DIISF - Direct Line: Too Much Uncertainty Even For 5x 2019 EPS

2023-03-16 07:04:08 ET

Summary

- After 2022 results on Monday, Direct Line's share price is now down 60% in the past 5 years and at 5.3x its pre-COVID 2019 EPS.

- Direct Line made a loss in 2022, partly due to inflation and regulatory changes, but management made mistakes in Motor pricing.

- Direct Line is making significant changes to improve its Solvency Ratio and profit margin, but visibility on future earnings is poor.

- 2022 headwinds will continue into H1 2023. 2023 earnings will likely be depressed and the dividend is currently suspended.

- Overall, we believe Direct Line is in the “too difficult” category for the moment and assign it a Hold rating. Avoid.

Introduction

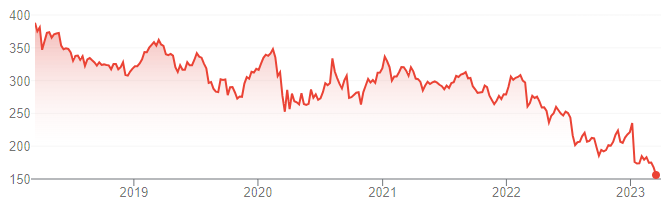

Direct Line Insurance Group plc ( OTCPK:DIISY ) released full-year 2022 results on Monday (March 13), having already disclosed some headline figures in a profit warning in January. Direct Line’s share price fell 6.6% in London in the three days after results, taking its total decline in the last 5 years to 60%:

{kind=link}

We have historically avoided Direct Line, seeing it as a weaker business and a long-term market share donor to sector leader Admiral Group plc ( OTCPK:AMIGY ), which has been Buy-rated in our coverage since October 2020 .

Direct Line made a loss in 2022 and its Solvency Ratio fell below target. While this was partly due to factors, management made key mistakes in Motor pricing. An acting CEO was put in place in January and he has lowered medium-term profitability targets. We only have limited visibility over future profitability, as Direct Line is making significant changes to improve its Solvency Ratio and profit margins. Headwinds from 2022 will likely impact at least H1 2023. The dividend has been suspended and will not be reinstated until half-year results at the earliest. Relative to pre-COVID 2019 financials, Direct Line shares have a P/E of 5.3x and a Dividend Yield of 13.8%, but EPS has now declined every year since 2018 and several of its businesses are now smaller. Overall, we believe Direct Line is in the “too difficult” category for the moment and assign it a Hold rating. Avoid.

Company Overview

Direct Line is a U.K. Property & Casualty insurer with a current market capitalization of £2.03bn ($2.5bn). In 2022, the group had £2.97bn of total GWP, and 9.69m in-force-policies at year-end. It is the second largest provider in U.K. Motor insurance (after Admiral), and a top-3 player in Home and Rescue; it also has a growing Commercial business as well as Other Personal Lines such as Travel and Pet. It generates roughly 70% of its Gross Written Premiums (“GWP”) from its own brands, the rest from partnerships.

Direct Line operates four segments, with Motor contributing the bulk of its profits. In 2019, the last “normal” year before the pandemic, Motor generated 52% of group GWP and 55% of group Operating Profit.

{kind=link}

Direct Line has historically had higher Loss Ratio and Expense Ratio than Admiral and others, which means it is less has weaker underwriting and is less efficient on costs. In 2019, Direct Line’s Loss Ratio was nearly 9 ppt worse than Admiral and its Expense Ratio was more than 6 ppt worse, which meant its Combined Ratio was 15 ppt worse:

| U.K. Motor Underwriting Ratios by Provider (2019) Source: Company filings. |

Direct Line’s cost disadvantage means it has been consistently losing market share, and we believe many of its customers have moved to Admiral, which has been consistently gaining market share:

| U.K. Motor Insurance Policy Numbers by Provider (2012-22) Source: Company filings. NB1. Direct Line figures include both own-brands and partnerships. esure and Sabre (SBRE) figures not available for 2022. Hastings and esure figures include estimates. |

Direct Line’s results were correspondingly poor in 2022.

Direct Line 2022 Results Headlines

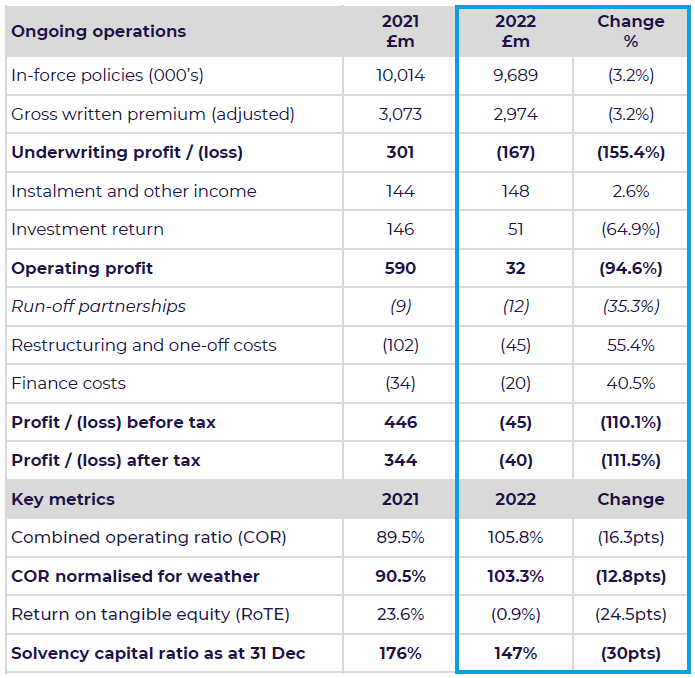

Direct Line made a loss in 2022 and its Solvency Ratio fell below target, as shown in the table below:

{kind=link}

Profit Before Tax was a negative -£45m, with an Operating Profit of £32m burdened by losses in three run-off partnerships (low-margin insurance and packaged bank accounts), restructuring and one-off costs and finance costs.

Operating Profit of £32m was entirely attributable to Instalment & Other Income and Investment Return, after an Underwriting Loss of £167m for the year.

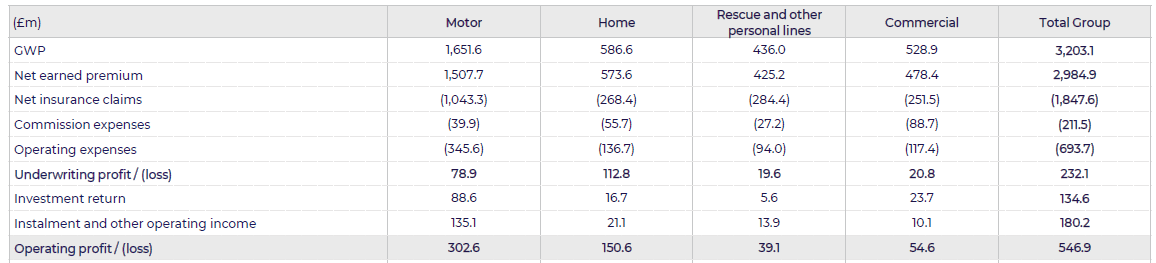

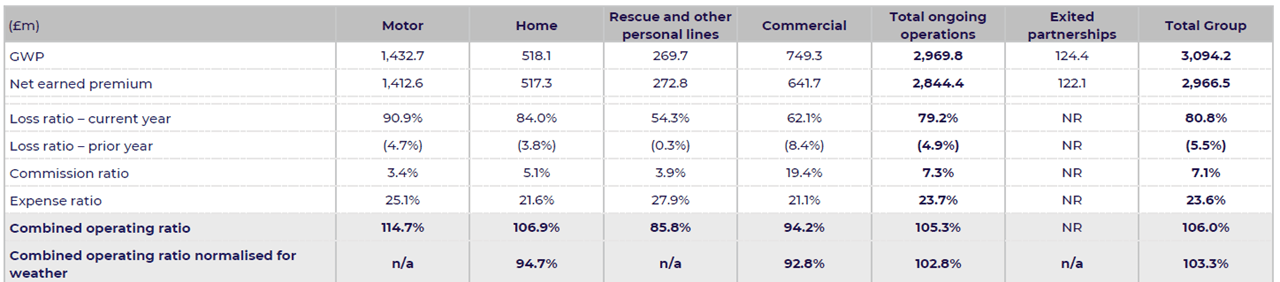

Underwriting Loss was the result of a group Combined Operating Ratio (“COR”) of 105.8% (103.3% excluding weather), with losses in both Motor (COR of 114.7%) and Home (COR of 106.9%), though Home was profitable excluding weather (COR of 94.7%). Commercial and Rescue & Other Personal Lines remained profitable:

| Direct Line Premiums & Underwriting Ratios By Segment (2022) |

{kind=link}

Investment Return of £51m was 64.9% lower year-on-year and 62.1% lower than in 2019 (£134m), despite a higher investment income yield, and was caused by £45m of mark-to-market losses on commercial property investments and £22m of realized losses on the sale of some longer-duration U.S. dollar credit holdings.

Group In-Force Policies fell 3.2% year-on-year, with declines in three of its four segments, Motor, Home and Rescue.

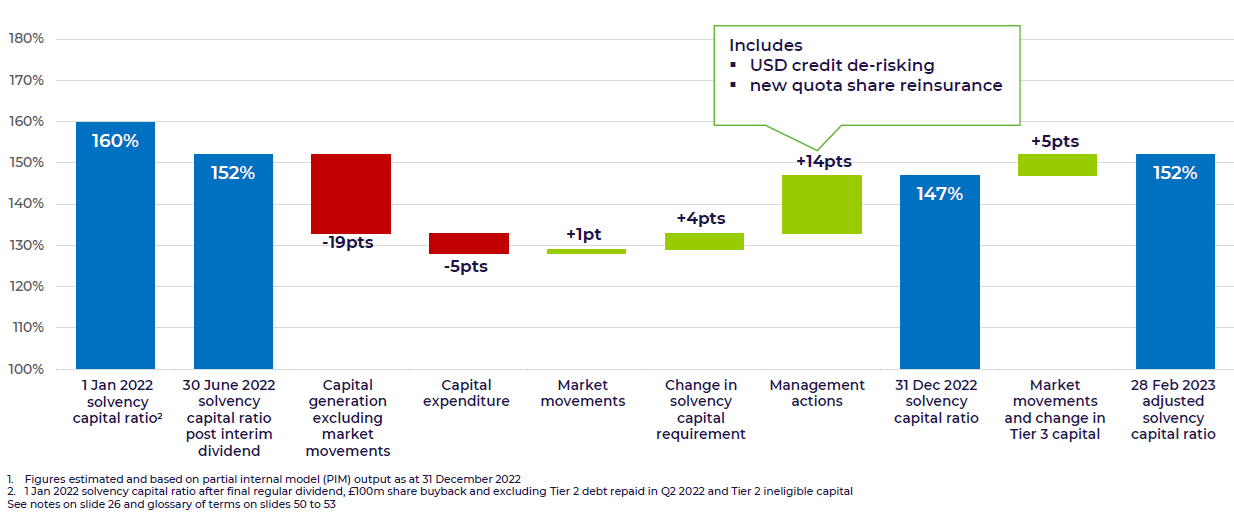

Solvency Ratio fell to 147% at 2022 year-end, due to losses and capital expenditure in H2. This was after 14 ppt of benefit from management actions (new quota insurance and sale of some U.S. dollar credit), and was only 7 ppt higher that the bottom of management’s 140-180% target range. However, the Solvency Ratio has risen to 152% at the end of February due to market movements and the impact of IFRS 17 (reducing ineligible capital):

{kind=link}

Direct Line’s poor 2022 results were due to both external factors as well as management errors.

Reasons Behind Direct Line’s Poor 2022

There were two external headwinds for U.K. general insurance in 2022:

- High inflation, especially after Russia invaded Ukraine in February

- A new Financial Conduct Authority (“FCA”) rule that requires insurers to offer the same prices to new and renewing customers, which came into effect in January 2022

In addition, for Home insurance, there was extreme weather throughout the year including storms, unusually dry weather and unusually cold weather.

Management made key mistakes in Motor insurance pricing, particularly renewal pricing, as acting CEO Jonathan Greenwood explained on the earnings call :

“We did not get the balance right between retention and renewal discounts, which eroded some of the rate increases ... For renewal business … we reduced our premiums by around 8% for the implementation of the FCA pricing reforms. We also put through 22 points of rate in response to claims inflation, but some of this was traded away to optimize retention, which increased to 82%. The net result of all these actions was a 6% fall in average renewal premiums.”

The actual amount of pricing that was “traded away” was not disclosed. However, the 6% fall in average renewal premiums was obviously damaging to underwriting margins when claim cost inflation was running at 10%+. (Direct Line estimated that its severity inflation was 14%, compared to a 3-5% long-term range)

Direct Line’s average new business premium rose 10%, also falling short of its severity inflation.

| Direct Line Motor Average Premium (2022 vs. Prior Year) Source: Direct Line results presentation (2022). |

Direct Line’s Motor premium increases were much smaller than that of market leader Admiral, which raised its new business prices in U.K. Motor by double-digits and reduced its renewal prices by mid-single-digits at the start of 2022, before raising them both by 25% since March. (However, both Direct Line and Admiral had a decline of around 10% in their Current Year Attritional Loss Ratio between 2019 and 2022.)

Management decisions were also responsible for the losses on commercial property investments (by having decided to pursue them) and the losses on the sale of U.S. dollar credit holdings (by spending too much on dividends and buybacks in prior years, which made the sale necessary).

Acting CEO & Lower Medium-Term Targets

Direct Line parted with its CEO Penny James “with immediate effect” on January 27, two weeks after its profit warning.

Jon Greenwood, previously Chief Commercial Officer, has been appointed Acting CEO. At 2022 results he announced a reduction in Direct Line’s medium-term COR target, from 93-95% to an effective 96%. (A higher COR means a lower profit, and the actual new target is a 10% Net Insurance Margin under IFRS 17, which is equivalent to a 96% COR.)

The new, lower target will not be met in 2023 and management declined to give a timeframe of when it will be met. As CFO Neil Manser explained on the call:

“We said it’s ambition. We have not put a time horizon around it given the headwinds in Motor coming through. Clearly, we will not meet that in 2023 because the Motor earnings lagged. And we are working hard to restore the margins that we need to hit that ambition. But I'm not going to give you an exact timeframe on it.”

We only have limited visibility over future profitability, because of significant changes Direct Line is taking.

Earnings Visibility Reduced by Changes

Significant changes currently made by management on capital and margin means future earnings are hard to predict.

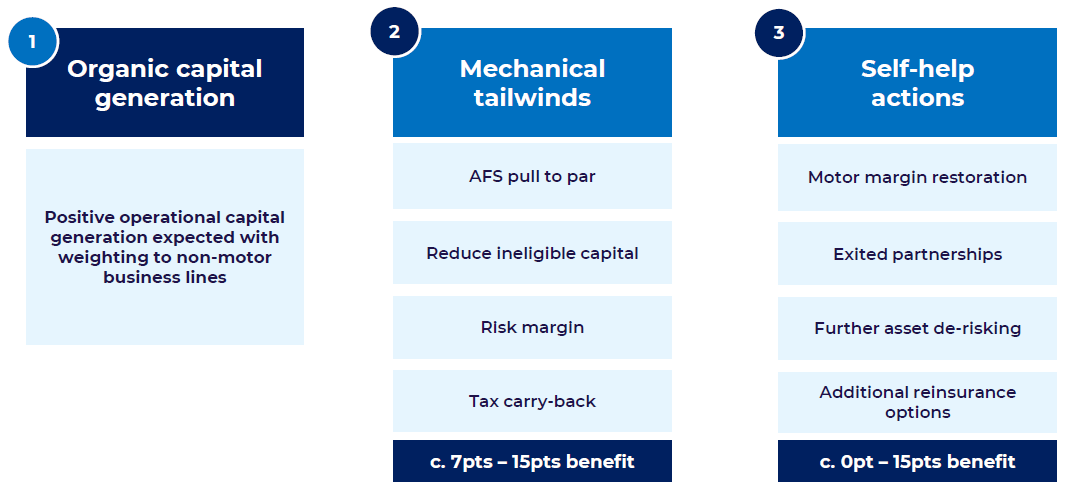

On capital, management aims to return the Solvency Ratio from 152% to 160%. While this will be partly achieved by organic profit generation (especially with the dividend now suspended), there will also be inorganic measures. The new 10% quota share reinsurance (announced on January 26) and sale of certain U.S. credit holdings were part of such measures, and Direct Line also intends to pursue “further asset de-risking” and “additional reinsurance options”:

| Direct Line Solvency Ratio – Organic & Inorganic Changes |

{kind=link}

These measures all come with costs – reinsurance means giving away some of Direct Line’s economics, while de-risking assets typically means accepting a lower investment return. We do not have good estimates of such costs.

On margin, Direct Line now has an explicit goal of prioritizing Motor margin over volume. As CEO Jon Greenwood said:

“We're very much guided this year by restoring margins over maintaining volumes. So whilst we can't predict what peers will do, our philosophy through 2023 will be very much centered around pricing for the margin.”

While we agree with this approach, the impact on the size of Direct Line’s profits is hard to predict, given it has a history of losing volumes consistently since 2018 (Motor policies fell by 3% in 2018-22) and such losses accelerated with price hikes in 2022 (Motor policies fell by 3.4 in 2022 alone):

| Direct Line Motor Policies (2012-22) Source: Direct Line company filings. |

A further headwind to Motor margins may be the continuing shift to Price Comparison Websites (“PCWs”), away from Direct Line’s historic focus on a direct model (implicit in its name). PCWs are now 90% of new business sales in the U.K., and on the call Greenwood declared that he will “accelerate the alignment of our model more closely to the PCW channel”. Again this approach is likely sensible (or even inevitable) but may impact costs and pricing.

Direct Line 2023 Outlook

Management refused to provide a 2023 outlook, but acknowledged that headwinds from 2022 will likely impact at least H1. As CFO Neil Manser explained on the call:

“The significant premium increases we've put through in 2022 and to date in 2023 will take time to earn through. But in the first half of 2023, the premium to be earned where in the main relate to business written during 2022, which, due to claims inflation revisions, we now expect to have a higher-than-target loss ratio. We, therefore, expect 2023 earnings to be depressed before recovering into 2024.”

Interestingly, he also said management has become now more “conservative” about 2023 COR than in January:

“We're not going to give a specific guidance for 2023 because of the uncertainty out there .. We're probably being slightly more conservative than we were back in January”.

Management likely struggles with predicting 2023 performance for the same reasons we have outlined above.

2023 Read-Across for Admiral

The read-across for Admiral was positive.

As mentioned, Direct Line will be prioritizing margin over volume in 2023, and has already raised prices in Motor by 11% so far in Q1. Management is expecting claim inflation to be high-single-digits in 2023, much lower than in 2022.

These bodes well for Admiral’s underwriting margins.

Direct Line Stock Valuation

With shares at 156.6p, relative to pre-COVID 2019, Direct Line has a P/E of 5.3x:

| Direct Line EPS & Dividends (2014-22) Source: Direct Line results releases. |

Dividends in 2019 totalled 21.6p, which implies a Dividend Yield of 13.8%. However, the dividend has been suspended since the January profit warning, and will not be resumed until H1 2023 results at the earliest. How quickly dividends will resume depends on the speed at which Direct Line can bring its Solvency Ratio back above 160%.

2019 may not be a good proxy for normalized future profitability. EPS has now declined every year since 2018 (which admittedly was a period with many one-off factors, including a benefit from the Ogden discount rate change in 2018, extreme weather in multiple years and COVID-19). Group profits fell even in 2020 because higher Motor profits were offset by declines in Home and Commercial, as well as a loss in Travel. Several businesses are now smaller, with group In-Force Policies shrinking 34% in 2019-22 (with most of the decline in Partnerships) and Motor In-Force Policies shrinking 5%.

Is Direct Line A Buy? Conclusion

Overall, we believe Direct Line is in the “too difficult” category for the moment and assign it a Hold rating. Avoid.

For further details see:

Direct Line: Too Much Uncertainty, Even For 5x 2019 EPS