DKS - DICK'S Sporting Goods: Strong Business To Tide Through This Environment

2024-01-21 08:35:53 ET

Summary

- I recommend to buy DKS due to its resilience business model, ability to navigate the current macro environment and potential for margin expansion.

- The company's affordable pricing strategy and position as the largest player in the industry allow it to withstand the weak consumer spending environment.

- Dick's Sporting Goods has a strong historical financial performance.

Summary

I am recommending buying DICK'S Sporting Goods, Inc. (DKS), as the business is well positioned to navigate the current macro environment and has room for margin to further expand. DKS's historical financial performance and track record of capital returns also lend credence to its ability to tide through this tough period. I expect the revenue growth trajectory to follow a similar fashion to what happened during subprime, where DKS saw growth acceleration.

Business description

DKS is the leader in the US sporting goods retail industry. Its strategy is to offer a large assortment of products and price them at an affordable price range that caters to the mass market. It boasts the largest revenue size of over $12 billion as of FY22, which represents about 11% of the industry's revenue share.

DKS is well positioned to tide through this weak macro environment

The worry about selling consumer products today is that the spending environment is clearly weak , mainly because of the higher interest rate and inflation environment that have reduced the amount of disposable income that consumers have. While this is a bad situation for many retailers, I believe it is net positive for DKS from multiple perspectives:

- DKS products are priced in an affordable price range that does not get impacted as much as other retailers that are priced higher. This is evident from DKS's recent performance, where the business continued to print positive growth.

- Being the largest player in the industry, DKS is able to pass through inflationary pressure to consumers to keep margins intact. This is evident from gross margin performance staying in the mid-30% range.

- The weak consumer spending environment and high cost of capital (high rates) have caused many retailers to shut their doors , giving up dollar shares for DKS to capture them. In economic terms, DKS was well positioned to consolidate market share when other players exited.

Regarding point 1, DKS's recent result says it all. In 3Q23, the business reported a comp sales growth of 1.7%, driven by both transaction volume and ticket size. The company is not witnessing any indications of a trade-down, and management mentioned that the DKS customer has held up well. They also mentioned that all income demographics across their portfolio grew. The one noteworthy qualitative observation is that the company's management observed an increase in customers' spending per trip. Additionally, the company continued to gain market share in core categories. These indicate that DKS products and price ranges are increasingly resonating with consumers. Since this dynamic is happening across all categories, it is safe to say that the trend is across the entire consumer population and not a particular group.

As a final thing to close off this section, as DKS has lived through two major economic downturns in the past (Dotcom and Subprime), it has an experience advantage over new players that only entered the industry in recent years. This experience is crucial as it equips the management team with knowledge on how to set the right price range, offer the right types of products, manage inventories, and calculate gross margins.

Margin has further room to improve

DKS should see margin expansion momentum continue in the near term. In 3Q23, DKS's gross margin expanded 88 bps to 35.1%, driven by lower supply chain costs and a better merchandise margin. I believe this margin expansion strength is a signal that DKS is completely done and dusted with regard to the inventory issues that it faced previously (inventory has been marked down and expectations reset). Essentially, DKS has cleaned up the inventory issue and now has a fresh set of inventories to address current demand. Looking into FY25, a lower shrink headwind (lower theft rate as management steps up combating against it), better inventory assortment, a higher merchandise margin (50% higher than pre-COVID), and lower freight costs, I expect gross margin to improve.

To be clear, absent the shrink headwind our merchandise margin would have increased over 70 basis points. Combating theft remains a top priority and we continue to invest in efforts to keep our stores, teammates, and athletes safe. Source: 3Q23 earnings

The improved gross margins should flow nicely to the EBIT line as DKS continues to manage its operating costs. There should be further room for SG&A to leverage as DKS continues to optimize the business in its support center function and also in its outdoor specialty business by integrating the team for Public Lands and Moosejaw. While it is tough to quantify the impacts, management expects to see positive impacts.

All in all, a better gross margin outlook coupled with further SG&A deleverage through productivity improvements should drive EBIT expansion.

Strong financial performance

One cannot talk about DKS without mentioning its historical financial performance, which lends credence to its execution strength. DKS has been a formidable force over the past 23 years, where it has never once generated negative annual growth except in FY19. Even during the subprime crisis, the business only saw growth deceleration, not negative growth. The same was true for its profitability performance; DKS has never once reported a loss on an annual basis and has generated positive FCF most of the time (only 4 out of 23 years was a negative figure). The DKS balance sheet also remained in net cash for the majority of the latest decade. The good thing here is that DKS returns cash to shareholders either via dividends or share buybacks. In recent years, management has stepped up its pace of share buyback, reducing the share count from 100 million in FY14 to just 58 million as of 3Q23. This is a massive reduction, or 42% over 9 years. This translates to around ~3+%/year, and if we include the ~2% dividend yield over the same period, DKS effectively returned 5+% a year to shareholders.

I believe this strong historical performance is a testament to DKS's ability to withstand economic cycles, and management has shareholder returns in mind. These are things that should support stock sentiment in today's capital markets environment.

Valuation

{kind=link}

Based on my view of the business, DKS should see growth and recovery over the next 2 years. I believe we are gradually going into the recovery phase as inflation has tapered down to 3.4% from the high of 6+% last year, and that the Fed is also looking to cut rates which will reduce the cost of capital for businesses. Both of these paint a positive picture of the economy, which has a direct positive impact on retail . Given DKS experience in the industry and execution capabilities (evident from both Academy Sports & Outdoors Inc. and Hibbett year-to-date showing negative growth unlike DKS which generated positive growth), should allow it to continue growing above industry levels.

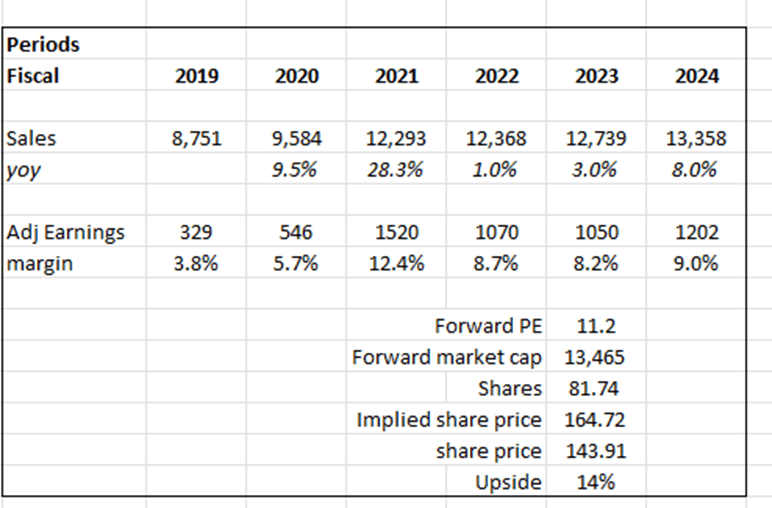

My growth assumptions are based on how DKS fared during subprime. Back then, growth saw a similar big decline from 25% growth in FY07 to 6% growth in FY08, followed by a modest recovery in FY09 and a bigger acceleration in FY10. I believe DKS is going through a similar motion. Growth saw a big decline, from 28% in FY21 to 1% in FY22. FY23 should see a modest recovery, followed by a bigger acceleration in FY24. My 8% assumption in FY25 is benchmarked against how the business has performed pre-COVID (growing at around 8% on average between FY14 and FY18). DKS has historically traded at a premium to peers like Academy Sports & Outdoors Inc. and Hibbett, who are trading at 8x and 7x forward P/E, respectively. I expect this premium to continue as DKS maintains its position as the largest player (highest EBITDA margin). I value DKS at 11.2x forward P/E, the current level it is trading at.

Risk & conclusion

Although DKS has gone through multiple cycles of economic downturn, there is no guarantee that DKS will get through this cycle in a similar fashion. For all we know, this could be a much bigger downturn than what we are seeing today. In a full-blown recession, DKS, being a consumer-facing retailer, will definitely feel the heat, and growth could very well turn negative.

Overall, I am recommending to buy DKS. Despite the weak consumer spending environment, I believe DKS is well positioned due to its affordable pricing strategy, product assortment, and experience in navigating such environment. Recent results also suggest that DKS products and pricing resonate with consumers across income demographics. Margin should improve from here as previous inventory issues are gone and management is working through their plans to optimize the business.

For further details see:

DICK'S Sporting Goods: Strong Business To Tide Through This Environment