DBRG - DigitalBridge: Cheap Compounder With A Clear Catalyst

2023-04-24 14:25:28 ET

Summary

- DigitalBridge is cheap, with a clear catalyst to unlock the value.

- Asset-light digital infrastructure manager disguised as an asset-heavy data center owner.

- 60%+ upside to the conservative sum of the parts valuation.

- One of the most interesting value plays at the moment.

This is an interesting opportunity to own a high-quality business at a substantial discount to its intrinsic value. Given secular industry tailwinds, the company is poised to generate a rapidly growing stream of long-term recurring revenues in the upcoming years. The market is currently ascribing little value to the company’s projected earnings power. However, I expect a near-term business structure simplification to lead to a substantial share price re-rate.

DigitalBridge Group ( DBRG ) is a $2bn market cap alternative asset manager focused on digital infrastructure assets, such as data centers, cell towers, and fiber networks. DBRG generates recurring and growing revenues from asset management fees on its AUM. The company also holds ownership stakes in two data center operators Vantage SDC (13%) and DataBank (11%). Currently, DBRG presents one of the most compelling investment opportunities available in the market. There is over 60% upside to the conservatively estimated sum-of-the-parts valuation. Fortunately, there is a short-term catalyst here. This year, the company expects to divest its non-core ownership stakes in Vantage SDC and DataBank. The move will allow DBRG to deconsolidate these businesses from its books.

This will likely lead to a substantial share price re-rate for a couple of reasons:

- After the divestitures, DBRG will appear as a much leaner entity as most of the company’s currently reported debt will simply disappear from the financial statements. Currently, DBRG screens as an asset-heavy overleveraged data center owner and operator.

- The move will shine the light on the company’s asset management business which generates high-margin and stable long-term recurring revenues. Most of DBRG’s managed assets are locked into long-duration funds (10+ years), allowing for high visibility into and stability of future revenue streams. Deconsolidation will put the company alongside much higher-valued peers such as Blackstone ( BX ) and KKR ( KKR ).

On top of that, DBRG’s focus on digital infrastructure provides a decent margin of safety in a potential recession given the industry’s secular tailwinds and relatively low sensitivity to macroeconomic downturns. Confidence in the fundraising environment of the broader infrastructure space is highlighted by the recently performed or announced infrastructure-focused capital raises from large alternative asset managers, such as Ares Management ( ARES ) and KKR.

My write-up is structured as follows:

- Overview of DBRG’s business and recent operational performance.

- Projected future performance of the core asset management business. The financials are largely based on management’s guidance so I also review the management’s credibility and track record to date.

- Recent strategic transformation and the planned divestiture of Vantage and DataBank’s stakes which I expect to be a major catalyst for the stock.

- Sum-of-the-parts valuation.

- Involvement of the activist investor Legion Partners.

- Digital infrastructure industry outlook, including secular tailwinds as well as recession-proof characteristics of digital infrastructure asset managers.

- Infrastructure sector’s fundraising outlook.

DigitalBridge

DBRG operates two segments which are discussed below.

Investment Management- This is a private equity funds’ management business focused on digital infrastructure assets. DBRG raises funds from third parties and the capital is subsequently deployed into the acquisitions and/or development of digital infrastructure assets, such as data centers, cell towers, and fiber networks, which are then managed by DBRG. As an investment adviser and general partner of its funds, DBRG receives a management fee which comes as a percentage of assets or fee-earning equity under management (FEEUM). DBRG’s annual management fee ranges from 0.2% to 1.5% of FEEUM. The weighted average fee rate stands at 0.9%. Importantly, Investment Management’s fee revenues are recurring, predictable and stable. DBRG’s funds generally have a long duration, with an average fund life of over 10 years. More than 80% of the counterparties are investment-grade, such as large technology companies which lease data centers owned by DBRG funds. Aside from management fees, DBRG is entitled to receive incentive (performance) fees when a given fund’s performance exceeds a certain threshold.

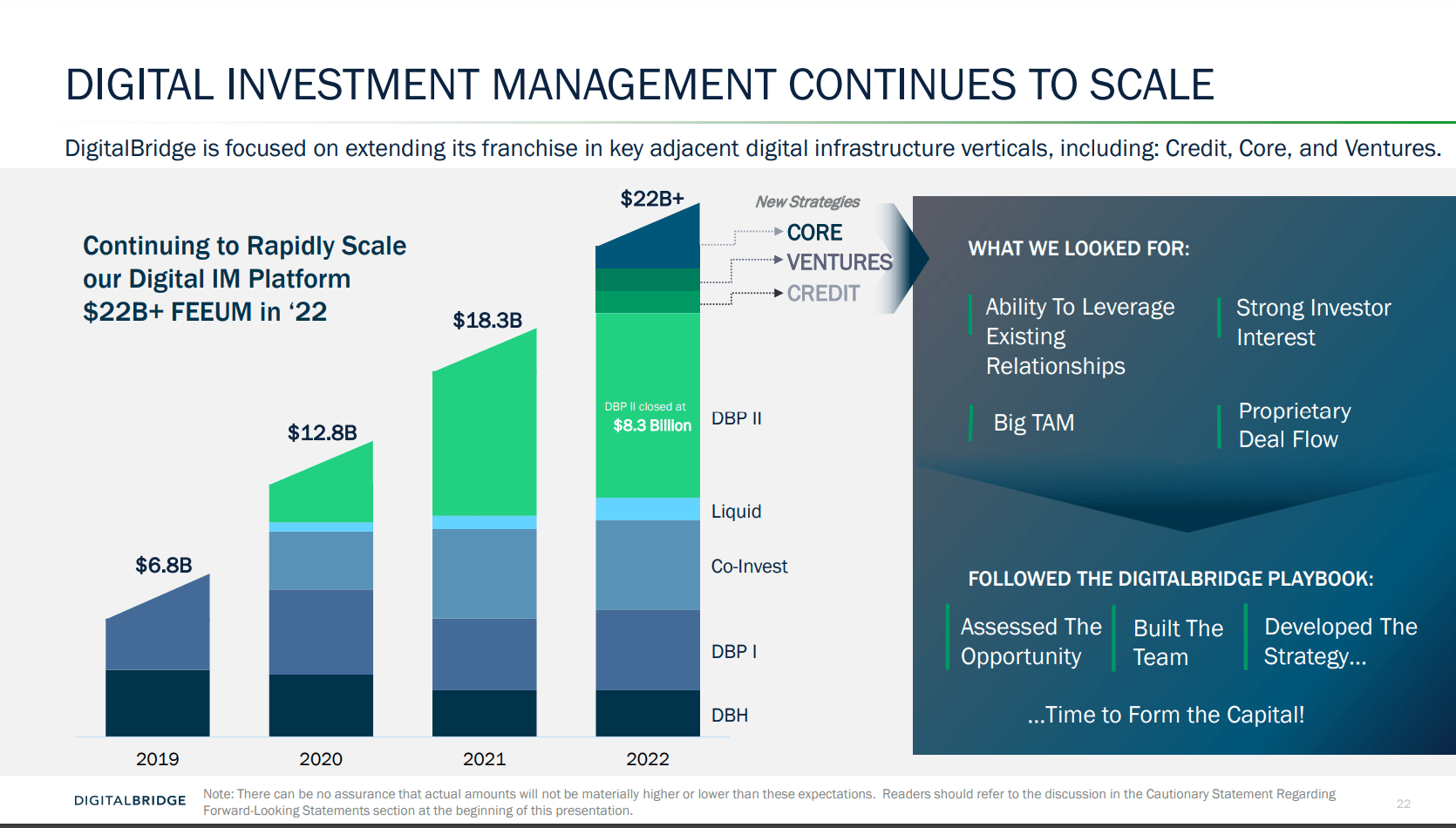

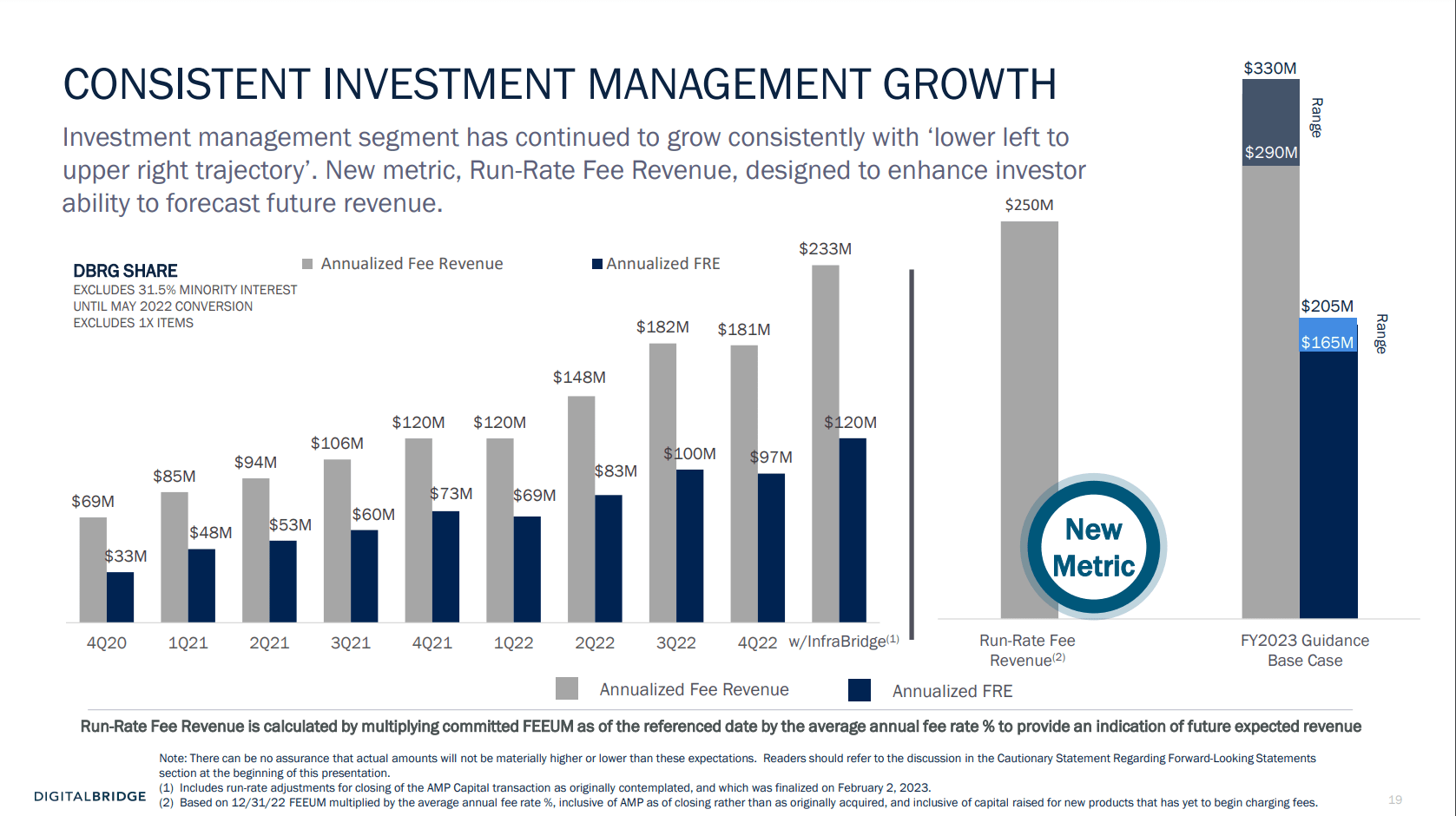

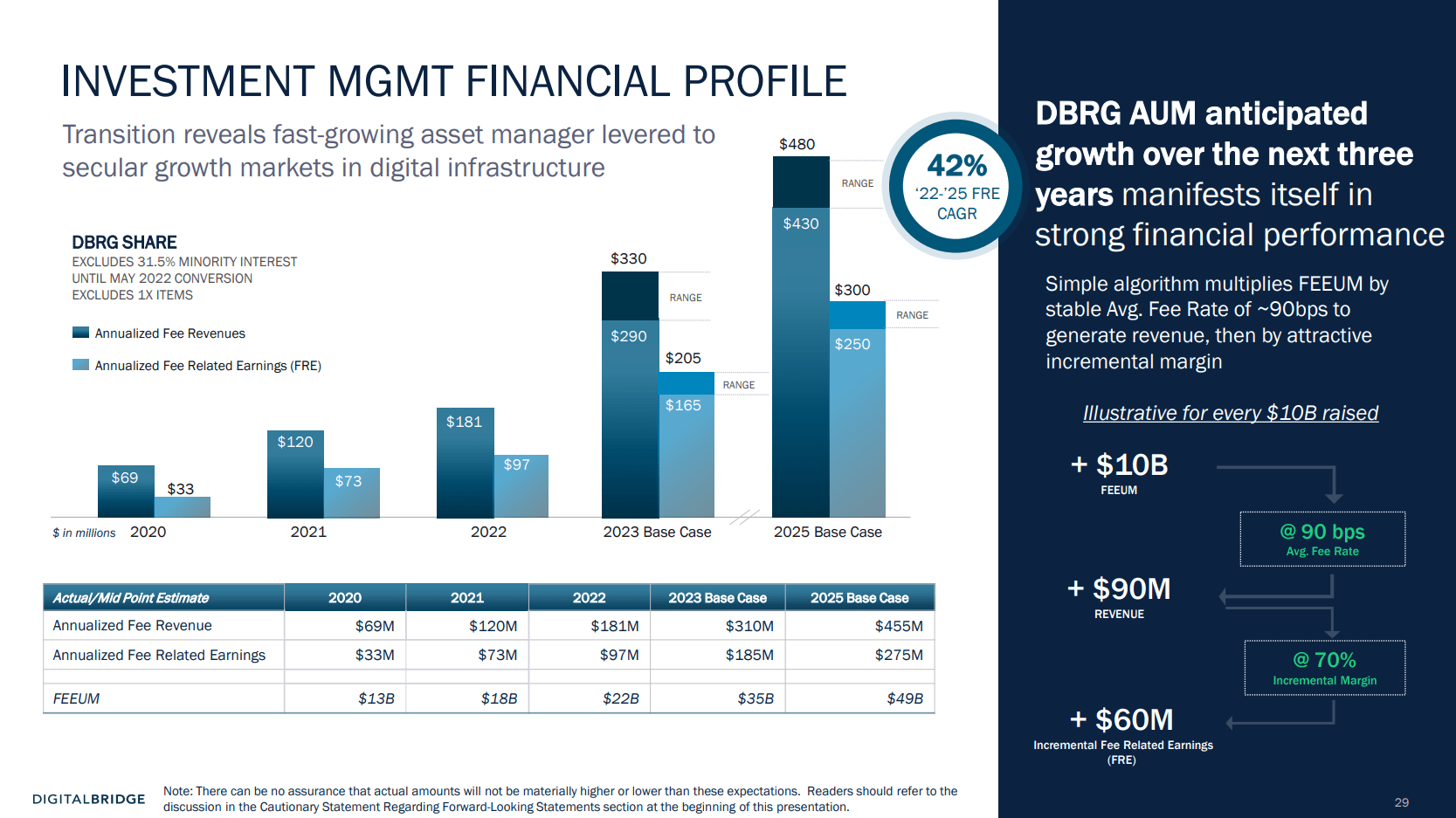

DBRG’s Investment Management has been a successful growth story, with the segment’s fee-earning equity under management (FEEUM) expanding rapidly in recent years. FEEUM has grown from $7bn in 2019 to $22bn as of December ’22 or a 48% CAGR. This has been driven by the launch of new funds, including the second flagship fund DBP II which closed its funding in January ’22 at an $8bn mark. The growth has also been spurred by acquisitions, including Switch (completed in December ’22). The latest large acquisition of InfraBridge (completed in February) has added over $5bn in FEEUM, bringing the total to $28bn as of February ’23. FRE, which is directly dependent on fee revenues (and, in turn, FEEUM), jumped from $39m in 2020 to $84m in 2022.

{kind=link}

DigitalBridge Q4'21 Earnings Presentation

{kind=link}

DigitalBridge Q4'22 Earnings Presentation

FEEUM expansion has been reinforced by the solid performance of DBRG’s funds comprised of the tower, data center, fiber, and small cells/edge assets. Monthly recurring revenue from the tower asset portfolio grew at 26% and 20% in Q3’22 and Q4’22 year-over-year whereas recurring revenue generated by data center assets expanded by 34% and 10%. Recurring revenue growth rates for fiber and small cells/edge portfolios in Q3’22/Q4’22 stood at 5%/6% and 28%/9% respectively.

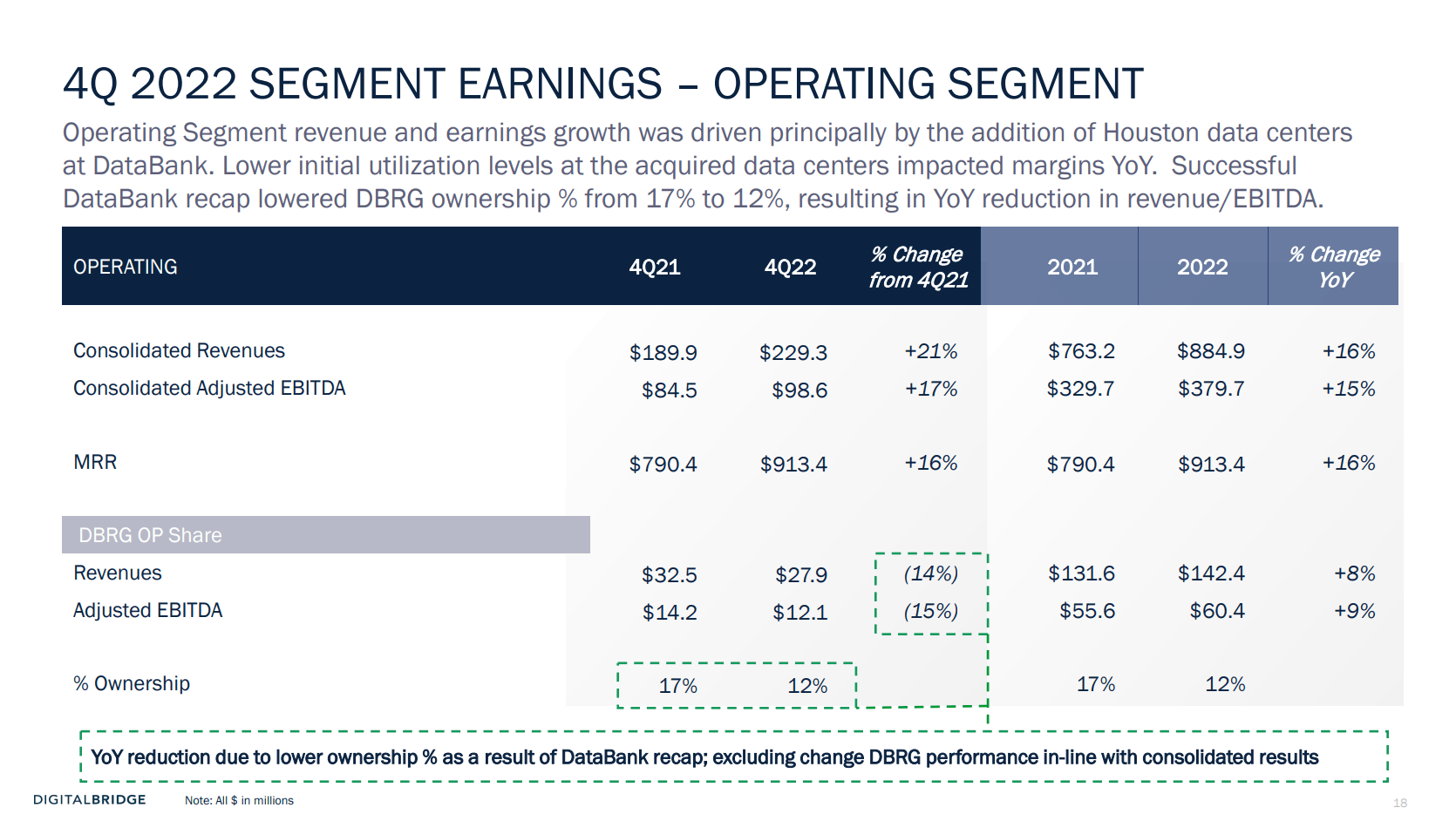

Operating- This segment comprises DBRG’s minority stakes in two data center operators - Vantage SDC (13%) and DataBank (11%). As opposed to the investment management business, these are balance sheet investments where DBRG has invested its own capital. The segment generates rental income from owned properties.

The performance of the Operating segment has been more stagnant vs the Investment Management segment though it still displayed growth in recent years. The segment generated $142m in 2022 revenues vs $132m in 2021 (DBRG’s share) as Vantage SDC and DataBank continued to scoop up and/or develop data center assets. Adjusted EBITDA likewise jumped slightly from $56m in 2021 to $60m in 2022.

{kind=link}

DigitalBridge Q4'22 Earnings Presentation

Projected Growth and Management’s Track Record

DBRG’s management expects the core investment management business to continue growing rapidly in all key metrics driven by the launch of new funds (including DBRG’s third flagship fund), capital raises in existing vehicles (Core and Credit strategies), and potential M&A activity. The company expects the business to generate $165m-$205m in 2023 FRE, with $35bn in AUM. Management has been confident about reaching its targets - several quotes from the company's leadership are below.

CFO during a conference call in March ’23:

If you look at 2022, we raised almost $5 billion last year, and that was without any of our flagship type of strategies out there in the market. So this year, what we've guided the street is an $8 billion to $12 billion fundraising haul in 2023. We feel good about being able to get $8-plus billion this year. And that's because in our conversations with limited partners, they're happy with our performance. They like the fact that we actually return capital back to them last year. We had 3 amazing exits, Wildstone digital, which was digital billboards. We had DataBank and we had Vantage Towers last year. So really good exits last year that demonstrated to them our track record, demonstrated to them that we get them good returns. And as a result, they're rewarding us with a check back.

CEO during a conference call in February ’23:

So on the ability to raise capital, as I said before, pro forma today, we're at about 20 -- call it, $23 billion, $28 billion of FEEUM today, post the InfraBridge acquisition and plus a little bit of fundraising here in the first quarter, which we'll update in the next quarter. Then if you take the guidance that we put out earlier on Friday, we said, look, we're going to raise $8 billion plus of new capital. Where does that come from? Once again, we're very prescriptive. We said there's another $2 billion raise in terms of credit and core. There's another $2 billion in co-invest, which we've already raised some of that this year. We've had a rich history of exceeding co-invest capital and then in our sort of what we call our core strategy, the launch of a third strategy in our flagship line.

Targets for 2025 stand at $49bn in FEEUM with $275m in FRE. The company expects the incremental FRE margins to reach 70% (vs 59% recorded in 2022) due to the existing operational leverage.

{kind=link}

DigitalBridge Q4'22 Earnings Presentation

What gives me confidence in management’s guidance is its reputation and track record so far. Since the management transition, CEO Marc Ganzi ’s team has delivered on several fronts:

- Substantially all legacy non-digital infrastructure assets have been disposed of. During 2018-2021, DBRG rotated $78bn in assets or nearly 100% of its legacy AUM. Correspondingly, digital infrastructure AUM soared from $14bn in 2019 to over $65bn currently (this includes ownership stakes in DataBank and Vantage SDC).

- The company is on track to exceed long-term FRE targets set out back in 2020. At the time, DBRG’s management targeted $80m-$110m in 2023 FRE compared to the current guidance of $165m-$205m. Moreover, DBRG raised $4.8bn in FEEUM in 2022 which was 26% above the company’s guidance midpoint.

The CEO seems to have a reputable background. Prior to co-founding DigitalBridge, Ganzi was the founder of Global Tower Partners - a cell tower company that received financial backing from Blackstone and was eventually sold to AMT for $4.8bn.

Importantly, the CEO is incentivized - he is set to receive a massive $100m payout if DBRG’s share price reaches $40 by mid-2024.

Catalyst

DBRG has undergone a major transformation since mid-2020 when Marc Ganzi took over the wheel of the company. Under Ganzi’s leadership, the company sold off its legacy real estate, including hospitality, healthcare, and other properties. Meanwhile, DBRG has continued to scoop up digital infrastructure assets through third-party capital while selling down/recapitalizing owned assets. The company has performed a number of transactions aimed at streamlining the company’s structure, including acquiring full ownership of its IM business from one of its shareholders (Wafra). In February ’22, DBRG shifted its incorporation from a REIT to a C-Corp.

Currently, however, the company’s financial reports are still convoluted as it has to consolidate Vantage SDC and DataBank businesses. DBRG's management has stated that the consolidation of these businesses is required as the company’s ownership stake exceeds 10% and it controls board seats in both Vantage SDC and DataBank. Several aspects illustrate the impact of the current consolidation:

- As of December ’22, DBRG reported $5.1bn in debt on its balance sheet. Meanwhile, DBRG’s corporate debt and its share of investment-level debt stood at a much smaller $1.3bn.

- In 2022, DBRG visually generated the majority of its revenues from property operating income - 81% of total sales. Meanwhile, on an unconsolidated basis, DBRG’s revenue split between the Operating and Investment Management segments stood at 48%/52%. Note that the Operating segment has displayed lower adjusted EBITDA margins in 2021-2022 at 42% vs 55-59% FRE margins of the Investment Management business.

- On a net income level, the fully consolidated Operating segment generated a loss of $330m in 2022 ($231m in 2021) compared to a total net loss of $421m ($217m). However, DBRG’s share of the Operating segment’s net loss stood at only $53m ($37m).

In other words, in its current form, the company appears to be an asset-heavy, overleveraged, and highly unprofitable business. Meanwhile, DBRG is already a primarily asset management business generating high-margin recurring fee revenues. DBRG’s CFO put it well during a recent conference call:

So we've got 2 businesses on the balance sheet. We have a digital operating segment. So it is still digital infrastructure. But because we own 13% of Vantage stabilized data centers on our balance sheet and because we own 11% of DataBank on our balance sheet, anything over 10% from an accounting perspective and the fact that we have control, that combination required us to consolidate those 2 businesses that we own 100% of it on our income statement and balance sheet. So on our books, it looks like these things are -- we are a big, big, big data center business. People look at our books, and they don't even realize we're actually really a private equity business.

The company has continuously noted its intentions to sell down its stakes in DataBank and Vantage SDC to below 10% in order to deconsolidate them. During the Q4’22 conference call , the CEO highlighted that divestitures and deconsolidation of non-core assets are likely to be completed this year:

We've got teams in place right now that are talking to investors on both assets. I think DataBank sort of comes first. Vantage SDC comes second. We're committed to deconsolidating both of those assets this year. I've given you a June 30 timeline on the DataBank fundraising.

It's worth noting that DataBank was already partially monetized in H2’22 whereby DBRG’s stake was reduced from 22% to 13% (delivering $318 in proceeds). In March ’23, media reports appeared that DBRG is considering a sale of its minority stake in Vantage SDC.

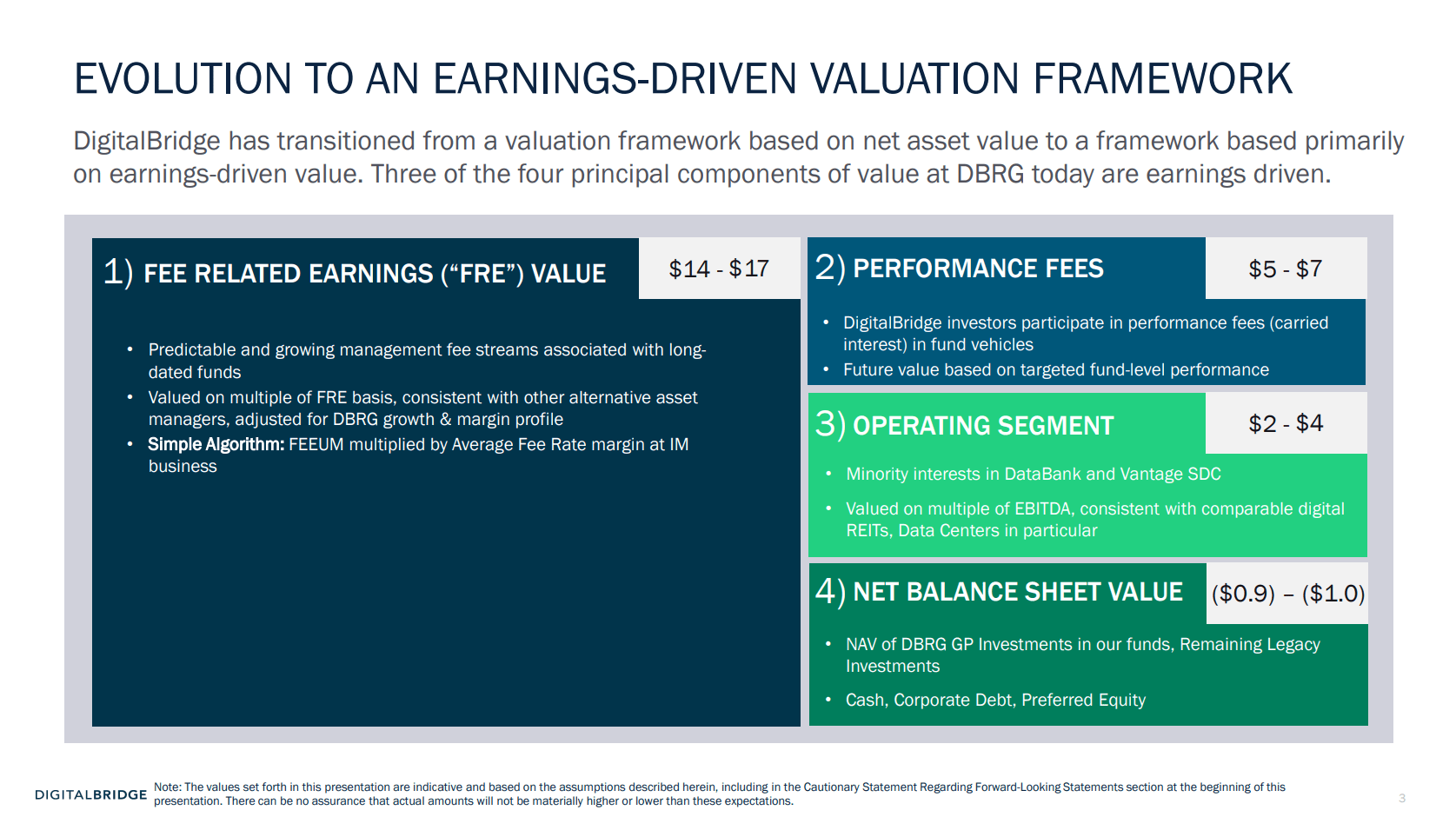

Valuation

I believe DBRG’s valuation is where it gets the most interesting. Management’s conservative SOTP valuation implies a price target of $20/share or a 66% upside. Meanwhile, the upper valuation range of $27/share is over 120% above current share price levels. A breakdown of management’s SOTP valuation assumptions is provided below.

{kind=link}

DigitalBridge Investor Presentation, April 2023

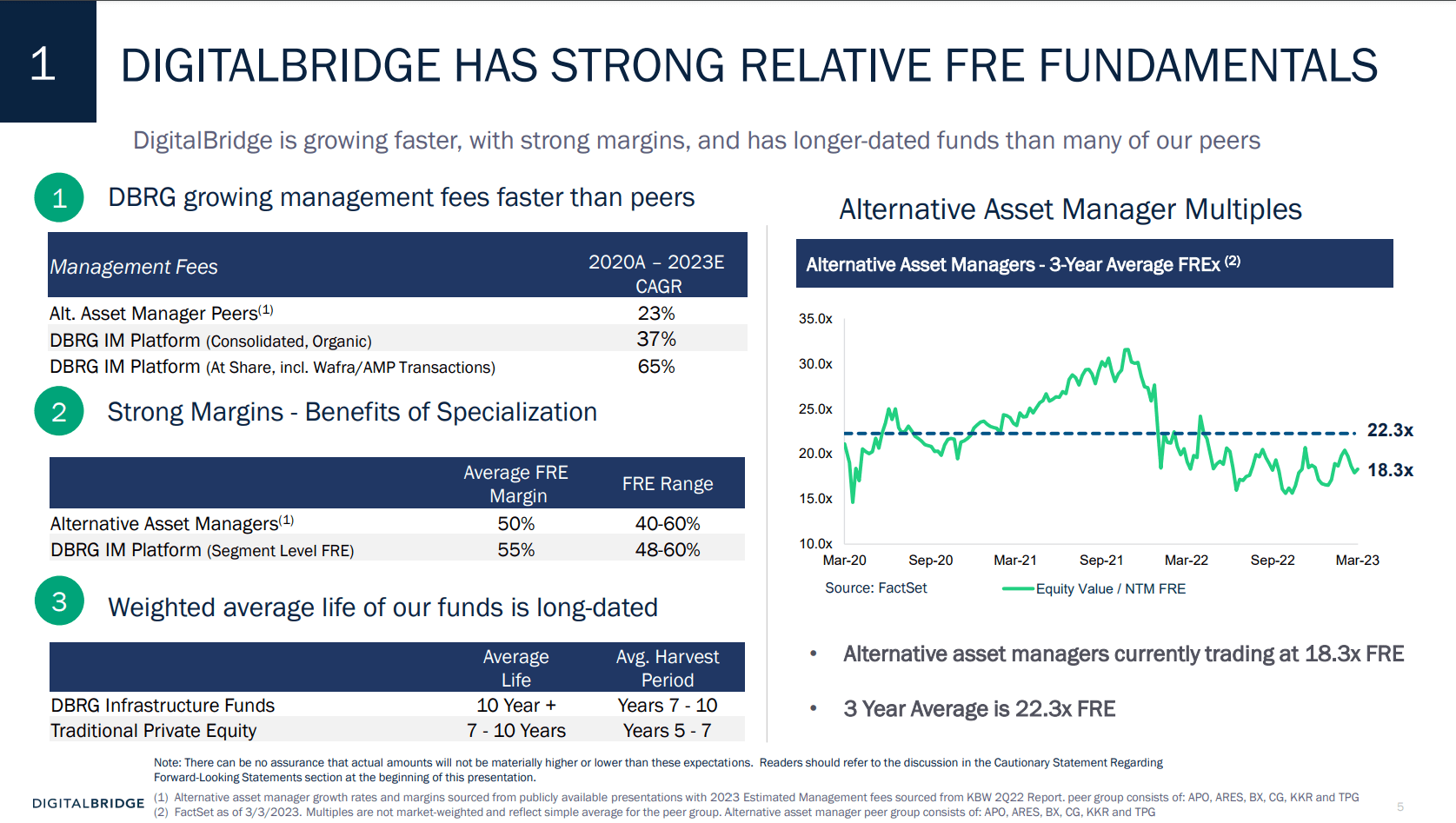

Fee-Related Earnings Value- The management has valued the company's fee-related earnings at 18.3x-22.3x 2023E midpoint FRE less 2023E corporate overheads ($50m). This range of P/FRE multiples is based on the current and three-year averages for the peer group of alternative asset managers, including APO, ARES, BX, CG, KKR, and TPG. The peers are admittedly much more diversified. Having said that, DBRG’s margins have stood at 55% during 2020-2023E which is comparable to 48-60% for the peer group. Moreover, DRBG is expected to grow its management fees much more rapidly - at a 65% clip in 2020-2023E vs a 23% average growth rate projected for the peers. I think the segment might very well be valued at a 21x 2023E P/FRE multiple - in line with peer APO which currently trades at 21.3x. Both APO and DBRG have displayed similar FRE margins in 2022 (52% for DBRG vs 54% for APO), however, DBRG has grown its FRE at a much faster 74% growth rate during 2020-2022 compared to 13% for APO. A smaller and lower-margin peer with exposure to infrastructure (22% of total FEEUM) StepStone Group ( STEP ) is currently trading at a 15.5x P/FRE multiple.

{kind=link}

DigitalBridge Investor Presentation, April 2023

{kind=link}

DigitalBridge Investor Presentation, April 2023

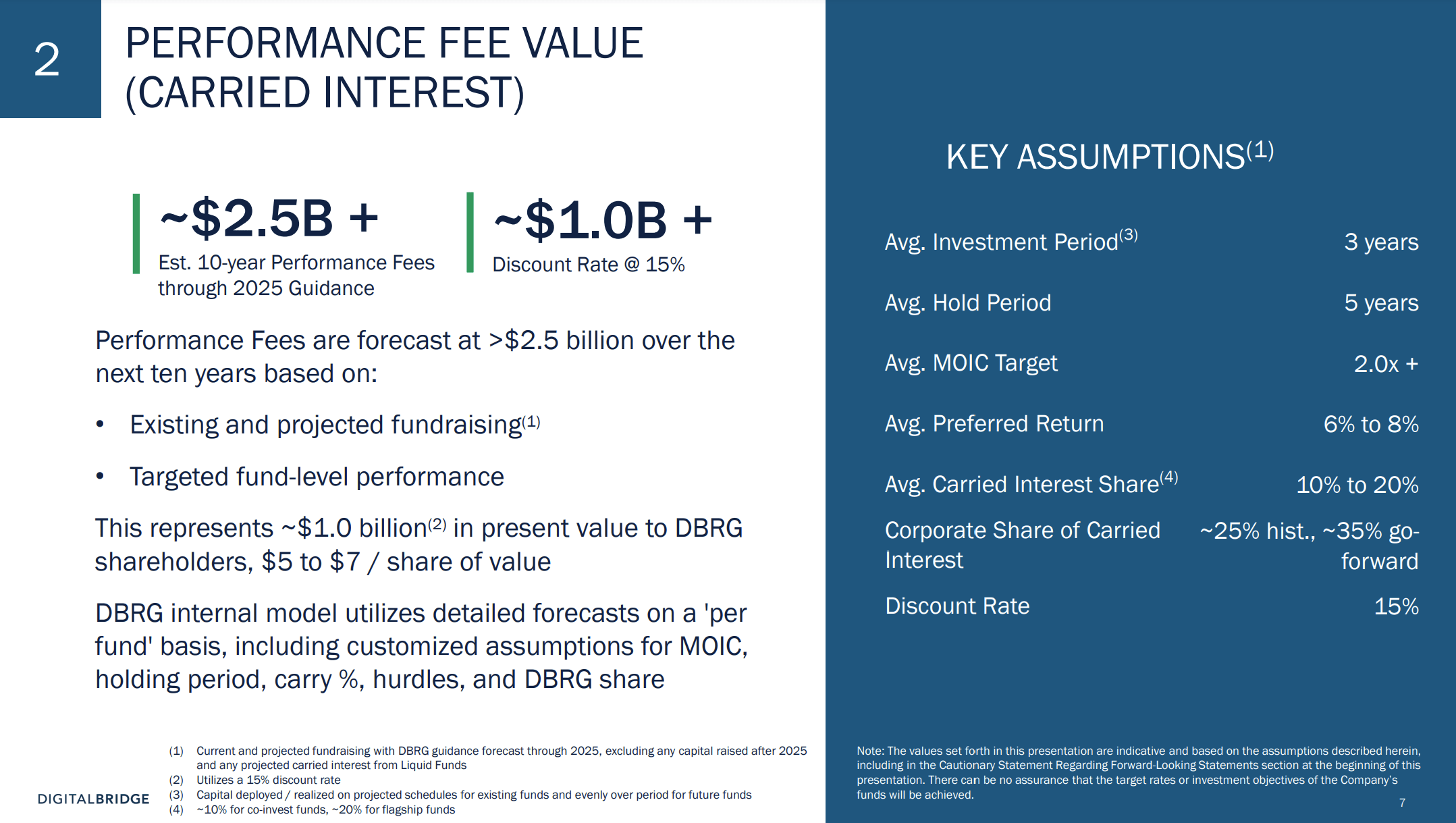

Performance Fees- Performances fees or carried interest represents the company’s share of returns in funds that exceed certain performance hurdles. In 2022, DBRG recorded $64m in carried interest, with $33m distributed to the company. DBRG’s management has valued the future stream of performance fees at $1bn. To arrive at this value, the company used a range of fairly conservative assumptions, including a 15% discount rate.

{kind=link}

DigitalBridge Investor Presentation, April 2023

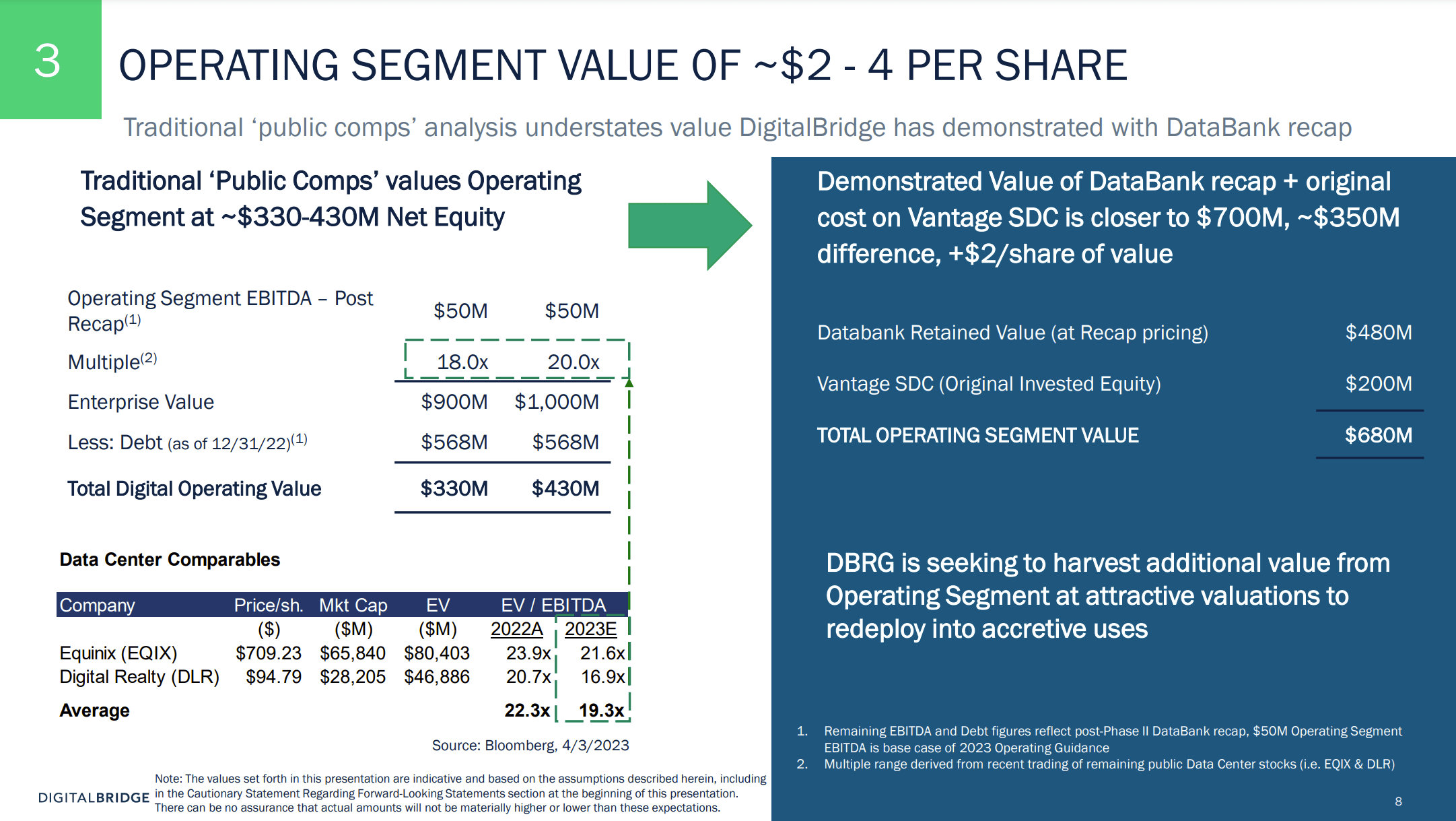

Operating Segment- DBRG’s Operating Segment might be valued using peer EBITDA multiples. DataBank and Vantage SDC’s closest comparables EQIX and DLR are trading at 17-21x 2023E EBITDA multiples, implying the Operating segment’s value of $2-$4 per share. Another way to appraise DBRG’s stakes in DataBank and Vantage SDC is to use the most recent transaction values. Pricing based on DataBank’s recapitalization in 2022 would value the company’s remaining 11% stake in the business at c. $480m. Meanwhile, DBRG acquired its 13% stake in Vantage SDC for $200m. However, DBRG’s holding in Vantage might be worth materially more than the original cost given that the business has been growing rapidly , with a number of new data centers acquired and/or developed in recent years.

{kind=link}

DigitalBridge Investor Presentation, April 2023

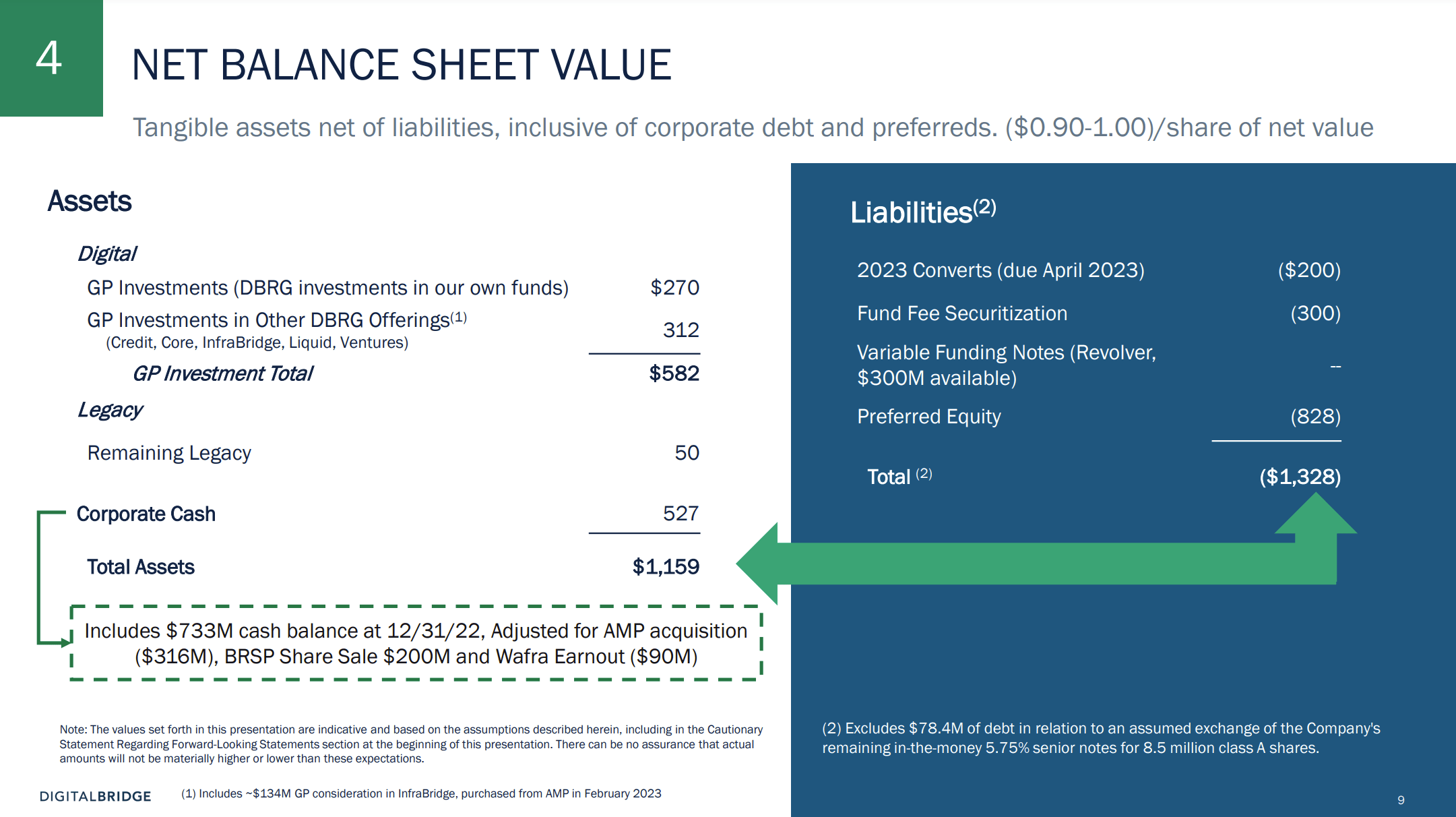

Net Debt- DBRG’s pro-forma net debt stands at $169m. This includes $1328m in corporate debt and the company’s share in investment-level debt less $1159m in gross cash as of December ’22. Note that the company’s gross cash is adjusted for the acquisition of InfraBridge (closed in February ’23) as well as several other corporate restructuring transactions.

{kind=link}

DigitalBridge Investor Presentation, April 2023

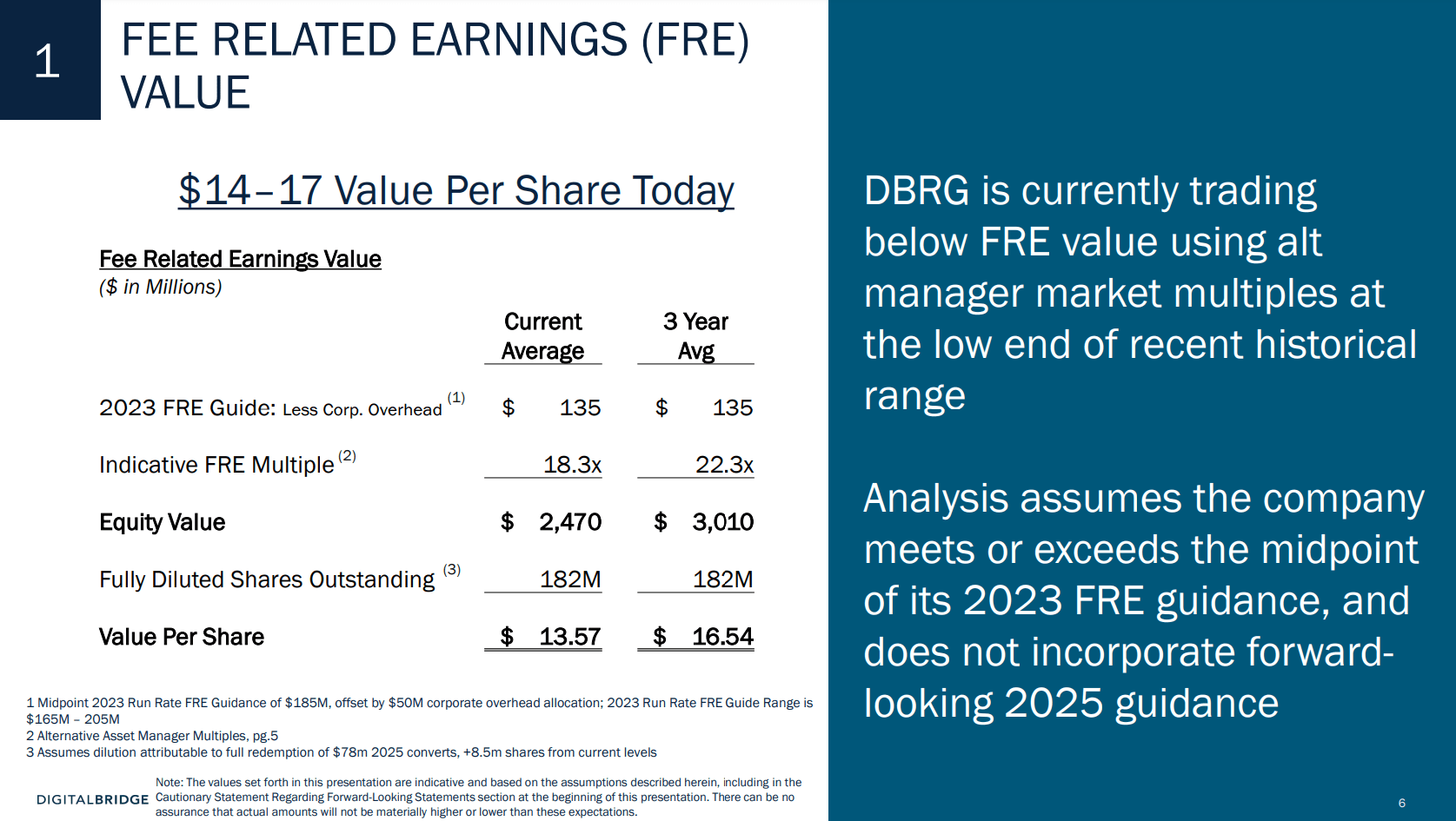

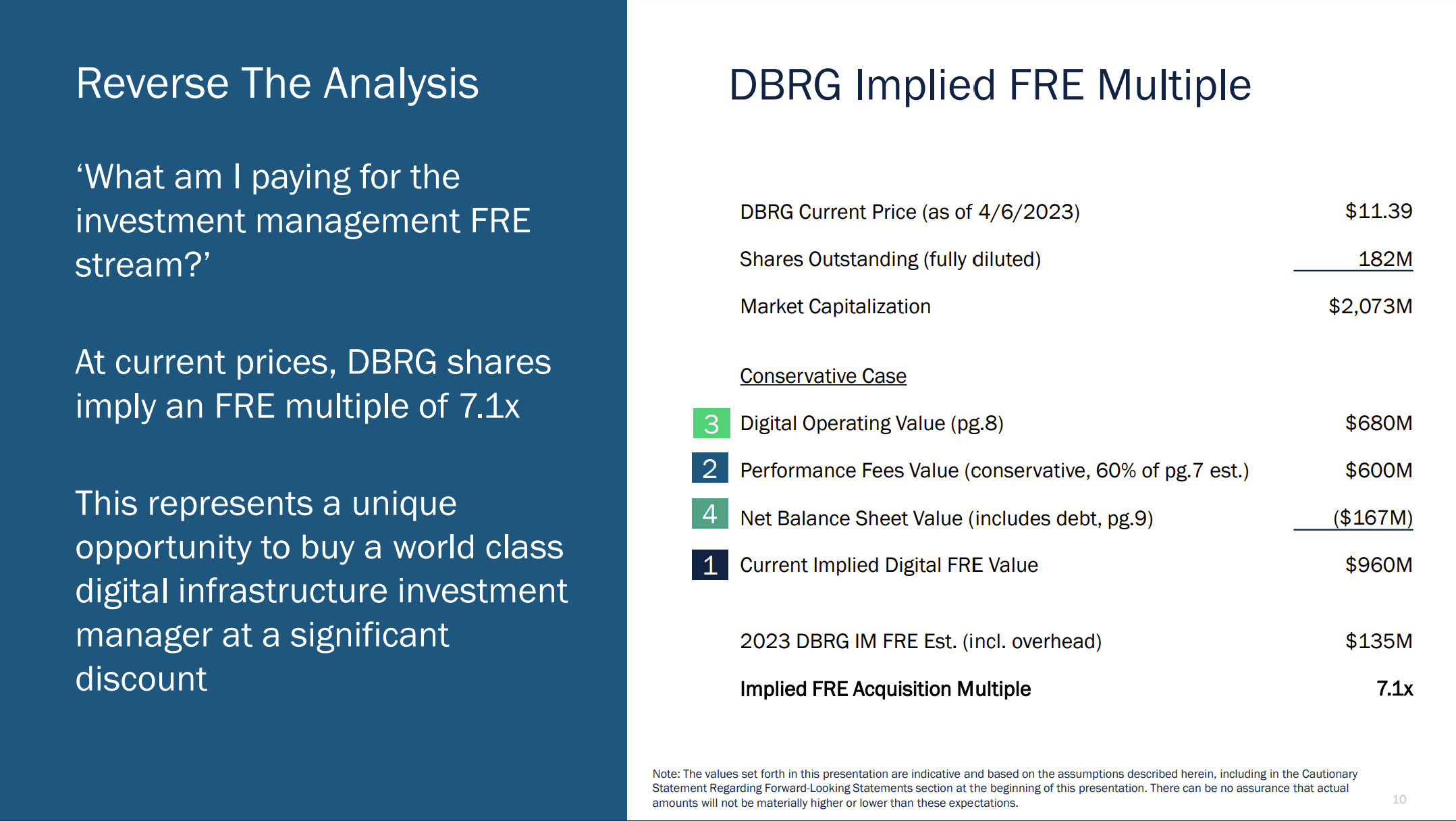

Another way to look at DBRG’s valuation is to consider how cheap investors are getting the company’s fee-related earnings. With management’s fairly conservative assumptions (see below), the market is currently valuing the core segment at $1.1bn or 8x 2023E FRE (less corporate overheads). I believe this multiple is way too low for a stream of fast-growing and long-duration recurring revenues.

{kind=link}

DigitalBridge Investor Presentation, April 2023

The Activist

Another interesting aspect here is the involvement of activist investor Legion Partners. Legion Partners is a tiny hedge fund with c. $500m in AUM. The activist investor has been DBRG’s shareholder since 2020. In December ’22, Legion came out publicly, expressing support for the company’s strategic transformation. The investor has noted that there might be an 80% upside on 2023E SOTP, with the potential for the share price to triple in the next two years. Legion has stated the company should consider a sale if current transformation efforts fail to drive up the share price. As of February ’23, DBRG was Legion’s fifth largest position.

Digital Infrastructure Industry Outlook

The digital infrastructure asset management industry is likely to fare well in a potential recession given the secular growth trends. The global digital infrastructure market is projected to expand at a 24% CAGR during 2022-2030. This is not surprising given the numerous long-term tailwinds which are expected to propel the digital infrastructure space, including cloud outsourcing trends and increasing network data traffic, leading to the expansion of 5G mobile networks. Gartner expects the global public cloud services market to grow by 21% in 2023. Meanwhile, global data infrastructure revenue is expected to expand at a rapid 26% CAGR clip from 2023 to 2026. The digital transformation still seems to be in the early stages globally, indicating that significant incremental supply will have to come online. As of 2020, 56% of data center capacity still remained in on-site legacy data centers.

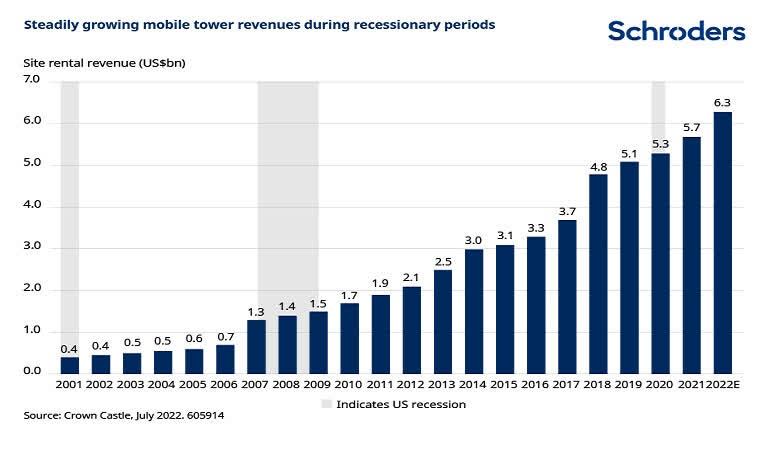

Another important aspect here is that digital infrastructure asset management businesses are considered to be recessionary-proof given that the funds are generally long-life. This means that asset managers do not have to sell the assets if the prevailing multiples fall due to higher interest rates. Moreover, digital infrastructure assets are usually leased on long-term contracts to investment-grade tenants, with built-in escalators that adjust lease payments to inflation. Digital infrastructure is generally considered to be mission-critical and a non-discretionary business expense. For reference, a number of digital infrastructure-focused operators, such as Equinix (focused on data centers), Cogent (fiber), and American Tower (towers) have historically grown their revenues during periods of recession. As another indication of this, the mobile tower revenues of Crown Castle, which is a communication infrastructure-focused REIT, have grown steadily during recessionary periods (see below).

{kind=link}

Schroders

Infrastructure Industry Fundraising Environment

Confidence in the broader infrastructure space is also highlighted by the recently performed or announced infrastructure-focused capital raises from the largest alternative asset managers. In January ’23, Ares Management raised $5bn for its infrastructure debt fund. A number of other asset managers have recently announced plans to raise significant amounts for funds targeting infrastructure investments, including KKR ( intends to launch a $20bn infrastructure fund), Carlyle ( plans to raise $2bn for its high-yield infrastructure debt fund), Blackstone ( considers raising $2bn for a new European infrastructure fund) and EQT ( intends to raise $21bn for its global infrastructure fund). According to the Infrastructure Investor, the top 10 infrastructure funds are expected to raise $121bn in 2023. The fact that a number of reputable asset managers, which are among the most knowledgeable institutional investors out there, have shown a high appetite for infrastructure fundraising might show that the asset class is expected to perform relatively well during a recession. As another illustration, Ares expects infrastructure to be the fastest-growing asset class through 2026, with an 18% CAGR. A number of alternative asset managers have likewise been bullish on the asset class - a quote from KKR’s Q4’22 conference call :

I think by strategy, you actually hit on probably the single busiest area in our firm, and that's infrastructure. And I think infrastructure has just continued to be a real success story and a real growth story for us. I think it's -- when we look back at our April '21 Investor Day, we gave a bunch of statistics there of actually where we thought infra would be over the course of 2022. Just to give you a sense, at that point, infra AUM was $17 billion. We estimated at that Investor Day that infra AUM would exceed $30 billion. And as of year-end, we're at $51 billion against that $30 billion estimate, all organic.

A quote from Blackstone’s Q4’22 conference call:

I do think you hit on a key element, which is the inflation-protected nature of hard assets, particularly in this portfolio. What it owns in transportation infrastructure, an area we went very long post-pandemic, investing in Atlantia in Europe; Autostrade in Europe; Signature Aviation here in the United States, which has been very positive for this fund. Our push in digital infrastructure, data centers, and towers, where there's really strong underlying demand. And then energy and energy transition, of course, given what's going on. And so it really has a really exceptional portfolio that investors find attractive. In an inflationary environment, it's delivered a very good performance. And in general, I would say our customers are under-allocated to infrastructure and want to hold more here.

Risks

One of the uncertainties here is elevated and potentially rising interest rates. DBRG is a levered company, with $5.1bn in total consolidated debt, $1.3bn of which is corporate/investment-level debt attributable to the company. Having said that, most of the company’s non-recourse debt is fixed rate (79% as of December ’22). DBRG has highlighted conservative management of its debt burden:

On the right side, you can see the conservative portfolio debt metrics that we put in place over a year ago and have been able to manage effectively through a dynamic macro environment. 42% loan-to-value, 74% of hedged debt fixed with an average full extended maturity of over 7 years. This is conservative management of the capital structures at our portfolio companies. This was not accidental. This is a plan we put in place at the beginning of COVID. We led multiple securitizations at the end of 2020, 2021, and 2022, setting up our portfolio companies to maximize their liquidity by having fixed debt with only 1 covenant, which is a DSCR ratio and no cash traps. This is a playbook that worked incredibly well for us in 2001 and 2002 and worked very well for us in 2008 and 2009, and it's working again.

Another risk is a potential recession, however, the predictable nature of DBRG's revenue streams coupled with digital infrastructure industry tailwinds and favorable broader infrastructure industry fundraising outlook all suggest DBRG would continue to grow its FEEUM, revenues and earnings in a potential macroeconomic downturn.

Conclusion

Digital infrastructure is likely to continue on its growth path despite a potential recession. Within these broader industry tailwinds, I consider DBRG to be among the most attractive value plays currently available on the market. The company trades at a substantial discount to its conservatively estimated sum-of-the-parts value. I expect the upcoming deconsolidation of the company’s non-core assets to catalyze the stock to more reasonable levels.

Editor's Note : This article was submitted as part of Seeking Alpha’s Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

DigitalBridge: Cheap Compounder With A Clear Catalyst