DKS - DICK's Sporting Goods: Still Not Quite In The Bargain Bin

2023-11-01 04:21:06 ET

Summary

- DICK's Sporting Goods stock is down nearly -25% after missing earnings estimates and cutting guidance.

- Gross margins were the main culprit, as they declined due to organized theft and aggressive discounting to clear outdoor inventory.

- While DKS looks much more attractive from a valuation standpoint, the stock is still not in the bargain bin based on historical multiples.

Back in May , I wrote that DICK's Sporting Goods ( DKS ) had done a great job of transforming its operations over the last several years. However, with the stock trading near its historic 10-year average, I thought the stock looked fairly valued. Since then, the stock is down nearly -25%. Let's catch up on the name.

Company Profile

As a refresher, DKS owns a variety of sporting goods retail concepts. In addition to its namesake brand, it also operates Golf Galaxy, Public Lands, and Going Going Gone!, as well as DICK'S House of Sport and Golf Galaxy Performance Centers. At the end of July, it had 725 DICK'S locations across the U.S. and 135 specialty store locations.

DKS sells merchandise from both national and in-house brands in its stores and online. Nike ( NKE ) is its largest vendor, accounting for just under a quarter of its sales. In-house brand sales, meanwhile, represent just under 15% of sales.

Gross Margin Pressure Leads To Stock Sell-Off

Shares of DKS sank -24.4% the session following its earnings report after the company missed results and cut its guidance.

For Q2, the sporting goods retailer saw its revenue rise 3.6% to $3.22 billion, coming in just shy of analyst estimates of $3.20 billion.

Same-store sales rose 1.8%, with a 2.8% increase in transactions. Average ticket was down -1%.

Adjusted EPS came in at $2.82, missing the consensus by 99 cents.

Gross margins were a big culprit for the earnings miss, as they declined -161 basis points to 34.4%. Merchandise margins dropped by -254 basis points. The company blamed organized theft for its weaker than expected margins. However, aggressively discounting on some items to keep its inventory clean accounted for about two-thirds of the gross margin decline, while the higher shrink due to theft made up a third of the decline.

On its Q2 earnings call, CEO Lauren Hobart said:

"Two key factors impacted our second quarter gross margin relative to our original expectations. The first was the impact of higher inventory shrink. Organized retail crime and theft in general, an increasingly serious issue impacting many retailers. Based on the results from our most recent physical inventory cycle, the impact of theft on our shrink was meaningful to both our Q2 results and our go-forward expectations for the balance of the year. We are doing everything we can to address the problem and keep our stores, teammates, and athletes safe. And second, beyond shrink, we also took decisive action on excess products, particularly in the outdoor category to allow us to bring in new receipts and ensure our inventory remains vibrant and well positioned. Keeping our inventory fresh is one of our key operating philosophies. And we're pleased that our inventory was down 5% at the end of the quarter."

Turning to the balance sheet, DKS ended the quarter with $1.9 billion in cash and equivalents and zero debt. Inventory was down -5%.

DKS bought back nearly $203 million in stock in the quarter, repurchasing 1.6 million shares.

Looking ahead, the company reiterated its guidance for full-year same-store sales of between 0-2%. It noted the mid-point of guidance implies comparable-store sales to be flat in the second half.

Meanwhile, it lowered its adjusted EPS guidance from a range of $12.90-13.80 to $11.50-12.30. Higher shrink will reduce its gross margins by 50 basis points, but it does expect gross margins to improve in the back half of the year as it anniversaries earlier clearance activity.

Organized retail theft is becoming a major issue for retailers. DKS isn't the only retailer to be impacted by the issue, with Target ( TGT ), Macy's ( M ), and Lowe's ( LOW ) also calling out theft as a reason for earnings softness. Last month , the National Retail Federation ((NRF)) said that in fiscal 2022 shrink from retail theft increased by over 19% to $112.1 billion. Meanwhile, a NRF survey showed retailers were seeing even more violence and aggression from organized crime this year.

Currently there are now signs of retail theft slowing down, and prevention attempts will also cost money. Right now, it doesn't seem any retailer has cracked the code to this problem yet. As such, expect this to be an ongoing headwind.

Meanwhile, the actions to clear inventory, while not a good sign, did appear very targeted towards the outdoor category and the company did end the quarter with lower inventory. So while the quarter and guidance were disappointing, I think overall DKS' management continues to do the right thing. Going forward, however, we'll also have to see if the macro environment has any impact on consumer spending as well.

Valuation

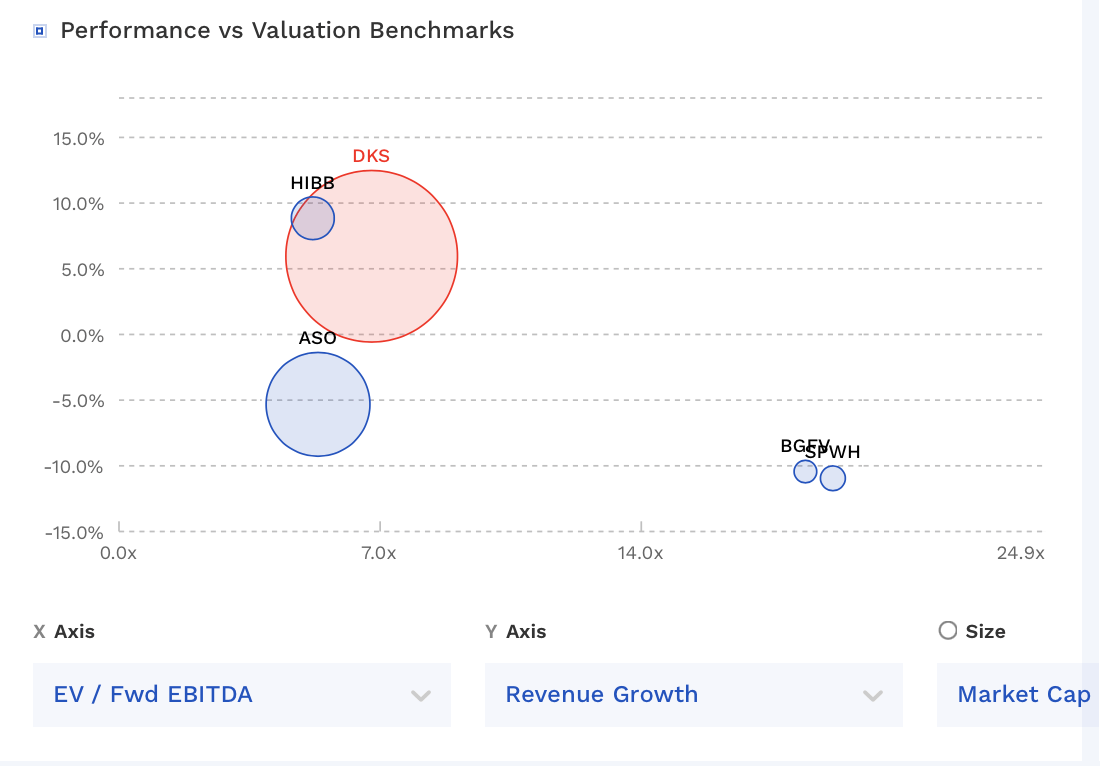

DKS stock currently trades just under 6.8x the FY 2024 (ending January) consensus EBITDA of $1.66 billion. Based on FY25 analyst estimates of $1.74 billion, its trades at 6.5x.

From an EBITDAR perspective, it trades at 5x FY24 estimates and 4.8x FY25 estimates.

It trades at a forward PE of 8.9x the FY24 consensus of $11.88 and 8.6x the FY25 consensus of $12.32.

The company is projected to grow revenue 3.1% in FY24 to $12.8 billion and 2.0% in FY25 to $13.1 billion.

The stock trades around the middle of where other sporting goods retailers trade, although a bit higher than its two closest competitors in Academy Sports ( ASO ) and Hibbett ( HIBB ). Given its leadership position in the space, this slight premium is deserved in my opinion.

{kind=link}

Conclusion

The sell-off in DKS stock has certainly made the valuation more attractive, although it is still not in the bargain bin by historical standards. The stock has traded at an average EV/EBITDA of 7.1x since 2019, so it right around those levels now.

Now I still like what the company has done with a shift towards selling more private label, as well as getting more exclusive items from brands like NKE to drive sales. I also like how it has started to create destinations with DICK'S House of Sport, which it is opening more of, including having 9 grand openings in August.

That said, the company is dealing with increased theft issues, and the macro is something that continues to need to be watched. The consumer and job market have continued to be resilient, but the Fed seemingly wants to push unemployment higher to get inflation down. That would likely hurt consumer spending and the retail sector as a whole.

Given this backdrop, I wouldn't be a new buyer in DKS at the moment with the stock trading near where it has historically over the past several years. If the stock gets thrown into the bargain bin - say $75 and a 5x EV/EBITDA multiple - I'd be a buyer of the stock. For now, though, my "Hold' rating remains.

For further details see:

DICK's Sporting Goods: Still Not Quite In The Bargain Bin