TFC - Disaster Or Opportunity: It's All A Matter Of Truist

2023-03-16 11:02:56 ET

Summary

- The article discusses a number of indicators that the current situation is quite different than it was 15 years ago, and attempts a few words of reason.

- Although the situation is serious, I don't think it's reasonable to expect a nationwide bank run that will bring down "smaller" regional banks like Truist Financial Corporation or U.S. Bancorp.

- I will be analyzing Truist Financial Corp. stock in depth, which I believe has a compelling risk/reward ratio. A look at TFC's preferred stock is quite reassuring in this context.

- In addition, I explain my own portfolio strategy - after all, I recently opened a position in Truist Financial Corp. and U.S. Bancorp.

Introduction - The Bear Is Growling

Since the collapse of SVB Financial Group (SIVB) last week, investors are focused on one aspect in particular: the available-for-sale ((AFS)) and held-to-maturity ((HTM)) portfolios of banks that are underwater due to interest rates rising at an unprecedented pace. The higher interest rates rise, the lower the value of bonds already outstanding. I explained this risk - which is particularly elevated for bonds with very long maturities - in detail in an article I wrote in October 2022 .

As banks (and other financials such as insurance companies) have been de facto forced to buy low-yielding, high-quality bonds such as U.S. Treasuries, in part due to increasingly stringent capital requirements , they now face unrealized losses (reported as other comprehensive income) that could be forcibly realized in the event of a bank run. Selling AFS and HTM assets at a loss can quickly bring a bank's Common Equity Tier 1 ((CET1)) capital to dangerously low levels. SVB suffered from over-exposure to unprofitable startup tech companies, forcing it to sell a portion of its securities portfolio to Goldman Sachs ( GS ) at fair value, thereby realizing a net loss of $1.8 billion.

Admittedly, the narrative of a chain reaction and systemic event due to a severe loss of confidence in the banking system sounds conclusive, especially considering our fractional reserve system and the Federal Deposit Insurance Corporation ((FDIC)) being able to cover only a little over 1% of insured deposits. Knowing that SVB was the 16th largest bank in terms of total assets (about $200 billion) and that other regional banks such as U.S. Bancorp ( USB , $580 billion) or Truist Financial Corporation ( TFC , $550 billion) are among the banks with the highest percentage of unrealized losses (page 2 of this J. P. Morgan report ), a theoretical endgame could be a self-reinforcing cycle in which depositors withdraw their savings from regional banks, which could lead to a systemic collapse. A less severe scenario could be seen in a secular trend toward global systemically important banks such as JPMorgan Chase & Co. ( JPM ), Bank of America Corporation ( BAC ), or even Citibank Inc. ( C ), further straining the deposit structure of regional banks.

So, the bear case is clear, and the situation is definitely serious. But are we really on the brink of disaster?

A Few Words Of Reason

Following the collapse of SVB and the subsequent takeover of Signature Bank ( SBNY ) by New York's Department of Financial Services, the Federal Reserve acted quickly to announce the Bank Term Funding Program ((BTFB)). It offers short-term loans to banks and other financial institutions for which they post Treasuries and other assets as collateral, which will be valued at par. This is good news, as it is an easy-to-understand measure that strengthens depositors' confidence. Also, it should be remembered that smaller banks such as TFC, USB, The PNC Financial Services Group, Inc. ( PNC ), and Capital One Financial Corporation ( COF ) must participate in the Federal Reserve's stress test and, as Category III institutions, must meet fairly high regulatory standards.

Of course, the recently announced BTFB is just another word for quantitative easing ((QE)) "light," and it essentially confirms how fragile our banking system is. However, confidence and trust are the most important aspects that keep our fractional reserve system intact, so it is important to welcome such measures.

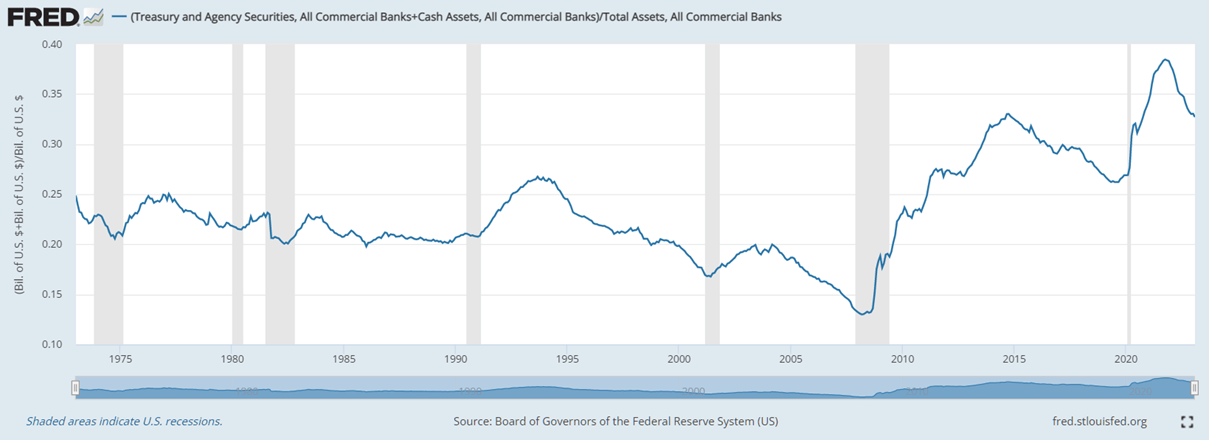

I think often overlooked, and especially in difficult times like these, is the fact that banks are capitalized very differently today than they were before the Great Recession. The stress-absorbing capacity of banks is much higher today than it was in 2008, as evidenced, for example, by the share of bank assets held in Treasuries and cash as a percentage of total bank assets (Figure 1).

Figure 1: Percentage of total bank assets held in Treasuries and cash assets as a percentage of total bank assets (USGSEC + CASACBW027SBOG) / TLAACBW027SBOG; note that 1 on the y-scale means 100% (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

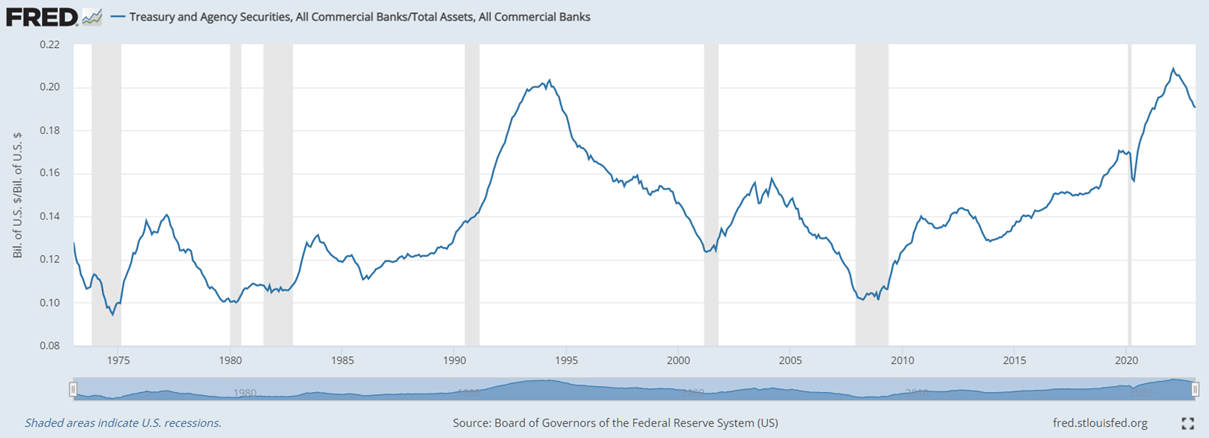

The share of Treasuries on commercial bank balance sheets increased from a low of 10% of total assets (e.g., 1975, 1980, and 2008) to over 20% in March 2022 (Figure 2). It is interesting to note that the local or global minima usually coincided with a recession.

Figure 2: Percentage of total bank assets held in Treasuries; note that 1 on the y-scale means 100% (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

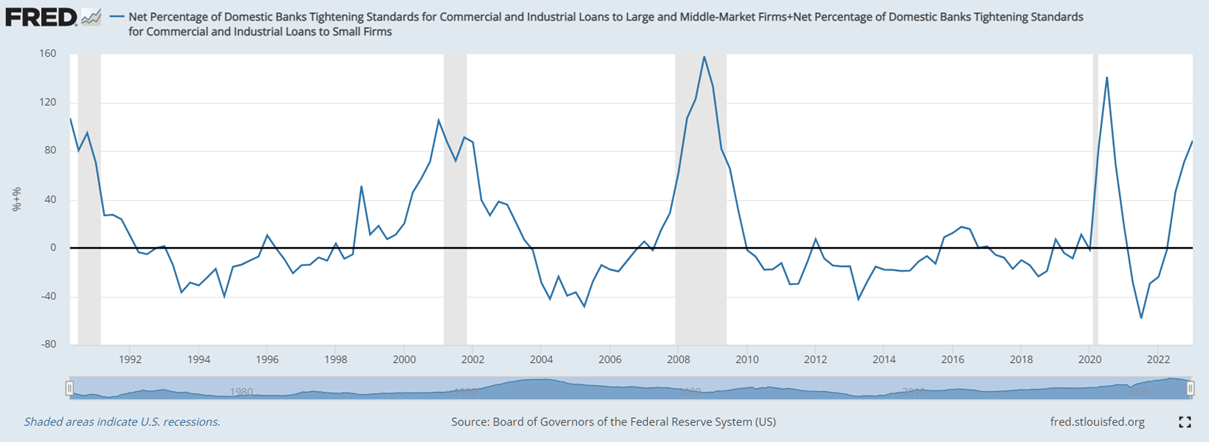

Another aspect worth considering is that lending standards (Figure 3) are quite different than they were before the Great Recession or before the Dot Com bubble burst. As a result of government-mandated measures to contain the spread of SARS-CoV-2 beginning in early 2020, banks tightened their lending standards and relaxed them when the measures subsided and the U.S. "reopened." Emergency loans and companies drawing on their revolving facilities when they scrambled for cash in the wake of the economic shutdown are nicely illustrated by the increase in Figure 5.

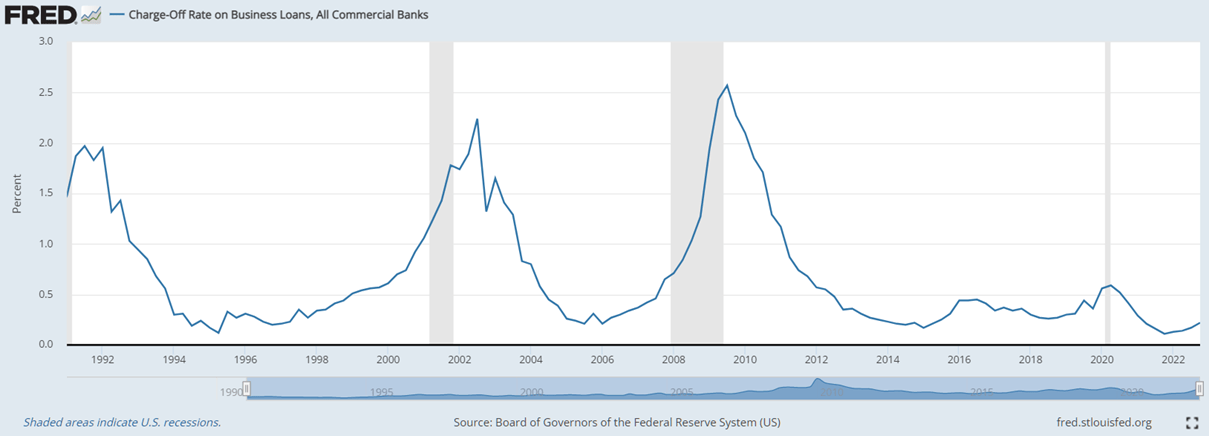

Since the third quarter of 2021, however, lending standards have been tightening again, but from a position of relative strength, unlike in 2000 and 2008. The housing market is also very different today than it was 15 years ago. Individuals who have purchased homes in recent years will confirm that the days of very low or no down payments are far behind us. Collateralized loan obligations, including loans to potential subprime companies (i.e., unprofitable startups or outright zombie companies - see my related article ), are a different story and could pose a systemic risk, but the matter requires more study before any definitive conclusions can be drawn regarding a 2008 2.0. A community member here on Seeking Alpha has kindly shared a highly interesting congressional hearing on the subject. In any case, the charge-off rate on business loans looks quite reassuring (Figure 4), but of course it can only be taken as a very rough guide and should also be viewed in the context of potentially intact pandemic-related loan moratoria.

Figure 3: Net percentage of domestic banks tightening standards for commercial and industrial lending to small, middle and large market firms; DRTSCILM + DRTSCIS (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

Figure 4: Charge-off rate on business loans; CORBLACBS (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

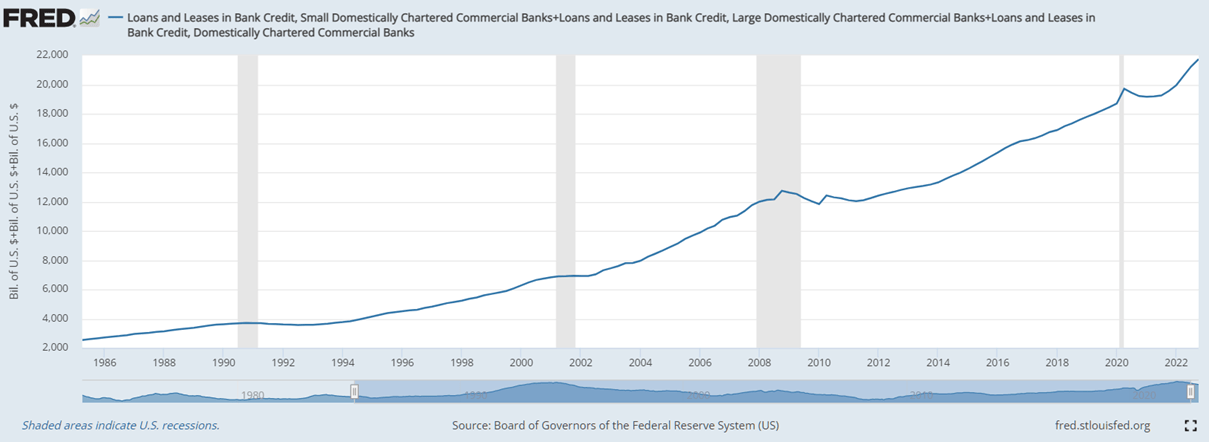

Finally, I think it is important to recognize that bank lending remains strong (Figure 5). A closer look shows that there is a feeble deceleration since mid-2022, and a recession is likely to put further pressure on lending, but things are definitely not as gloomy as is often reported.

Figure 5: Lending activity; LLBSCBW027SBOG + LLBLCBW027SBOG + LLBDCBW027NBOG (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

Although consumers are under pressure from high inflation and rising mortgage rates, I still think the situation is quite robust, at least that is my impression when I read the earnings reports of companies like The Home Depot, Inc. ( HD ) or Lowe's Companies, Inc. ( LOW , see my recent article ). Of course, discretionary spending on durable goods has been declining for some time, confirming a deterioration in consumer sentiment. This is easily seen, for example, in the earnings reports of Leggett & Platt, Incorporated (LEG), a supplier of bedding, furniture, and industrial components that I cover regularly .

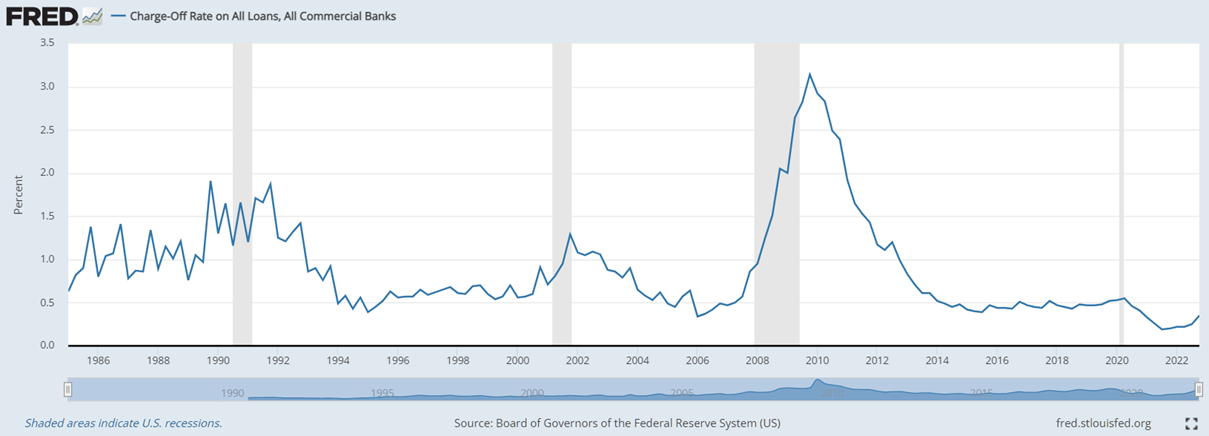

To conclude this FRED graph marathon, consider the charge-off ratio for all loans across all commercial banks (Figure 6). Of course, the same caveats as above apply, but I think there is something to be said for not acting from a position of weakness.

Figure 6: Charge-off rate on all loans; CORALACBN (Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis)

{kind=link}

Making The Case For Regional Banks -Truist Financial Corp. Stock

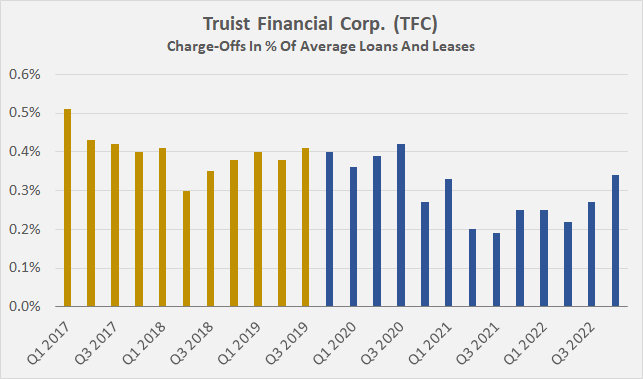

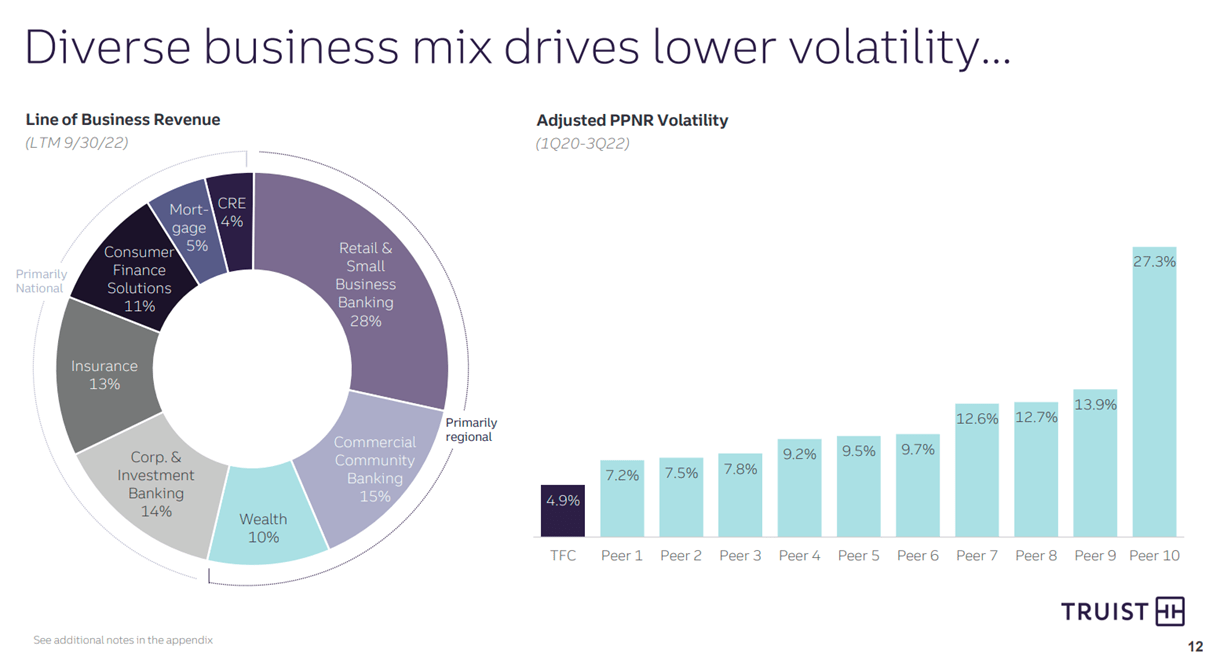

TFC, as an example of a fairly large regional bank - the seventh largest in the U.S. by assets - is no different when it comes to charge-offs (Figure 7). They are increasing, of course, but I think the bank has a well-diversified portfolio with a very manageable risk profile (Figure 8).

Figure 7: Truist Financial Corp. [TFC] charge-offs on a quarterly basis; note that yellow color indicates pre-merger data when Truist was still BB&T (own work, based on the company's quarterly earnings press releases) Figure 8: Truist Financial Corp. [TFC] line of business revenue, as of September 30, 2022 (Slide 12, Truist Goldman Sachs 2022 US Financial Services Conference; https://ir.truist.com/events-and-presentation?item=50)

{kind=link}

{kind=link}

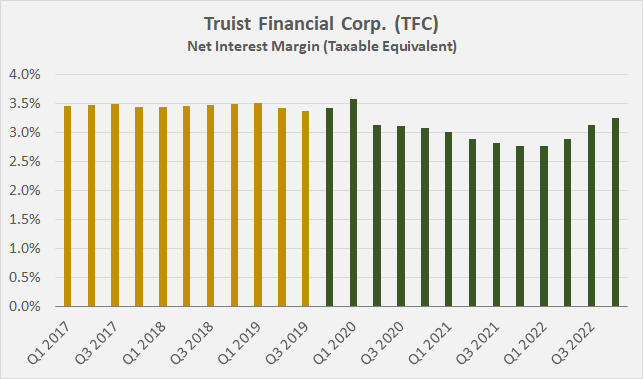

Truist's net interest margin has been trending up for several quarters (Figure 9). Taking deposits at a rate of 0.66% (Q4 2022, up 33 basis points QoQ) and lending at rates of 4% or more is obviously a much better situation than it was a year or two ago.

Figure 9: Truist Financial Corp. [TFC] net interest margin; note that yellow color indicates pre-merger data when Truist was still BB&T (own work, based on the company's quarterly earnings press releases)

{kind=link}

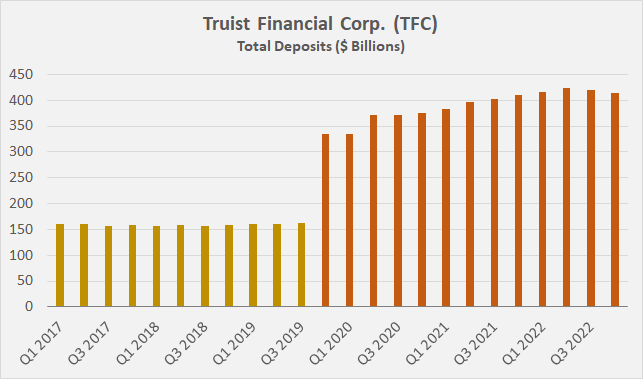

But it's not just lending rates that have improved. Truist, through its reserves held at the Federal Reserve, benefits from a de facto profit of currently around 4% thanks to the rising IORB (Interest Rate On Reserve Balances), which is currently at 4.65% . Of course, one must keep in mind the inverted yield curve (negative margin for mismatched maturities lending) and the increasing pressure on deposits as holders look for a better deal. With the growing uncertainty, deposit holders will likely seek to move some of their savings to "too big to fail" institutions such as JPM, BAC, or C. According to a report , BAC saw inflows of about $15 billion in new deposits in recent days. While that sounds like a lot, it should be viewed in relation to deposits at Category III banks. For example, Truist reported average total deposits of more than $413 billion for the fourth quarter of 2022 (Figure 10). After a more or less steady increase following the merger of merger of BB&T and SunTrust in late 2019, deposits declined for the first time in Q3 and Q4 2022, at sequential rates of 0.9% and 1.6%, respectively.

Figure 10: Truist Financial Corp. [TFC] total deposits, average quarterly numbers; note that yellow color indicates pre-merger data when Truist was still BB&T (own work, based on the company's quarterly earnings press releases)

{kind=link}

Of course, a bank run would be devastating, but I do not think it is plausible to assume a nationwide bank run as a baseline scenario. In such a scenario, all banks would probably be more or less the same; after all, banks operate with a fractional reserve system. Bank runs, and thus bank failures, are an extreme tail risk that I think would be very difficult to manage in a portfolio (maybe with physical precious metals) - the resulting problems would be so devastating that the wipeout of Truist (and other banks') shareholders is probably one of the least of our worries.

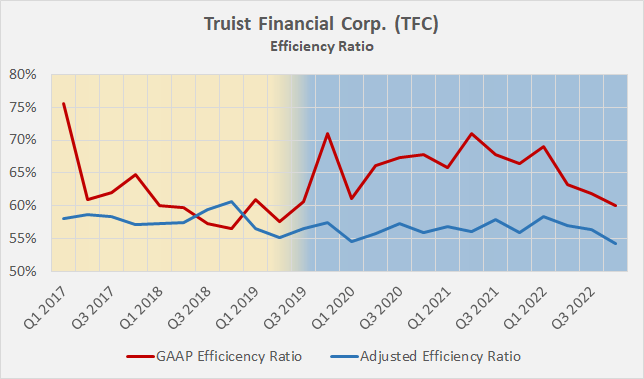

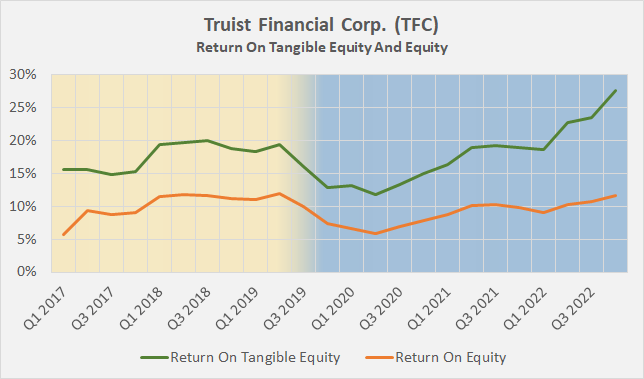

Apart from this risk, I believe that Truist is a solid Category III bank according to its capital and stability ratios. The integration of the merger came at an extremely unfortunate time - in the middle of the pandemic - but I think the integration is finally bearing fruit, as can be seen in the declining efficiency (Figure 11) and rising profitability ratios (Figure 12). Of course, some of the improvement is due to rising interest rates and thus rising profits.

Figure 11: Truist Financial Corp. [TFC] GAAP and non-GAAP efficiency ratios; note that yellow color indicates pre-merger data when Truist was still BB&T (own work, based on the company's quarterly earnings press releases)

{kind=link}

Figure 12: Truist Financial Corp. [TFC] return on average tangible common shareholders' equity and average common shareholders' equity; note that yellow color indicates pre-merger data when Truist was still BB&T (own work, based on the company's quarterly earnings press releases)

{kind=link}

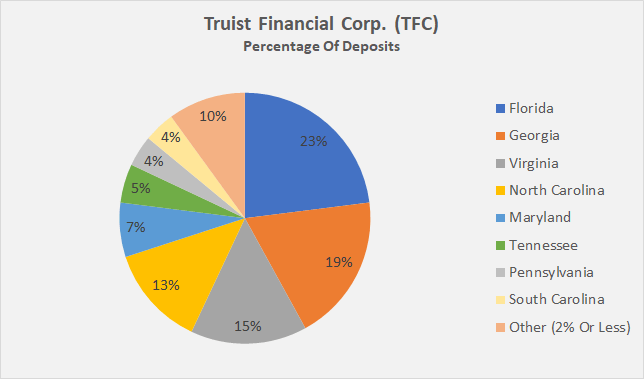

What I really like about Truist is its regional exposure to the southeastern U.S., which is characterized by favorable population growth. Truist's deposits in Florida, Georgia, Virginia and North Carolina together account for about 70% of total deposits, and the bank has third, first, second, and first deposit market share in those states, respectively (Figure 13). Of the approximately 2,100 branches, approximately 61% are located in Florida, Georgia, Virginia, and North Carolina.

Figure 13: Truist Financial Corp. [TFC] regional distribution of deposits (own work, based on the company's 2022 10-K)

{kind=link}

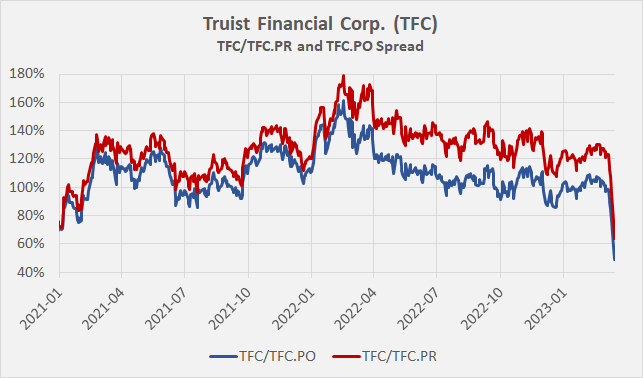

Finally, I would like to briefly mention TFC's preferred stock. If Truist were in acute danger of failure, why are the preferred shares (TFC.PI) and (TFC.PR) still trading near their October 2022 lows? In a liquidity event that breaks the bank's neck, the common stock, preferred stock, and likely also debt securities will become worthless. From this, I conclude that holders of common stock think differently than holders of preferred stock (or even bondholders). I think the issue is best illustrated by looking at the spread between TFC.PI and TFC, and TFC.PR and TFC (Figure 14). As a new holder of TFC common stock, I find this chart pretty reassuring. In addition, I think it is worth noting that Truist and others like U.S. Bancorp were not among the six banks put on downgrade watch by Moody's. However, investor service Morningstar raised its uncertainty rating on Truist from medium to high, citing:

Another source of uncertainty is related to regulatory pressure. Nothing is official yet, but we would not be surprised if regulators create rules that crack down harder on those banks that have the largest unrealized losses on their securities portfolios. This is why we've added Truist into the High Uncertainty Rating mix, as the bank has a higher unrealized loss percentage than peers, even as we admit the bank screens better on the estimated percentage of deposits at risk (42% versus an average of 47%), and so is perhaps in a better position to defend its deposit base.

Nevertheless, Morningstar has not changed its fair value estimate of $57 (a 44% discount at the time of writing).

Figure 14: Spread between Truist Financial Corp. common stock [TFC] and TFC.PO and TFC.PR preferred stock (own work, based on the daily adjusted closing price of the mentioned securities)

{kind=link}

Conclusion

I do not want to be misunderstood with this article - the situation is serious and a policy mistake could have serious negative consequences. However, considering that our banking system is a fractional reserve system that depends entirely on depositor confidence, I do not think it is realistic to assume a devastating run on regional banks. A nationwide bank run that could bring down even large regional banks like Truist Financial Corporation or U.S. Bancorp would lead to far more serious problems than the current ones, and I would go so far as to conclude that the Federal Reserve would do literally anything to prevent a systemic event. Also, I think the macro indicators in this article have shown that the situation is very different today than it was 15 years ago. Lending standards have been tightened, charge-off rates are still very low (however, keep in mind possible pandemic-related moratoria), bank capitalization is much stronger, and lending - although showing signs of deceleration - is still growing strongly.

In order to contain the current situation, the Federal Reserve announced a kind of "soft QE" with the Bank Term Funding Program, which I think was an important step in the right direction to strengthen confidence in our banking system. However, the collapse of SVB et al. showed how fragile our system is and that the Federal Reserve cannot continue to raise interest rates at the current pace. I think we will have to get used to inflation staying higher for longer for several reasons. The market is currently undecided on what the Fed will do on March 22. A 50 basis point hike is no longer expected, and perhaps the fed funds rate will be left (temporarily) at 450 to 475 basis points - the odds of that are currently 50/50, according to the CME's FedWatch tool.

To contain the current situation, the Federal Reserve announced a form of soft-QE via the Bank Term Funding Program, which I think was an important step in the right direction to inspire confidence in our banks. However, the collapse of SVB et al. has demonstrated the fragility of our system and that the Federal Reserve cannot continue to raise interest rates at the current pace. I think that we will need to get used to the fact that inflation will remain higher for longer for several reasons. The market is currently undecided about what the Fed will do on March 22. A 50 basis point hike is no longer expected, and maybe the Federal target rate will be (temporarily) maintained at 450 to 475 basis points - the current odds are 50/50 according to the CME's FedWatch Tool .

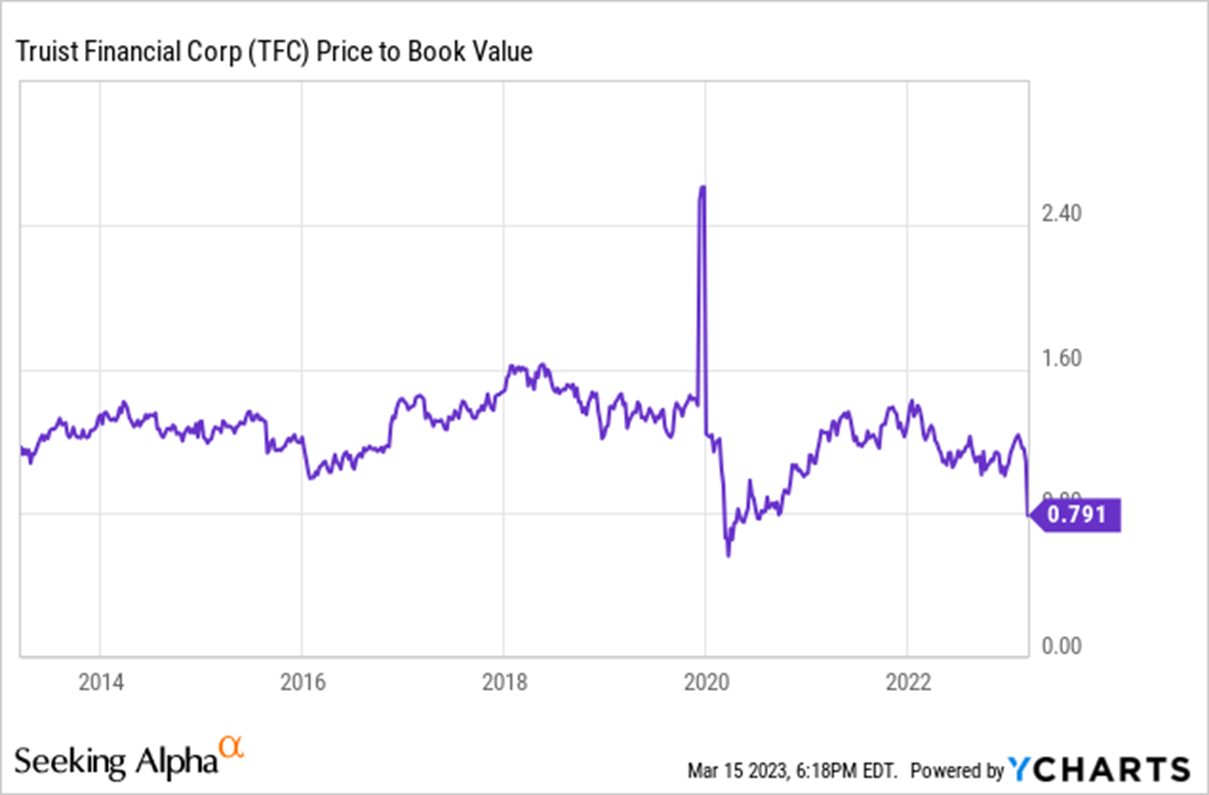

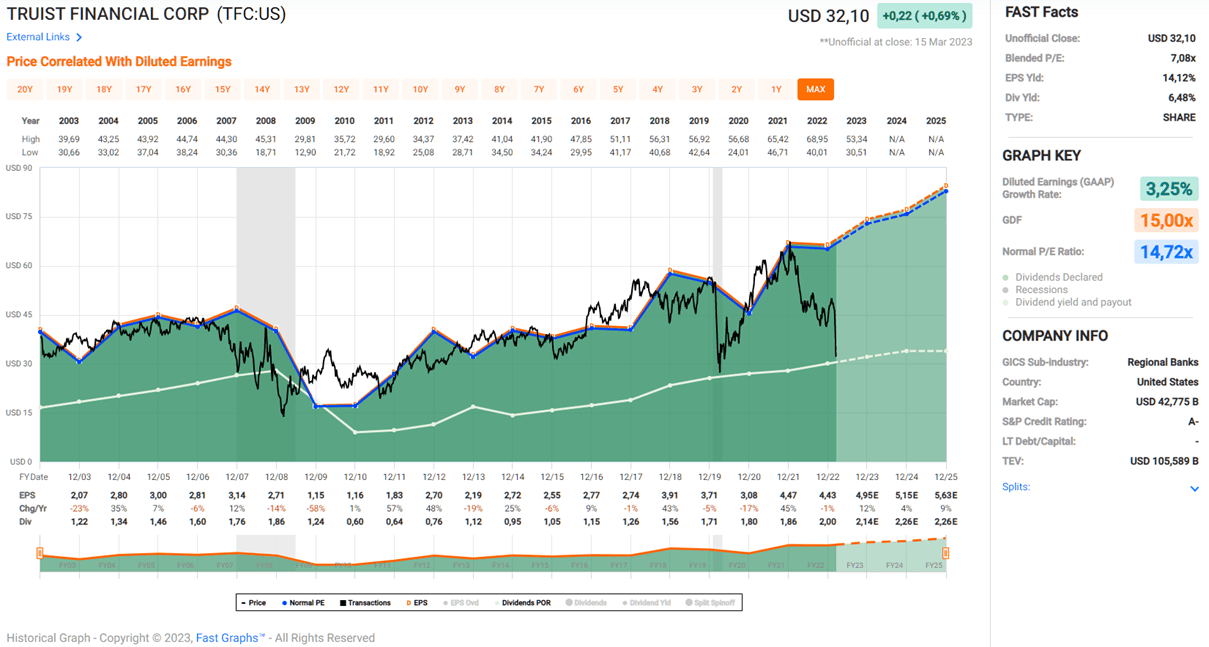

In this article, I not only provided an overview of the current situation from a macro perspective, but also took a closer look at Truist Financial Corp., the seventh largest bank in the United States. In my opinion, aside from the now-familiar bear case associated with relatively large unrealized losses, there are many positives about Truist. It is solidly profitable, has a well-diversified loan portfolio, and the merger integration is finally bearing fruit. It is a $500 billion Category III bank with a current market capitalization of $42 billion. It operates in demographically favorable regions and also owns an often-overlooked insurance business, of which it recently announced the sale of a 20% stake at an attractive adjusted 27x earnings multiple, valuing the entire business at $14.8 billion - certainly not what I would consider a fire sale price. TFC stock currently trades at a price-to-book ratio of less than 0.8 (Figure 15) and offers a dividend yield of 6.5%. A blended price-to-earnings ratio of about 7 (Figure 16) also looks very compelling to me, as does the 44% discount to Morningstar's fair value estimate.

Figure 15: Price-to-book value of Truist Financial Corp. [TFC] (generated with Y-Charts)

{kind=link}

Figure 16: FAST Graphs chart of Truist Financial Corp. [TFC] based on adjusted operating earnings (obtained with permission from www.fastgrpahs.com)

{kind=link}

For regional banks, I see the bear case in an increased risk that they will be under competitive pressure to raise interest rates to keep deposit outflows in check. In this context, I doubt that the larger institutions like U.S. Bancorp, Truist, and PNC Financial Services are in much trouble.

I have opened a small position in Truist (and also in U.S. Bancorp), which I will be adding to over the next few weeks. I think it makes perfect sense to focus on the better regional banks in a diversified portfolio, due to a favorable risk-reward ratio. I don't think investing 2% of total portfolio value in such companies is an overly risky proposition - at least I'm comfortable with such an allocation, knowing that less than half a year of dividend income will be enough to offset the loss if these companies go under.

However, I don't think it's realistic to expect banks like U.S. Bancorp and Truist to falter. If one expects such a situation, one should ask whether it is fundamentally right to invest in stocks (and other financial assets) in the first place. After all, those who invest in financial assets trust the financial system on a daily basis. It is faulty logic to be overly bearish on banks on the one hand, and on the other hand, to maintain accounts with banks and brokers that hold assets on our behalf. Of course, there is asset segregation, but I imagine it will be an extremely unpleasant time until the bankruptcy trustee sorts out all the bank's assets, clients' assets and other claims.

As always, please consider this article just a first step in doing your own due diligence. The situation is serious, and I think it warrants a more in-depth investigation, especially with regard to leveraged business loans and other potential concentration risks.

Thank you for taking the time to read my article. Regardless of whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments section below. And if there is anything you would like me to improve or expand upon in future articles, drop me a line as well.

For further details see:

Disaster Or Opportunity: It's All A Matter Of Truist