DGII - Digi International: Strong Start To Fiscal Year 2023 But Hold Rating Stands

Summary

- Digi had a strong start to fiscal year 2023 with balanced strength across all business units and geographies.

- Digi provided guidance for the second quarter of fiscal year 2023 with revenues of $105 million to $109 million and Adjusted EBITDA between $21.0 million and $22.5 million.

- Digi has confidence in its annual projections for FY23, with expected revenue growth of over 10% and faster growth for ARR and adjusted EBITDA.

- At the P/E multiple of 52.4x, Digi stock trades at a premium confirmed by the DCF valuation, where Digi's fair value is $29.5 against the market price of $34.5 per share.

Investment Hypothesis

Digi International Inc. ( DGII ) has reported strong financial results for the first quarter of its fiscal year, 2023, due to high demand and a better supply chain. All its business units and geographies saw revenue growth, with balanced strength across the company. The IoT products and services segment saw a 28% growth driven by growth in OEM and cellular product lines, while IoT solutions saw a 35% growth driven by the Ventus acquisition .

The company has forecasted revenues of $105 million to $109 million in the next quarter. Digi is confident that they will grow revenues by over 10% in FY23, with ARR growing faster than their revenue growth. However, at the current P/E of 52.4x, Digi trades at a higher earnings multiple. Further, my DCF analysis yields $29.5 per share against the current $34.5. Digi is a growth stock; all growth stocks trade at a premium due to the high potential growth. Thus, my recommendation for the existing stockholders is to hold the stock, while for the new investors, I suggest waiting until the next quarter's results to make a buy decision.

About Digi International

Digi International Inc ., headquartered in Hopkins, Minnesota and founded in 1985, offers IoT products, services, and solutions in the United States and internationally. The company has two segments: IoT Products & Services and IoT Solutions. The company provides products and services that help customers create and deploy secure IoT (Internet of Things) connectivity solutions. These products include wireless modules, routers, and device management platforms. The company also offers Managed Network-as-a-Service (MNaaS) and SmartSense by Digi services that provide cellular and fixed line WAN solutions for various sectors and wireless temperature and other monitoring services for specific markets such as food service, healthcare, and supply chain. Digi International competes on various factors such as product features, service and software application capabilities, brand recognition, technical support, quality and reliability, product development, price, and availability to win customers. Thus, the company strives to offer high-quality products, reliable and responsive customer service, and competitive prices to stay ahead of the competition.

On February 2 2023, Digi International Inc. reported its results for the first fiscal quarter of 2023. The company saw a 30% increase in revenue, totalling $109 million. The gross profit margin was 56.3%, slightly lower than last year's, but it was 57.3%, excluding amortization. Adjusted EBITDA was $23 million, a 38% increase. In addition, the company reported $96 million in annualized recurring revenue at the end of the quarter, which is an 8% increase.

{kind=link}

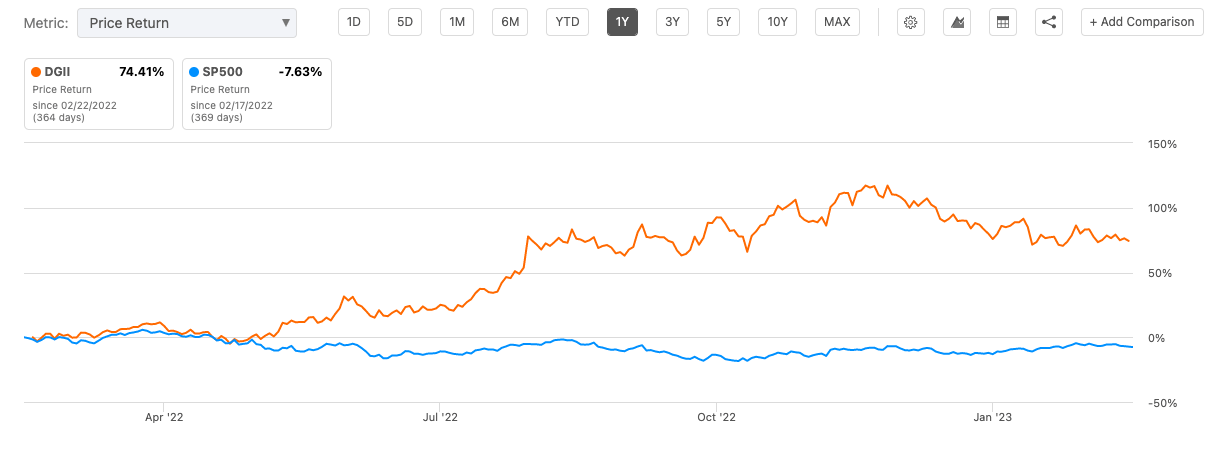

Digi has generated excellent returns for its shareholders, giving 74.4% returns in the last year and 231.2% returns in the last five years compared to the S&P 500 index of -7.6% and 49.8% in the last twelve months and five years, respectively because of the double-digit growth the company has managed in the low growth environment and the high growth markets it operates.

Author Calculations

The high share price is reflected in a higher P/E ratio as the P/E multiple jumped from 34.8x in 2019 to 95.7x in 2022, as EV/EBITDA doubled from 11.9x in 2019 to 22.6x in 2022, implying that the market has priced a high growth potential for the company in the future.

For Digi International Inc., ARR (Annual Recurring Revenue) is a way to measure the value of all its subscription contracts over a year based on how much money the company gets each month from these subscriptions. The company uses ARR to track the growth of the company's subscription business and how it's doing over time. ARR differs from revenue and deferred revenue. It helps the company understand how much money it can expect to receive over the next year from its existing subscription customers and is helpful for planning and decision-making.

According to Ron Konezny , President and Chief Executive Officer of Digi International.

Digi is off to a fast start to our fiscal 2023, driven by solid demand and a gradually easing supply chain. Our fiscal first quarter saw balanced strength across all our business units and geographies. Our business and mission-critical solutions are helping drive our customers' digital transformation and delivering valuable ROI. Thank you for the incredible performance of the Digi team and our suppliers and channel partners.

Author Calculations

The company grew steadily in the last five years, from $226.9 million in 2017 to $388.2 million in 2022 at 16.4% CAGR. However, the company reported spectacular growth in 2022, growing at 25.8% year-on-year.

10 Q Report

IoT Products & Services revenue increased by 28.3% last quarter due to higher demand for specific products like OEM, console servers, and cellular products. Further, IoT Solutions revenue increased 34.8% for the last quarter due to higher sales of SmartSense and Ventus offerings, which the company acquired in November 2021.

Author Calculations

The company's gross margin improved steadily from 48% in 2019 to 57.1% in 2022. An increase in EBIT margin from 5.8% in 2021 to 9.5% in 2022 means that the company has become more profitable and reduced its expenses as a percentage of revenue. The reason for this improvement could be a decline in spending on marketing and advertising costs, better optimization of its supply chain and higher operating efficiency. This increase in EBIT margin is a positive sign for the company, as it is becoming more efficient and profitable.

10Q Report

During the three months ending on December 31, 2022, the gross profit margin of the company's IoT Products & Services division increased slightly compared to the same period the previous year because the company changed the types of products sold and the customers who bought them, which allowed them to sell at a slightly higher profit margin. On the other hand, the gross profit margin of the company's IoT Solutions division decreased significantly for the same period, mainly due to higher expenses incurred to maintain inventory levels, which reduced the profit margin.

Author Calculations

The company's asset turnover is 0.5x and stable in the last two years. However, the company does not capitalize on its R&D expenses; thus, the asset turnover does not indicate how much turnover it generates from its assets. R&D expenses generate future benefits, thus, they are capital expenditures, and as with any capex, the company must capitalize on these investments. Furthermore, asset efficiency declined from 10.1% in 2021 to 5.5% in 2022 due to the Ventus acquisition and higher inventory buildup. The company expect inventory levels to decrease over time but notes that some constraints may cause inventory to fluctuate. The company will add inventory to secure forward-looking revenue from the backlog. With component shortages, the company will take advantage of them and buy the necessary components even if they don't yet have a particular project for them. Still, the company is confident that inventory will reach normalized levels over time.

Author Calculations

The company had a negative net debt, implying it held more cash than debt. However, its net debt increased from -85.6 million in 2021 to $223.2 million in 2022, with its total debt to capital increasing from 8.6% in 2021 to 18.5% in 2022.

Digi has historically funded its operations and expenses from funds generated by its business. However, in the fiscal year 2022, Digi took on some debt to finance its acquisition of Ventus. As a result, Digi's liquidity requirements mainly stem from its working capital needs, but it also needs funds to pay for capital expenditures necessary to run and grow its business.

Digi entered a new credit agreement on December 2, 2021, refinancing its previous loan facility. The new credit agreement includes a $350 million term loan B secured loan and a $35 million revolving credit facility with a $10 million letter of credit sub facility and a $10 million Swingline sub facility. As of December 31, 2022, there was $35 million available under the Revolving Loan, which included $10 million available for a letter of credit sub facility and $10 million for a Swingline sub facility. In addition, Digi repaid all outstanding balances on its previous loan facility during the first quarter of fiscal 2022.

Author Calculations

Due to the debt taken for acquisitions, Digi's interest coverage ratio declined from 12.8x in 2021 to 1.9x in 2022. However, additional debt taken for acquisitions has increased the interest expenses, impacting the company's credit rating.

Author Calculations

Digi's Days sales outstanding have improved from 61 days in 2021 to 44 days in 2022, implying that companies efficiently collected cash from their customers partly due to their growth in subscription revenues. Thus, the cash conversion cycle has improved from 120 days in 2021 to 112 days in 2022.

Author Calculations

Due to the Ventus acquisition, Goodwill increased from $225.5 million to $340.5 million, implying that the company has paid a premium for the acquisition after accounting for the fair value of the assets and intangibles. In addition, the Goodwill and intangibles also increased from $343.6 million to $642.5 million.

Author Calculations

Digi had less cash inflow from its operations in the three months that ended December 31, 2022, compared to the same period in 2021.

The decrease of $3.2 million in cash flows from operating activities from $37.7 million in Q3 2022 to $34.5 million in Q4 2022 was primarily due to two factors. Firstly, there was an increase in operating assets and liabilities (net of acquisitions) of $18.3 million in 2022 compared to $10.3 million in 2021, implying that the company had to use more cash to fund its operations in 2022 than in 2021. Secondly, there was an increase in stock-based compensation expense, a non-cash expense that reduced cash flows from operations. However, this decrease was partially offset by increases in net income and the provision for inventory obsolescence and decreases in the provisions for deferred income tax, bad debt, and amortization expense.

The decrease of $347.1 million in cash flows from ($349.5) million in Q3 2022 to ($2.4) million used in investing activities was primarily due to the absence of any amounts used for the acquisition of businesses in 2022 compared to $347.6 million used for acquisitions in 2021, which was primarily related to the Digi's acquisition of Ventus in November 2021.

The decrease of $242.9 million in cash flows from financing activities ($192.8 million in Q3 2022 to $-50 million in Q4 2022) was primarily due to the absence of any proceeds from debt in 2022 compared to $350.0 million in proceeds from a Term Loan issued in 2021. In addition, there was a $3.4 million decrease in proceeds from stock issuances in 2022 compared to the previous year. However, this decrease was partially offset by debt payments of $4.4 million in 2022 compared to $98.1 million in 2021, $13.4 million in debt issuance cost payments, and a $3.0 million decrease in taxes paid for net share settlements. Thus, Digi used more cash to fund its operations in 2022 than in 2021 but had lower cash outflows for investing and financing activities.

Author Calculations

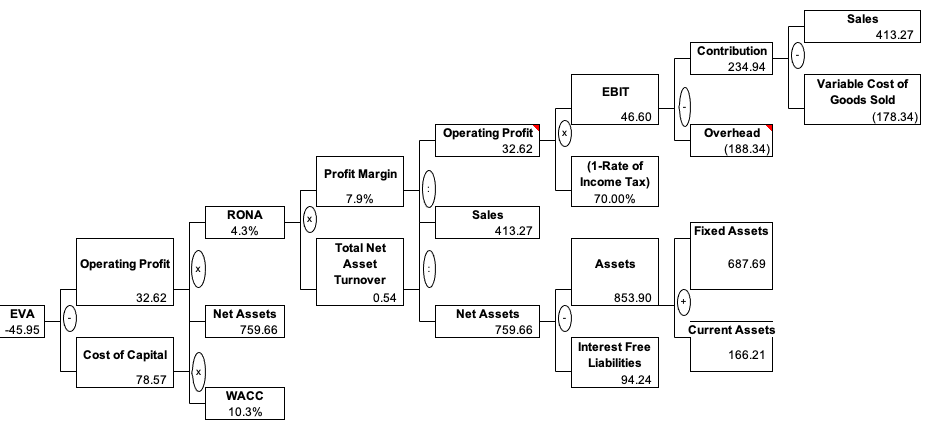

Digi's ROIC and ROA have improved to 4% and 2.6% in 2022 from 2.5% and 1.8% in 2021. However, though there is an improvement in ROIC and ROA, it is lesser than its cost of capital of 10.3%, implying that the company is not generating excess returns.

{kind=link}

The company generates -45.9 million in Economic value added, implying that Digi has not generated enough operating profits to cover its cost of capital. As a result, the company must find a way to improve its EVA; otherwise, it could lead to a decline in its stock price, decreased investor confidence, and difficulties accessing financing.

According to the company, Ventus integration is mainly complete. However, a significant milestone still exists: converting their ERP and CRM to Digi's systems. In addition, the acquisitions give Digi access to European markets. At this point, Digi is focused on integration execution, reducing leverage, and preparing for rising rates environments. After that, however, the company intends to do bigger deals for inorganic growth. Still, they want to take time to identify the right target that gives them confidence in being the best owner and operator of those businesses.

In the future, Digi expects revenues for the quarter to be between $105 million and $109 million, slightly above the consensus estimate of $104.53 million. The company also expects Adjusted EBITDA to be between $21.0 million and $22.5 million for the quarter. Using a diluted share count of 37.0 million outstanding shares, the company projects its Adjusted EPS to be between $0.42 and $0.46 per diluted share, slightly below the consensus estimate of $0.45.

The company will focus on two initiatives in 2023. The first initiative is transitioning to complete solutions that include software and service offerings and their products which will drive Annualized Recurring Revenue ("ARR") and more predictable and higher margin revenue. The second initiative is to deliver higher customer service across all their businesses, improving customer satisfaction, loyalty, and retention, all essential factors driving long-term growth and profitability.

According to the company.

Based on our first fiscal quarter performance and second fiscal quarter guidance, we have stronger confidence in our annual projections for FY23. We now expect to grow revenues by over 10% as the supply chain continues to ease and demand remains strong. We expect ARR and A-EBITDA to grow faster than our revenue growth.

Risks

Digi has borrowed debt to fund the acquisition, exposing the company to interest rates and foreign currency risk.

Digi is exposed to fluctuations in interest rates on amounts borrowed under the Credit Facility, which could impact future earnings and cash flows. For example, the annualized effect of a 25 basis point change in interest rates would increase or decrease Digi's interest expense by $0.6 million.

Digi is exposed to foreign currency translation risk as its foreign subsidiaries' financial position, and operating results are translated into U.S. Dollars for consolidation. A 10% change in the average exchange rate for the Euro, British Pound, Australian, and Canadian Dollar to the U.S. Dollar during the first three months of fiscal 2023 will result in a 1.0% increase or decrease in stockholders' equity due to foreign currency translation.

Valuation

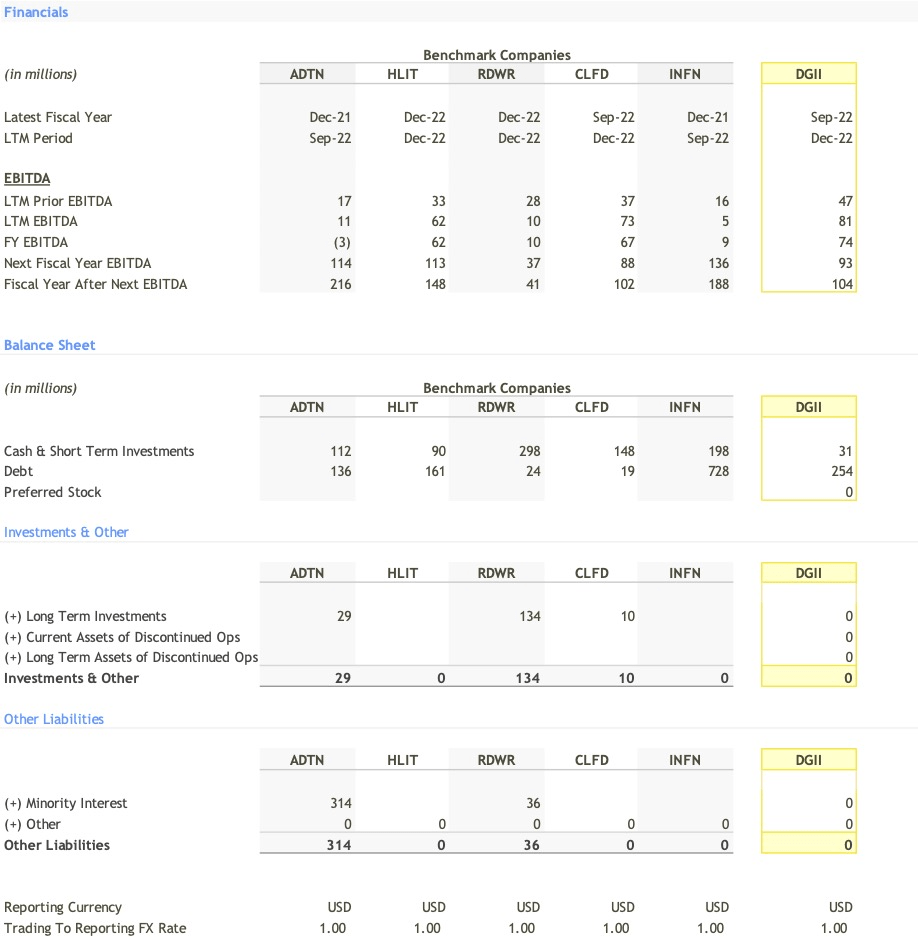

Before I do the Discounted cash flow valuation of Digi, I wanted to benchmark Digi against its peers to assess its performance in revenue growth, margin, leverage and returns it generates for its shareholders.

For my benchmarking analysis, I identify the following companies:

- ADTRAN Holdings, Inc. ( ADTN )

- Harmonic Inc. ( HLIT )

- Radware Ltd. ( RDWR )

- Clearfield, Inc. ( CLFD )

- Infinera Corporation ( INFN )

{kind=link}

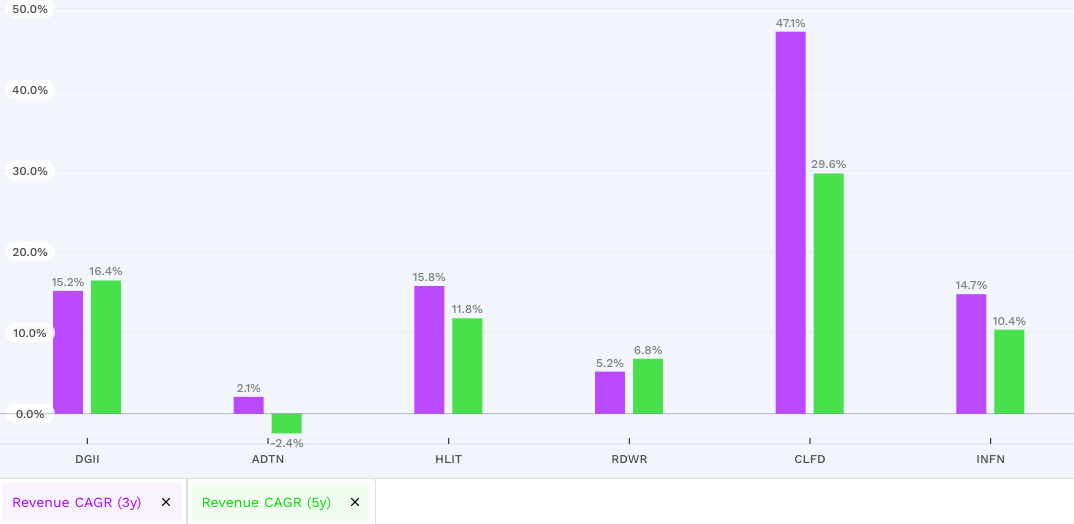

Digi's revenues have grown by 15.2% CAGR in the last three years and 16.4% CAGR in the last five years, much better than its peers. A part of this growth is because the company operates in highly growing IoT markets and responds to the demand with its attractive portfolio of services.

{kind=link}

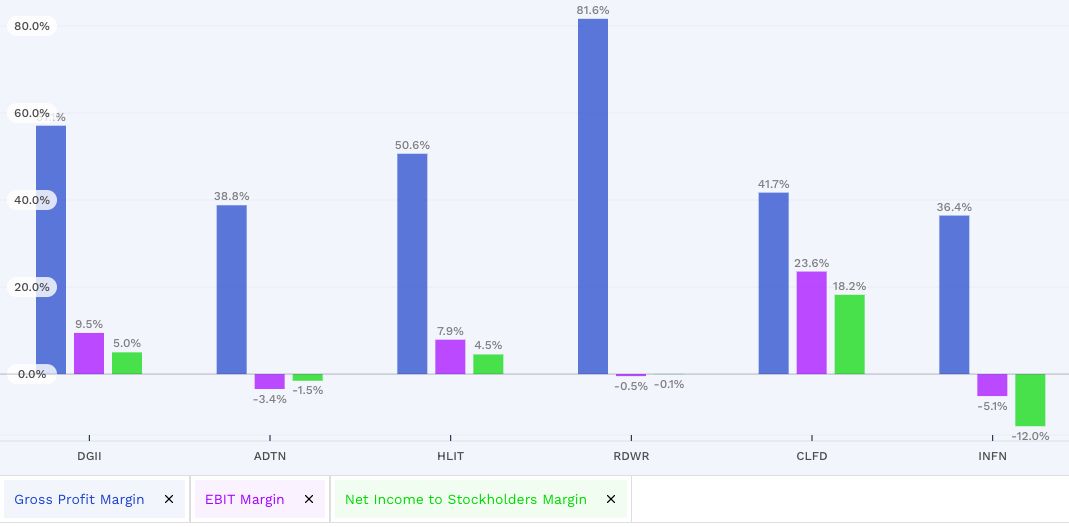

Digi's gross margin of 57% is healthy and comparable to the sector. However, the operating margin of 9.5% is partly due to higher spending on marketing and advertising and partly because the company expenses R&D instead of capitalizing on its R&D spend. Thus, all the peers have a low EBIT margin, which indicates the sector.

{kind=link}

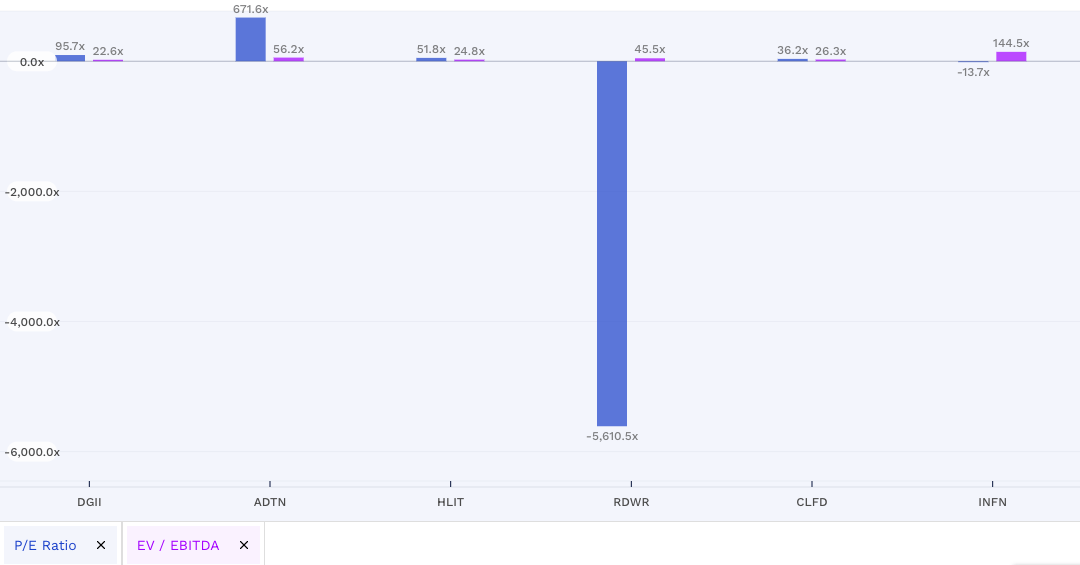

Digi is operating in a high-growth IoT market that reflects high P/E ratios. All companies in this sector have high P/E multiples, reflecting IoT markets' high growth potential.

{kind=link}

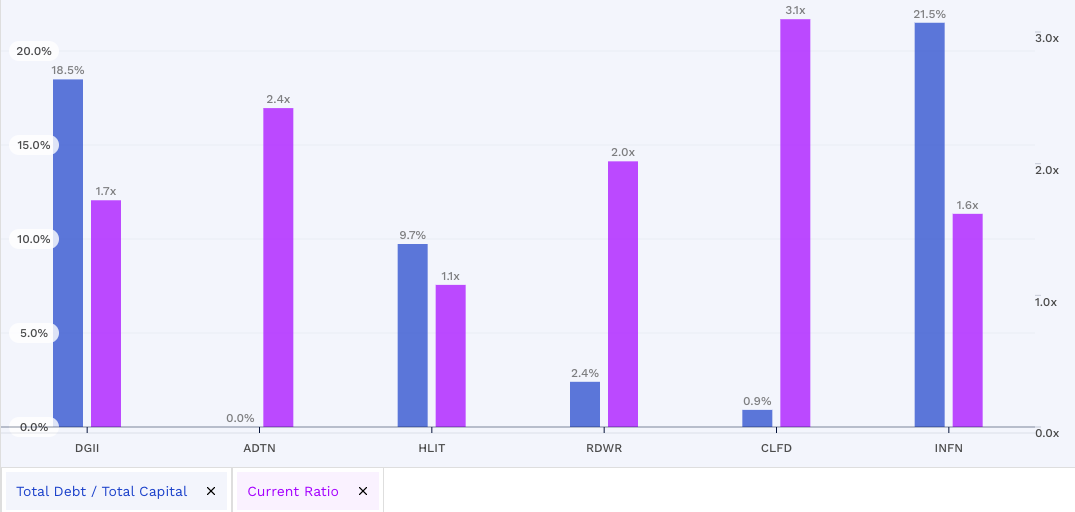

Digi is operating in a high-growth IoT market and is reinvesting a significant part of its earnings to fund its growth. As with other firms operating in high-growth sectors, companies have a low debt ratio as they value flexibility. Digi's debt ratio has increased in the last year as it has taken debt to fund the acquisitions, because of which it appears to have high leverage against its peers. However, the company will reduce its debt, and the debt ratio will revert to normal. Digi's current ratio is also lower than its peers, which reflects its higher inventory levels to fund its high backlog of projects. However, the company is confident that the inventory will normalize.

{kind=link}

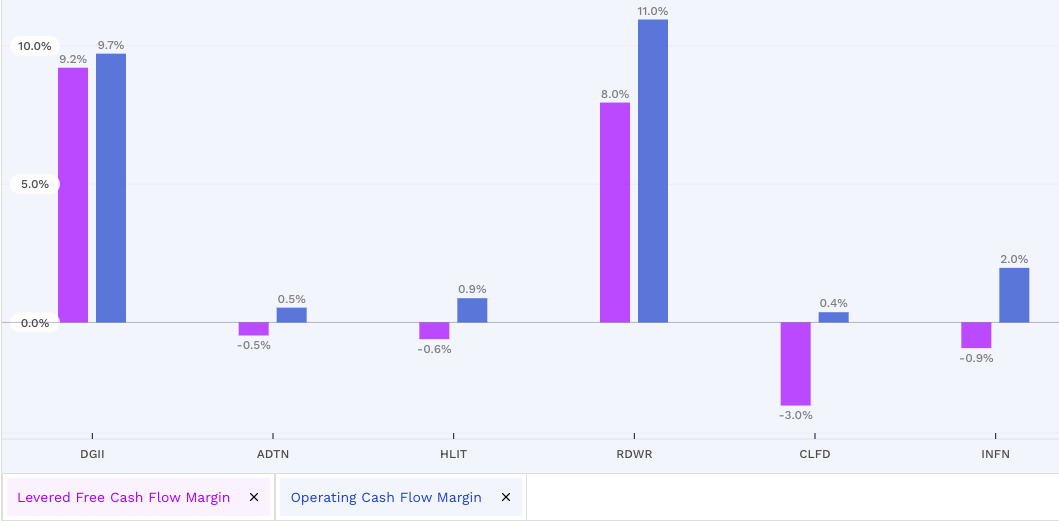

Digi has better cash flows from operations as a percentage of revenues compared to its peers and indicates that a company is generating more cash from its core operations, which can be used to invest in the business, pay down debt, or return capital to shareholders.

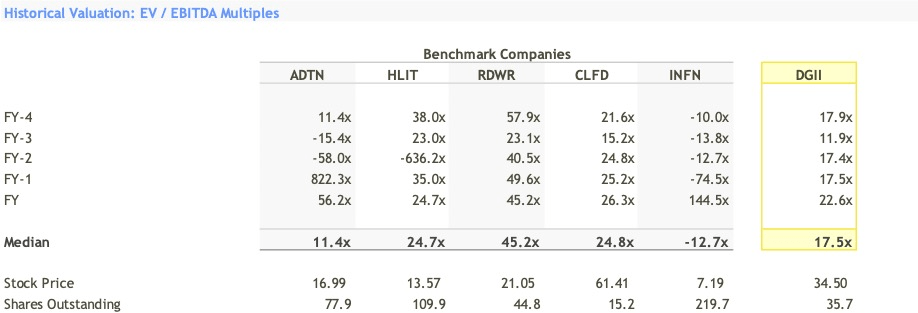

I do a comparable valuation for Digi benchmarking it against other companies using the EV/EBITDA multiple.

{kind=link}

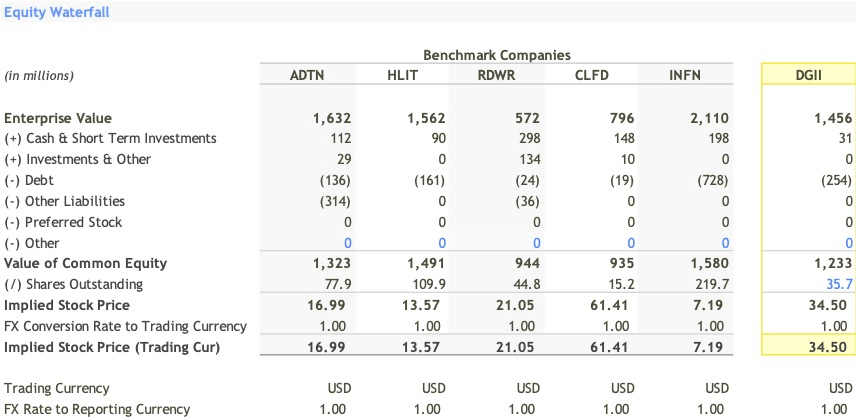

I calculate the equity waterfall for all the companies by looking at the total debt, cash and other liabilities and deducting them against its enterprise value.

{kind=link}

Then, I look at Digi and its peers' income statements and balance sheets. Digi's cash reserves are the lowest among its peers, while its debt is among the largest due to additional debt taken by the company to fund the Ventus acquisition.

{kind=link}

After looking at the financials, I analyze the historical EV/EBITDA multiples of Digi and other companies. All the companies are trading at higher multiples because they operate in high-growth IoT markets.

{kind=link}

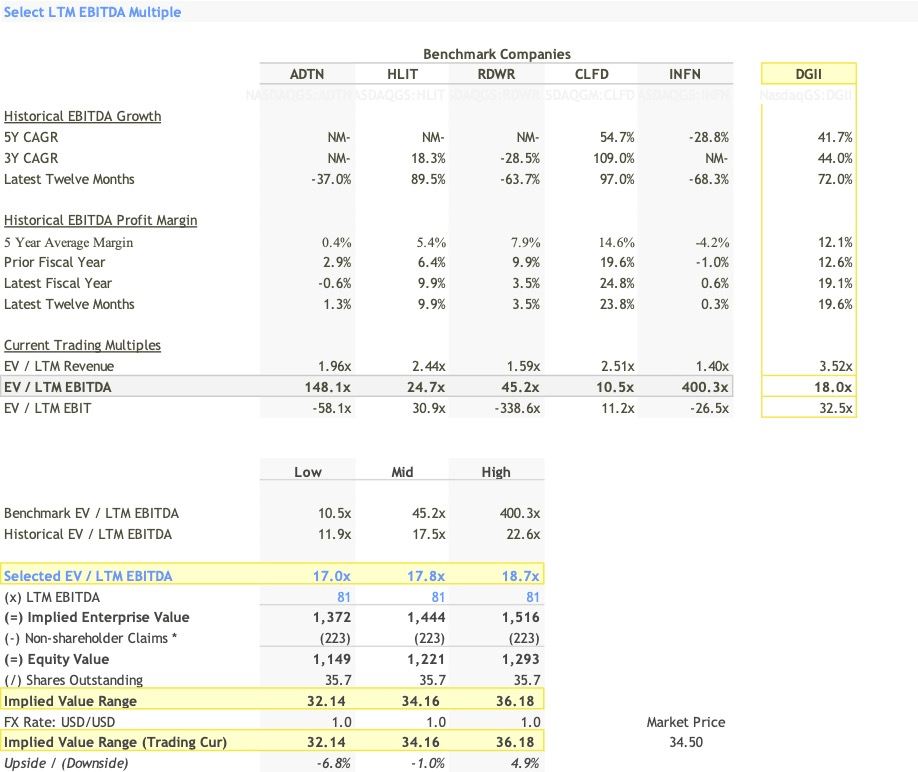

I calculate the implied value for Digi by taking the average of the median of the historical EV/EBITDA multiples and the median of its peer's EV/EBITDA multiples. I derive the selected multiple at 17.8x and $81 million LTM EBITDA; the implied price for Digi is $34.1 per share, which is slightly higher than the current trading price of $34.5 per share.

{kind=link}

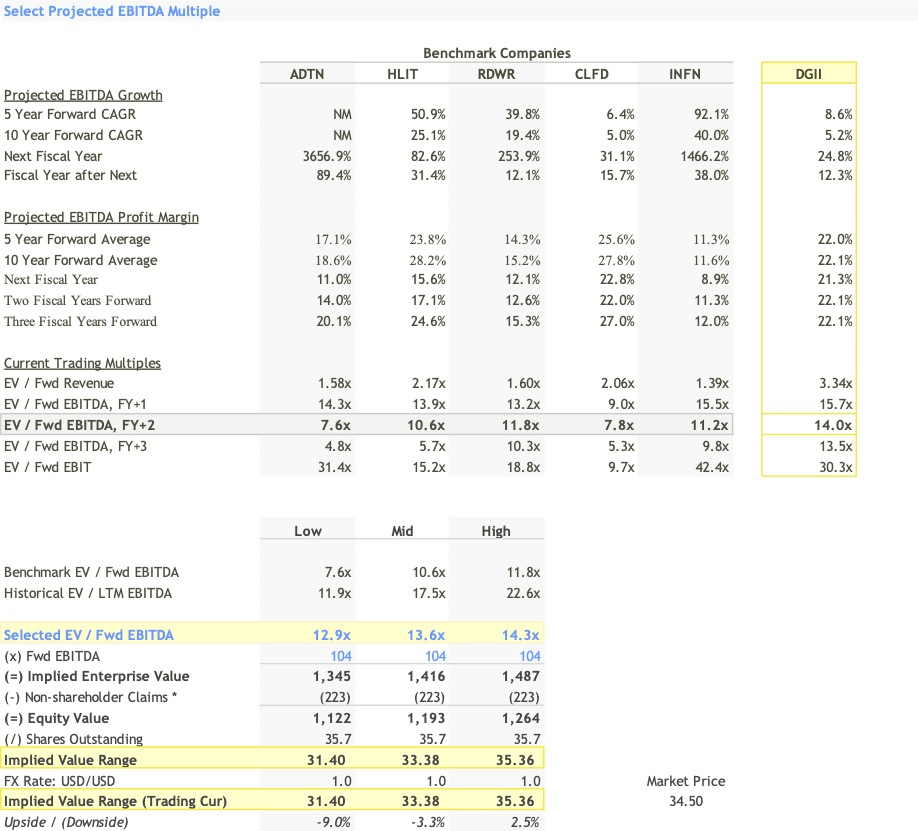

I assume Digi's EBITDA will grow by 24% next year due to the optimistic commentary from the management. Thus at the forward EBITDA of $104 million and taking the average of the forward EBITDA multiple of its peers and the historical EBITDA multiples of Digi, I use 13.6x as the selected EV/EBITDA multiple. At this multiple, the implied price is $33.38 per share, lower than the current $34.5.

Author Calculations

I average the implied price from LTM and forward EV/EBITDA multiple to arrive at a fair value of $33.7 per share. Thus, Digi looks overpriced at $33.77 per share against the $34.5, the current market price.

For the DCF valuation, I assume the following:

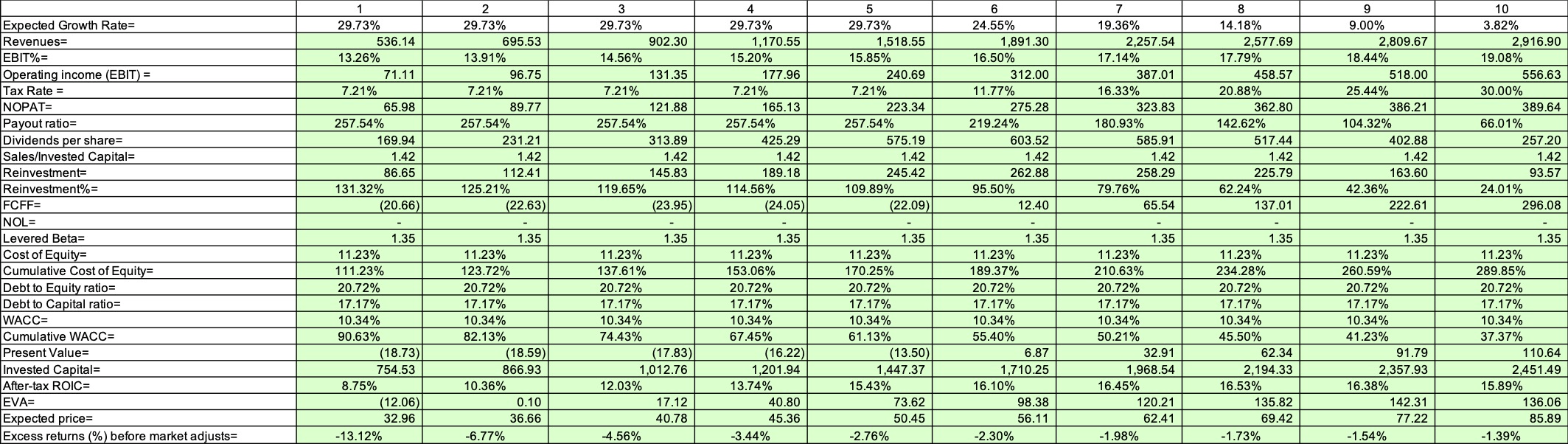

Digi's revenues will grow at 30% CAGR for the next five years and 18.4% CAGR for the next ten years.

I assume Digi's EBIT margin will improve from 11% and converge to an industry average of 19% in the terminal year.

I assume the Sales to invested capital at 1.42 to continue going forward.

Digi has $55.7 million in R&D expenses, which is included in the operating expenses. As R&D expenses yield future benefits, I have capitalized the R&D investments by amortizing the investments for three years.

| Year |

| R& D Expenses |

| -1 |

| 55.10 |

| -2 |

| 46.62 |

| -3 |

| 43.77 |

| Year |

| R&D Expense |

| Unamortized portion |

| Amortization this year |

| Current |

| 55.78 |

| 1.00 |

| 55.78 |

| -1 |

| 55.10 |

| 0.67 |

| 36.73 |

| 18.37 |

| -2 |

| 46.62 |

| 0.33 |

| 15.54 |

| 15.54 |

| Value of Research Asset = |

| 108.05 |

| Amortization of asset for the current year = |

| 48.50 |

| Adjustment to Operating Income = |

| 7.28 |

Digi's R&D expenses generate higher value; thus, I adjust the operating income by adding $7.2 million.

For the cost of capital, I assume the 10-year U.S. treasury bond of 3.8% as the risk-free rate.

I assume the US ERP of 5.49% is the equity risk premium.

I use the bottom-up beta of 1.18 as the unlevered beta, and at the debt-to-capital ratio of 17%, the levered beta is 1.35.

I derive the cost of equity at 11.23% and the cost of capital at 10.34%.

{kind=link}

| Estimating the value of growth |

| Value/Share |

| Value of assets in place = |

| 303.57 |

| 8.49 |

| Value of stable growth = |

| 62.77 |

| 1.76 |

| Value of extraordinary growth = |

| 915.64 |

| 25.62 |

| Value of the stock = |

| 1,281.97 |

| 35.87 |

On these assumptions, I derive the enterprise value of $1.28 billion at $35.87 per share.

Subtracting debt and adding cash, I get an equity value of $1.05 billion at $29.53 per share.

Thus, at this value, Digi looks overvalued.

I do a Monte Carlo simulation to understand at what percentile my DCF value lies. I assume revenue growth, target EBIT margin and Sales to Invested capital as the value drivers.

For simulation, I assume a truncated normal distribution for revenue growth for a high growth period of the next five years with a mean of 15%, a minimum of 8% and a maximum of 35% with a 35.6% standard deviation.

For the EBIT margin, I use a triangular distribution with a minimum of 5%, a mode at 19% and a maximum of 25%.

For Sales to invested capital, I use a uniform distribution between 1 and 2.

Then I do a bivariate analysis to understand the r-square between the equity value and the value drivers.

| Intrinsic equity value= |

| Revenue Growth= |

| Target Operating Margin= |

| Sales to Invested Capital= |

| Intrinsic equity value= |

| 1.0000 |

| 0.3794 |

| 0.4778 |

| 0.0485 |

| Revenue Growth= |

| 0.3794 |

| 1.0000 |

| 0.0002 |

| 0.0000 |

| Target Operating Margin= |

| 0.4778 |

| 0.0002 |

| 1.0000 |

| 0.0002 |

| Sales to Invested Capital= |

| 0.0485 |

| 0.0000 |

| 0.0002 |

| 1.0000 |

Thus, Digi's future value depends on revenue growth and the margin but is more sensitive to changes in the operating margin with an r-square of 48%.

Author Calculations

| Intrinsic equity value= |

| Revenue Growth= |

| Target Operating Margin= |

| Sales to Invested Capital= |

| Minimum |

| (10.65) |

| 7.93% |

| 4.81% |

| 1.00 |

| First Quartile |

| 8.40 |

| 14.39% |

| 13.39% |

| 1.25 |

| Median |

| 13.86 |

| 20.76% |

| 16.80% |

| 1.50 |

| Third Quartile |

| 21.78 |

| 27.78% |

| 19.54% |

| 1.75 |

| Maximum |

| 61.72 |

| 35.00% |

| 24.86% |

| 2.00 |

My DCF value of $29.5 per share lies between the 85th and 90th percentile.

I conclude my analysis that the fair value of Digi at $29.5 using DCF and $33.7 using comparables valuation looks overvalued and overpriced against the market price of $34.5 per share.

The market is attaching a premium to Digi for its ARR growth. For their solution segment, which requires a subscription to use, Digi's attach rate is 100%. However, the attach rate is currently less than 30% in Digi's products and services businesses. The company is increasing the attach rate by offering more bundled solutions, such as system process offerings, increased software content, and support services like 24/7 support, limited lifetime warranty, and device management capabilities. In addition, Digi has recently announced services such as connect core cloud and connect core security services designed to provide customers with more of the solution and get them to market more quickly. If Digi improves the attach rate to 100%, then it deserves the premium; however, if the attach rates decline, then there is a higher chance of stock price correction to happen.

For further details see:

Digi International: Strong Start To Fiscal Year 2023, But Hold Rating Stands