DKS - DICK'S Sporting Goods: Parsing Under The Earnings Report Sustained Our Thesis

2023-03-22 03:16:01 ET

Summary

- Latest earnings report has improvements in the right direction but the overall trend in weakening margins and cash flow are as we expected.

- The aggressive expansion plan in the current environment will incur large costs and expenses that further strain the company.

- Market priced in too much optimism that is unlikely to realize in the medium term.

Investment Thesis

Our previous thesis on DICK'S Sporting Goods ( DKS ) concluded the company has potential risks from weakening cash flow to support aggressive expansion and a historically high debt load. After the Q4 earnings report, we checked that the thesis is on track and Dick's risks have only grown. We continued to recommend a sell.

Holiday Season Review

Is this holiday season a bang on the right drum? Indeed, Dick's net sales have grown by 7.3%, and comparable store sales maintained a similar growth pace YoY at 5.3% compared to 6.6% same quarter last year. However, its net income has declined by 32%, and its earnings per diluted share have declined by 18% YoY.

Dick's Q4 Operating Results Excerpt (Company Earnings Release)

If comparing this Q4 operating cash flow against its own peers, all the Q4 operating cash flow every year since 2007, this past holiday season, is at a historical average. Indeed, it is much better than Q4 of 2007 or 2019, but that bar seems to be too low to warrant the stock price's jump to a historical high.

Dick's Historical Holiday Season Sales (Charted by Waterside Insight with data from company)

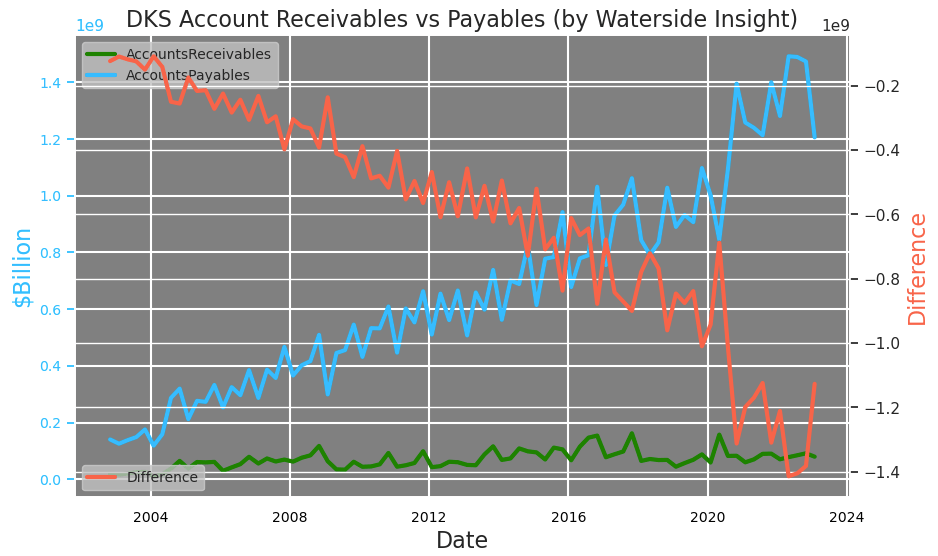

Revisiting one of the charts we previously posted that compared its accounts receivable and payables, we can see improvements have been made to reduce the account payables. But it is only bringing it back to the level in 2021, which is still a notch higher than before 2020. It is a step in the right direction. However, with accounts receivables staying at a similar level, the difference between them is still at one of its lowest levels historically.

{kind=link}

Dick's Accounts Receivables vs Payables (Calculated and Charted by Waterside Insight with data from company)

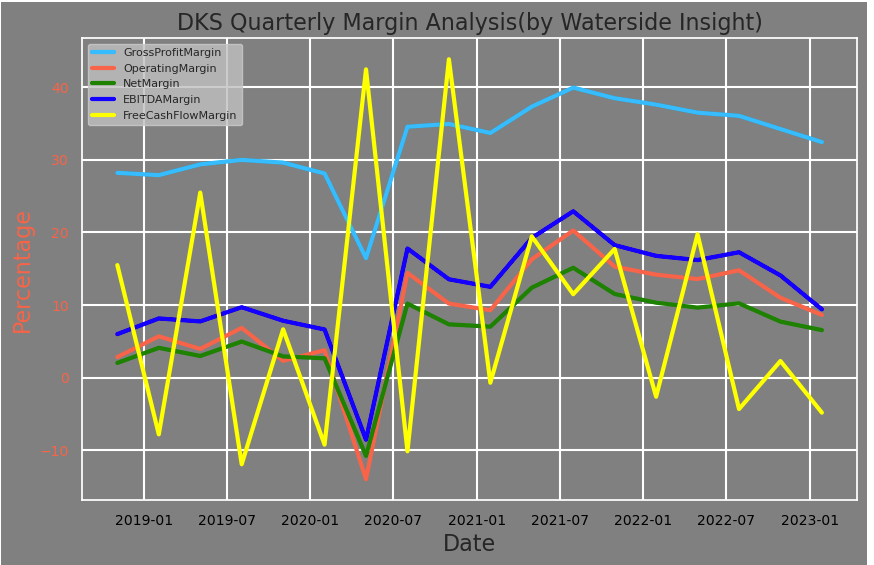

The quarterly margin analysis shows most of its important margins continued the downward trend, although its gross margin is still at its higher level. Its free cash flow margin has notably declined to one of its lowest levels. This was what we pointed out previously; its cash flow generation weakened.

{kind=link}

Dick's Margin Analysis (Calculated and Charted by Waterside Insight with data from company)

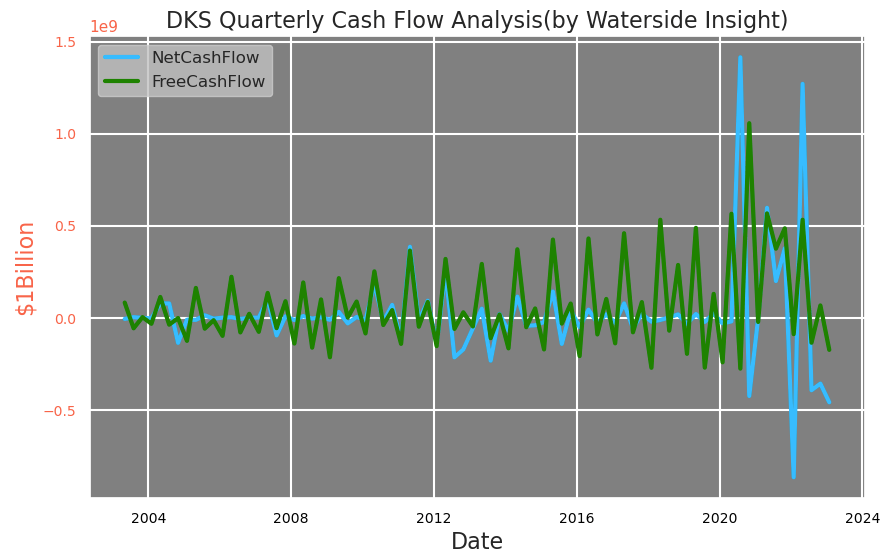

In particular, both its free cash flow and net cash flow have declined to negative in the latest quarter. The company has doubled its dividend payout to $4. This means it will further stretch its negative cash flow going forward.

{kind=link}

Dick's Cash Flow Analysis (Calculated and Charted by Waterside Insight with data from company)

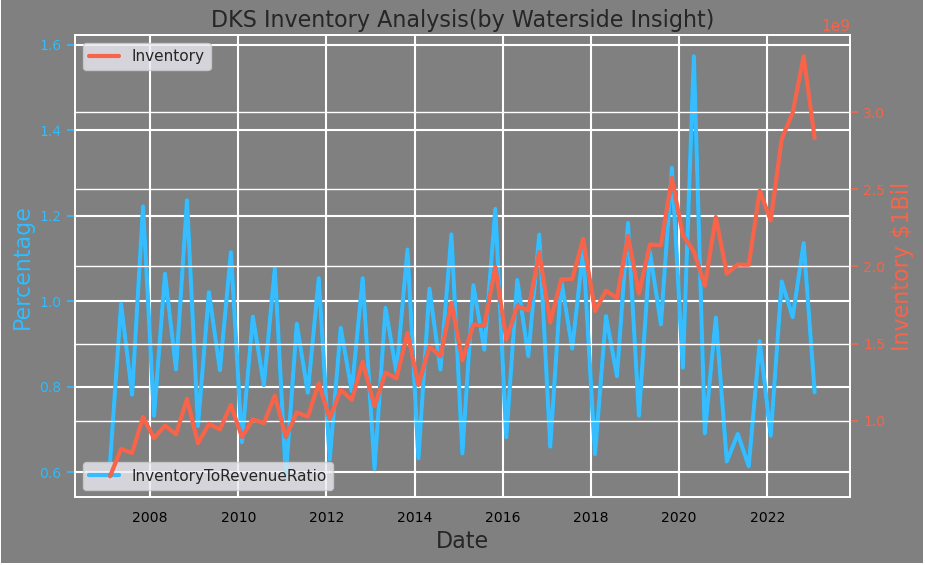

At the same time, the company's inventory for the quarter has grown by 23% YoY, and its total debt has decreased by 20% YoY, according to its earnings release.

Dick's Balance Sheet Excerpt (Company Earnings Release)

To put that in historical context, its inventory, although very high in its net value, is not as daunting when seen as a portion of the revenue. This ratio is only at its average level. And the latest quarter has reduced the inventory by 15% QoQ . So, we are not as concerned with that right now so long as its sales growth stays up.

{kind=link}

Dick's Inventory Analysis (Calculated and Charted by Waterside Insight with data from company)

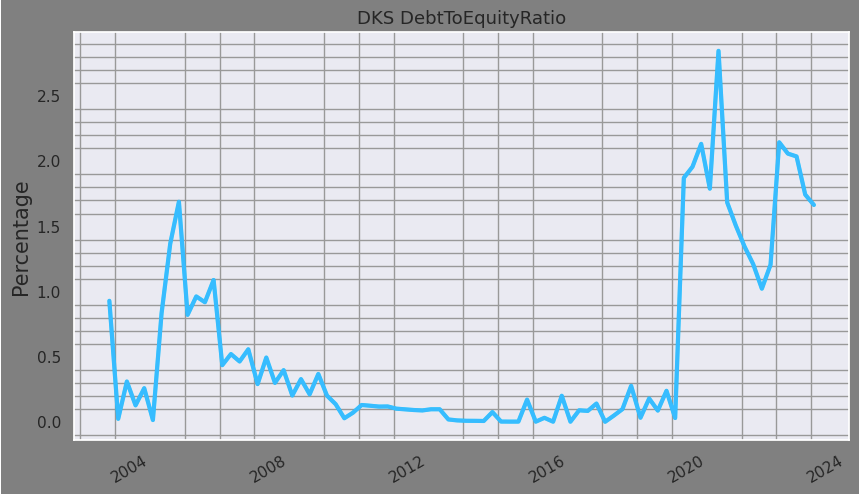

But its debt-to-equity ratio is still at one of its historically higher levels even though the company started to pay some of it off.

{kind=link}

Dick's Debt-to-Equity Ratio (Calculated and Charted by Waterside Insight with data from company)

In our previous article about Dick's, we pointed out it is in an expansionary mode, but the number of stores hadn't grown much at the time. Since then, the company has announced it would expand by about 9 new stores in 2023, 20 new stores across the US in two years, and 100 more new stores in five years, in addition to its recently announced acquisition of Moosejaw. It shows that we were correct and early. To expand aggressively when both interest rates and the inflation rate are higher is an endeavor, to say the least. And on top of that, to expand aggressively, when most of its margins are weakening, and its weakened cash flow has to support not only the high-level debt but also the increased dividend payout, bears the risk that the current market price is not accounted for. Our previous thesis remains valid: Dick's will need to foot the expansion bill with a weaker cash flow. Dick's might capture more topline growth due to this expansion, but it will also have to pay up the costs. As we previously mentioned, most of its stores are through leasing terms, so the costs have large fixing components to them. If the expansion doesn't pan out as expected, the fallout could be more than the market expects.

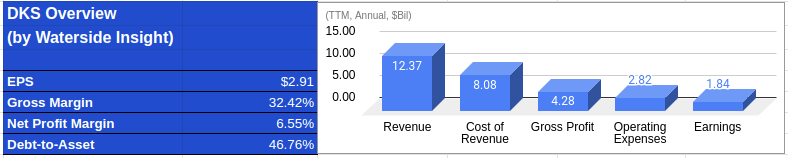

Financial Overview

{kind=link}

Dick's Financial Overview (Calculated and Charted by Waterside Insight with data from company)

Valuation

We maintain our previous assessment of the company regarding its fair valuation since the latest quarter's result confirmed our expectation of continued weakening in cash flow and margin. The current price is much higher than our top estimate. One of the scenarios that could fulfill the current market price is that the company's cash flow and earnings could expand at the mid-teen for the next five years and high single digits for the next five years without any down year. Given the macro environment, the company will be hard-pressed to turn around the current weakening margins within a year or so. Achieving that kind of growth in the next five years will literally require the company to more than double its revenue growth plus a strong cut in costs and expenses every year for at least five years. We think that is unlikely.

For further details see:

DICK'S Sporting Goods: Parsing Under The Earnings Report Sustained Our Thesis