DKS - DICK'S Sporting Goods: Outshining Their Peers And More Room To Run

2023-06-20 09:43:25 ET

Summary

- DICK'S Sporting Goods is reporting positive sales growth and is not seeing evident signs of consumer stress.

- Higher traffic levels and sales volumes support this view. The higher volume also appears to be at the expense of their smaller-sized peers.

- An expanding footprint that includes a more immersive retail format is likely to result in further share gains.

- Despite trading at the top-end of their 52-week range, I view shares as undervalued due to recent outperformance, the positive future outlook, and their current trading multiple, which remains below their five-year average.

DICK’S Sporting Goods ( DKS ) is showing investors that necessities aren’t just limited to lower priced consumables. Spending on team-based sports is proving to be just as essential to some consumers.

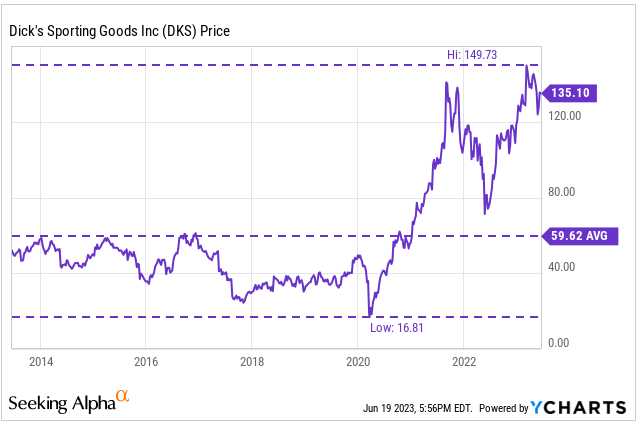

Shares in the stock are trading near their all-time highs. And over the past six months, YTD, and the past year, investors have realized gains of 20%, 12%, and 90%, respectively.

{kind=link}

YCharts - Recent Price History Of DKS

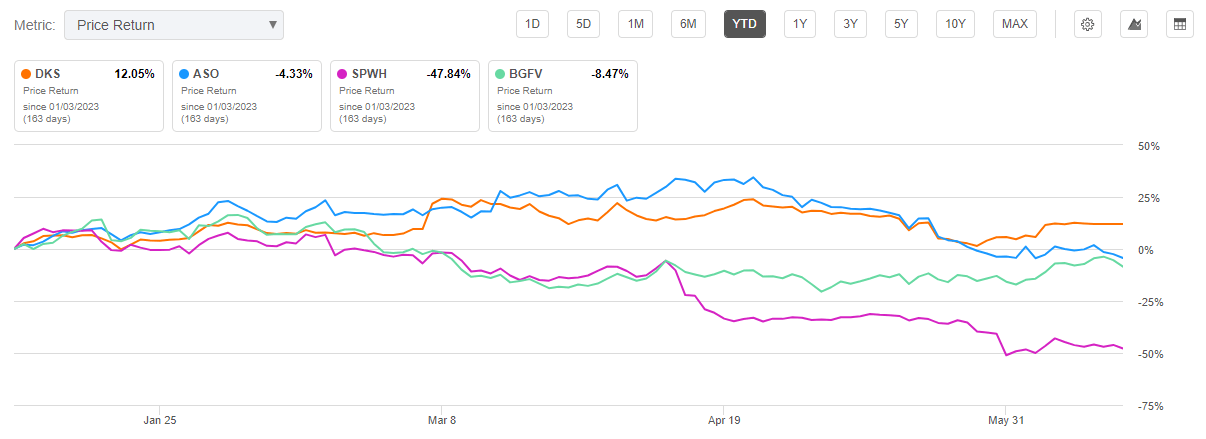

DKS appears to be an under-the-radar sleeper that continues bucking the trend of their counterparts, which are all trading in the negative on a YTD basis.

{kind=link}

Seeking Alpha - YTD Returns Of DKS Compared To Peers

Has DKS run its course? I’d argue that it has further to run.

Why Is DKS Stock Outperforming?

In Q1, DKS beat on both the top and bottom lines. Overall revenues were up 5.3%. In contrast, Academy Sports ( ASO ), Sportsman’s Warehouse ( SPWH ), and Big 5 Sporting Goods ( BGFV ) all reported losses over the same period.

One common headwind reported by DKS’ peers was poor weather. This was a non-factor for DKS due in part to their diversified footprint across the U.S. Their peers, on the other hand, have their operations concentrated in select regions or states.

BGFV, for example, has a major presence in California. ASO has a high concentration in Texas . And SPWH is top-heavy in the mountain states. If the weather is abnormal in any one of these regions, their operations will be set back. And that was exactly the case in Q1.

DKS also reported comparable sales growth of 3.4% on a 2.7% increase in transactions on higher traffic levels. In contrast, their peers all reported declining traffic in Q1. This is simply DKS taking away share from their competitors.

Will DKS Continue To Gain Market Share?

DKS is also tapping into their financial heft to expand their House of Sport stores, which is a more immersive type of retail experience. They also have plans on integrating this into their re-imagined next generation 50K SF space. These spaces are expected to appeal to the avid sports fan and would give further reason for consumers to shop at DKS over their counterparts.

Granted, it’s not going to come without a cost. For the full fiscal year, DKS is expecting to spend about +$550M at the midpoint in capital expenditures (“capex”). That’s about +$250M over what they spent last year. But they have the capacity for the increase. In FY22, for example, DKS generated over +$500M in free cash flow. It’s expected to be in-line or higher this year due to their positive sales growth.

In addition to the capex, DKS pays out a quarterly dividend and engages in share repurchases. Their cash position and earnings growth can support this. At period end, DKS had +$1.6B of cash and equivalents as well as +$1.6B available on their unsecured credit facility.

Will Expansion Negatively Impact Earnings?

One can point to the potential drag from increased administrative costs (“SG&A”). SPWH, for example, is bearing the brunt of the heightened costs associated with their own expansion plans . In Q1, SPWH’s SG&A as a percentage of sales increased to 37% compared to 31% last year. This was due primarily to the increased costs from additional store openings. Would DKS experience a similar hit?

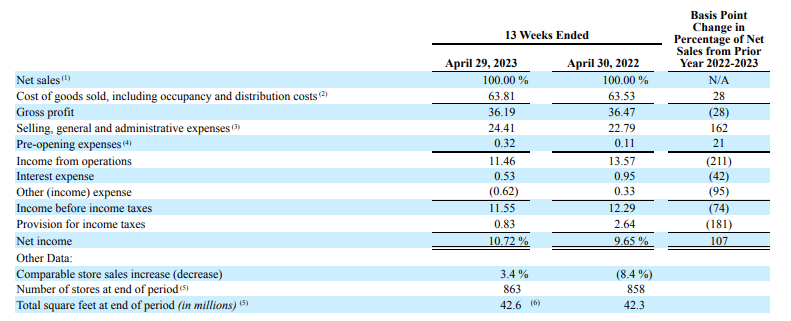

Their costs appear more controlled. As a percentage of DKS’ sales, SG&A runs at about 24%. That’s up 162 basis points (“bps”) from last year. But it’s not trickling significantly into overall operating margins, which were down just over 70bps during the period. This was due in part to savings realized from the freight environment.

{kind=link}

Q1FY23 Form 10-Q - Summary Of Operating Performance

And looking ahead , DKS expects margins to remain about the same for the year. This would be despite a ramp up in their long-term investments.

DKS also maintained their overall guidance for the full year. This sees diluted EPS coming in at $13.35/share at the midpoint, representing 9% YOY growth (based on a 52-week comparable basis). Comparable sales are seen flat to up 2%. The positive growth is notable, as their peers are seen in the negative.

Is DKS Stock A Buy, Sell, Or Hold?

Worries regarding the consumer could create some skepticism as to whether DKS can hit their full year targets. But I expect that they will. As seen in their Q1 results, they are taking away share from their smaller peers due to their more national presence and scale in cost control.

And for those that participate in team sports, the associated gear is considered essential spending. Equipment, such as bats, gloves, and masks, among others, often need to be replaced. This is the case with footwear, such as cleats, as well. Quarterly traffic growth at their stores versus declines elsewhere supports the view that demand will remain stable in the periods ahead.

The Commerce Department’s May retail report lends further credence to the demand environment. The report noted an increase of 0.3% on the month in the sporting goods and other hobby materials category. With the summer season just about here, the environment is expected to remain accommodative for continued spending.

The expected restart in student loan repayments could disproportionately affect DKS since their target customers tend to skew to the younger cohort. With shares trading at the top end of their 52-week range, some may find it best to hold off on new or further positioning until there is more clarity surrounding the impacts of the resumption in the student loan repayments.

While a better opportunity may in fact present itself, I still view shares as an attractive pick-up at current pricing. The stock trades at about 10x forward earnings. This is below their five-year average of 12x. It’s also not significantly out of line from the multiple commanded by their smaller peers. And these peers all reported weak quarterly results. Yet they trade at about the same level as DKS.

Consensus estimates on Wall Street peg shares with upside of about 15% from current trading levels. I see the upside potential closer to 20%. That would bring shares closer to their five-year average valuation. Given current strength and the positive forward outlook, I view this as attainable. A more pronounced divergence in performance compared to their peers further solidifies their leadership stake in the sector.

DKS has a strong batting average. Investors may very well find it worthwhile to take a flyer on the shares.

For further details see:

DICK'S Sporting Goods: Outshining Their Peers And More Room To Run