DBRG - Dislocation Of The REIT Preferred Market - PFFR

2023-06-20 15:01:33 ET

Summary

- Preferreds are fixed income instruments that normally provide strong yield but minimal capital appreciation potential.

- Recently, however, prices have become dislocated and irrational.

- They now have around 50% capital appreciation potential on top of outsized dividend yields.

Those who follow my work may have noticed a recent concentration of articles about preferreds. It is not that my objectives have changed, I remain focused on maximizing total return. It is that the market has changed. The forward expected return of preferreds has become improperly high due to a price dislocation.

The dislocation

As preferreds sit between bonds and equity in terms of risk, they should provide an expected return that is higher than bonds but lower than common equity.

Usually they do.

But in the last 18 months REIT preferreds have become dislocated such that in many cases the forward expected return exceeds that of its counterpart equity. The source of this dislocation is that the REIT market moved improperly in response to the rapid rise in interest rates. In brief, the current yield moved in parallel without any attribution of value to discount to par.

As a result, REIT preferreds now have current yields that sit at a healthy premium to high yield bonds in addition to nearly 50% capital appreciation potential.

Current yield versus yield to maturity

As you know, interest rates have moved up considerably. Such a move does and should have an impact on fixed income securities. Treasuries dropped in price (yields up) and bonds move with treasuries.

The way a bond moves when interest rates change is that its yield to maturity moves in parallel with the yield curve. For a given bond that trades at, let's say, a 2% premium to treasuries, if prevailing treasuries of a similar duration had a 3% yield to maturity, it would have a YTM of 5%. So then when rates increased and that treasury moved to a 4% yield the bond would have a YTM of 6%.

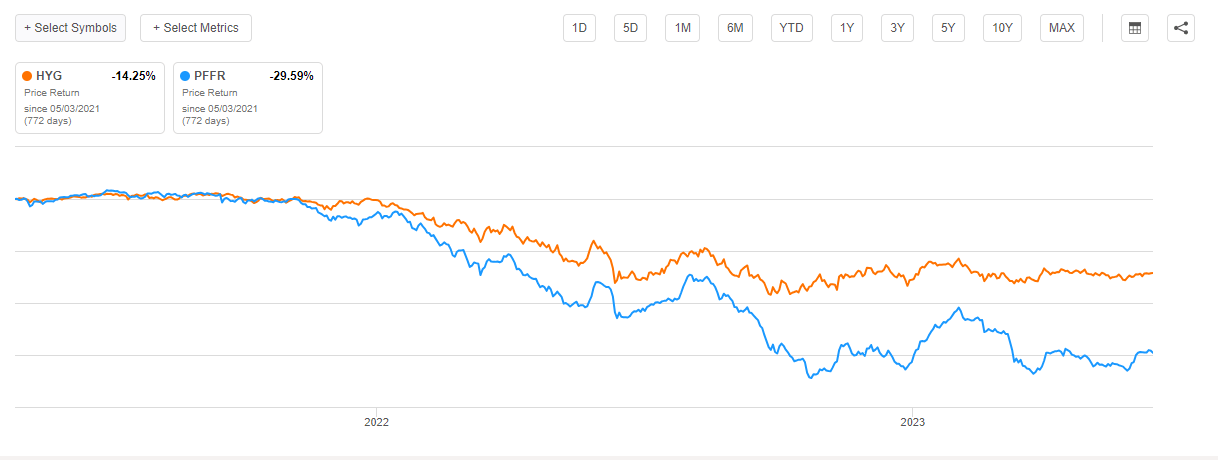

Of course the risk premium could also change, but generally speaking that is how fixed income securities are supposed to move with interest rates. Indeed, that is largely what happened with the high yield bond ETF ( HYG ) dropping about 14% in the last 18 months. The same drop should have happened in preferreds, but instead REIT preferreds, as measured by the InfraCap REIT Preferred ETF ( PFFR ), dropped more than twice as much, down about 30%.

{kind=link}

I think the market was attempting to use the same yield to maturity math, but the process is a bit weirder with preferreds as they do not have a fixed maturity date. Most have a date at which they can be redeemed at the company’s option, but in this sort of environment redemption is unlikely for most.

Thus, with a theoretically infinite maturity, the yield to maturity becomes the current yield. With a bond, yield to maturity includes the capital appreciation to par through the remaining life. So if a bond with five years left is trading at 90% of par, it is getting roughly 2% return per year from capital appreciation. This is included in the YTM and is why corporate bonds were only down a moderate amount.

Consider the math on a REIT preferred that was formerly trading at par with a 6% coupon. As interest rates rose, the market now demands a yield of 9%. To get to a 9% current yield the $25 par has to trade down to the mid $16s.

Nominally, a 9% yield makes sense for a fixed income instrument of medium risk in this interest rate environment. However, in pricing preferreds in this way, the market has attributed zero value to the capital appreciation potential. That preferred that now trades at the 9% current yield now has 50% capital appreciation potential.

2MCAC

Surely that has some value.

Attributing no value to 50% capital gains potential is assuming there is no chance the preferreds are redeemed or companies are bought via mergers which triggers change in control clauses resulting in the full $25 payout.

Beyond special events the capital appreciation is likely to happen naturally. Market consensus right now is that the Fed starts cutting significantly in 2024. I don’t know if or when interest rates will go back down, but undoubtedly there is a pretty good chance that interest rates go back down at least a couple percentage points.

Whether you personally believe the chance of any of the above occurrences is 20% or 80%, mathematically that capital gains potential has value. Yet the market is valuing this entire set of preferreds as if they are a current yield and nothing more.

Return comparison in a normalized environment

To make the math simple let us consider the following:

- A bond with a 6% coupon and 9% yield to maturity with five years left

- A preferred with a 6% coupon and 9% current yield

Over the course of the next five years, interest rates move back down to a level where 6% is considered a proper return for a fixed income instrument of the given risk level.

Both the bond and the preferred would return to par value, but the total return is drastically different. For simplicity we will ignore compounding aspects as compounding applies more or less equally to both cashflows.

- The bond returns 45%

- The preferred returns 95%

What is the difference?

The capital appreciation is INCLUDED in the bond’s yield to maturity but it is not included in the REIT’s current yield.

Therefore, it is ridiculous that the market has treated REIT preferred current yields as if they were yield to maturity. The now vast capital appreciation potential is going completely unvalued.

It is extreme mispricing and I am taking full advantage of the dislocation.

Counterargument #1: Do the preferreds involve outsized risk relative to the bonds?

The relative risk between preferreds and bonds has not really changed. Just as there are some bad corporate bonds there are some dangerous REIT preferreds.

The HYG is a risky ETF because it contains things like DISH bonds.

PFFR is a risky ETF because it contains things like the DigitalBridge ( DBRG ) preferreds

That is just the nature of ETFs. They contain the junk along with the good stuff.

I believe much of this risk can be circumvented by selecting the good REIT preferreds which oddly enough in this environment trade at just about the same yield as the bad REIT preferreds. It is amazing to me how beaten up the preferreds of really high quality REITs with growing cash flows and great balance sheets have gotten.

Counterargument #2: What if interest rates stay high?

While far from my base case, it is possible interest rates will stay high for a long time. In such a scenario the capital appreciation on the discounts to par might take longer to be realized. Even in that case, however, one would still be collecting the outsized dividend which makes it much easier to wait however long it takes for the environment to normalize.

Additionally, there is another work around here in the form of floating rate preferreds. In 2CHYP, the Portfolio Income Solutions portfolio, we balance fixed income preferreds with floating rate preferreds such that the dividends actually go up if interest rates remain high.

With a mixed basket of fixed and floating preferreds, the investor gets a sort of win-win scenario with regard to the direction of interest rates.

Wrapping it up

REIT preferreds are substantially underpriced. The market has mistaken current yield for yield to maturity. Capital appreciation potential of around 50% has a non-zero value.

For further details see:

Dislocation Of The REIT Preferred Market - PFFR