VLO - Dirt Cheap - Why I'm Buying Valero Ahead Of Earnings

2023-07-24 10:59:03 ET

Summary

- Valero Energy is a compelling choice for dividend investors due to its strong position in the refining industry and its ability to generate consistent shareholder value.

- The company is experiencing healthy industry fundamentals with high refinery utilization rates and strong demand for gasoline and distillate fuels.

- Looking ahead to the upcoming 2Q23 earnings, the company is expected to generate strong earnings, further supporting its undervaluation and potential for dividend growth.

Introduction

It's time to talk about one of the most volatile dividend growth stocks in my portfolio: Valero Energy ( VLO ) .

The company is currently my second-smallest position, which is based on two things:

- I haven't bought a lot of VLO since initiating my position in 2020. I mainly bought upstream energy instead of downstream (refining).

- Other stocks in my portfolio also performed really well, which somewhat offset the 114% return (ex-dividends) of VLO.

Now, I'm looking to buy more VLO, which is based on surprisingly healthy industry fundamentals, the company's valuation, and its ability to generate consistent shareholder value.

As we head into its 2Q23 earnings, I'll elaborate on all of this and explain why I'm about to buy more VLO.

So, let's get to it!

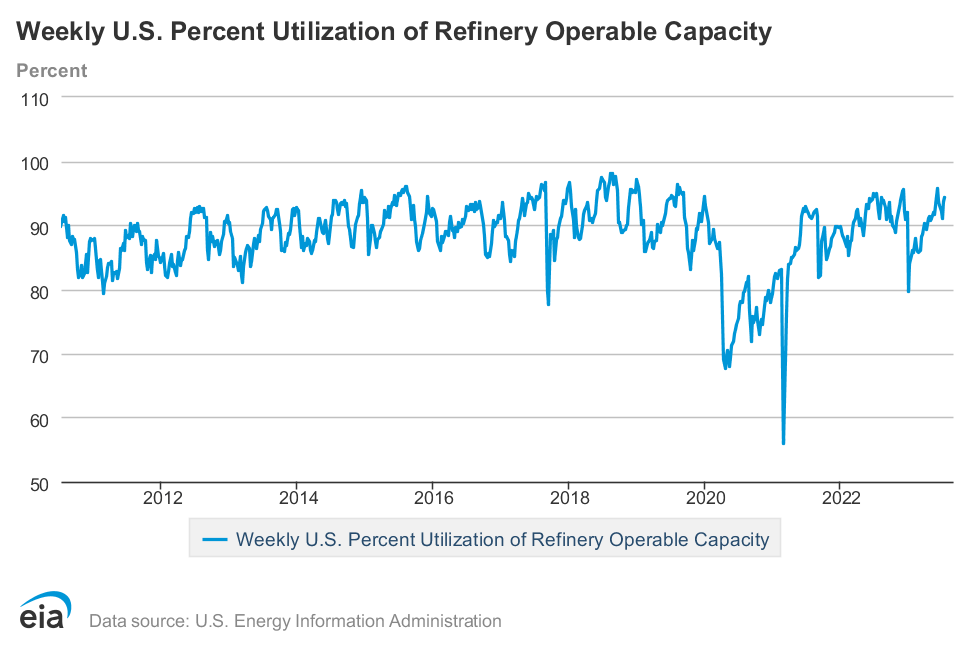

The Industry Is Doing Well

Last month, the Wall Street Journal reported on high refinery utilization rates.

{kind=link}

Wall Street Journal

The refining capacity utilization rate soared by 2.7 percentage points from the previous week to 95.8%. That was the highest rate since Aug. 16, 2019, and compared with expectations for just a 0.5-percentage-point increase.

While I'm using a somewhat old article, it needs to be said that refinery utilization rates have remained very strong. The current rate is above 94%, which is the sweet spot for these companies. Bear in mind that the goal isn't to achieve 100%. That would be dangerous. Companies like VLO want elevated rates, but not too high, as regular maintenance is required to reduce operational risks.

{kind=link}

Energy Information Administration

Now, to use a recent article, Reuters reported that gasoline demand is strong indeed (emphasis added):

Fuel stocks drew or remained stagnant week on week amid stronger demand for gasoline and distillate fuels.

Gasoline product supplied, a proxy for demand, rose by about 100,000 bpd while distillate product supplied jumped by about 700,000 barrels per day, the EIA data showed.

On top of that, export markets are getting attractive again.

As reported by Bloomberg , the month of June witnessed a decline in diesel and heating oil inventories held in independent storage facilities in northwest Europe. These inventory levels dropped below the 5-year seasonal average, further emphasizing the (valid!) concerns over the tightening supply situation.

Bloomberg

Given the constraints in imports from the Middle East and other suppliers East of Suez, the diesel market in Europe faces an urgent need for short-term resupply solutions.

Limited volumes from the US Gulf Coast add to the challenges, making it crucial to use more volumes out of storage to bridge the supply gap.

Essentially, the spike in premiums for diesel supplies underscores Europe's vulnerability to supply disruptions. The ban on Russian imports and recent refinery outages highlight the importance of diversifying and securing alternative diesel supply.

This will continue to provide tailwinds for Valero as well.

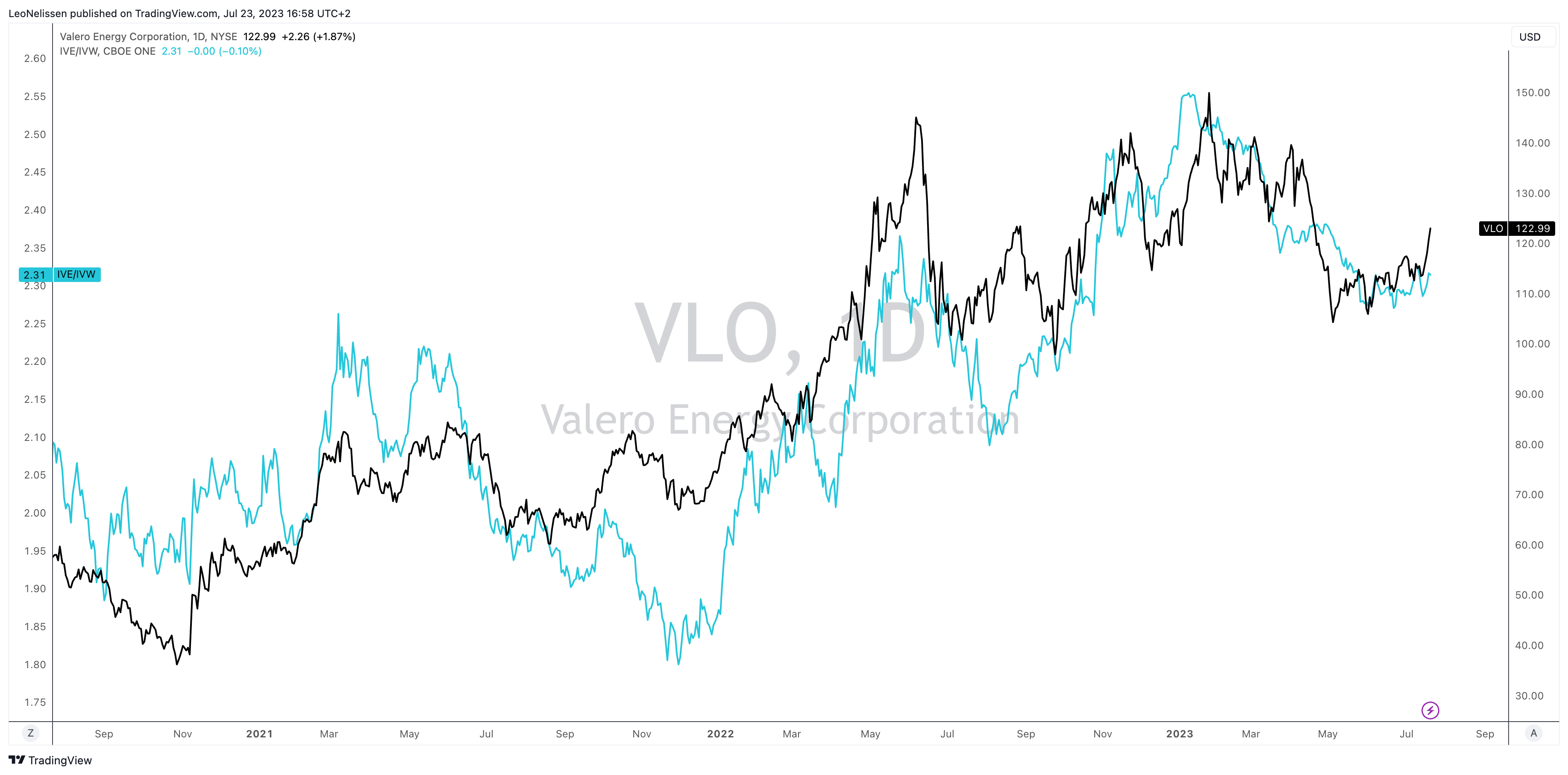

Valero Is Working On An Uptrend

In the chart below, I'm comparing two lines.

{kind=link}

TradingView (VLO, IVE/IVW)

As most of my readers will know, I've been betting on a rotation from growth back to value. I believe that inflation is sticky and likely to force massively overcrowded tech/growth trades to unwind - especially because value stocks like Valero offer inflation protection and better valuations at this point.

So far, it is starting to look like this is indeed happening, as we're now more than 12 months past the inflation peak.

Bank of America

Additionally, gasoline/energy fundamentals are strong, as we just briefly discussed.

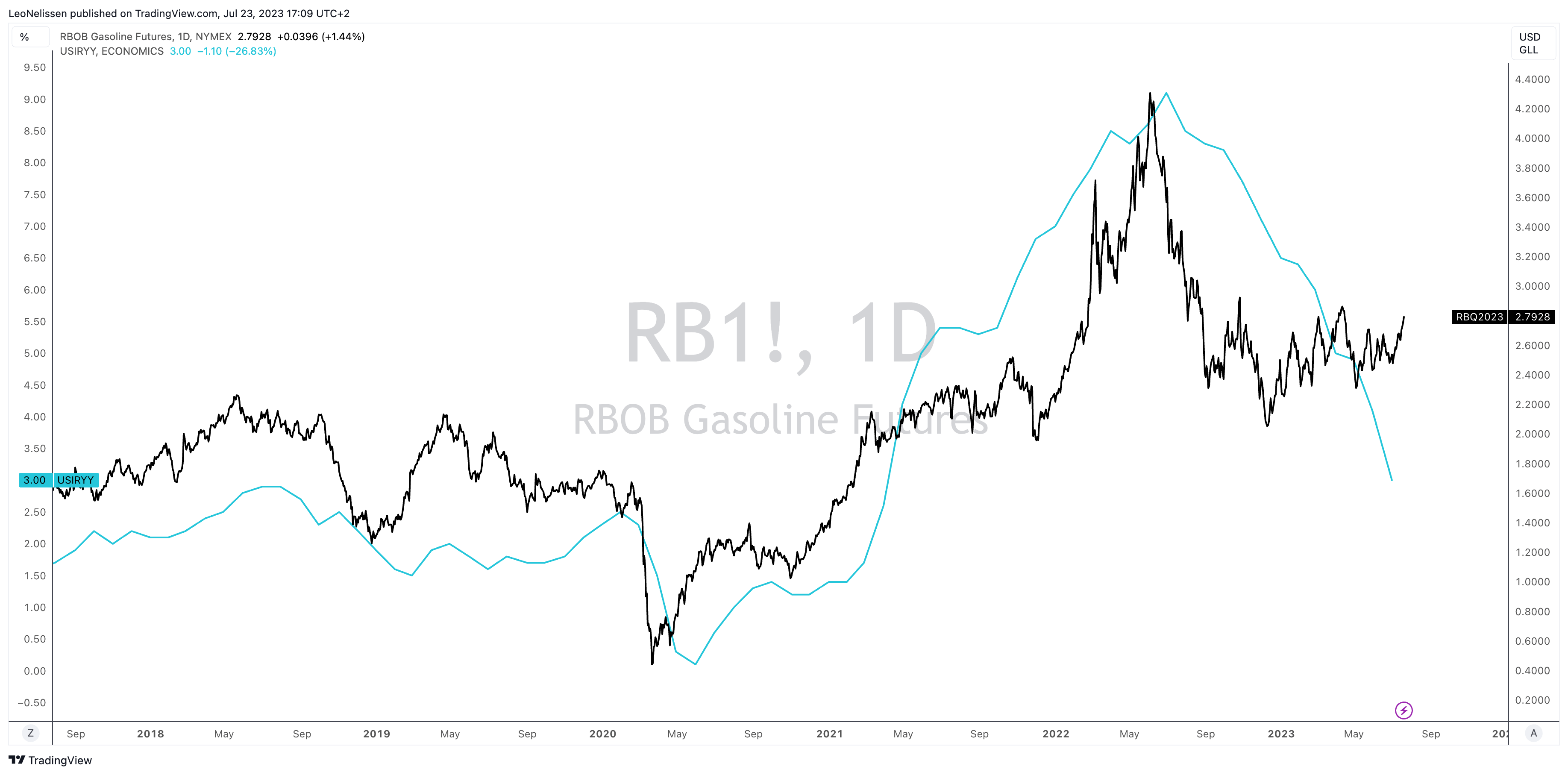

On top of that, we're seeing an increase in gasoline futures.

Looking at NYMEX RBOB gasoline futures, we see an upswing, which could be bad news for inflation (meaning: re-acceleration is likely).

{kind=link}

TradingView (NYMEX RBOB, All-Item CPI Y/Y)

I expect Valero to comment on this re-acceleration and unusual demand strength, given the broader economic weakness in its 2Q23 earnings call.

In 1Q23, the company already reported unusually strong numbers.

- Back then, net income was $3.1 billion or $8.29 per share, compared to $905 million or $2.21 per share for the first quarter of 2022.

- Adjusted net income for the same period was $3.1 billion or $8.27 per share, compared to $944 million or $2.31 per share in 2022.

- The Refining segment's operating income surged to $4.1 billion in the first quarter of 2023, supported by higher throughput volumes and lower natural gas prices.

On top of that, the company is ramping up its output in growth areas like renewable diesel.

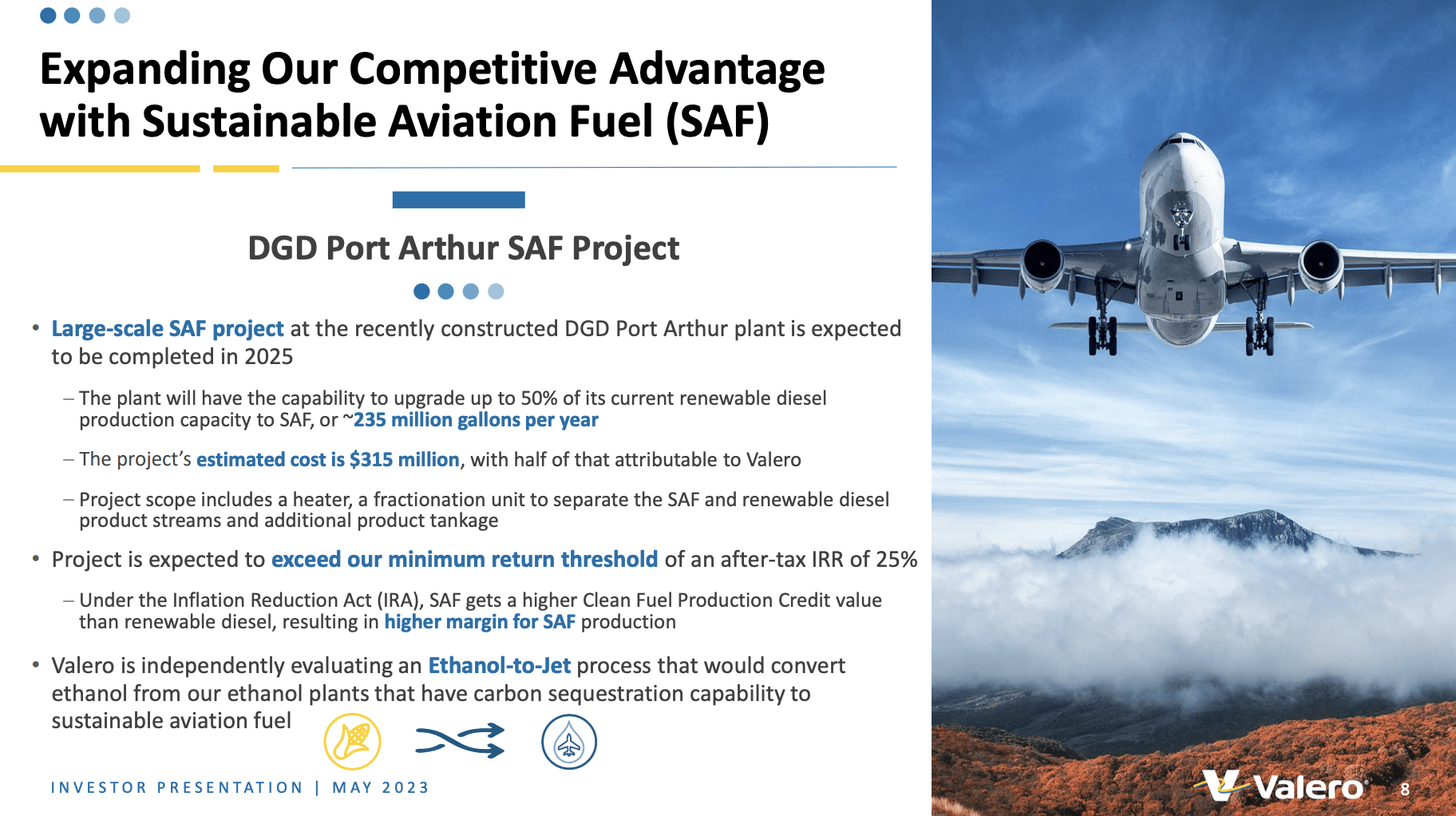

Valero's Renewable Diesel segment set a new sales volume record in the first quarter of this year, driven by the continued ramp-up of DGD Port Arthur, which started operations in November 2022.

{kind=link}

Valero Energy

The company also announced plans for a sustainable aviation fuel ("SAF") project at the Port Arthur plant.

This project aims to upgrade around 50% of the current 470 million-gallon annual renewable diesel production capacity to SAF. Upon completion in 2025, DGD is expected to become one of the world's largest SAF manufacturers.

{kind=link}

Valero Energy

Additionally, in 1Q23, the company commented that it expects refining fundamentals to remain strong, benefiting from low global light product inventories, tight supply/demand balances, and increasing product demand as air travel and summer driving season peak.

So far, all of these things are still tailwinds.

Good News For Shareholders

Roughly three years after the depths of the pandemic, Valero has a healthy balance sheet again. Bear in mind that it did not cut its dividend in 2020, which added additional debt to its balance sheet.

In the first quarter, Valero's focus on strengthening its balance sheet continued, with a reduction of $199 million in debt during the first quarter of 2023. The company ended the quarter with a net debt-to-capitalization ratio of 18%.

The net leverage ratio is now below 0.3x EBITDA, which supports the BBB credit rating (stable outlook).

While the company did not comment on future hikes, it made clear that it remains committed to its dividend.

In January, we announced an increase in our quarterly dividend on our common stock from $0.98 per share to $1.02 per share, demonstrating our long-standing commitment to stockholder returns. - VLO 1Q23 earnings call

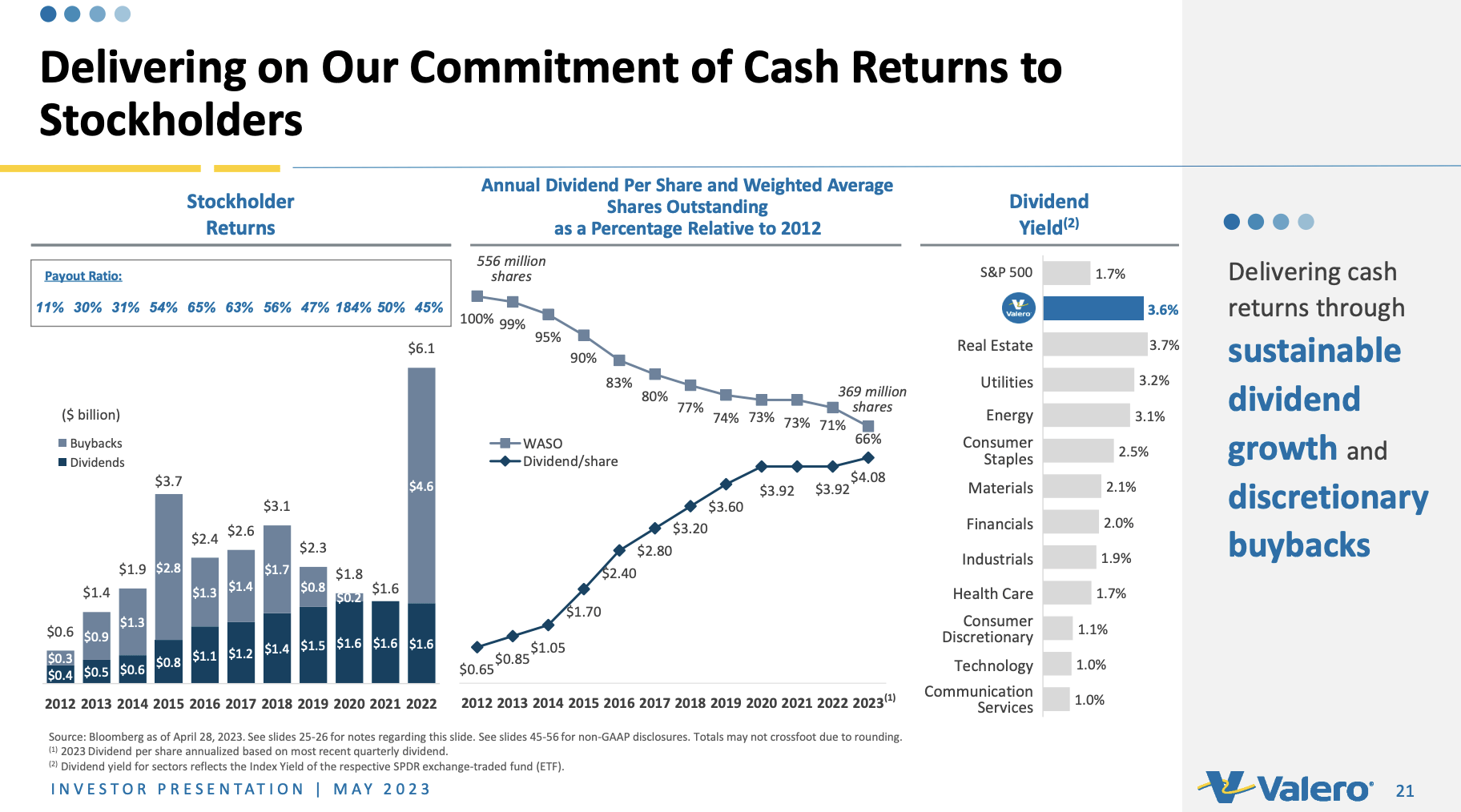

The stock currently yields 3.3% with an 11% payout ratio. The average annual dividend growth rate of the past five years is just 6%, which is caused by the pandemic. Going forward, I expect the dividend to be hiked way more aggressively.

While the payout ratio is low, the company is keeping the total payout ratio (including buybacks) close to 50%.

We returned over $1.8 billion to our stockholders in the first quarter of 2023, of which $379 million was paid as dividends and $1.5 billion was for the purchase of approximately 11 million shares of common stock [...] - VLO 1Q23 earnings call

Despite not buying back stock for two years, VLO has reduced its share count by 33% over the past ten years, which is truly remarkable and one of the reasons why this refinery giant is doing so well on the stock market.

Going forward, I expect some of these buybacks to make room for more aggressive dividend growth.

{kind=link}

Valero Energy

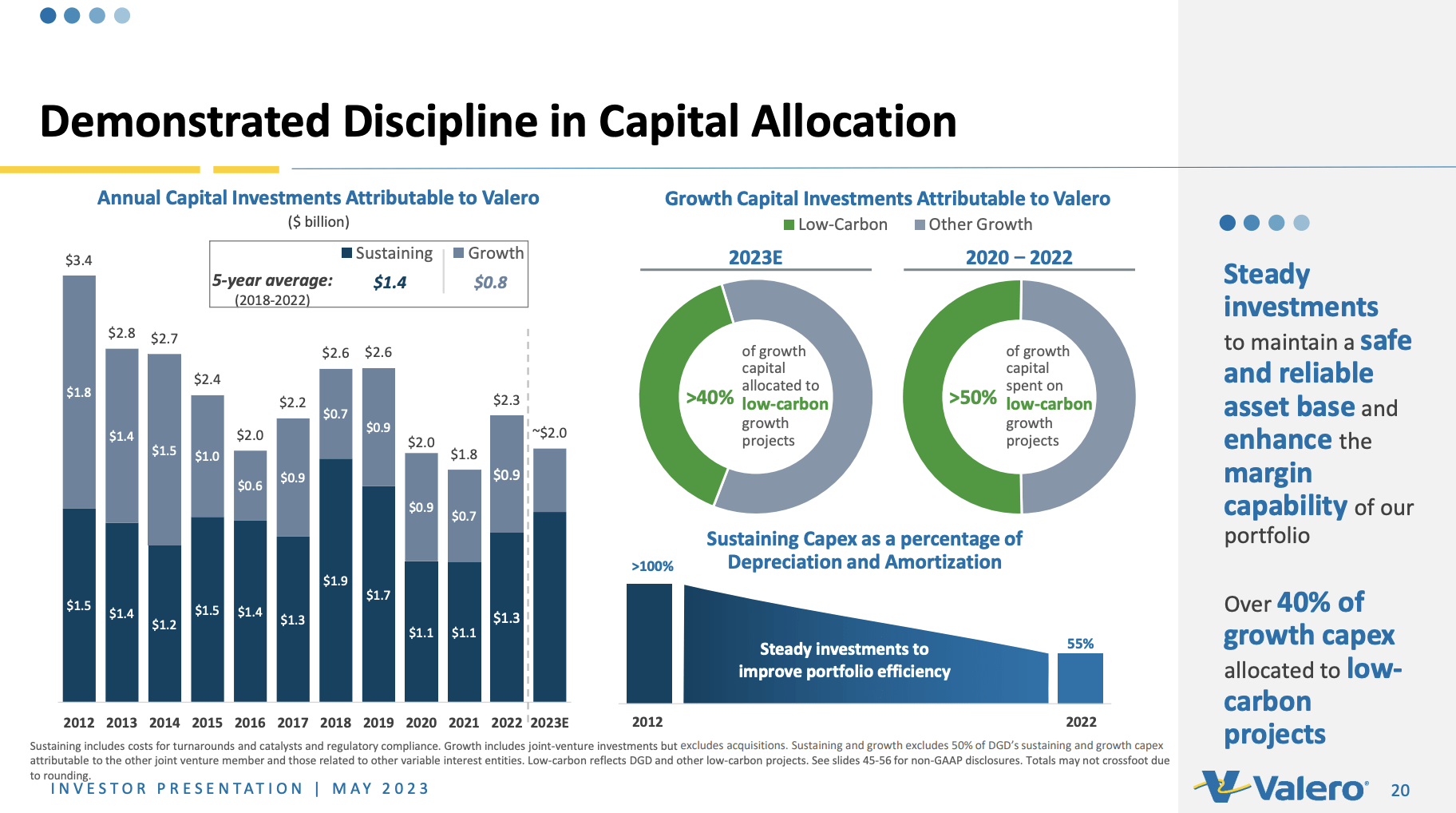

While I completely understand that Valero wants to prevent going into a future recession with an elevated payout ratio, the current payout ratio is so low that even temporary aggressive hikes would not put VLO in an uncomfortable spot.

{kind=link}

Valero Energy

It also needs to be said that the company is reducing growth CapEx, which leaves more room for free cash flow growth - especially if industry fundamentals remain healthy.

Valuation & 2Q23 Assumptions

Valero is scheduled to release its earnings on July 27 before the market opens. While the market expects an obvious decline in earnings after last year's blowout refinery margins, the company is expected to generate strong earnings.

The current consensus is $5.08 per share, which I expect the company to beat if history and current developments are any indication. In general, I believe that its industry is stronger than people expect, which could pave the way for a surprise.

{kind=link}

Nasdaq

It also needs to be said that the bar has been lowered. Over the past four weeks, the company has gotten four earnings downgrades and one upgrade. The current EPS forecast is based on six estimates.

Having said that, the VLO valuation remains extremely attractive.

The company is expected to generate $8.3 billion in free cash flow this year, which translates to an 18.7% free cash flow yield. Although new global supply is expected to reduce that number to $5.8 billion in 2024 (13.1%), it is still indicative of aggressive buybacks and a lot of room to boost the dividend.

If we apply a conservative 10x multiple on next year's FCF estimate, we get 31% undervaluation. I think the same case can be made when looking at the EV/EBITDA multiple.

The current consensus price target is $140, which is 13% above the current price. Needless to say, I'm more bullish than that and agree with the $160 price target the company got from BMO Capital Markets in January.

However, I do not expect the stock to take off past $160 without support from economic growth indicators.

Once economic demand bottoms, I believe we could be looking at much higher prices, as it would put a floor under free cash flow and likely come with the aforementioned rotation from growth back to value.

Takeaway

Valero Energy is a compelling choice for dividend investors due to its strong position in the refining industry and its ability to generate consistent shareholder value. The industry is experiencing healthy fundamentals with high refinery utilization rates and strong demand for gasoline and distillate fuels, leading to favorable tailwinds for VLO.

The company is also showing promising signs of an uptrend, benefitting from the rotation from growth to value. With a focus on strengthening its balance sheet and a commitment to maintaining and potentially increasing dividends, VLO remains attractive to shareholders.

Moreover, its aggressive share buybacks have contributed to remarkable stock market performance.

Looking ahead to the upcoming 2Q23 earnings, the company is expected to generate strong earnings, further supporting its undervaluation. While the market expects a decline in earnings from the previous year's exceptional performance, the company has the potential to surprise and exceed expectations.

Considering VLO's attractive valuation and ample room for dividend growth, I believe the stock has the potential to outperform, especially once economic growth indicators provide further support.

For further details see:

Dirt Cheap - Why I'm Buying Valero Ahead Of Earnings