O - Digital Realty: Solid Growth But Priced In

2023-11-21 18:46:07 ET

Summary

- Data centers are experiencing high demand as companies invest in AI capabilities, benefiting Digital Realty Trust, Inc. with higher rent and strong returns on capital.

- Same-store NOI growth has returned to data centers.

- Digital Realty Trust is financing developments through partnerships, allowing them to leverage their expertise and generate outsized returns with minimal capital investment.

Data centers are the hot sector right now, with demand exploding as companies ramp up their artificial intelligence ("AI") capabilities. Digital Realty Trust, Inc. ( DLR ) is one of the main beneficiaries, as it gets to charge higher rent on existing facilities as well as generate strong return on capital in developing additional facilities. This article will explore the following concepts:

- Same-store NOI growth has returned to data centers

- How DLR is making developments work in the tight capital environment

- Potential for oversupply

- Valuation and opportunity.

Same-Store NOI

Data centers have significantly different fundamentals than other kinds of real estate because their tenants are also competitors.

A direct data center real estate investment trust ("REIT") peer, Equinix (EQIX), is DLR’s 6 th largest tenant.

{kind=link}

Beyond the direct peer, most of these tenants also are capable of building and running their own data centers.

It creates an elevated level of competition as tenants just about always have a choice which puts the data center in a somewhat precarious position when leases expire. They have to price a renewal lease in such a way that the tenant will choose to stay rather than just building their own facility.

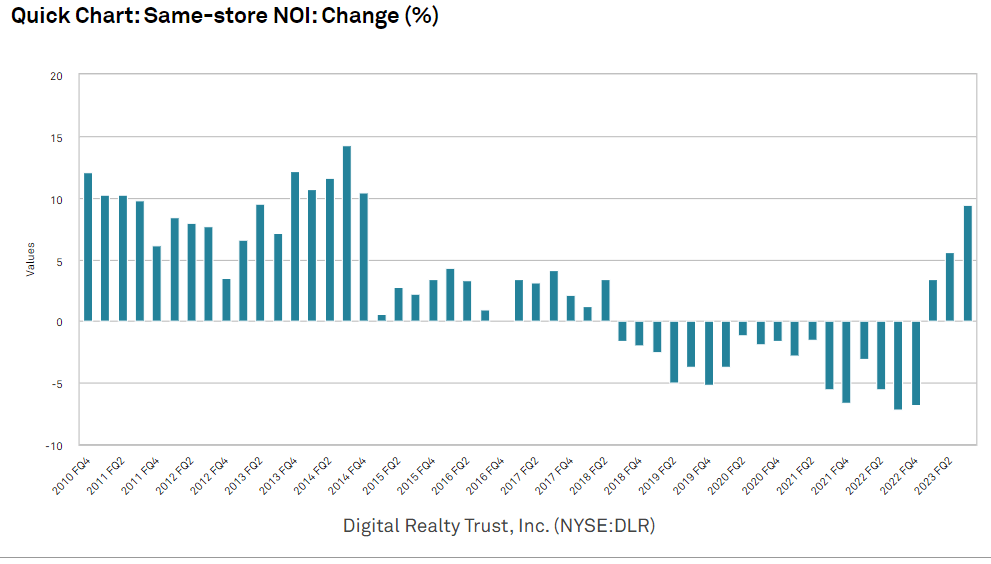

This really hurt data centers in 2021 and 2022, when many of the cloud companies were opting to build their own data centers, and it shows up in the numbers.

{kind=link}

For a few years, renewal rates were actually below expiring lease rates.

Much of that can be attributed to the zero interest rate environment. When money was nearly free, someone like a Google (GOOG) or Microsoft (MSFT) would be quite willing to spend the capital to build their own facility.

Today, money has a cost again and companies are getting more hesitant to build their own. This has restored pricing power to the data center REITs allowing DLR to raise rents on renewals. Same-store NOI in Q3 2023 came in around 9%, the highest it has been in nearly a decade.

There are 2 main sources of strong organic growth:

- The aforementioned capital constrained environment

- Rapid demand growth due to AI craze.

I anticipate same-store NOI to remain strong for the next couple years, assuming AI remains a popular investment allocation for companies.

Beyond organic growth, DLR has significant growth potential through development.

Data center development

I tend to view data centers as somewhat commodity-type buildings. It takes a certain degree of expertise to build a proper facility, but once a company has that blueprint, they can replicate it any number of times.

At times, rampant development has resulted in oversupply and because of the cookie cutter nature, such oversupply is likely to be cyclical in nature. Presently, however, demand drivers are strong enough that most developments are being well absorbed.

Development comes down to 3 aspects:

- Expertise in data center

- Expertise and relationships to facilitate lease-up

- Large amounts of capital.

As a massive data center REIT, Digital Realty meets the first 2 requirements with ease. The third is a bit harder today.

DLR’s balance sheet is fine, and they do have access to capital if they need it, but capital is expensive right now, which cuts into development spreads.

How DLR is financing developments in capital constrained environment

Those who follow my work know that I am often opposed to joint ventures. It adds complexity and administrative burden as well as opacity to earnings. Thus, joint ventures done for no reason are value destroying.

In the case of DLR, however, I think they have hit upon something quite interesting with their partnerships.

To a well-capitalized entity that lacks the expertise to develop their own data center, DLR’s expertise is quite valuable.

The non-data center party can contribute the majority of the capital while DLR contributes the development and lease-up expertise resulting in a win-win situation.

- The partner who would normally not have access to data center exposure gets to invest in the hot sector

- DLR gets an outsized return with minimal capital investment.

So how does this work?

Digital Realty builds a facility just as they normally would, and upon stabilizing it with tenancy sells the majority to a JV partner. Since DLR has already gotten past the development and lease up risk, these sale cap rates are really low.

So far, there was a $900 million deal with GI Partners at a 6.5% cap rate and a $1.5B deal with RPG Real Estate at a 6.0% cap rate.

{kind=link}

Note that DLR is developing at a double-digit cap rate, so their development spread over exit cap rate is around 400 basis points making the round trip very profitable.

DLR’s double-digit development yields were twice reference on the Q3 2023 conference call .

Jordan Sadler (SVP):

“The capital that we've raised this year has enabled us to increase our liquidity and delever while expanding our investment in development that we expect to generate double-digit unlevered returns.”

Andrew Power ((CEO)):

“So I think I'd point you to our development schedule, which has now been in the double digits category across the board for the whole portfolio, including an increase in, call it, 65 megawatts quarter-over-quarter. North America, where, I would say, is the current home to the largest deals is in double digit by itself and has moved up dramatically.”

It creates a sort of engine that DLR can just rinse and repeat.

- Develop a property at high cap rate

- Stabilize it

- Sell it at low cap rate

- Net the difference while retaining partial ownership of the property.

Realty Income ( O ) has joined the fray as a joint venture partner. Here is the description of the deal from the press release:

“The two build-to-suit data centers commenced construction in the fourth quarter of 2022 and are slated to deliver 16 megawatts ((MW)) of initial data center capacity, which is expandable up to 48MW at the client's option. The budget for the first phase of these yield-on-cost developments is approximately $400 million. The client maintains the option to expand the projects up to 48MW of total capacity during the initial lease term, which could increase the budget up to $800 million, based on current development cost estimates.”

O is going to get a 10 year triple net lease on the data center at a 6.9% cap rate. That works for O. It is accretive and diversifies them into what might be a nice growth sector.

It works even better for DLR who likely developed these properties at a much higher cap rate.

How long will the opportunity last

I think DLR can rinse and repeat their growth engine as long as those with capital remain excited about AI build-out and data centers don’t become too oversupplied.

The exact duration is unknown. I would guess 1-3 years.

Valuation

Digital Realty is among few options for investing in data center REITs. The other main choices would be Equinix and Iron Mountain ( IRM ), so I will summarize their valuations briefly before getting to DLR.

I have in the past been very bullish on IRM, but it has become a bit pricey. I still like it and am still slightly long, but it is much closer to fair value now.

EQIX is premium quality and also trades at a premium valuation.

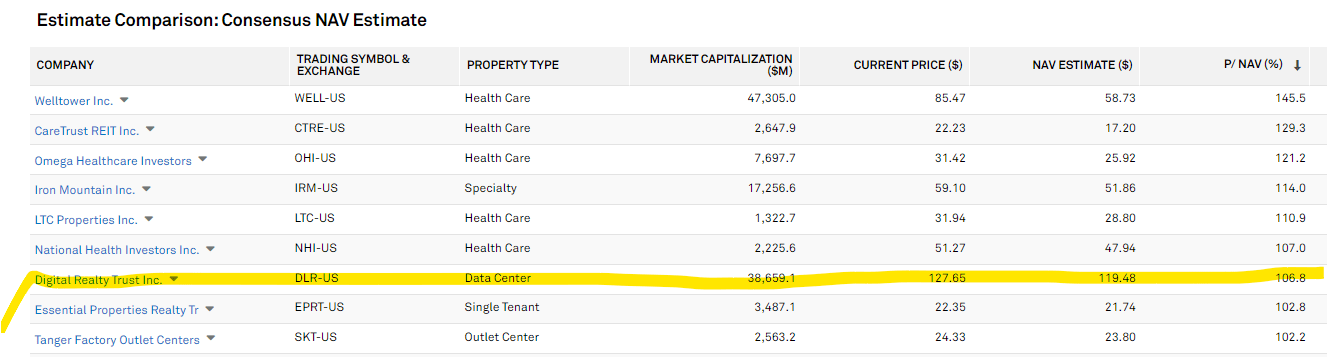

Digital Realty is also rather expensive. It is one of only a handful of REITs that trades at a premium to net asset value.

{kind=link}

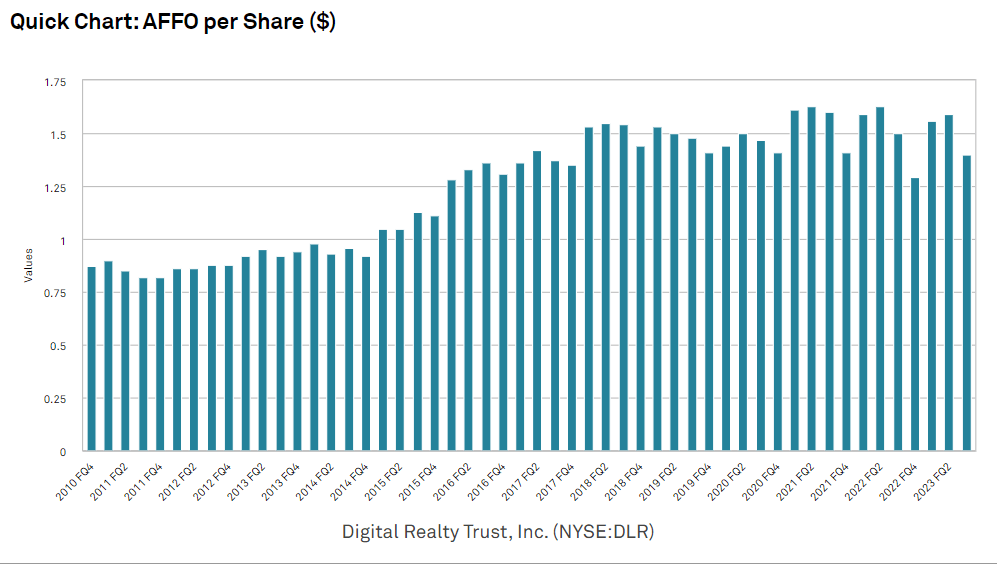

A forward adjusted funds from operations ("AFFO") multiple of 20X is also rather high compared to the median REIT at 12.5X AFFO.

In my opinion, DLR’s premium is somewhat justified, as it does have nice growth prospects such as the engine discussed earlier. AFFO/share growth tends to come in bursts and given the strong recovery in same-store NOI growth, DLR could be headed for a burst of AFFO/share growth similar to the 2013-2017 era.

{kind=link}

News flow has been quite positive, with a demand surge resulting in twice increased rental rate guidance.

{kind=link}

I think the higher rental rates are sustainable for the medium term.

The Hold Thesis

Overall, Digital Realty is fundamentally well positioned, with a recently improved balance sheet and healthy growth prospects. However, all the strength seems to already be priced in with a multiple that far exceeds the REIT index.

A 20X AFFO multiple would only be opportunistic if growth were truly secular in nature, but given how susceptible the sector is to oversupply, I think it will always be cyclical. Therefore, I think Digital Realty Trust, Inc. is an okay investment, but I wouldn’t expect too much upside from its already high price.

For further details see:

Digital Realty: Solid Growth, But Priced In