JOUT - DICK'S Sporting Goods: Still Appealing As Fourth Quarter Earnings Near

Summary

- DICK'S Sporting Goods has had some mixed results as of late, though an increase in guidance sent shares of the business higher.

- Fundamentally speaking, the business looks solid, though we could see some weakness at some point due to continued economic uncertainty.

- Given how cheap shares are, though, it seems as though the company has additional upside to offer investors right now.

Every time a company reports financial results for the most recent quarter, it gives that firm an opportunity to reveal the good and bad of how business is going. Because this is the main time when firms provide financial updates, it's also the time when the greatest volatility with a stock can occur. One firm that does have something big to prove when it announces financial results on the morning of March 7 is sporting goods retailer DICK'S Sporting Goods ( DKS ). For the most part, the 2022 fiscal year proved to be rather painful for the company. Having said that, there was a bit of a bright spot when the company announced financial results for the third quarter of the year. Leading up to the fourth quarter earnings release, analysts seem to have somewhat mixed expectations. But a lot of this guidance is not too different from what management has forecasted. Although we're faced with some uncertainty leading into the earnings release, and we also know that shares of the company have roared higher in recent months, I would make the case that the business probably does still have some additional upside to be had. Shares are quite cheap, even if we assume some deterioration in operations. So absent anything significantly outside of the expected, I would make the case that investors should be optimistic moving forward.

Great returns from mixed performance

Back in early August 2022, I wrote an article that took a bullish stance on DICK'S Sporting Goods. In that article, I talked about how the company was showing some signs of returning to more normal financial results following the COVID-19 pandemic. Even with that factored in, I acknowledged that shares of the business looked pricey compared to similar firms. But on the whole, shares were still quite affordable, and the fact that the company is an industry leader makes it even more appealing. At the end of the day, this combination of factors led me to rate the business a "buy." That rating reflects my belief that shares should outperform the broader market for the foreseeable future. And outperform the company did. While the S&P 500 is down 3.4% since the publication of that article, shares of the sporting goods retailer have generated an upside for investors of 38.8%.

{kind=link}

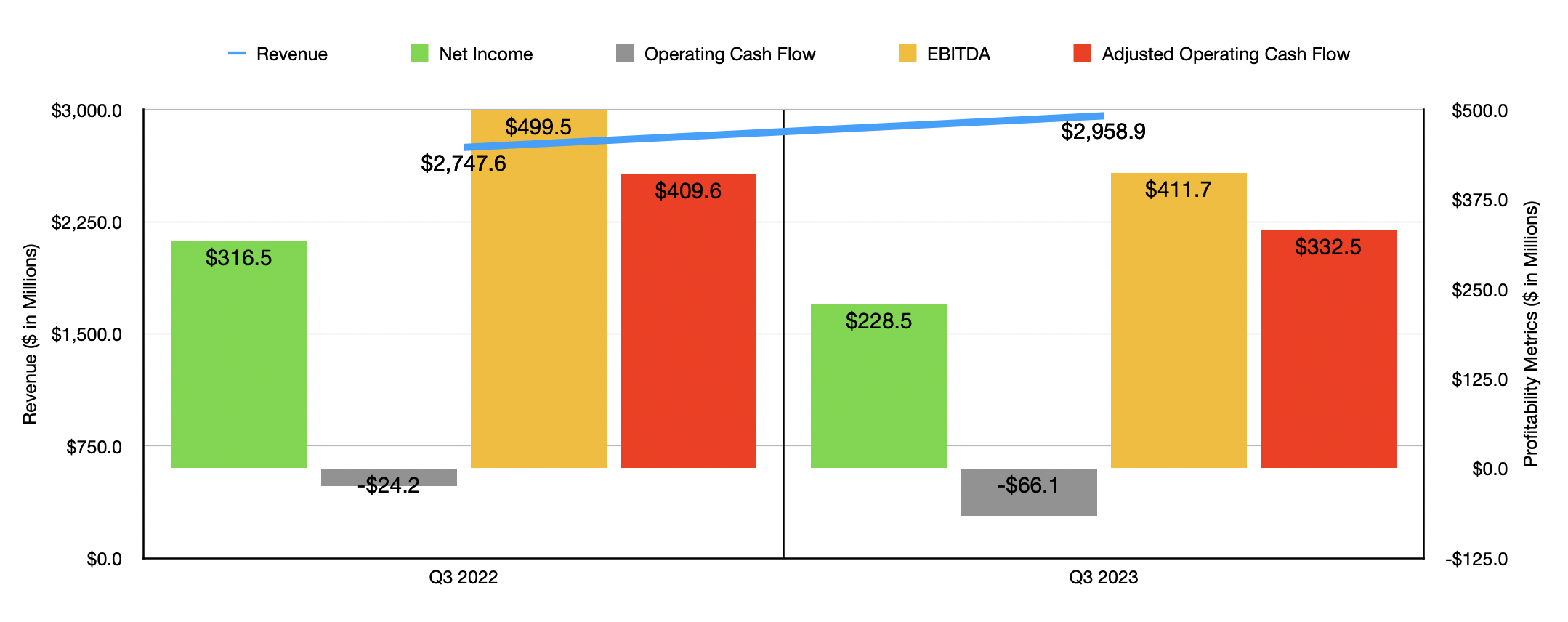

A lot of this upside can be attributed, in my belief, to the financial results that management reported during the third quarter of the 2022 fiscal year . Revenue for the time came in at $2.96 billion. That's 7.7% higher than the $2.75 billion reported the same time one year earlier. This move higher for the company was driven in large part by a 6.5% comparable store sales increase. This was comprised of a 3.7% increase in the number of transactions and a 2.8% rise in the average sales per transaction for the company. It also benefited from two additional locations that the company had in operation compared to the same time one year earlier. $38.2 million worth of the sales increase was driven by new temporary Warehouse Sale stores that the company had.

Although revenue increased nicely, profits pulled back. Net income went from $316.5 million in the third quarter of 2021 to $228.5 million in the third quarter of 2022. The largest contributor to this pain was a decrease in the company's gross profit margin from 38.5% down to 34.2%. This, management said, was attributed largely to actions the company took to reduce targeted apparel inventory overages, as well as higher inventory shrink caused by a rise in theft. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from negative $24.2 million to negative $66.1 million. If we adjust for changes in working capital, it still would have fallen from $409.6 million to $332.5 million. And finally, EBITDA for the business contracted from $499.5 million to $411.7 million.

{kind=link}

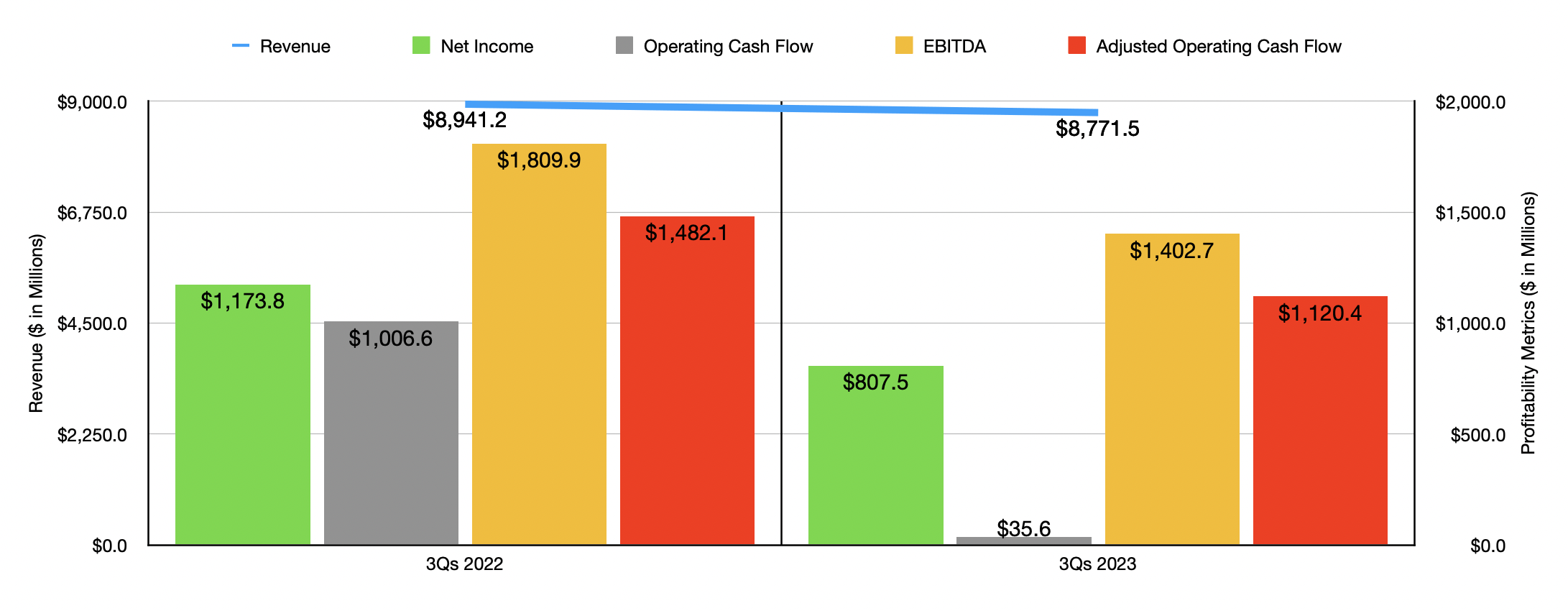

While bottom line results for the company for the third quarter of the year were very similar to what they were for the first nine months as a whole compared to the same time one year earlier, the sales picture was different. For the first nine months of 2021, revenue came in at $8.94 billion. It then dropped to $8.77 billion in the first nine months of 2022. Net income plunged from $1.17 billion to $807.5 million. We saw operating cash flow worsen from $1.01 billion to $35.6 million, while the adjusted figure for this fell from $1.48 billion to $1.12 billion. And finally, EBITDA for the company declined from $1.81 billion to $1.40 billion.

It will be interesting to see what the company reports for the final quarter of 2022. Management did say, during the third quarter earnings release , that 2022 as a whole should be better than previously anticipated. Comparable store sales should range between being negative 3% and negative 1.5%. This compares to the negative 6% to negative 2% previously anticipated. For context, analysts are currently anticipating revenue for the final quarter of roughly $3.44 billion. That would compare to the $3.35 billion the company reported the same time one year earlier. From a profitability perspective, management expects earnings per share for the entirety of the year to come in between $10.50 and $11.10. That's up from the $8.85 to $10.55 previously expected. On an adjusted basis, earnings per share for the entire year should be between $11.50 and $12.10. Previously, management forecasted this at between $10 and $12.00.

When it comes to the fourth quarter alone, analysts currently expect profits per share of $2.83, with adjusted profits per share of $2.89. In the final quarter of the 2021 fiscal year, profits per share stood at $3.16. It's also worth noting that, if we assume that management is accurate about their guidance, then we should anticipate earnings per share for the final quarter of the year of between $2.33 and $2.93, with a midpoint of $2.63. Adjusted earnings, meanwhile, should be between $2.39 and $2.99, with a midpoint of $2.69.

{kind=link}

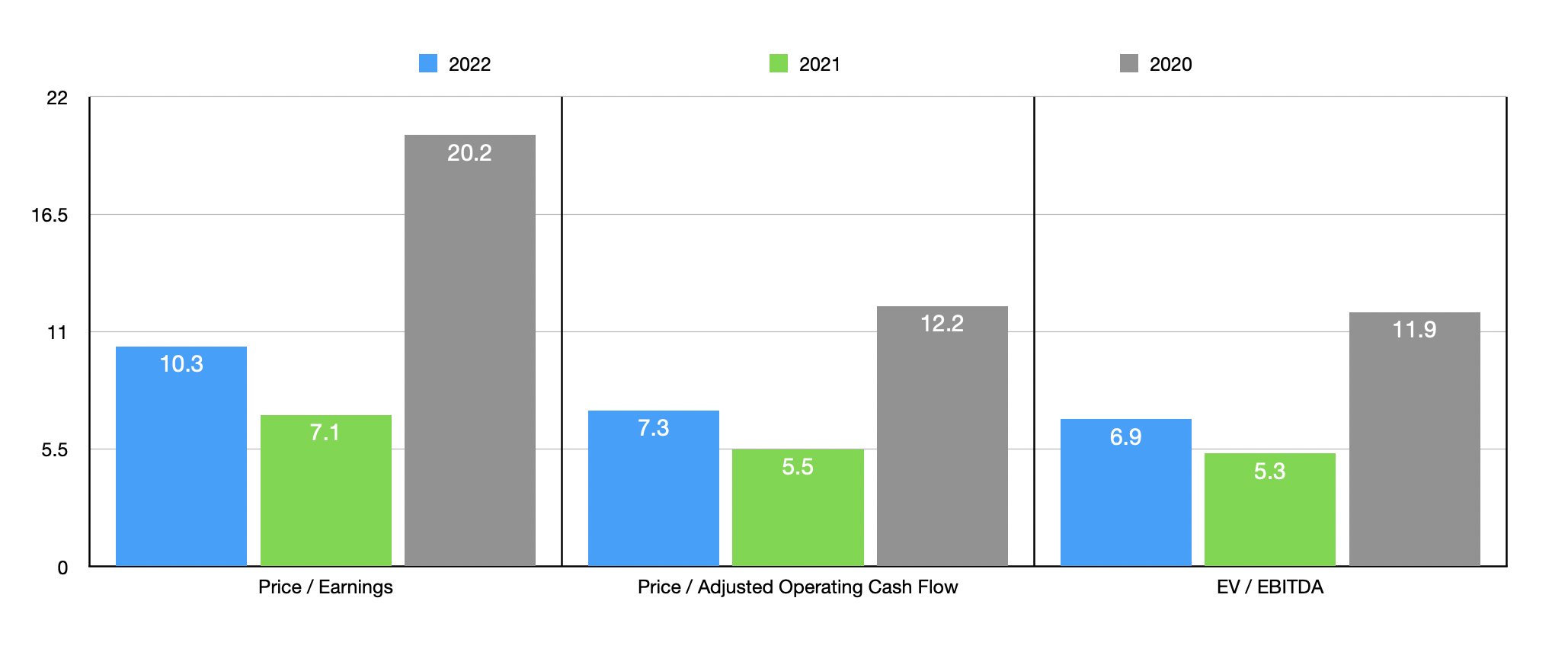

If we take management's forecast on this and use midpoint expectations, then we should anticipate net income for all of 2022 of $1.04 billion. Annualizing results experienced in the first nine months, we would end up with adjusted operating cash flow of $1.47 billion and EBITDA of roughly $1.59 billion. Based on these figures, the company would be trading at a price-to-earnings multiple of 10.3. The price to adjusted operating cash flow multiple would be 7.3, while the EV to EBITDA multiple would come in at 6.9. Using data from 2021, these multiples would be 7.1, 5.5, and 5.3, respectively. Even if we assume that operations deteriorate some and dip back to what they were during the 2020 fiscal year, shares would not look unreasonably priced. At worst, they might be fairly valued in that case, with multiples of 20.2, 12.2, and 11.9, respectively.

As part of my analysis, I ultimately compared DICK'S Sporting Goods to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 3.9 to a high of 16.8. Four of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range for the four companies with positive results was between 4 and 9.9. In this case, two of the four companies were trading cheaper than our prospect. And finally, using the EV to EBITDA approach, the range would be from 4.2 to 8.9, with three of the five companies trading cheaper than our target.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| DICK'S Sporting Goods |

| 10.3 |

| 7.3 |

| 6.9 |

| Academy Sports and Outdoors ( ASO ) |

| 8.1 |

| 9.9 |

| 6.5 |

| Big 5 Sporting Goods ( BGFV ) |

| 4.4 |

| N/A |

| 6.1 |

| Hibbett ( HIBB ) |

| 9.1 |

| 9.2 |

| 7.2 |

| Vista Outdoor ( VSTO ) |

| 3.9 |

| 4.0 |

| 4.2 |

| Johnson Outdoors ( JOUT ) |

| 16.8 |

| 6.1 |

| 8.9 |

Takeaway

I understand that these are confusing times for investors. Mixed financial performance is never a great thing to see for any business. However, investors should be encouraged by the sales figures reported in the third quarter of 2022, as well as by the expectation from analysts that sales should be higher than they were one year earlier. Earnings also are being forecasted by management, it's coming in higher than previously anticipated. Add on top of this how cheap shares are on an absolute basis, even though they might be closer to fairly valued compared to similar firms, and I do believe that some additional upside is probably warranted even though the stock has risen so much in the past several months. Because of all this, I have decided to keep the "buy" rating I assigned the company previously.

For further details see:

DICK'S Sporting Goods: Still Appealing As Fourth Quarter Earnings Near