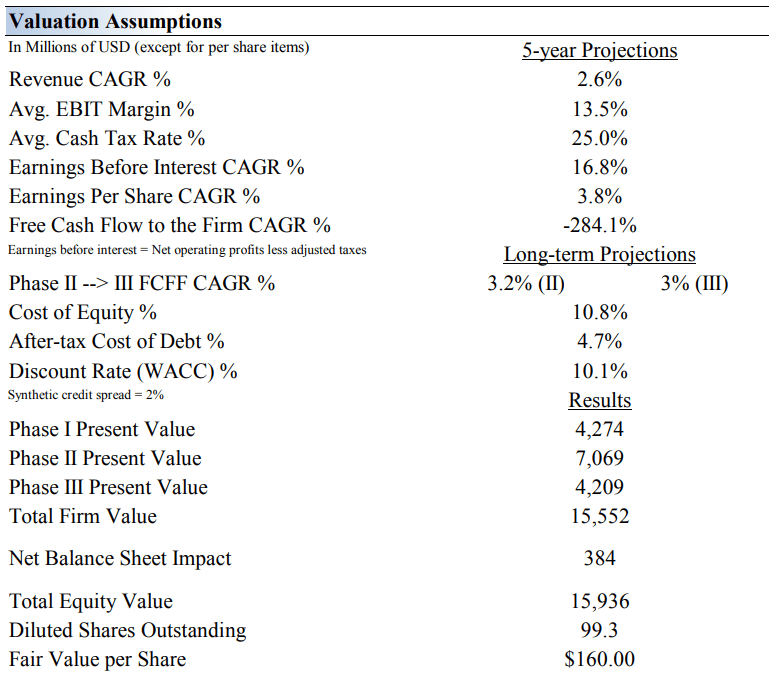

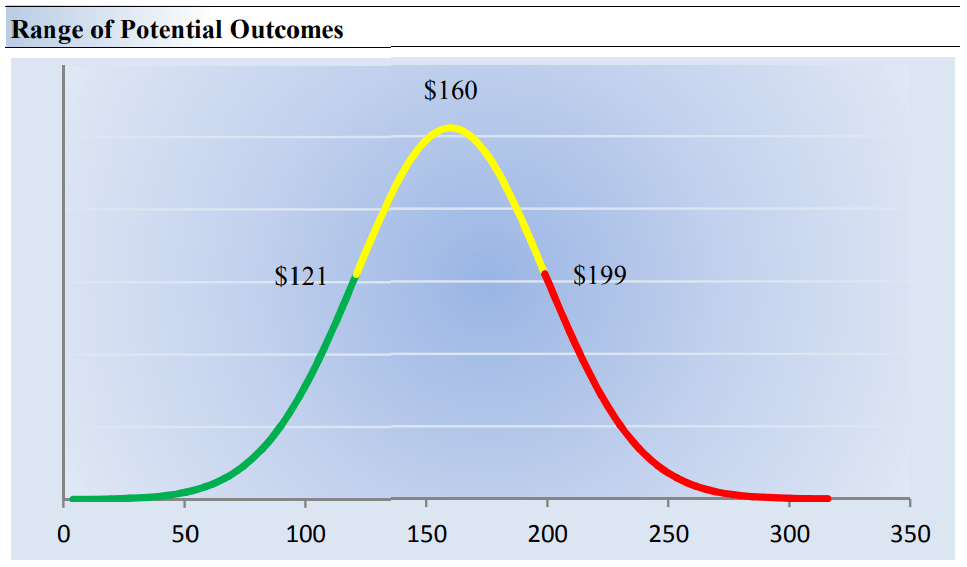

We think DICK'S Sporting is worth $160 per share with a rather large fair value estimate range of $121.00-$199.00. Note the updated fair value estimate is higher than our latest on Seeking Alpha, but represents a modest downward revision from our last update on our website. The margin of safety around our fair value estimate is driven by the firm's MEDIUM ValueRisk rating, which is derived from an evaluation of the historical volatility of key valuation drivers such as revenue and free cash flow and a future assessment of them. Our near-term operating forecasts, including revenue and earnings, do not differ much from consensus estimates or management guidance.

Our valuation model reflects a compound annual revenue growth rate of 2.6% during the next five years, a pace that is lower than the firm's 3-year historical compound annual growth rate of 12.2%. Our model reflects a 5-year projected average operating margin of 13.5%, which is above DICK'S Sporting Goods' trailing 3-year average. Beyond year 5, we assume free cash flow will grow at an annual rate of 3.2% for the next 15 years and 3% in perpetuity. For DICK'S Sporting Goods, we use a 10.1% weighted average cost of capital to discount future free cash flows, which is reasonable but could be considered rather high for a company with a net cash position.

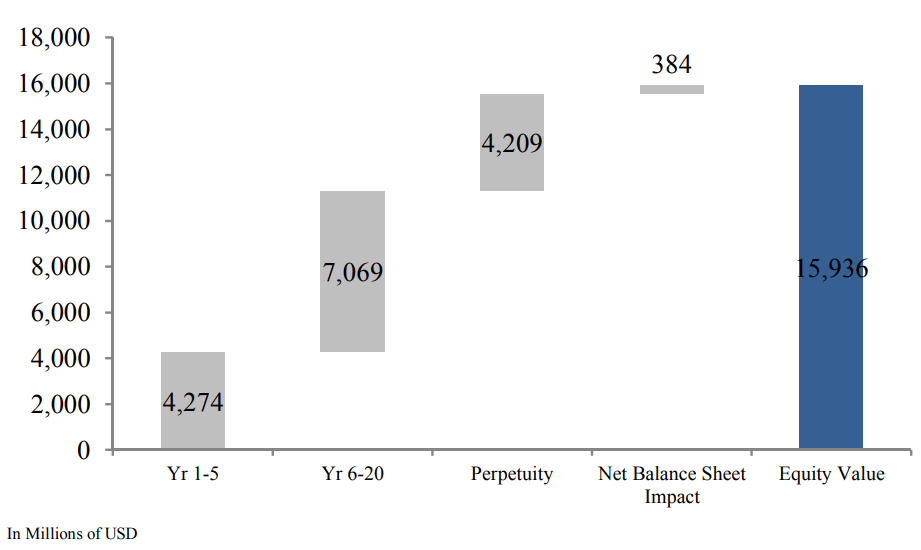

In the chart below, we show the build up to our estimate of total enterprise value for DICK'S Sporting Goods and the break down to the firm's total equity value, which we estimate to be about ~$16 billion. The present value of the enterprise free cash flows generated during each phase of our model and the net balance sheet impact is displayed. We divide total equity value by diluted shares outstanding to arrive at our $160 per share fair value estimate.

A breakdown of how we derive our estimate of DICK'S Sporting Goods' equity value. (Valuentum) Our fair value estimate range of DICK'S Sporting Goods. (Valuentum)

{kind=link}

{kind=link}

Our discounted cash flow process values each company on the basis of the present value of all future free cash flows. Although we estimate DICK'S Sporting Goods' fair value at about $160 per share, every company has a range of probable fair values that's created by the uncertainty of key valuation drivers such as future revenue or earnings, for example. After all, if the future were known with certainty, we wouldn't see much volatility in the markets as stocks would trade precisely at their known fair values.

Our ValueRisk rating sets the margin of safety or the fair value range we assign to each stock. In the graph above, we show this probable range of fair values for DICK'S Sporting. We think the firm is attractive below $121 per share (the green line), but quite expensive above $199 per share (the red line). Shares are trading at ~$112 each at the time of this writing. The prices that fall along the yellow line (above) represent a reasonable valuation for the firm, in our opinion. Shares look cheap to us.

How we think about the future trajectory of DICK'S Sporting Goods' intrinsic value. (Valuentum)

{kind=link}

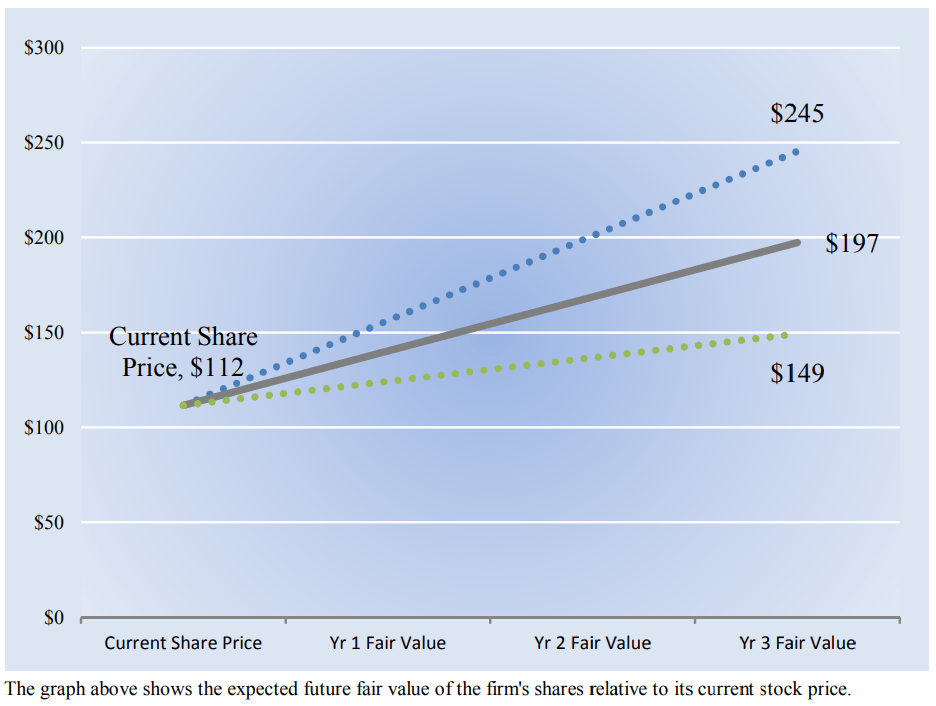

As noted previously, we estimate DICK'S Sporting Goods' fair value at this point in time to be about $160 per share. As time passes, however, companies generate cash flow and pay out cash to shareholders in the form of dividends. The chart above compares its current share price with the path of DICK'S Sporting Goods' expected equity value per share over the next three years, assuming our long-term projections prove accurate. To learn more about why the stock price faces headwinds with respect to dividend payments, please see this article .

The range between the resulting downside fair value and upside fair value in Year 3 represents our best estimate of the value of the firm's shares three years hence. This range of potential outcomes is also subject to change over time, should our views on the firm's future cash flow potential change. The expected fair value of $197 per share in Year 3 represents our existing fair value per share of $160 increased at an annual rate of the firm's cost of equity less its dividend yield. The upside and downside ranges are derived in the same way, but from the upper and lower bounds of our fair value estimate range.

Assessing the financial health of DICK'S Sporting Goods' dividend. (Valuentum)

{kind=link}

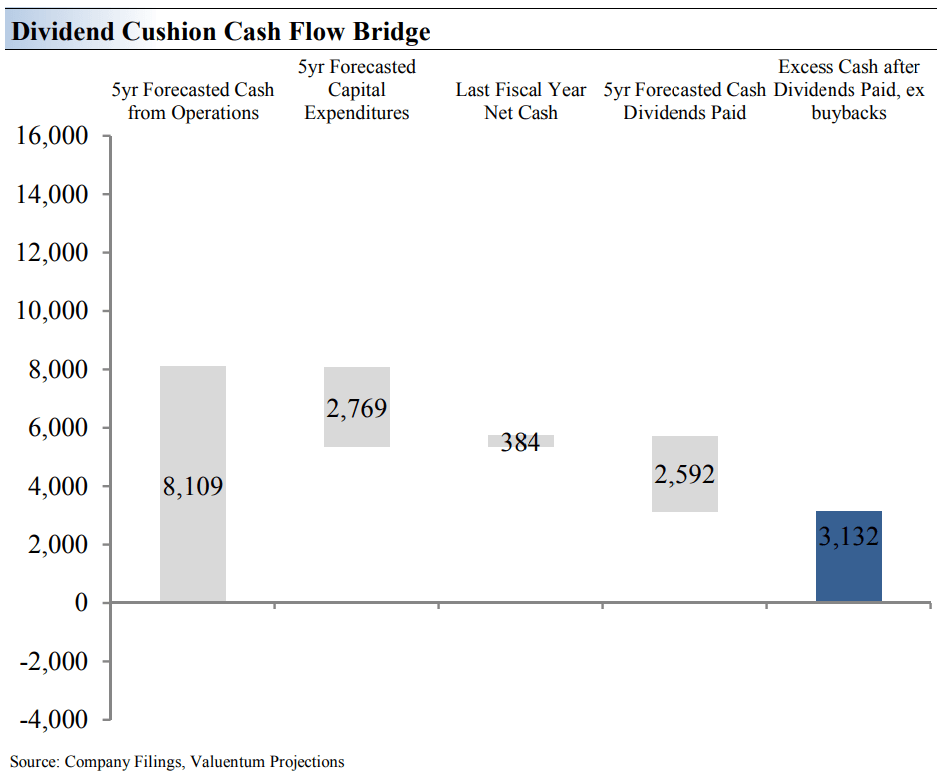

The Dividend Cushion Cash Flow Bridge, shown in the image above, illustrates the components of the Dividend Cushion ratio and highlights in detail the many drivers behind it. DICK'S Sporting Goods' Dividend Cushion Cash Flow Bridge reveals that the sum of the company's 5-year forecasted cumulative free cash flow generation, as measured by cash flow from operations less all capital spending, plus its net cash/debt position on the balance sheet, as of the last fiscal year, is greater than the sum of the next 5 years of expected cash dividends paid. Because the Dividend Cushion ratio is forward-looking and captures the trajectory of the company's free cash flow generation and dividend growth, it reveals whether there will be a cash surplus or a cash shortfall at the end of the 5-year period, taking into consideration the leverage on the balance sheet, a key source of risk.

On a fundamental basis, we believe companies that have a strong net cash position on the balance sheet and are generating a significant amount of free cash flow are better able to pay and grow their dividend over time. Firms that are buried under a mountain of debt and do not sufficiently cover their dividend with free cash flow are more at risk of a dividend cut or a suspension of growth, all else equal, in our opinion. Generally speaking, the greater the 'blue bar' to the right is in the positive in the image above, the more durable a company's dividend, and the greater the 'blue bar' to the right is in the negative, the less durable a company's dividend. As one can see in the image above, DICK'S Sporting Goods' dividend looks solid and poised for continued growth.

Wrapping Things Up

DICK'S Sporting Goods benefited greatly from the COVID-19 "boom" as e-commerce sales soared, but the company is now facing headwinds as operations normalize following the pandemic and organized retail theft remains problematic. Nonetheless, the firm is a tremendous generator of free cash flow and has a pristine balance sheet to boot, though we note that it does have operating lease liabilities to be aware of. We expect DICK'S Sporting Goods to continue to grow its dividend at a strong pace going forward on the basis of its robust forward-looking, balance-sheet focused, cash-flow based Dividend Cushion ratio. With an impressive free cash flow yield, a low price-to-earnings ratio, and a ~3.6% forward estimated dividend yield, DICK'S Sporting Goods looks unbelievable cheap and should be on your radar, in our view.

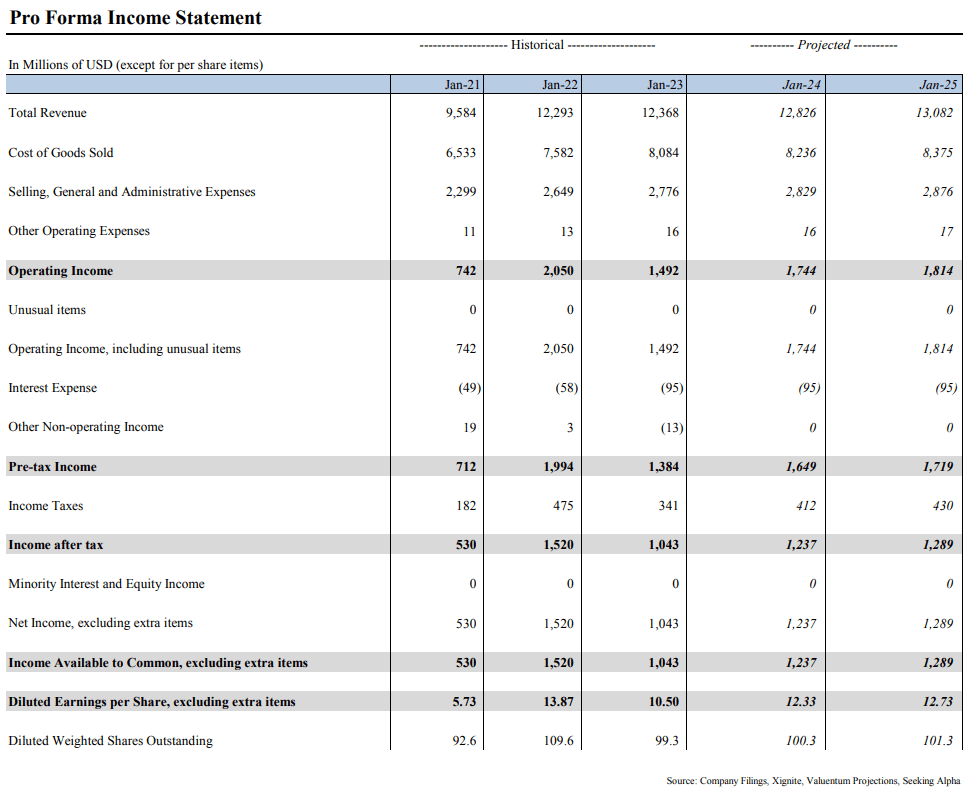

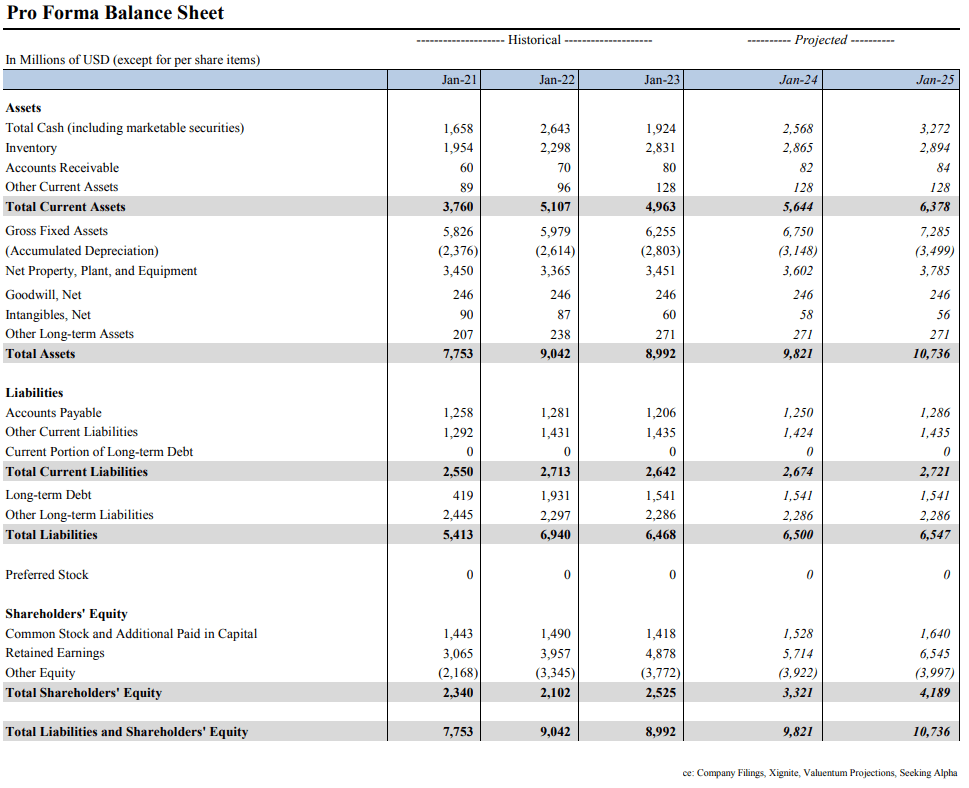

Pro Forma Income Statement (Valuentum) Pro Forma Balance Sheet (Valuentum) Pro Forma Cash Flow Statement (Valuentum)

{kind=link}

{kind=link}

{kind=link}

For further details see:

DICK'S Sporting Goods Is Unbelievably Cheap