DISH - DISH Network: Why It Could Be A Gamble To Invest Right Now

2023-05-26 11:40:14 ET

Summary

- The company has been losing value for the longest time.

- Does it have any potential in such a competitive environment?

- Outlook seems promising, however, it’s too early to tell if the shift will bear fruit in the end.

- Financials reveal a company that is struggling to stay relevant.

- I’ll stay away for now until the company proves itself.

Investment Thesis

I wanted to take a look at DISH Network Corporation ( DISH ) which has seen a massive deterioration of its share price in the past 5 years, due to losing Pay-TV subscribers to many streaming services available for a good price. I wanted to see what it is doing to stay in business in the future and if the drop in the share price has been warranted. I think right now with the potential that the company has; the share price depreciation has been warranted because the growth catalysts have not been reached yet, and the company continues to bleed subscribers even losing its subscriber base on its streaming service. At this point, I will assign a hold rating until DISH can prove that it can shift its business strategy towards wireless networks and rejuvenate its TV offerings.

I like to look at companies that used to be big players in their sector to see what they are still up to if they managed to find a new area where they can thrive, or if they are on the brink of extinction. In the past, I covered Nokia ( NOK ) where I saw that it managed to shift its business model completely, and it has good potential ahead of it now, which has not been realized by investors yet, which is a shame. Another one was Xerox (XRX). It didn't look like they are innovating enough to keep going for much longer but are still kicking.

Now it's time to look into DISH and what is it going to do to stay in business for the foreseeable future.

Outlook

It is not very surprising that the company lost around 78% of its value in the last 5 years. The company has been bleeding subscribers in every quarter reported. It still is generating a lot of revenue every year, around $12B. It's safe to say that it won't lose all of that revenue overnight, but if it keeps losing to the competition, I could see this revenue dwindling further.

I would have thought maybe their Sling TV segment would have more potential, but that is not the case also, as it has been losing subscribers for many quarters. There are many better alternatives to what DISH is offering out there these days, with more and more people being connected to the internet to enjoy their shows, sports and other entertainment on demand is amazing and if the company isn't going to do something about it, I believe it will keep losing revenue at alarming rates.

It seems to me they are shifting their business model quite a bit, just like Nokia did when their phones became obsolete and couldn't keep up with the competition and went into the 5G network business, just like DISH is doing right now. 5G coverage is being pushed out at much faster rates than just a few years ago. DISH is building out its 5G network sites to stay relevant and rejuvenate revenue growth. The company needs to be able to cover 70% of the US population by mid-June of this year and if they do not succeed in that, they will be subject to penalties and will be able to extend that deadline by two years. The company has started to build around 15,000 extra network sites as of December 31st, '22, if they complete these, the company will reach 60% of coverage. DISH aims to complete 1,000 sites a month , so it looks like they will miss that deadline by quite a bit and the deadline will be extended automatically, as long as they reach coverage of 50% by that time.

It's tough for DISH to secure funding at home. The CEO has recently flown to Dubai for assistance in building its 5G network. Charlie Ergen has said that it's due to investors not liking the leverage they have on their books, and I don't blame them. I will go into more detail on debt in the financials section.

DISH is the fourth-largest wireless provider, which doesn't say much because, compared to the biggest ones like AT&T (T) and Verizon (VZ), which have 217m and 143m subscribers respectively, while DISH with its 7.9m subscribers as of the latest quarter seems tiny in comparison. There are talks that DISH will start to sell phone plans through Amazon (AMZN) to extend its reach, however, nothing has been confirmed yet, so we will have to see what happens, as both sides did not provide any further details on the matter. The stock price saw a massive jump on this news, which suggests to me that investors are looking for hope of a turnaround. I don't think that this news warranted such a jump in the price and will come back down in the next couple of weeks.

It's hard to know how much more revenue this segment will generate for the company as it is still in the very early stages. I like to invest in companies that already have been growing consistently in their respective segments and have not been losing revenue y-o-y.

In summary, if the company is not able to stop the bleeding in its biggest revenue generator segment and 5G networking is not going to become a catalyst for revenue rejuvenation, I think the company will continue to go down in value, but if it can successfully shift its business to 5G as Nokia did, it could have a future yet, however, only time will tell.

Financials

The company had $2.2B in cash and around $300m in short-term investments against a whopping $20B in long-term debt as of Q1 '23. This kind of leverage may keep a lot of investors on edge and may keep them away from investing in the company. Is it actually a problem, though? At the end of FY22, the company paid almost $23m in interest expenses, while their short-term investment income came in at $42m, which more than offset the annual interest on the debt. In fact, EBIT covers the interest expense around 48 times as of FY22. The company is not in trouble because of its high debt amount as it looks very manageable.

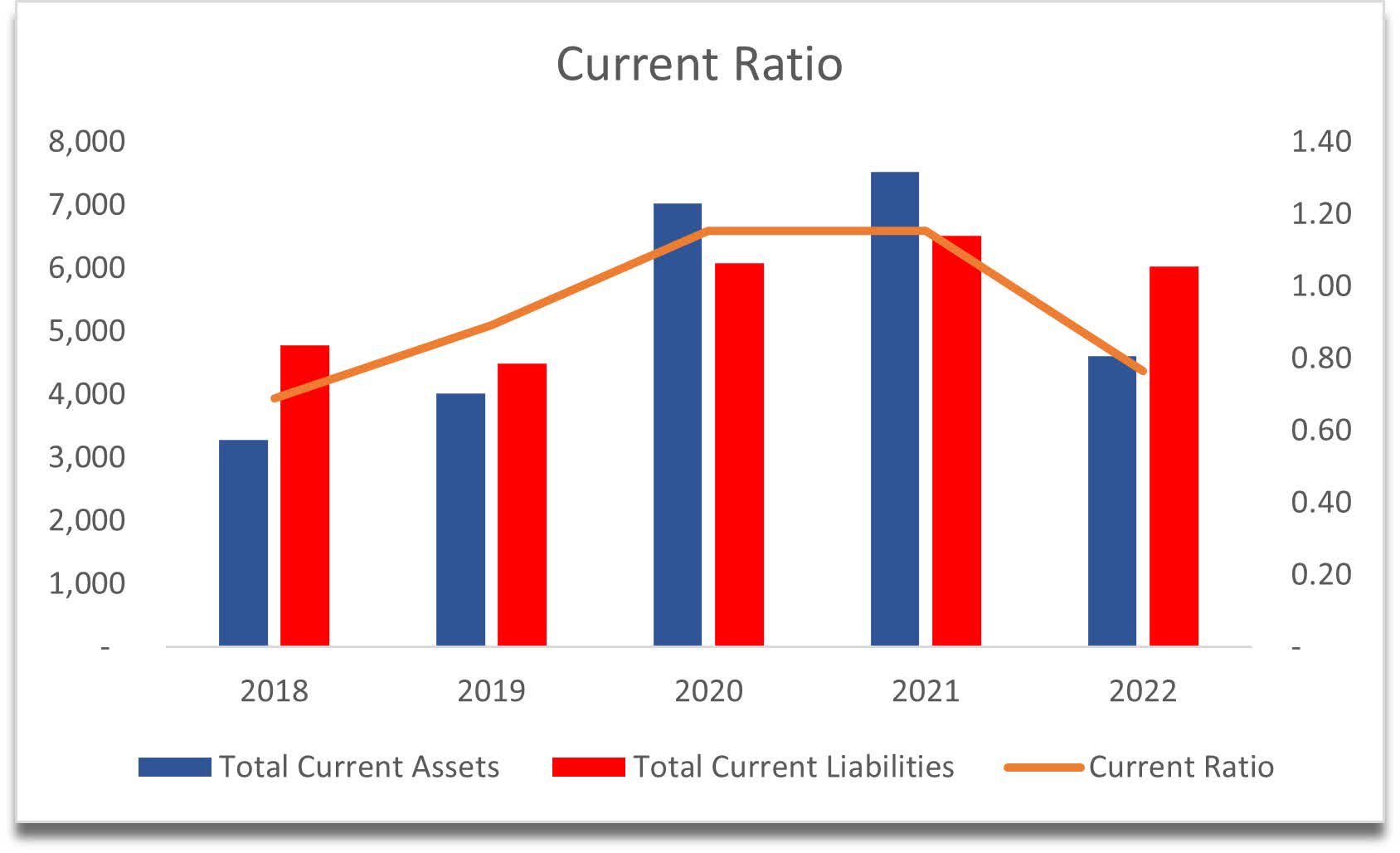

Continuing with liquidity, the company's current ratio dipped below 1 at the end of FY22, which can be explained by the company's short-term investments going down by $2.1B. I don't believe this to be an issue because the company can generate a lot of cash flow. I would prefer companies to have at least a 1.5 current ratio, however.

{kind=link}

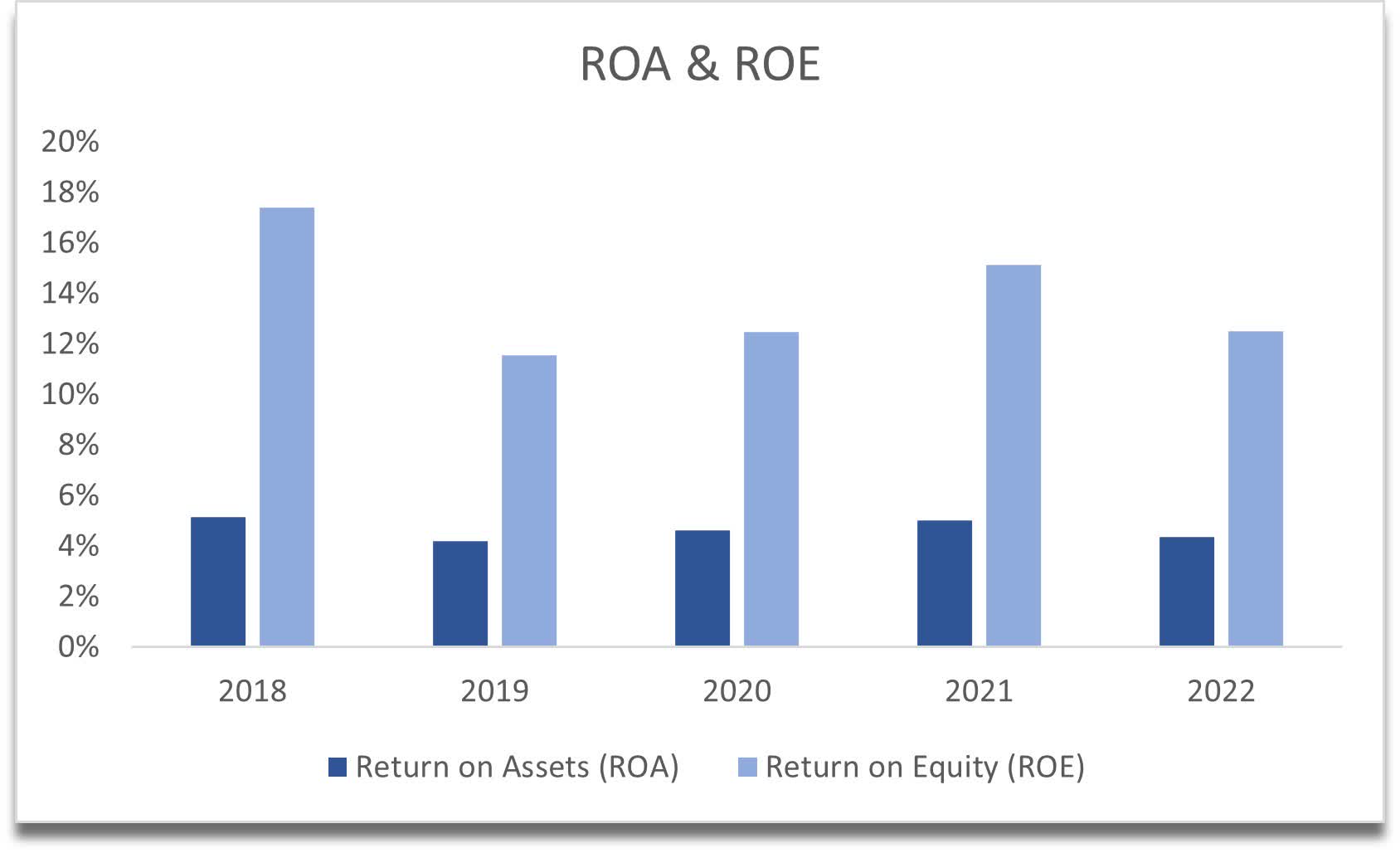

In terms of efficiency, the company has decent ROA and ROE numbers, with a slight drop in the latest FY22, which could become concerning if it continues to trend down.

{kind=link}

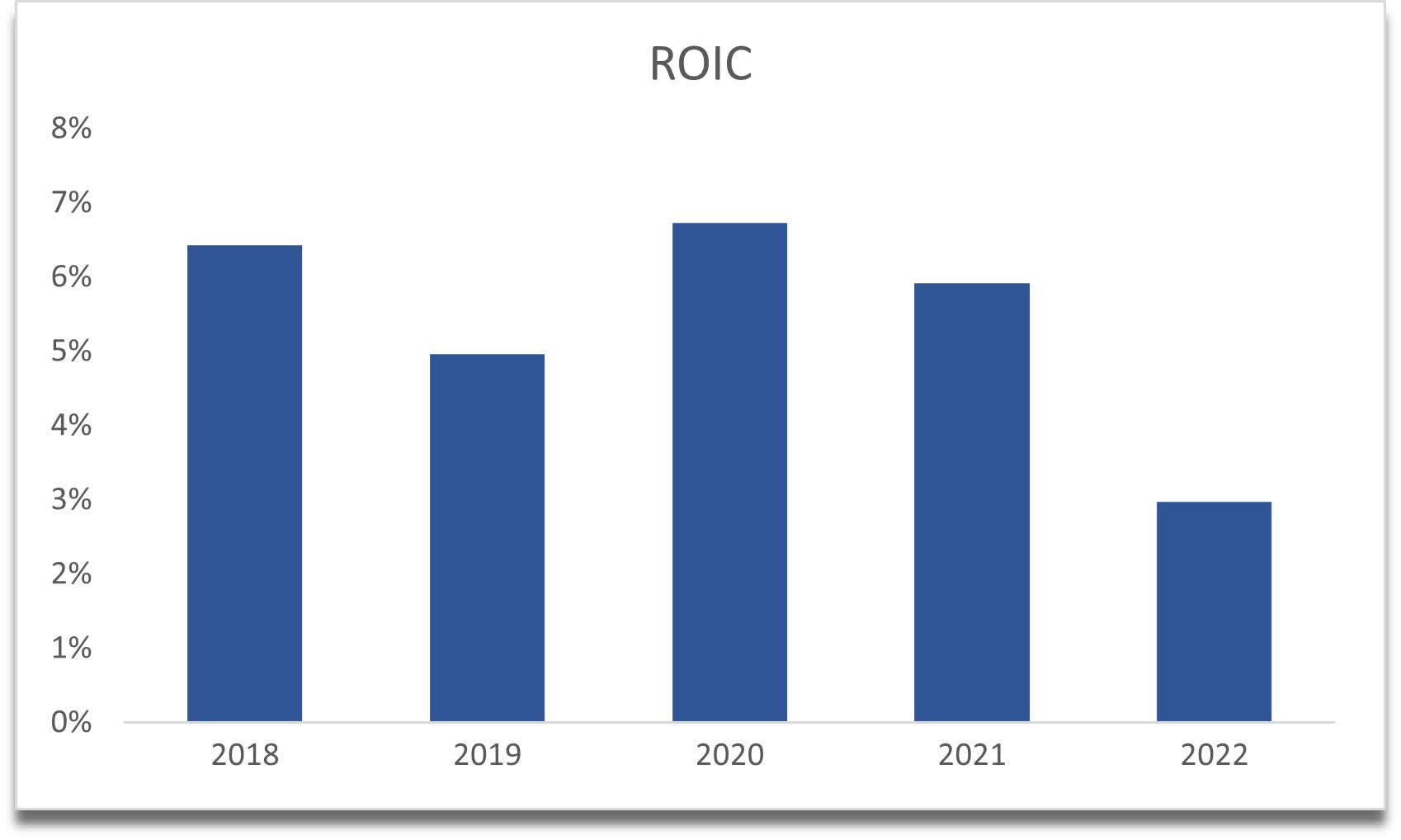

I can also see that the company has started to lose its competitive edge over the last while, which is not surprising. It didn't have a spectacular ROIC, to begin with, but now it is getting even worse. The company is losing its moat to other players in the business.

{kind=link}

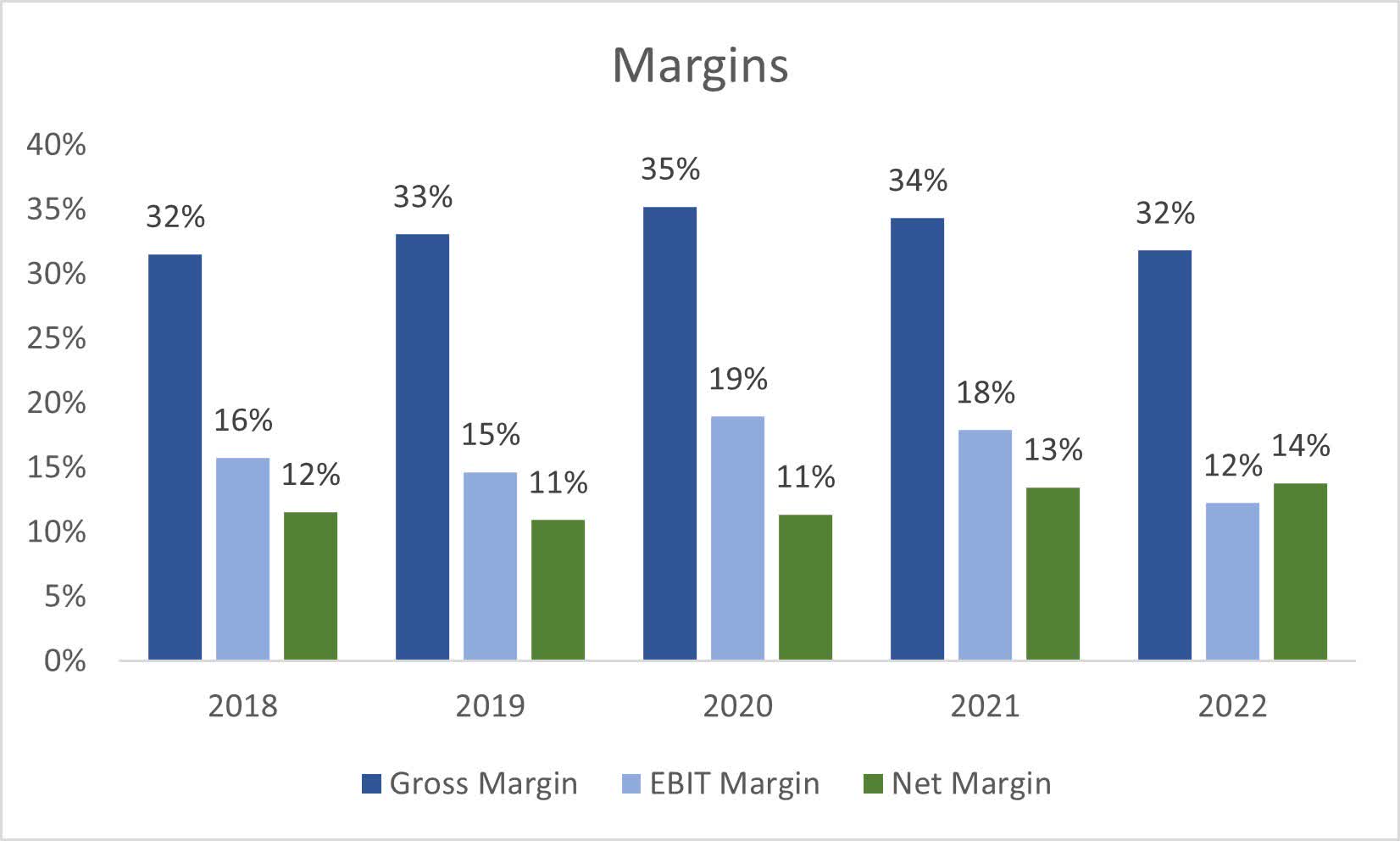

Margins have been hovering around the same numbers for the last 5 years, with EBIT margins slightly down from the previous year while net margins saw a slight expansion. I wouldn't be surprised if margins were to contract more due to the projects it still has in store in terms of building out 5G networks throughout the year.

{kind=link}

Overall, I can see from these numbers that the company is struggling to remain relevant in this world and needs to get a good catalyst to propel the company out of this downward spiral and to become more efficient and profitable, so that the shareholders are rewarded for sticking around with them.

Valuation

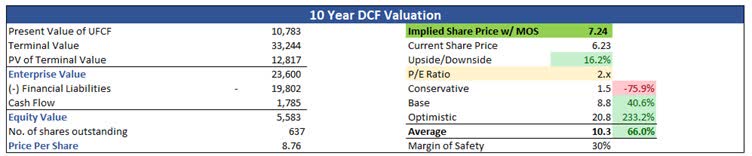

The company grew its revenues by around 2% in the last decade. I will approach my valuation conservatively as well and for the base case, I have modeled the company to keep growing at around the same, 2.5% CAGR for the next decade. For the optimistic case, I went with 3.6%, while for the conservative case, I went with 1.5%. I can see the company beating these estimates if the shift to 5G turns out to be a winner, and they manage to gain a bigger market share, and if their TV segment stops losing subscribers, but for now I wanted to keep these on the conservative side because of the prevailing negative sentiment towards the company.

In terms of margins, I decided to expand gross and operating margins by 200bps or 2% each in the next decade, which seems reasonable because just a year ago the company had those kinds of margins.

For the optimistic case, I went with a slightly higher margin expansion than on the base case, and vice versa for the conservative case.

Since I'm not the biggest fan of the company's financials, I will add a higher margin of safety to the calculation than my usual 25% for companies that have outstanding books. I decided to go with 30% for DISH.

With that said, I calculated the intrinsic value of DISH to be $7.24, with around a 16% upside from current valuations.

{kind=link}

Closing Comments

I believe the negative sentiment towards a company like DISH plays a huge role in its valuation. There are a lot of uncertainties for DISH in terms of where it's headed in the future. The catalysts may work out, and it can stop the main revenue generator from losing subscribers quarter after quarter, but we cannot assume that these will work out in the end and the company becomes successful yet again. For this reason, I will give it a hold rating until I see a positive shift in how the company operates.

The segments the company is operating in have a lot of strong competition, and if it cannot keep up with it, I believe it will continue to lose market share all across its reportable revenue segments and eventually be either acquired by some big player or potentially even go out of business.

I don't think that the company will be very attractive for me to invest in anytime soon, because I like companies that are already operating smoothly, with great future potential for growth, and a good value proposition for shareholders. DISH is not there yet. It would be a gamble for me to invest in the company right now, in hopes that it turns around. The metrics did not show me a turnaround story just yet.

For further details see:

DISH Network: Why It Could Be A Gamble To Invest Right Now