DSGR - Distribution Solutions Group: Growth On Acquisitions Brings Opportunity

2023-04-19 00:02:36 ET

Summary

- Distribution Solutions Group, Inc. is a $900-million market cap distribution company that offers valuable solutions to the MRO, OEM, and industrial technologies markets.

- In my opinion, over the past couple of years, the company has expanded its operating activities quite qualitatively.

- The management estimates the combined addressable market for DSGR now stands at $57 billion, and that the company's asset-light business model is going to help it grow organically and inorganically.

- Given the relatively low valuation amid good operational growth rates, I would recommend looking into DSGR stock at its current price levels.

The Company And Its Markets

Distribution Solutions Group, Inc. ( DSGR ) is a $900-million market cap distribution company that offers valuable solutions to the MRO, OEM, and industrial technologies markets. They were created by combining 3 industry leaders: Lawson Products [28.2% of total sales], Gexpro Services [34.1%], and TestEquity [33.5%]. Lawson Products specializes in MRO and C-parts distribution, while Gexpro Services is a global supply chain services provider to the OEM market. TestEquity is an expert in electronic test and measurement solutions. Apart from the above 3 segments that DSGR reports, they have a category called "All Other," which encompasses the DSG holding company costs that are not specifically linked to the regular operating activities of the listed segments. Additionally, this category includes the minor outcomes of a non-reportable segment - in total, this category brought ~4.3% of combined sales in FY2022, according to the company's 10-K filing .

On December 29, 2021, DSG made two merger agreements: one with TestEquity and another with Gexpro Services. These agreements involved multiple parties and conditions but essentially resulted in DSG's subsidiary companies merging with TestEquity and Gexpro Services, which would become wholly-owned subsidiaries of DSG.

On April 1, 2022, the TestEquity and Gexpro Services Mergers were completed. As part of the TestEquity merger, DSG issued 3,300,000 shares of common stock to TestEquity equity holders, paid off TestEquity's debts, and covered some of their expenses. Similarly, as part of the Gexpro Services Merger, DSG issued 7,000,000 shares of common stock to the Gexpro Services Stockholder, paid off Gexpro Services' debts, and covered their transaction expenses.

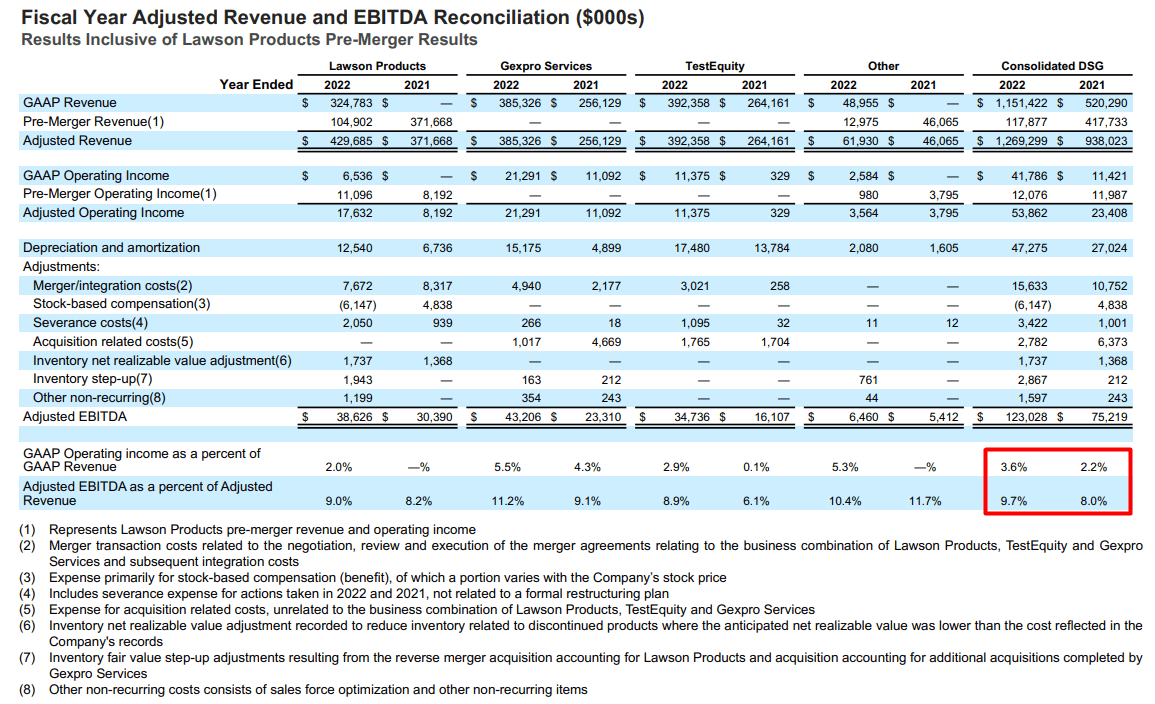

As far as I can see from the financial reports of the consolidated company, DSG has slightly improved its EBITDA margin on a post-merger basis:

{kind=link}

DSGR's recent IR materials, author's notes

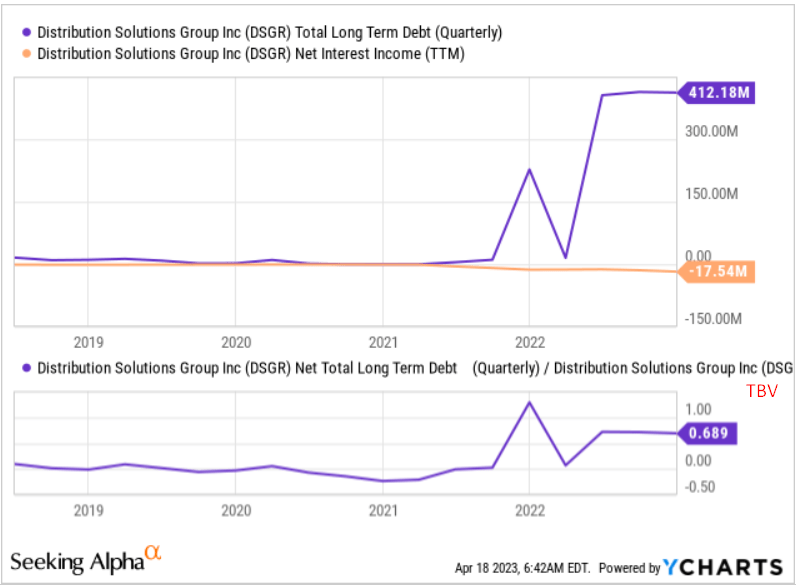

To finance the merger, the consolidated company took on large liabilities. However, this did not materially affect its creditworthiness, as all acquired companies were profitable before the merger and had positive retained earnings balance sheet items.

{kind=link}

YCharts, author's notes

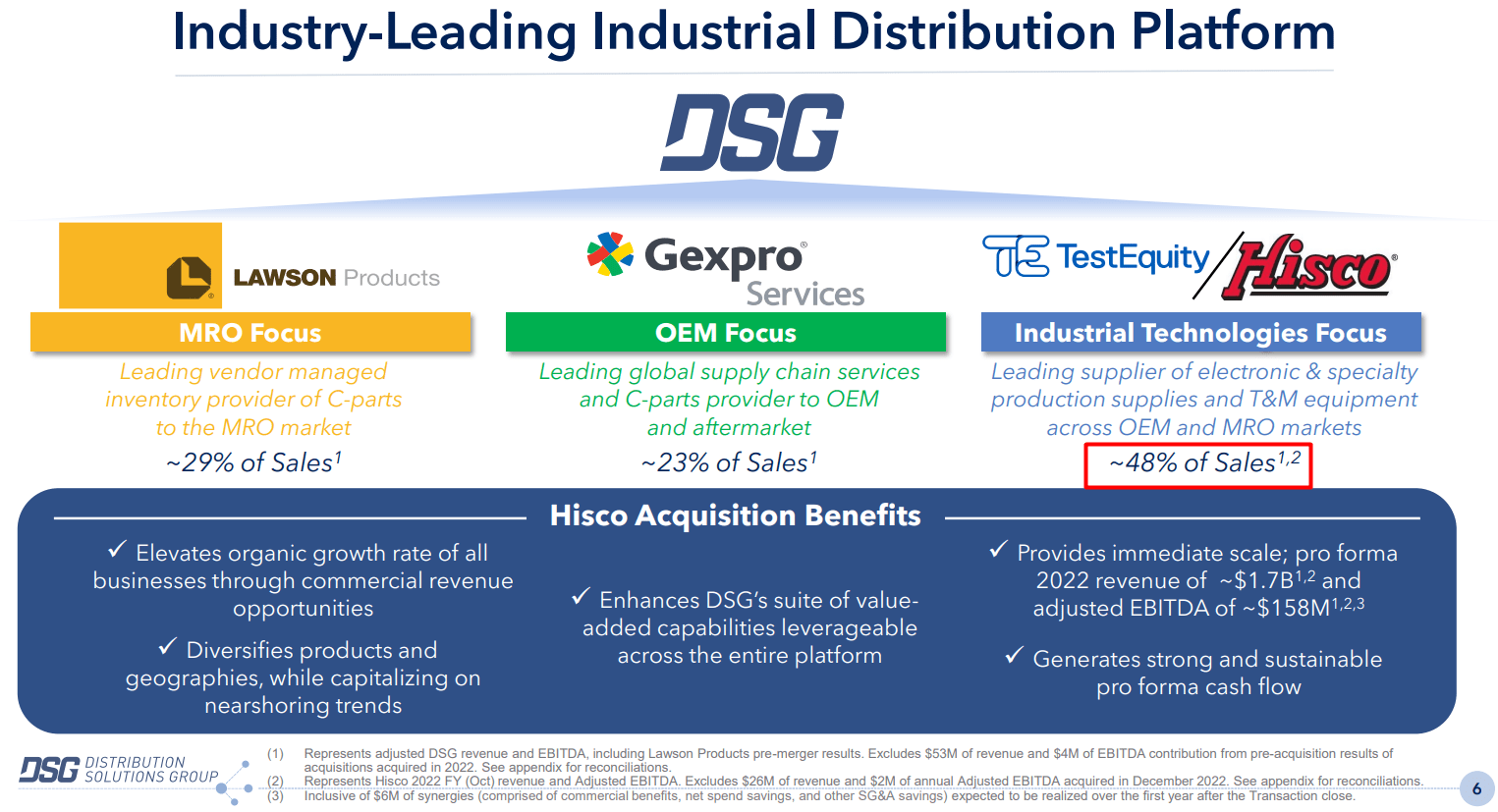

The latest news is the purchase of another target company by DSGR - HIS Company Inc. - on March 31, 2023:

DSGR, a NASDAQ-listed company, plans to buy Hisco for $269.1 million, combining it with TestEquity. The deal will be funded using the company's committed credit facility, and about $100 million will be raised in equity through a rights offering to existing shareholders. There may be an additional payment of up to $12.6 million if Hisco meets certain performance targets. DSG will pay $37.5 million in cash or stock as retention bonuses to select Hisco employees. The company will distribute subscription rights for shares to raise about $100 million. After the merger, DSG's net debt leverage on adjusted EBITDA is expected to be between 3.25x to 3.50x.

Source: Summarization by the author, based on SA News

As a result of this new acquisition, the TestEquity segment will account for ~48% of total revenue, bringing the total pro forma revenue to ~$1.78 billion and adjusted EBITDA to ~$158 million:

{kind=link}

DSGR's IR materials, author's notes

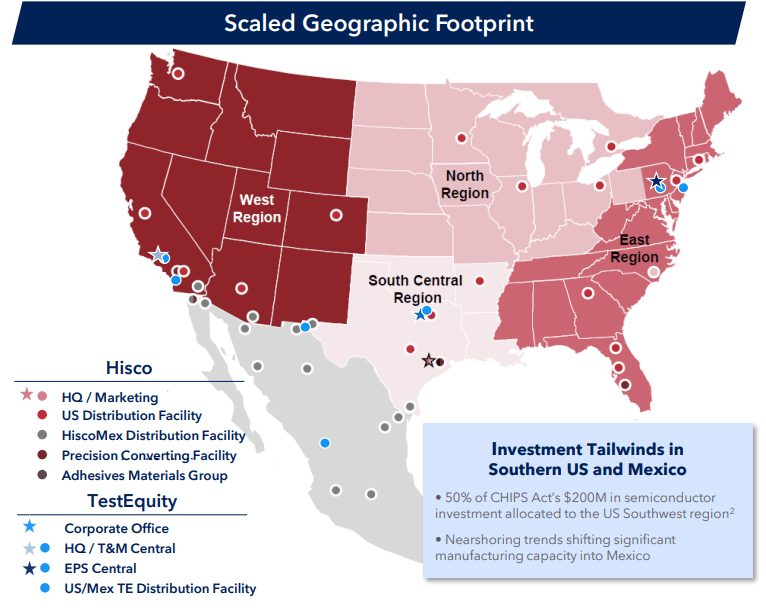

DGRS will now have a stronger presence in the Electronic Assembly, Converting/Repackaging, Aerospace, Medical Devices, and Transportation end markets - both in the West and East regions of the United States:

{kind=link}

DSGR's IR materials

The management estimates the combined addressable market for DSGR now stands at $57 billion, and that the company's asset-light business model is going to help it grow organically and organically going forward [based on the latest earnings call, Q4 2022 ].

Financials And Valuation

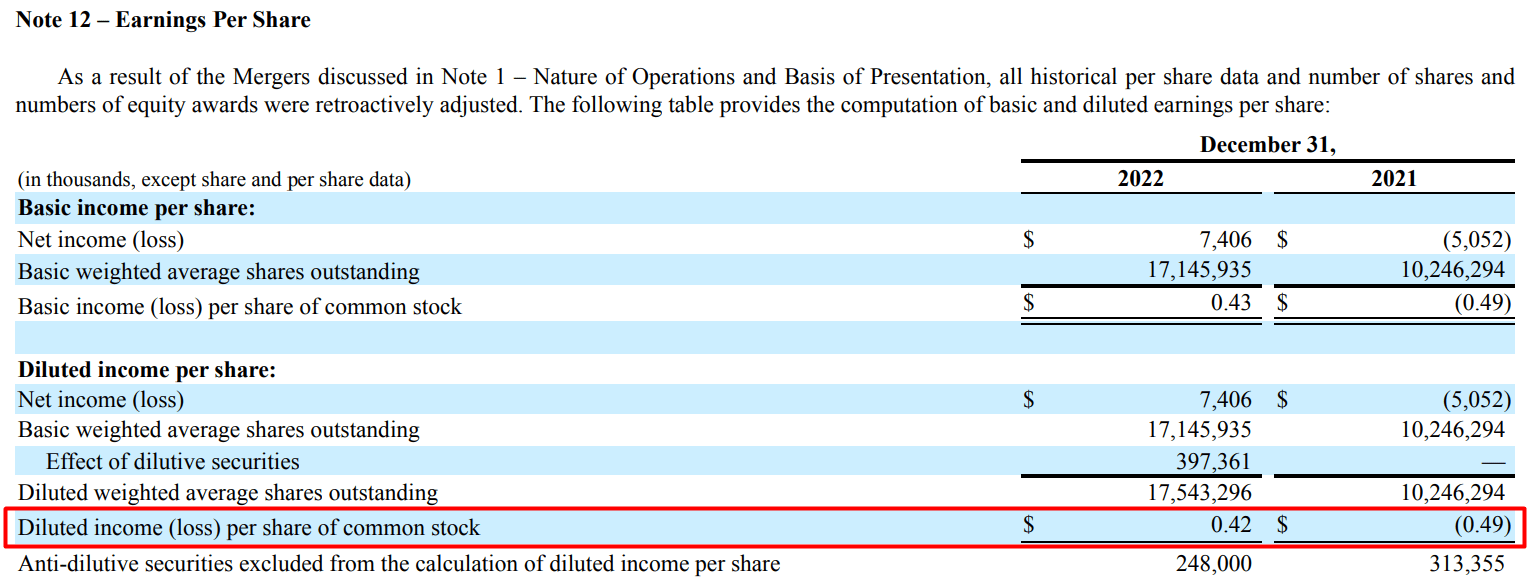

Regarding financial results for Q4 and full-year 2022, DSGR reported strong top and bottom line results as I see it across its 3 principal operating companies, with total sales growth of 42% and organic sales growth of nearly 17% through both price and volume in Q4. In FY2022, DSGR closed on 5 acquisitions with an annualized 2022 revenue run rate of $204 million and acquired a higher EBITDA of $21 million. Consolidated sales for Q4 were $328.9 million, representing an increase of 155% on a GAAP basis, while reported GAAP operating income was $12.7 million [compared to a loss of $1.8 million in Q4 2021]. Adjusted EBITDA improved to $34 million from $16.3 million last year, amounting to 10.3% of sales. DSGR's full-year adjusted diluted EPS rose from negative $0.49 to positive $0.42 despite the significantly increased number of shares outstanding [because of all the mergers].

{kind=link}

DSGR's 10-K, author's notes

The company has a prudent leverage target of 3-4x Net Debt to Adjusted EBITDA. They have a trailing net debt to 2022 adjusted EBITDA leverage ratio of 3.1x due in part to $67 million in acquisitions closed since the merger date. DSGR has cash of $24.6M and $77 million of availability under the existing credit facility, with the ability to access a $200 million accordion for M&A. The company's total debt is $417.1 million, with only $15 million in nominal debt due over the next 12 months.

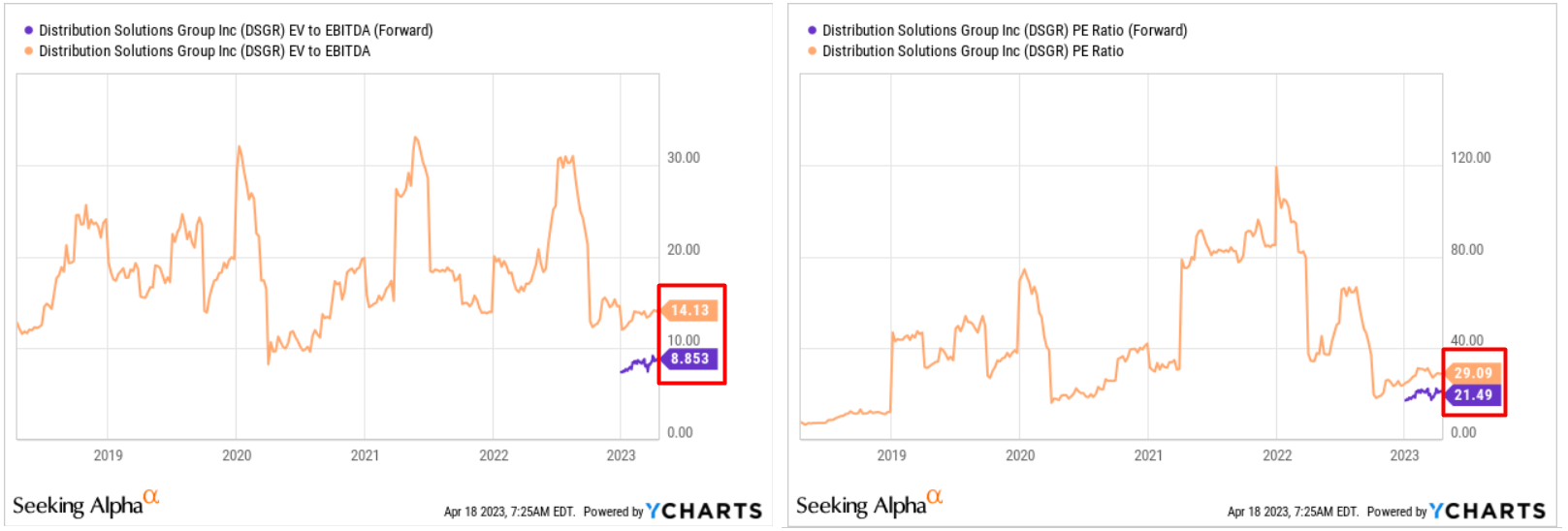

A few words about the current valuation of the company. Although DSGR stock is up 16.8% YTD and 20.86% over the past year, its key valuation multiples remain at local lows within their historical patterns:

{kind=link}

YCharts, author's notes

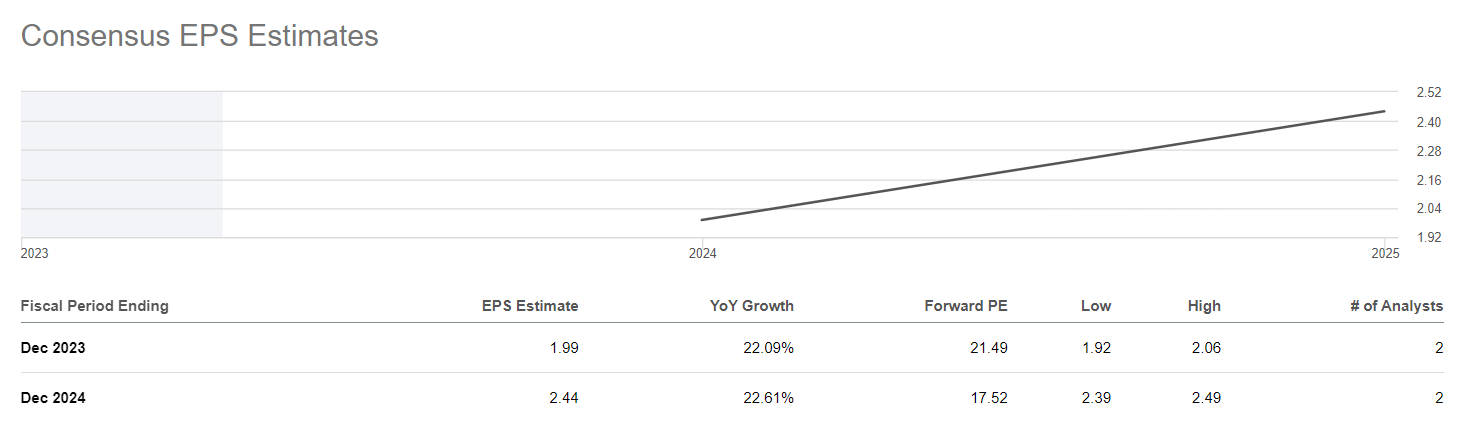

Meanwhile, if we look at Wall Street forecasts, analysts are assuming a continuation of the multiple contraction - the estimates are data poor, so to speak, which is explained by the size of the company, but still:

{kind=link}

Seeking Alpha, DSGR's Earnings Estimates

The company's problem to solve is still weak profitability - but as far as I can see, DSGR just has not had time to take advantage of the synergies from recent acquisitions. Most likely, over the next few years, all of the company's organic [and not only] operating growth will be eclipsed by operating leverage - EBITDA should grow faster than sales and EPS - faster than EBITDA. If this is true, it is probably not yet priced in by the market because few analysts cover the stock in general and can assess this financial effect. Retail investors should either trust management and wait for the outcome, or stand by and see what happens. Given the relatively low valuation amid such good operational growth rates, I would recommend looking into DSGR stock at its current price levels.

Concluding Thoughts

I have to admit that the valuation of DSGR is currently low due to the uncertainty level. In my opinion, it is not yet possible to accurately and unbiasedly evaluate the synergies from all its recent acquisitions. However, it is obvious that management is not buying everything - judging by the operating metrics of the target companies, all of them had positive adjusted EBITDA numbers, and DSGR did not overpay for its acquisitions.

In 2023-2024, there is going to be many new opportunities in the M&A market - DSGR management will likely look for new acquisition targets given the financing problems of some of the smaller companies. This could expand synergies in the future - currently the forwarding valuation multiples look favorable enough to consider DSGR stock as a potential purchase.

From my perspective, it appears that Mr. Market is currently inappropriately pricing DSGR's prospects - so I expect the stock to continue to rise as EPS and revenue numbers revise upward. DSGR appears to be a cautious "Buy" at its current levels.

Thank you for reading!

For further details see:

Distribution Solutions Group: Growth On Acquisitions Brings Opportunity