DMRC - Digimarc: Automatic Recognition Appears Undervalued.

2023-04-06 03:26:30 ET

Summary

- Digimarc Corporation has developed its business by providing watermark service for products of different types, thus offering the possibility of automatic recognition and identification.

- I believe that future sales growth will likely continue as many clients in new markets may not know the technology proposed by Digimarc.

- Taking into account the current size of Digimarc, I believe that there is significant room for expansion.

Digimarc Corporation ( DMRC ) already signed agreements with massive retail clients and central banks to provide automatic recognition and identification services. Considering the current market potential, new innovations, and more products, in my view, sales growth will likely continue for many years. Even assuming risks from slow technology adoption or failed introduction of products in international markets, future free cash flow would imply higher stock price marks.

Digimarc Corporation: Several Products And A Large Market Opportunity

Digimarc Corporation has developed its business providing watermark service for products of different types, thus offering the possibility of automatic recognition and identification. Such forms of identification are oriented to all kinds of digital objectives, ranging from music and video to product packaging or digital printing. Among these services there are three leading products, which include Digimarc Watermark, Digimarc Discover, and Digimarc Verify.

Source: Investor Presentation

The watermarks serve to make imperceptible identifications for the users to be able to replicate them on a long series of production of the same object. Digimarc Discover is a digital object recognition software, which is used for those working with the company's products and for all types of digital identifiers, universal codes, and other types of codes. Finally, Digimarc Verify is a series of tools within the same software that are used to measure the effectiveness of the watermark besides ensuring that it is well done.

The company offers its customers the possibility of authenticating their products as well as avoiding complications in this regard, facilitating the recycling of products, an easier way to track products in series, increasing the visibility of products through the brand of water, strengthening of digital security, and monitoring of retail sales operations.

Digimarc is still a young company that has taken advantage of the new market transformations to establish its business as a quality and security offer in terms of identification as well as digital security and product authenticity. In recent years, the company has achieved significant growth thanks to a large series of acquisitions, mainly in 2021. In my view, most investment advisors will appreciate that Digimarc counts with expertise in the M&A markets.

The company reports a single segment of operations that includes its sales to government channels and private companies. Mostly, the income comes from the sale of the software, the provision of services within the platform, and the subscription and the updates of the contracting terms. I believe that Digimarc is a good read not only because of its innovative portfolio of products, but because of the target market. The total market opportunity including plastic recycling, anti-counterfeit packaging, and digital packaging stands at close to $167 billion. Taking into account the current size of Digimarc, I believe that there is significant room for expansion.

Source: Investor Presentation

Digimarc is already working with many large clients, so it will likely not be difficult to find new customers outside the United States. In this regard, I believe that internationalization could be a serious revenue catalyst for Digimarc.

Source: Investor Presentation

The year 2022 presented a total revenue of $11.884 million together with a growth of 47%, and subscription revenue of $10.033 billion with a growth of 44%. Services were worth $1.851 million with a growth of 65%. I believe that future sales growth will likely continue as many clients in new markets may not know the technology proposed by Digimarc.

Source: Investor Presentation

Balance Sheet: The Total Amount Of Assets Increased Significantly Driven By Cash Increase And Inorganic Growth

The current state of the balance sheet is significantly better than that of 2021. Cash increased significantly along with the goodwill and intangible assets thanks to inorganic growth. Digimarc acquired EVRYTHNG, a London-based product cloud company, for close to $37 million, including intangibles worth $35 million and goodwill worth $7 million.

Source: Annual Report

As of December 31, 2022, the company reported cash of $33.598 million, marketable securities of $18.944 million, and receivable trade accounts of $5.427 million. Together with other current assets of $6.172 million, total current assets stand at $64.141 million. Current assets are close to six times the total amount of current liabilities, so I believe that liquidity does not seem a problem for Digimarc.

On the other hand, property and equipment stood at $2.390 million along with intangibles of $33.170 million and goodwill of $8.229 million. Additionally, with lease rights of use assets close to $4.720 million, total assets are equal to $113.777 million.

Source: Annual Report

The liabilities included accounts payable and other accrued liabilities of $5.989 million, deferred revenue of $4.145 million, and total current liabilities of $10.134 million. Besides, long term lease liabilities were equal to $5.977 million with total liabilities close to $16.187 million. In my view, with an asset/liability ratio of more than 6x-7x, the balance sheet appears solid.

Source: Annual Report

Assumptions Behind My DCF Model Include New Patents, Know-how, And More Services And Products

I am optimistic about further developments and investments in services for government central banks and services for retail businesses. Considering the target market, I believe that new products or services will likely lead to FCF growth. Besides, in my view, an expansion in the portfolio of intellectual property, which is undoubtedly one of the great values ??of the company, may also lead to more brand recognition. New clients may also appreciate the new know-how acquired, which may lead to revenue generation. I also believe that many large retail clients could knock at the door of Digimarc. Walmart ( WMT ) recently signed an agreement with Digimarc. In my view, as soon as other large retailers have a look at the agreement signed by WMT, they will likely be interested in the technologies offered by Digimarc.

In December 2022, Digimarc announced an additional multi-year agreement with Walmart to help further optimize store operations. The agreement covers an expanded deployment of Digimarc Illuminate Platform capabilities beyond the scope of the existing agreement between the two companies. Source: Annual Report

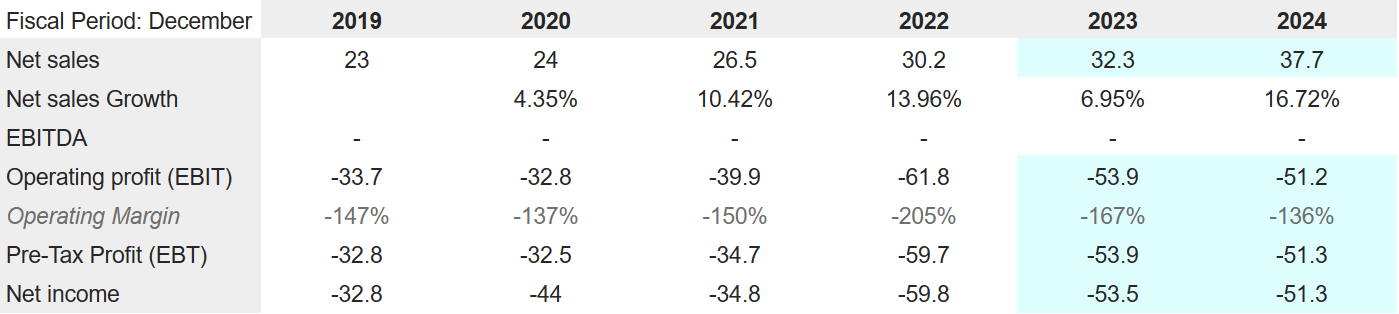

Analysts Expect Double Digit Sales Growth In 2024, And My DCF Model Indicated Significant Upside Potential

Analysts foresee 2024 net sales of $37.7 million and 2024 net sales growth of 16.72%. The operating profit would stand at -$51.2 million with a net income of -$51.3 million.

{kind=link}

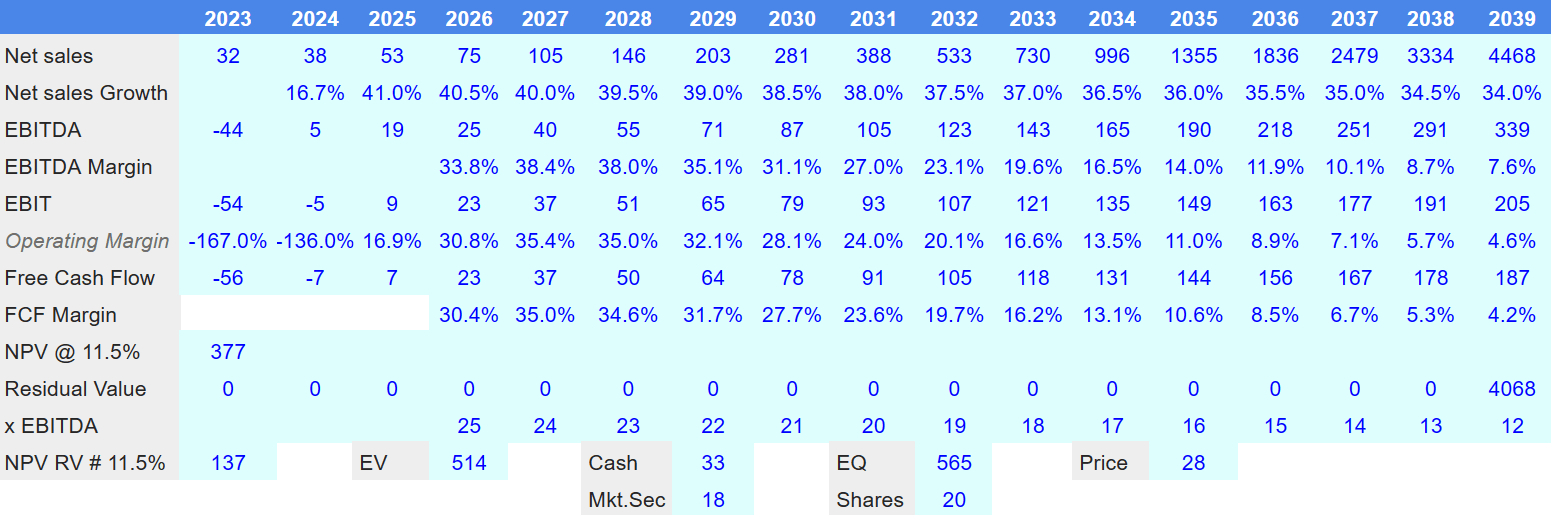

Considering the current sales growth, I believe that using a DCF model from 2023 to 2039 makes a lot of sense. My numbers include 2039 net sales of $4.468 billion with net sales growth of 34%. 2039 EBITDA would stand at $339 million with an EBITDA margin of 7.6%, EBIT of $205 million, and an operating margin of 4.6%.

2039 free cash flow would stand at close to $187 million with a FCF margin of 4.2%. If we assume a conservative EV/EBITDA multiple of 12x and a WACC of 11.5%, my results would include an enterprise value of $514 million. Besides, with cash of $33 million and market securities of $18 million, the implied equity would be close to $565 million. Finally, the fair price would be close to $28 per share.

{kind=link}

There Are Not Many Competitors, But Technology May Be Adopted Slowly

I believe that there are not many companies doing exactly what Digimarc does. Competition varies by service portion, and comes mainly from traditional forms of identification such as barcodes, fingerprint recognition, or pattern identification. I believe that Digimarc has an advantage in terms of its technology offer and low cost. Taking into account the rate of adaptation of certain markets to this technology, shareholders may have to wait some years to see abundant net sales.

Risks

In relation to the risks, we can first point out that Digimarc presents a lack of client diversification. Only 5 of its clients accounted for a significant part of the annual revenue. In addition, most of the revenue comes from contracts with government agencies, which will end in 2029. If management cannot renew its contracts with the Central Banks, revenue growth will likely not increase.

Historically, we have derived a significant portion of our revenue from a limited number of customers. Five customers represented approximately 72% of our revenue for the year ended December 31, 2022. Source: Annual Report

Nearly half of our revenue came from our contract with the Central Banks in 2022. That contract was recently extended and now expires at the end of 2029. The customer contracts we enter into may contain termination for convenience provisions. Source: Annual Report

Digimarc has to respect a significant number of regulations not only in the United States, but also international laws that may also change in the future. If Digimarc requires to invest a lot of dollars to comply with regulations, profitability may decline, which would bring the fair value down.

If we fail to comply with the many international laws and regulations to which we may be subject, we may be subject to significant fines, penalties, or liabilities for noncompliance. These factors may result in greater risk of performance problems or of reduced profitability with respect to our international programs in these markets. Source: Annual Report

My Takeaway

Digimarc offers innovative technology and a massive target market. Large clients like central banks and large retailers already signed agreements to use the services offered. In my view, further innovative products and technologies, more clients, and internationalization will likely lead to FCF generation. Besides, considering that management counts with expertise in the M&A markets, I believe that inorganic growth could enhance future revenue growth too. There are obvious risks from the fact that the business is still small, and technology adoption could be slow, however I believe that the company could trade at higher marks.

For further details see:

Digimarc: Automatic Recognition Appears Undervalued.