DDS - Dillard's: Healthy Cash Flows In A Slow Industry

2023-12-31 07:20:02 ET

Summary

- Dillard's operates department stores in the US, making the company's growth slow due to a shrinking industry.

- The company has elevated its gross margins during the pandemic with better inventory management, and the improvements have so far stuck around greatly rising the company's earnings level.

- With continuing store closedowns, the company's large amount of real estate could provide investors with a good amount of capital.

- The stock rally in recent years seems to have some room left with a slight undervaluation, but not a high enough amount for a buy rating.

Founded in 1938, Dillard’s ( DDS ) operates department stores in the United States. Currently, the company has 273 open Dillard’s stores , of which 27 are clearance centers. The stock price has rallied impressively in the past years, as Dillard’s has been able to drive higher margins, multiplying the bottom line. As the company operates on a mature or even declining industry, the strong performance in recent years comes as quite a surprise.

Five Year Stock Chart (Seeking Alpha)

{kind=link}

A Slow Industry

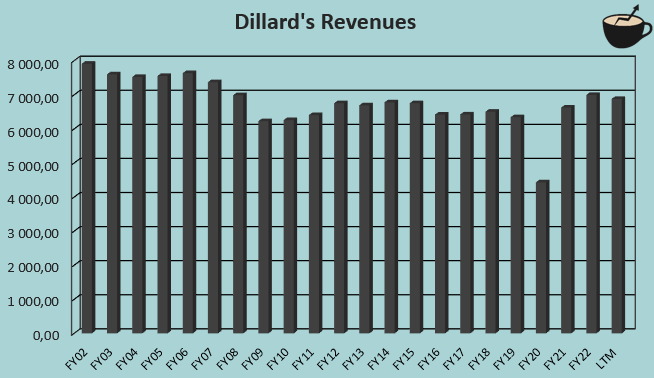

The increasing share of online purchases has made the market for department stores quite challenging. Dillard’s also sells through its website, but isn’t as competitive as online-dominant operators on the sales channel. As a result, the company’s revenues haven’t had a very great performance – Dillard’s has a negative revenue CAGR of -0.7% from FY2002 to current trailing figures .

Author's Calculation Using TIKR Data

{kind=link}

In Q3, Dillard’s closed down a location in Virginia, decreasing the company’s square footage by around 0.51%, with a current total square footage of 46.7 million. The closedown isn’t a first of its kind – the company’s earliest easily available report, Q1/FY2013 , includes the mention of a total square footage of 50.9 million. Dillard’s is reducing its brick-and-mortar operations in a steady manner. Investors are likely looking at a similar future where revenues continue on a very small, steady decline. As a silver lining, the decreasing square footage does provide investors with temporary cash flows with store closedowns as the need for inventory becomes smaller.

Impressive Gross Margin Elevation After FY2020

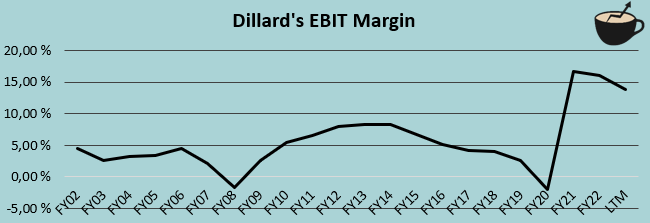

After the Covid pandemic wrecked the company’s financials in FY2020, Dillard’s has achieved EBIT margins well above historical levels. Prior to the pandemic, Dillard’s had EBIT margins in the low single-digit levels, compared to a FY2021 level of 16.8% and a trailing level of 13.8%:

Author's Calculation Using TIKR Data

{kind=link}

Driving the higher profitability, Dillard’s has had an elevated gross margin from Q1/FY2021 forward. Historically speaking, Dillard’s has had a stable gross margin, ranging from 33.2% to 37.1% in the decade prior to the pandemic. On the other hand, the gross margin for FY2021 was 43.4%, and still stands at a substantially higher level at 41.7% with trailing figures.

In Q1/FY2021 and Q2/FY2021 , as the gross margin started to be at an elevated level, the company related the strong performance mainly to a better inventory management. The inventory savings seem to have stuck around, as Dillard’s still achieves quite high gross margins even in a poorer consumer spending environment – it is very possible, that the higher EBIT margin level will stick around. The sudden improvement doesn’t seem to have been boosted by an industrywide improvement in gross margins, but rather by the company’s own doing – for example, Macy’s and Kohl’s both currently have gross margins quite near pre-pandemic levels. Dillard’s currently has the highest of the three with the figure of 41.7%, as Macy’s has a trailing gross margin of 39.3% and Kohl’s a gross margin of 36.8%.

A Valuable Balance Sheet

Dillard’s owns a great amount of real estate. At the end of FY2022, the company had almost $3.1 billion in buildings on its balance sheet , adding up to around $187 per share. Normally, I’d see the buildings as necessary operating assets that don’t necessarily add to investors’ value, but as Dillard’s has closed down stores in past years and is likely to continue the closedowns, the buildings seem valuable as the capital could be partly returned to investors as time goes on. In addition to the real estate, Dillard’s has a good cash balance, with around $893 million currently in cash and short-term investments. The company leverages a low amount of debt with $521 million in long-term debt.

Slight Room Left for the Stock Rally

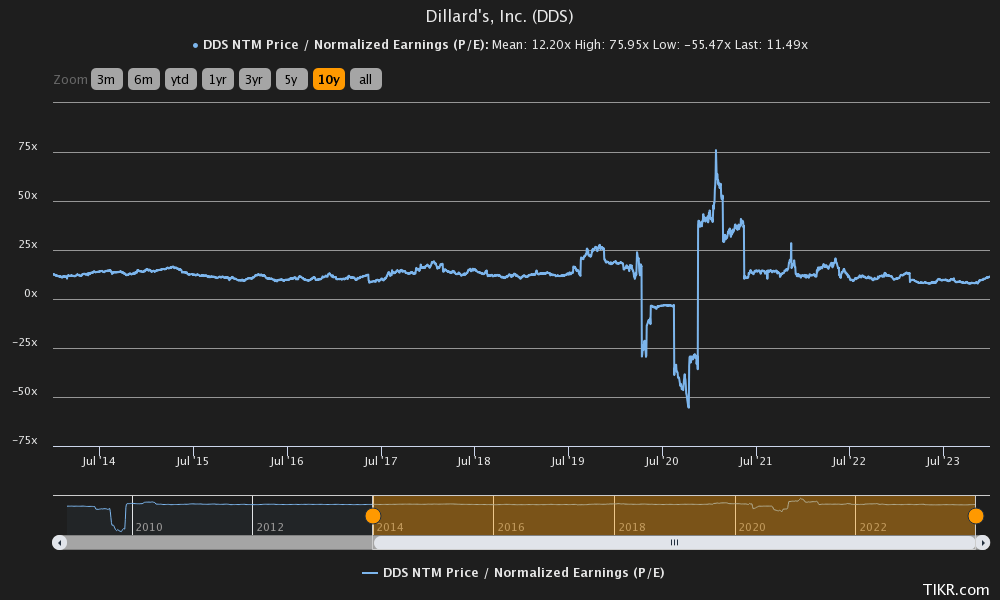

Dillard’s currently trades at a forward P/E multiple of 11.5, a bit below the ten-year average of 12.2. With the poor long-term sales performance, but strong balance sheet, the multiple seems like a reasonable baseline.

{kind=link}

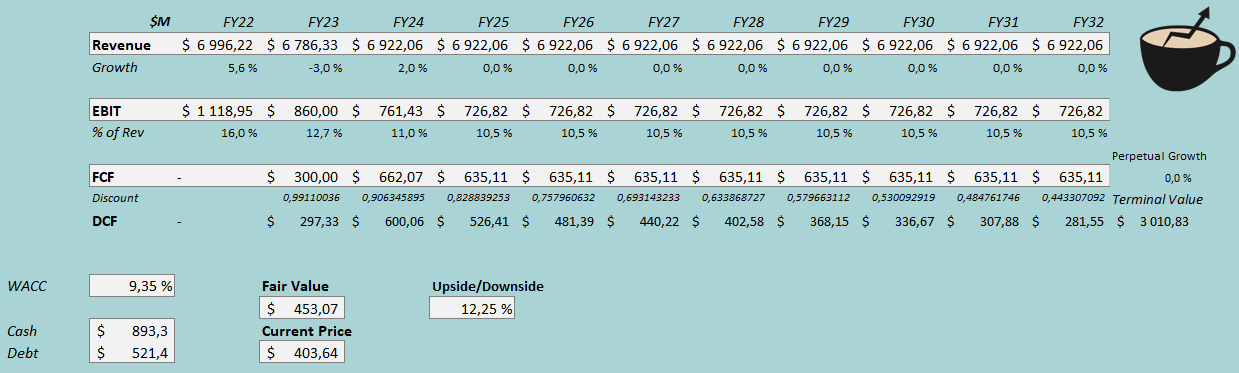

To estimate a fair value for the stock, I constructed a discounted cash flow model with future financials that I believe to be good baseline expectations. For FY2024, I estimate a growth of 2% as the macroeconomic situation should eventually slightly improve consumer spending. Afterwards, I estimate stable nominal revenues, signifying slightly negative growth in real terms.

For the margins, I estimate some deterioration from the current level – the sudden change in gross margin has seen some pressure already, that I associate to the macroeconomic environment, but a possibility of gross margin deterioration into a more historical level should be considered in my opinion. I estimate the EBIT margin to fall into 12.7% in FY2023, and to fall further by 2.2 percentage points into a sustained EBIT margin of 10.5%. The estimate could be due for either a upgrade or downgrade with upcoming quarterly results, but I see the estimate as a good baseline scenario. The company also has a very good cash flow conversion with decreasing working capital needs and a high amount of depreciation compared to a moderately low capital expenditure level.

With the mentioned estimates along with a cost of capital of 9.35%, the DCF model estimates the stock’s fair value at $453.07, around 12% above the stock price at the time of writing. The stock rally seems to still have some room left, but not an extraordinarily great amount; the undervaluation brings a good risk-to-reward, but not enough for a buy rating just yet.

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In the past twelve months, Dillard’s has had around $13.7 million in interest expenses. With the company’s current amount of interest-bearing debt, its annualized interest rate comes up to a low figure of 2.63%. The company uses debt quite modestly, and I estimate a long-term debt-to-equity ratio of 10%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.87% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates the company’s beta at a figure of 1.01 . Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 10.09% and a WACC of 9.35%.

Takeaway

The rally in the stock in recent years seems justified, as Dillard’s has improved the company’s gross margin very impressively. Although department stores aren’t facing a future of good growth, and Dillard’s seems likely to continue store closedowns, the cash flows should still provide investors with great cash flows in upcoming years. The store closings create the opportunity to free capital from inventories, as well as the company’s significant real estate portfolio. The stock rally still seems to have some room for more appreciation as the stock seems slightly undervalued, but not at a level that’s enough for a buy rating in my opinion. For the time being, I have a hold rating.

For further details see:

Dillard's: Healthy Cash Flows In A Slow Industry