DKS - DICK'S Sporting Goods: Long-Term Winner But Upside Limited

2023-05-06 22:04:06 ET

Summary

- DICK'S Sporting Goods is a sporting goods retailer in the United States.

- Revenue has grown at a CAGR of 8%, although this is expected to slow to 4% in the coming 3 years. We think there is scope for outperformance.

- EBITDA margin is 15%, with management believing this is sustainable. This is a market-leading level.

- Distributions have been sustainable and strong, driving shareholder value.

- DICK's valuation does not suggest enough upside, given the risks present.

Investment thesis

Our current investment thesis is:

- DICK'S is a commercially attractive retailer, having cornered the sports segment with a strong product offering and geographical reach.

- Digital integration, concept stores, and vertical brands are driving value.

- Margins have improved substantially, rocketing the business to a leading position. Although we are slightly skeptical, these look sustainable.

- We have assessed DICK'S valuation based on its historical trading range. It looks fairly valued / slightly undervalued but the risks around margin contraction and slowing growth make applying a buy rating premature.

Company description

DICK'S Sporting Goods ( DKS ) is a sporting goods retailer in the United States that offers a wide range of products such as sporting goods equipment, fitness equipment, golf equipment, hunting and fishing gear, apparel, footwear, and accessories.

Additionally, the company offers a youth sports mobile application called GameChanger, which enables video streaming, scorekeeping, scheduling, and communications.

Share price

DICK'S share price has performed well in the last decade, returning over 200% to shareholders. The looks to be a story of two halves. Initially, the share price trended down, as profitability declined despite growth. The pandemic looks to have revitalized the business, with profitability returning and growth becoming supercharged.

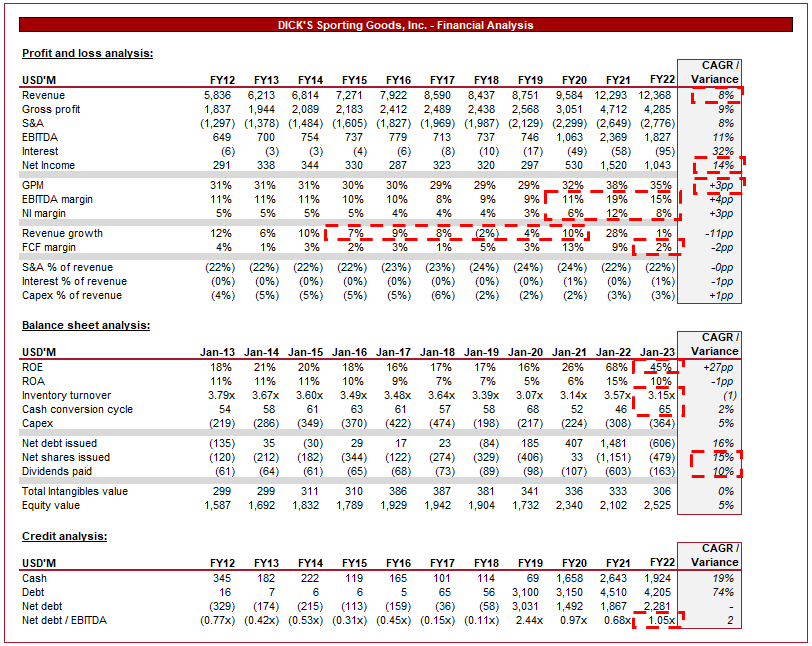

Financial analysis

{kind=link}

DICK'S financial performance (Tikr Terminal)

Presented above is DICK'S financial performance for the last decade. The company has fundamentally improved across the historical period but has shown areas of weakness, which make investors hesitant.

Revenue

DICK'S revenue has grown well in the last decade, with a growth rate of 8%. This is impacted somewhat by Covid, as FY21 was an outlier year. Despite this, growth has been strong outside of FY18.

One of the key growth drivers is the company's leading position in the US. DICK'S has over 850 stores, with a strong presence in key US States. This allows the business to cement itself as the leading sports goods provider through reach, competing with both brands and other retailers.

National footprint ( DICK'S )

DICK'S estimates that its market share in the US is 8%, which has increased by 1ppt since 2019. This is a reflection of consumers valuing the breadth of services DICK'S provides relative to alternatives.

Market share ( DICK'S )

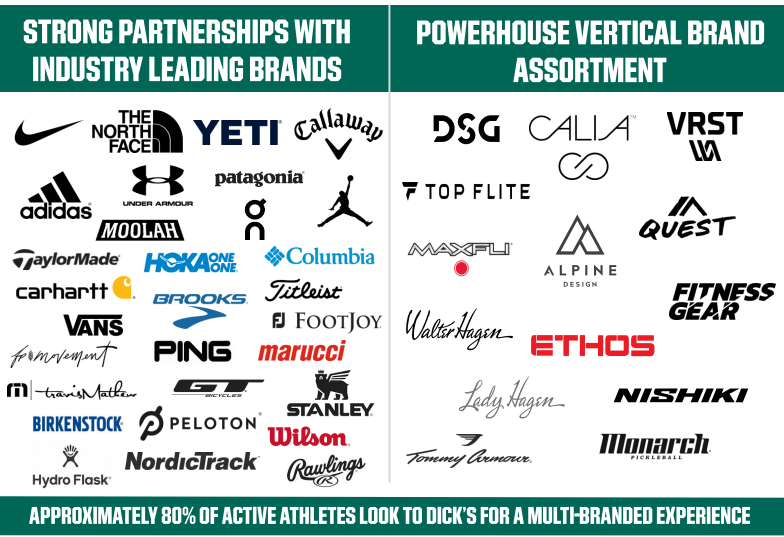

DICK'S currently boasts an impressive variety of brands, all of whom are leading in the sporting segment. This is highly attractive for consumers as the preference is a one-stop shop where different products can be compared. Further, consumers generally like to try products first and so in conjunction with its geographical reach, DICK'S is the best option for consumers looking to shop for sporting goods.

{kind=link}

Brands ( DICK'S )

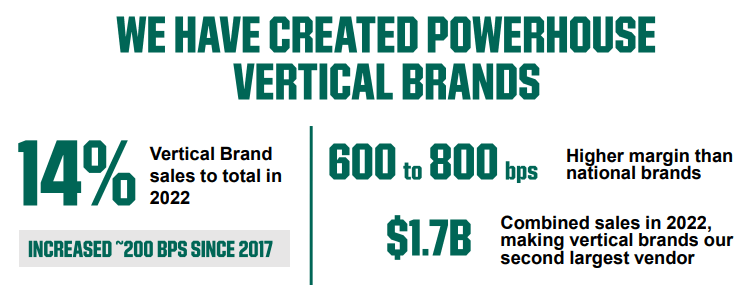

From a financial perspective, DICK'S has been focusing on developing vertical brands and leveraging customer trust. This has been beneficial as this segment comes with improved margins, allowing the business to generate accretive revenue through a change in brand mix.

{kind=link}

Vertical brand benefits ( DICK'S )

The company's current product mix is weighted toward softlines and footwear, which comprise 58% of revenue. This weights the business toward apparel, which makes sense as many individuals will participate in activities that do not need equipment.

Sales breakdown ( DICK'S )

DICK'S has invested in growing its direct exposure to sports, allowing it to connect directly to athletes. An example of this is its specialty concept stores such as Sporting Goods, Golf Galaxy, Field & Stream, Public Lands, and others. This looks to be a shrewd decision, as the company is gaining direct exposure to its core market and encouraging new individuals to take an interest in sports. This is essentially an on-the-ground marketing exercise.

Further, its investment in the GameChanger service has also rapidly grown its user base, with engagement in the millions. This has the potential to contribute a material amount to revenue but the key for us is again engagement, which markets the products that DICK'S sells.

GameChanger ( DICK'S )

As more people prioritize comfort and versatility in their clothing choices, there has been a rise in demand for athleisure wear. This trend has been particularly pronounced during the COVID-19 pandemic as more people work from home and so have a greater ability to engage in activities. DICK'S launched an athleisure brand in 2021 , with the view to competing with leading players such as Lululemon ( LULU ).

The rise of e-commerce has transformed the retail industry, and sporting goods are no exception. Consumers are increasingly shopping online, which has driven retailers to invest in their digital capabilities as a means of retaining and growing their customer base. DICK'S has made significant investments in its e-commerce platform, as it is threatened by lower-cost e-commerce sellers. The key advantage DICK'S has is the ability to utilize its locations to support e-commerce sales. For example, a consumer would need to purchase and try a product from an e-commerce-only brand once it's been delivered, whereas, with DICK'S, a consumer can purchase the product online but pick it up in-store. As the following illustrates, 50%+ of e-commerce sales are through mobile and 70% of e-commerce sales are fulfilled by stores, allowing for a cost-efficient distribution channel.

Omnichannel ( DICK'S )

DICK'S has also expanded its clearance offering, through the Going, Going, Gone!" brand. This is a great decision for two reasons. Firstly, many leading sports products are expensive, pricing out a large number of consumers. Secondly, we have seen an uptick in interest in clearance products, as consumers tighten up their finances.

Going, Going, Gone! ( DICK'S )

An underappreciated factor is employee satisfaction, which is industry-leading. This is highly important for two reasons. Firstly, in our to communicate expertise to potential customers, employees need to be enthusiastic and knowledgeable. Secondly, we have seen the labor market materially disrupted post-Covid, with some businesses closing stores due to a lack of employees.

{kind=link}

Employee satisfaction ( DICK'S )

Economic considerations

Current economic conditions are weakening, driven by persistent inflation which has remained stubborn in declining. This has caused serious issues for many individuals, with their cost of living rapidly rising. This is a threat to DICK'S near-term performance as consumers may defer or reduce discretionary spending to protect finances.

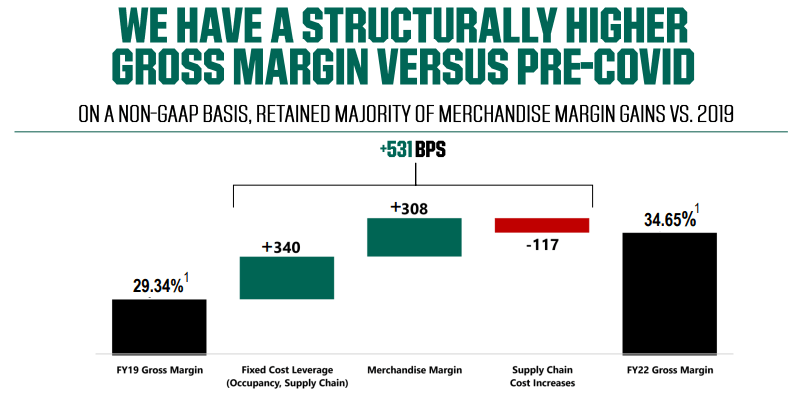

Margin

The company's margins were in decline between FY12 and FY19, with NIM falling to 3%. This is the primary reason for weak financial performance as DICK'S essentially traded growth for profits. Since then, things have rapidly improved, with the pandemic representing opportunities to improve both GPM and OPM.

The drivers of GPM improvement are:

- Differentiated products - DICK'S has increased the number of exclusive and differentiated products it is selling. These are generally higher-margin products with less susceptibility to downside risk.

- Vertical brands - As mentioned previously, DICK'S has increased the number of vertical brands sold, which have a margin superiority of 6-8%.

- Active pricing - Management has improved pricing activities through data analysis, allowing the business to personalize promotions and respond to changes in demand.

These factors are seemingly changes to the company's operations, rather than one-off gains, which suggest they are sustainable going forward. We are slightly skeptical, only because the gains have been quite incredible for a mature business in such a short amount of time. Within this will be a degree of aggressive Covid-19 pricing in response to demand.

{kind=link}

GPM bridge ( DICK'S )

S&A expenses have also declined as a % of revenue, driven by:

- Fixed costs - Scale benefits as the sales base increased relative to the fixed proportion of operating costs.

- Promotions - Improving promotional spending through targeted activities and further collaborations with athletes.

Our view is that the FY20-FY22 margins are very attractive for a retailer, both top and bottom line. The key question is whether DICK'S can maintain these going forward or whether we will see a reversion to its historical mean. We are skeptical due to the rapid nature of improvement but there are some structural improvements made.

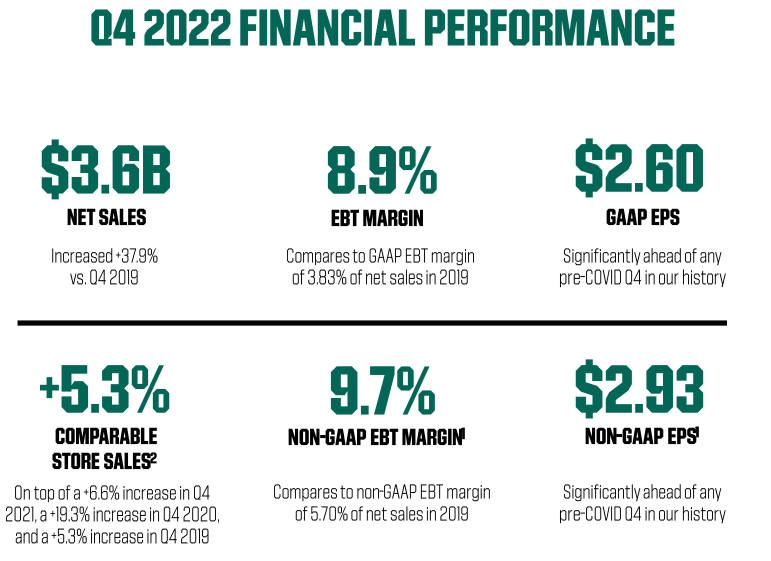

Q4 download

{kind=link}

Q4 performance ( DICK'S )

DICK'S most recent quarter shows impressive resilience to market conditions. The business is seeing healthy quarterly growth relative to prior periods, while margins are remaining sustainable. This suggests so far at least, business is as usual.

Balance sheet

The company's inventory turnover has declined marginally since Jan22, suggesting continued weakness in inventory management. This could be early signs of slowing demand but is more so an area for improvement which Management has identified. Providing a clearance option should help lift this figure but the impact so far is not seen. A retailer should target 4-5x in our view, although DICK'S will be lower than average due to the hardline products it sells. The benefit of improving its capital commitment to working capital is increased distributions.

DICK'S is very conservatively financed, with a ND/EBITDA ratio of 1x. This is far below the maximum the company can sustain, giving Management flexibility to operate aggressively if required. The business could expand its marketing activities further, conduct M&A, or increase distributions if they so require.

Speaking of distributions, Management has sustainably returned capital to investors through both dividends and buybacks, at an impressive growth rate. Our view is that current levels are sustainable, although growth may slow.

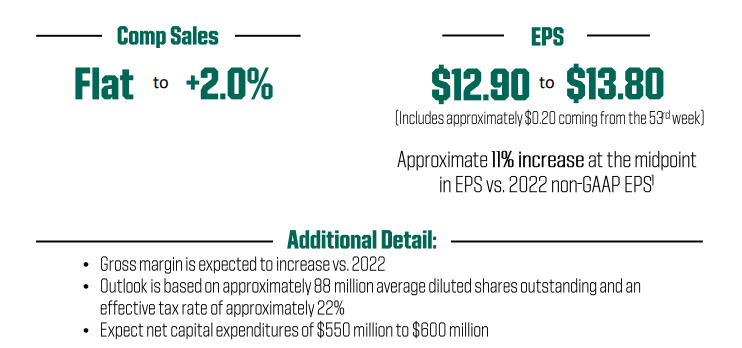

Outlook

{kind=link}

Management forecast ( DICK'S )

Management is forecasting flat-to-2% growth, which looks reasonable based on current market conditions. Although the business has shown resilience, it is conservative to assume demand will weaken.

Interestingly, further margin improvement is forecast, which could help cement margins at this elevated level to investors.

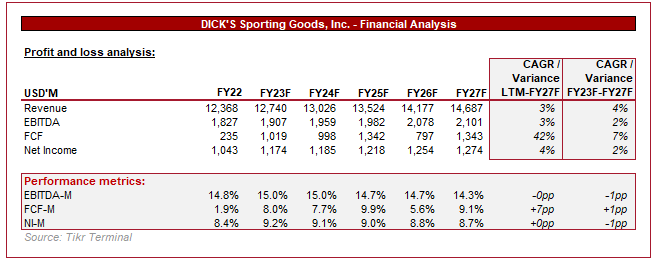

{kind=link}

Wall Street outlook (Tikr Terminal)

Presented above is Wall Street's consensus view on the coming 5 years.

FY23 forecasts are more bullish than Management on growth but less so on margins.

Healthy growth is forecast although to a level lower than achieved historically. Our view is that this is conservative as the company's commercial standing has shown its ability to achieve better growth.

Margins are expected to decline but not to any material degree, instilling further confidence that DICK'S will be able to maintain this heightened level.

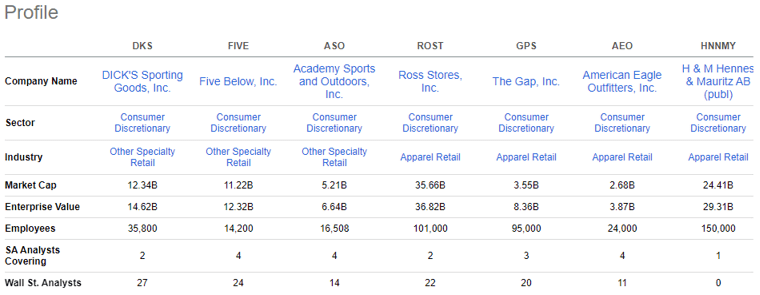

Peer analysis

{kind=link}

Comps (Seeking Alpha)

In order to assess DICK'S relative performance, we have compared the company to a cohort of apparel retailers. This is not a perfect comparison due to the softline/hardline split but serves as a high-level retailer comparison.

{kind=link}

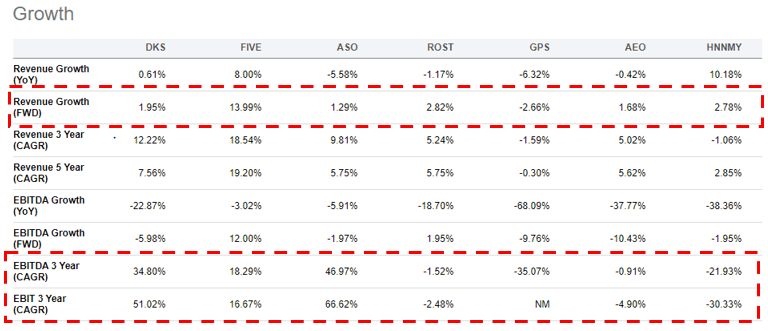

Growth (Seeking Alpha)

The company's forecast growth is slightly below the average, although when factoring in the 5Y CAGR, it looks far better. It is clear from this data that the outperformance in the last 3 years is not purely due to market conditions but an active improvement from Management.

{kind=link}

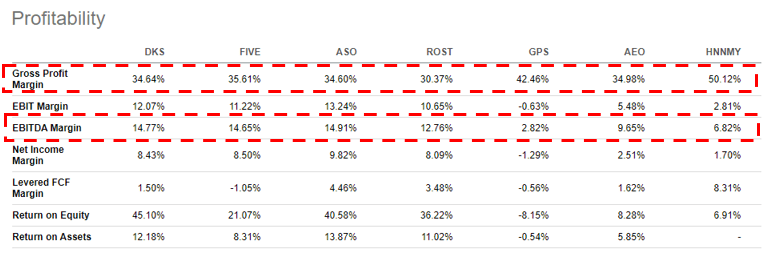

Profitability (Seeking Alpha)

DICK'S shines when comparing profitability, with its current levels in line with the leaders of the pack. Even with a slight dilution, DICK'S is clearly a strong performer.

Valuation

{kind=link}

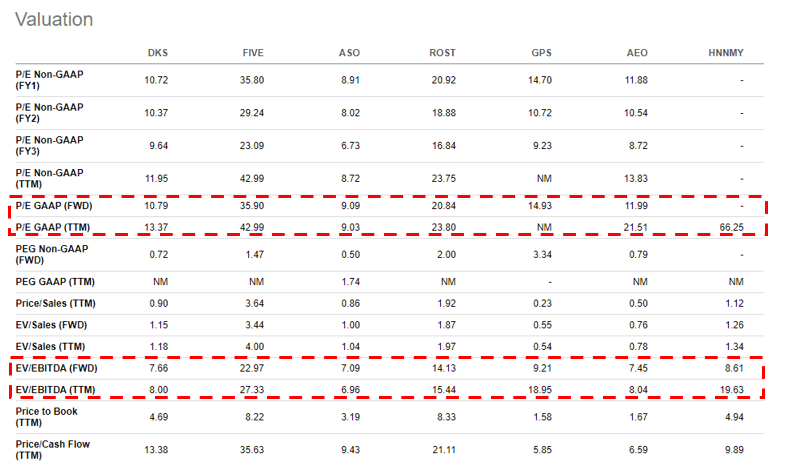

Valuation (Seeking Alpha)

DICK'S is trading at a noticeable discount to its peers, even with the exclusion of the rapidly growing Five Below ( FIVE ). Despite this, it is difficult to take a view due to the large variability in valuations. The most comparable company in terms of financial performance is Academy Sports ( ASO ), which is trading at a discount to DICK'S.

If we consider its historical trading multiple (2011-2023 - Source: Tikr Terminal ), DICK'S is trading at a premium to its historical NTM & LTM EV/EBITDA multiple. The company's current margins are superior to what was achieved historically, although this is offset somewhat by contraction risk and slower growth. Based on this, we would argue a slight premium is justified. This suggests DICK'S is trading around its fair value, which aligns with Wall Street's consensus upside of 6%.

Key risks with our thesis

The key risks with DICK'S are:

- Margin contraction in FY23, against Management guidance, driven by inflationary pressures.

- A decline in demand due to current market conditions.

Final thoughts

DICK'S is a fantastic specialty retailer which has achieved outsized growth through commercial superiority in its segment. Our view is that growth should continue as demand for sports products remains robust. The company does face near-term headwinds but evidence of this is yet to be seen. When compared to other retailers, the business does well but its valuation does not suggest upside based on its historical trading range.

For further details see:

DICK'S Sporting Goods: Long-Term Winner, But Upside Limited