DIISF - Direct Line: Don't Be Fooled By Its Discounted Valuation

2023-11-07 05:47:48 ET

Summary

- Direct Line continues to struggle in its motor segment, leading to weak financial performance.

- The company has made efforts to improve profitability, including selling its brokered commercial insurance business.

- Direct Line's capital position is expected to improve after the sale, but a dividend resumption will depend on improved operational performance.

Direct Line (DIISF) continues to report a relatively weak financial performance due to struggles in its motor segment, justifying its current valuation.

As I've covered in a previous article , while Direct Line had a good financial performance historically, its fundamentals suffered significantly during 2022 due to several external factors, including high inflation that led to much higher claims costs than expected. This setback was not particularly positive for the company and, not surprisingly, its shares have been relatively weak in recent months.

In this article, I update Direct Line's most recent financial performance and investment case, to see if it now offers better value for long-term investors' or if it remains a stock to avoid.

Financial Overview

Direct Line's business is quite geared to the motor segment, even though it also offers other insurance lines within the Property & Casualty (P&C) market, including home insurance and commercial lines. Its main strength is its strong market position in the U.K. motor segment, where is the second-largest company following the market leader Admiral Group (AMIGY), with a market share of about 11%.

Despite this position, investors should be aware that the U.K. motor segment is quite fragmented given that top three companies only hold some 35% of total written premiums. This means that larger players don't have much pricing power, and potential price wars can lead to lower profitability across the industry.

Given that motor is Direct Line's largest segment and its biggest driver of top-line and earnings growth, this industry backdrop is not a great support for its fundamentals over the long term.

Indeed, in 2022, the operating landscape turned quite negative in the U.K., due to higher cost claims in the motor segment due to inflation and bad weather than led to higher losses in home and commercial insurance lines. Moreover, weak performance in the capital markets also led to lower investment income in the year, having a negative impact on its overall profitability.

Given this backdrop, Direct Line's operating profit in the year was only £32 million, a decline of 94% YoY, and it reported a net loss of £40 million in the last year (vs. a net income of £344 million in 2021).

While most factors that led to this collapsing profitability are largely outside of the company's control, Direct Line made some efforts to improve its underwriting profitability and better adapt its business to the current operating landscape.

Indeed, Direct Line has recently decided to sell its brokered commercial insurance business, in a transaction that generates some £520 million of cash inflow. This business has been part of Direct Line since 2003, and operated in a different part of the U.K. insurance market than its core businesses, thus management decided to sell it to improve the company's balance sheet and to focus exclusively on direct to retail consumer insurance lines.

In motor, Direct Line has decided to increase prices in recent months and expanded its own managed repair network, to have better control over its underwriting profitability in the motor segment.

This led to higher premiums in motor during H1 2023 , up by 8% YoY, with average premiums increasing by 28% YoY in the second quarter, a growth that is ahead of the industry. These higher prices are mainly reflected in new business, while renewals have softer price increases, as Direct Line wants to maintain customer churn rates at moderate levels.

Motor pricing (Direct Line)

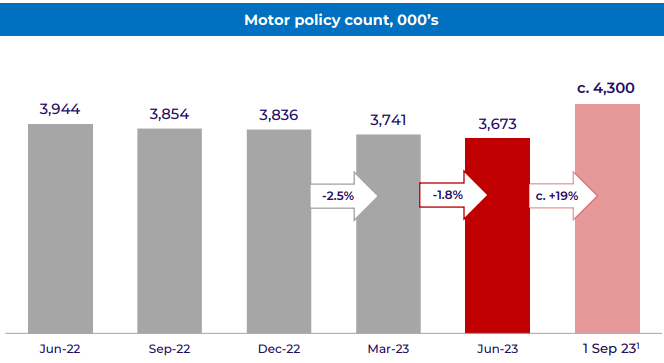

Not surprisingly, while Direct Line was able to increase prices across its motor segment, the total number of policies declined by 4% YoY in H1 2023, to less than 3.7 million at the end of June. This is an acceptable decrease considering the price increases performed in recent quarters, which would naturally lead to higher churn compared to previous years.

Nevertheless, due to price increases in motor and strong performance in commercial lines, Direct Line's gross written premiums increased by 9.8% YoY to £1.6 billion. Its insurance premiums ex-motor increased to £857 million (+12.2% YoY), and represented some 53% of total premiums, showing that home, commercial, and other lines had a good performance during the first six months of the year.

Indeed, all insurance lines excluding motor reported an operating profit in H1 2023, while motor continued to suffer from high levels of claims, which were not offset by higher pricing in the segment. This led to an operating loss of £180 million in motor in H1 2023, pushing the overall company's operating result to negative in this period.

Operational performance (Direct Line)

This means that Direct Line continues to report a weak financial performance due to a challenging operating environment in motor, not boding well for its profitability and earnings growth ahead.

On the other hand, Direct Line was able to gain some 700 thousand new customers in September, as the company is now the insurance partner of Motability, a U.K. institution that provides mobility solutions for disabled people. Motability switched from RSA Insurance Plc, which is part of Intact Financial Corp (IFCZF), to Direct Line in its Motability scheme, which will represent a significant boost for the company's costumer and premium growth in the second half of the year.

{kind=link}

Another tailwind for its earnings is higher investment income due to rising interest rates, which benefit its investment yield both in fixed income securities and cash. Given that Direct Line has a conservative investment allocation, with more than 30% of its investment portfolio in cash and cash equivalents, higher short-term interest rates are a boost to its investment income, explaining why its net investment income increased by 48% YoY in H1 2023, to £80 million.

Its investment income yield was 3.2% in H1 2023, still considerably lower than short-term rates in the U.K., and the company expects its 2023 investment income yield to be between 3.4-3.5%, thus higher investment income is expected in the second half of the year, being positive for its earnings in the next few quarters.

Another positive development was its stable Solvency ratio during the first half of 2023 despite its net loss, given that it reported a Solvency ratio of 147%, unchanged from the end of 2022. However, this Solvency ratio is weaker than compared to its closest peers and the average of the European insurance sector, thus it's not likely that Direct Line will resume a dividend payment in the short term.

Investors should note that Direct Line had a good dividend history until 2022, but this changed dramatically last year due to weak earnings, which led to a dividend suspension. Taking into account that Direct Line continues to report losses due to tough conditions in the motor segment and its capitalization is not great, I think the prospects of resuming a dividend in the short term are quite low.

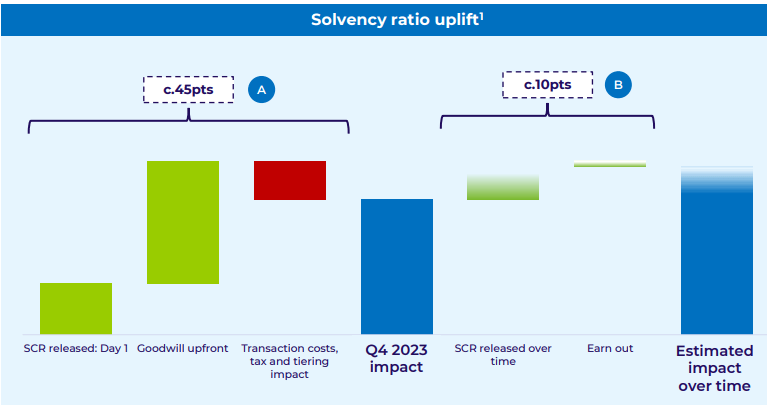

However, when the sale of its brokerage business is completed, its Solvency ratio is expected to have an uplift of some 45 percentage points, plus there will be some 10 percentage point's benefits over time, putting Direct Line's capital position in a much stronger position.

Therefore, assuming a Solvency ratio closer to 200% at the end of 2023, higher than its desired 140-180% range, Direct Line may decide to resume a dividend payment, if it returns to a positive net income in the second half of the year.

{kind=link}

Conclusion

Direct Line continues to report weak results due to the woes in its motor segment, which is critical for its financial performance by being the largest one within the group. While the capital position is set to improve markedly after the sale of its brokerage insurance business, a resumption of its dividend is only expected to happen if the operational performance improves and Direct Line is able to report a positive net income.

A high-dividend yield is an important factor within the insurance sector, given that generally growth prospects are muted, thus this puts Direct Line on a weaker position compared to its peers. This profile is also reflected in its valuation, as the company is currently trading slightly below book value, at a discount to its peers and its own historical average, but this seems to be fair considering Direct Line's recent financial performance and that a rapid turnaround is not expected over the next few quarters.

For further details see:

Direct Line: Don't Be Fooled By Its Discounted Valuation