DECPF - Diversified Energy Company May Face Headwinds In Their Derivatives Book

2023-11-14 11:58:22 ET

Summary

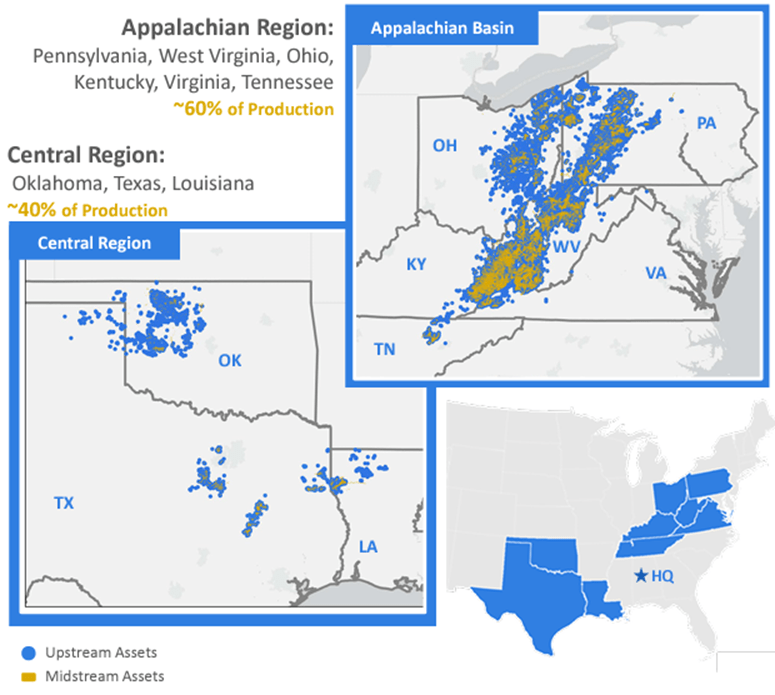

- Diversified Energy Company is an Alabama-based O&G company with operations primarily in the Central Region and the Appalachian Basin in the U.S.

- The company hedges 85% of production, and experienced a significant return from their hedges in 1H23.

- 64% of the firm's enterprise value comprises net debt, suggesting the firm may be overleveraged.

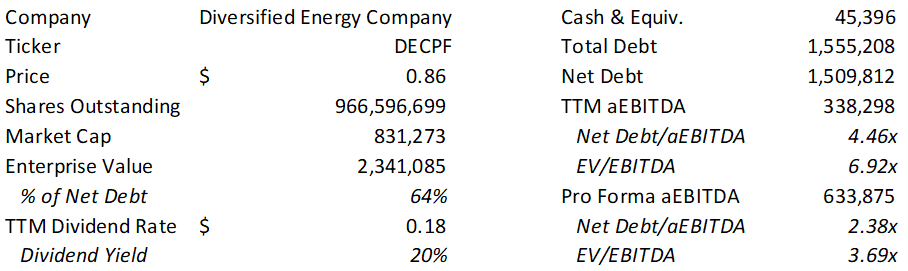

Diversified Energy Company (DECPF) is an Alabama-based oil & gas company with operations primarily in the Central Region (Barnette & Anadarko Basins) and the Appalachian Basin in the US, focusing on E&P, marketing, and transportation services for natural gas. The firm's production is 86% natural gas, 11% NGLs, and the remainder is oil with daily production of 144mboe/d. Diversified Energy hedges roughly 85% of their book, and experienced a significant return as a result of their hedges in 1h23. The firm's equity is currently valued at $831mm with an enterprise value of $2,341mm with 64% of its enterprise value being comprised of net debt. Diversified Energy trades at a relatively higher multiple to its peers at 6.92x EV/aEBITDA. Though comparing aEBITDA to their peer group's EBITDA isn't one-for-one, I believe these adjustments are prudent given the level of significance their commodities hedging book is on operating profits (89% in 1h23). With this, I provide DECPF a SELL recommendation with a price target of $0.47/share, and a downside risk of 45%.

{kind=link}

Operations and Performance

{kind=link}

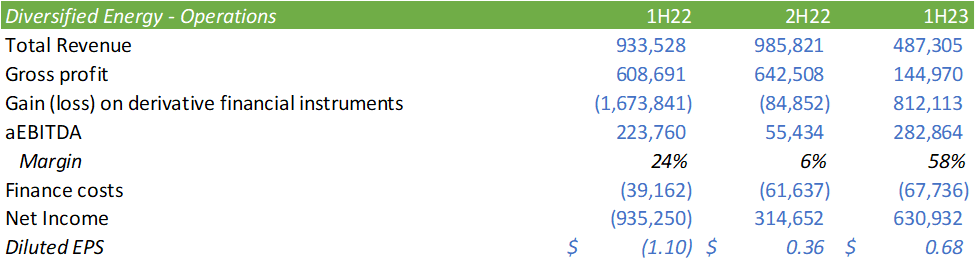

1h23 reported earnings are coming off of challenging comps as the realized price per barrel of equivalent declined by -52% from the previous year, offset by a 4% increase in production. Despite the challenging commodities market, Diversified Energy has a well-hedged book and managed to salvage a significant profit resulting from a realized gain of $54mm across their entire book.

{kind=link}

Diversified Energy was able to manage much of the costs associated with the lower produced prices; however, their newly acquired Central Region assets came with a higher cost to operate as compared with their other assets. Much of these costs were offset by lower transport costs (-17%) and taxes (-11%) tied to commodity prices.

{kind=link}

Management appears to be leaning toward transforming their operations into a more ESG-oriented firm with a focus on well plugging operations. The firm emphasizes its acquisitions of multiple plugging companies and currently operates 16 teams with 17 rigs. During the first 6 months of 2023, the firm retired 100 of their own wells, costing between $20-25k per well. In aggregate, the firm spent $2mm in plugging costs, a significant reduction from the prior year of $4.9mm.

Hedging

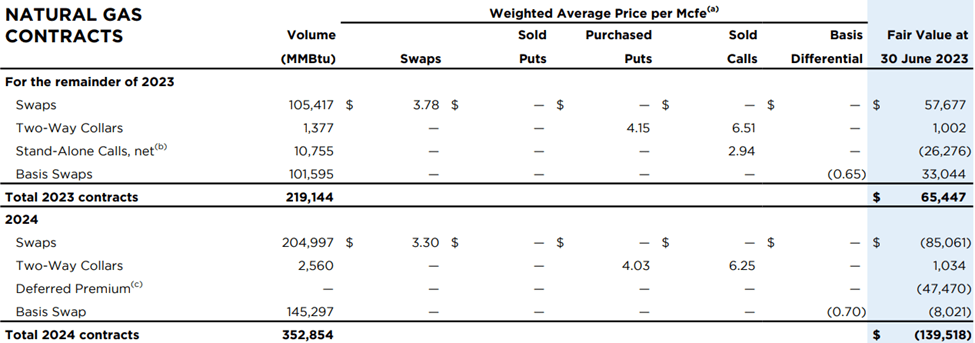

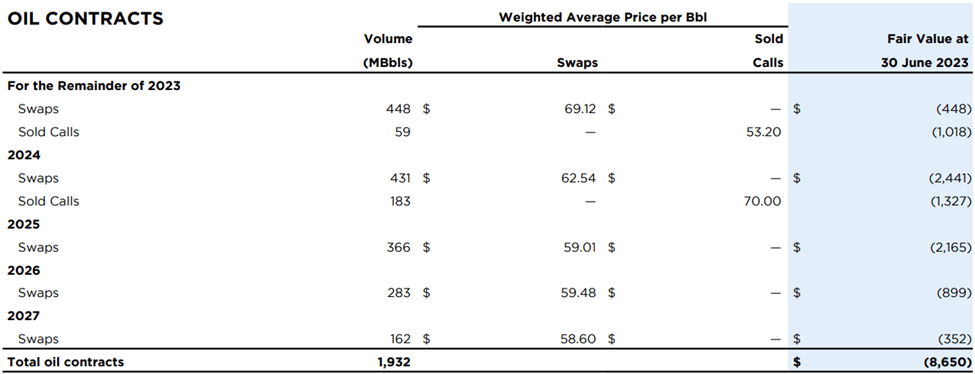

Aside from E&P and midstream operations, the firm runs a very robust hedge book with 219,144mmbtu of natural gas hedges for the duration of FY23. Considering production for 1h23 totaled 127bcf, the firm either significantly increased their production volumes as a result of the Tanos or is embedding more focus on speculative trading. The firm has 105,417mmbtu of natural gas hedged using swaps with a ceiling of $3.78/mcf and should be able to capitalize on these contracts for the duration of the year.

{kind=link}

2024 contracts hedge 352,854mmbtu and are currently running at a paper loss as of 1h23 reporting. Given the forecasted futures prices for natural gas in 2024 remain below their $3.30 swap price for the majority of the year, the valuation of their contracts should adjust positively at their 2h23 reporting period, reversing their negative figures on their 1h23 report.

{kind=link}

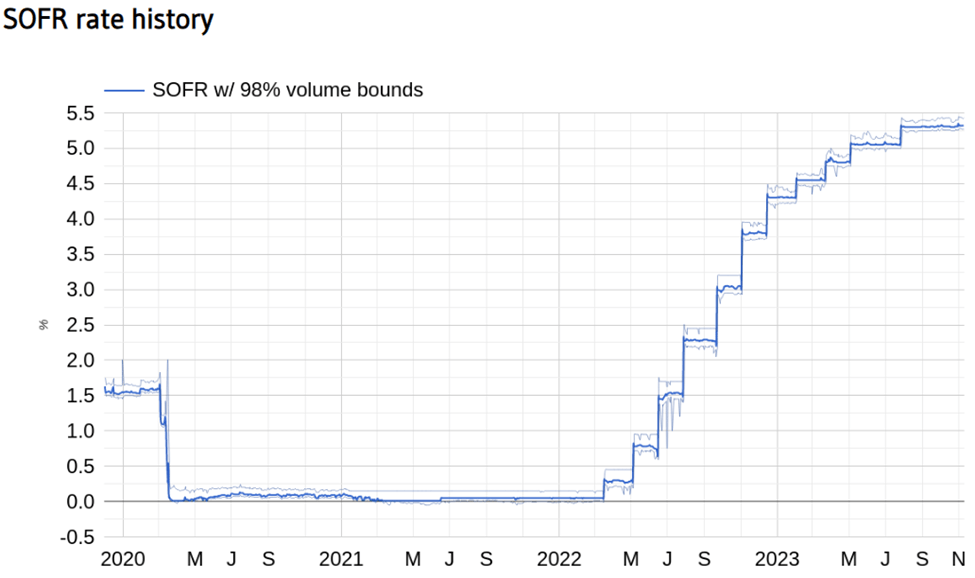

The firm also has significant exposure to interest rate swaps with a receive fixed rate of 4.15% while paying the floating rate. The 30-day SOFR rate currently sits at 5.32% and isn't expected to fall below their fixed pay in the near term.

sofrrate.com Corporate Reports Corporate Reports

{kind=link}

{kind=link}

{kind=link}

Capital Structure

In addition to higher operating costs, Diversified Energy has taken on a substantial amount of debt that has increased their interest expense by 76% when compared to 1h22. As of their 1h23 financial report, Diversified Energy had an average borrowing cost of 6.19% with 82% of its borrowings on a fixed-rate basis. Total debt sums to $1,555mm with $45mm in cash & equiv and restricted cash on the balance sheet. Accordingly, their pro forma net debt/aEBITDA ratio sits at 2.38x.

The firm heavily utilizes its asset-backed credit facility with $99mm remaining of the $375mm plus an additional $135mm resulting from the Tanos II acquisition. The rates on their credit facilities are SOFR+ 2.75-3.75% in the original $375mm and SOFR+ 4-5% on the $135mm addition. This facility also includes $11mm in letters of credit outstanding against their credit facility not reported on the balance sheet.

Aside from debt, the firm has also raised a significant amount of capital through equity raise. In February 2023, the firm sold 128,444 new shares priced at $1.27/share to raise $163mm in part to finance the Tanos II transaction. The firm has no limitations on capital raised through equity sales. Since reporting their interim financials, the firm has repurchased 4,475,000 shares for $3.4mm.

Diversified Energy has financed and collateralized their acreage using ABS vehicles which are amortized over the life of the security. The total ABS liability sums to $1,169mm as of 1h23. The rate on these vehicles ranges from 4.875-7.5% for an aggregate cost of 5.61%. Because these are secured loans, there is some risk involved in which Diversified Energy has to perform to perfection and generate adequate cash flow in order to repay these loans, whether through ordinary operations or derivatives trading.

Recent Acquisitions & Divestitures

It should be noted that Oaktree co-invests with Diversified Energy in their asset acquisitions. Because these assets are acquired through a JV-like structure and the firm separates PUDs from provided producing assets, the firm's asset acquisitions can be considered a "business" acquisition, allowing Diversified Energy to report pro forma financials.

Diversified Energy acquired upstream assets and related infrastructure in the Central Region of Tanos II on March 1, 2023, for $262mm. The asset purchase was funded through an equity raise in February 2023, cash on hand, and their Credit Facility. The firm also divested $43.5mm in assets in the Central Region across Texas and Oklahoma that were considered non-core or non-operating in 2023. The firm also divested $16mm of non-core acres in the Central Region on July 17, 2023.

Given their current asset base, it appears that Diversified Energy is focusing its efforts in the Appalachia region and Barnett & Anadarko Basins. Given that natural gas is their primary producing asset, it would make sense for the firm to diversify its production into more liquids-rich regions. The firm also acquired G&P assets in the Central Region in 2022 for $18mm. The midstream assets generate roughly 3% of their total revenue and generate an operating loss of $18mm. The primary purpose of their midstream assets is to lower the cost of production on the firm's operations as well as sell excess capacity to 3rd party producers, so the operating loss may not necessarily be a negative effect but rather a cost-reducing asset when compared to utilizing 3rd party G&P assets.

The firm also owns midstream assets in the Appalachia region. This includes 17,000 miles of gathering and transport lines and associated compression stations. The firm markets 1.2bcf/d of produced and 3rd party natural gas. Despite its midstream reporting segment, the firm doesn't appear to disclose the capacity of its midstream assets, so understanding the excess capacity for third-party utilization is relatively limited. Given that midstream assets operate at a loss, it is safe to assume that the majority of capacity is for internal utilization.

{kind=link}

Diversified Energy has a total $2.5b in O&G properties with $463mm in fixed capital. The firm also holds $1,178mm in derivative liabilities on $14mm assets. Though the firm is an O&G producer, I believe its derivatives exposure challenges this stature as the firm is walking a fine line as a nonbank financial institution. Given that their CEO, Rusty Hutson, is an ex-banker, this doesn't come as much of a surprise.

Shareholder Value & Valuation

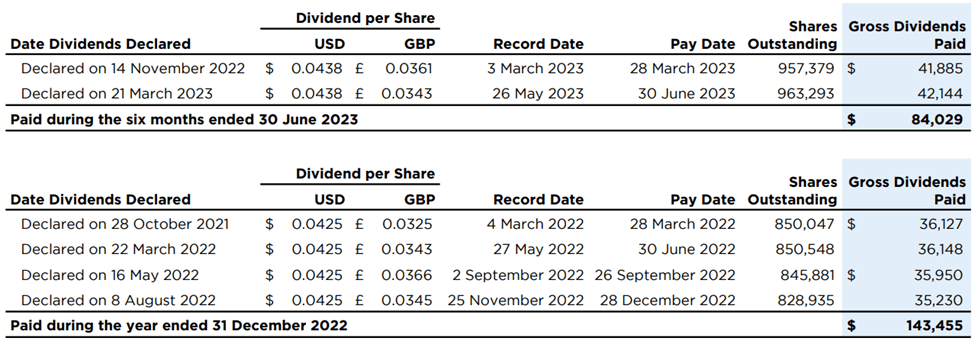

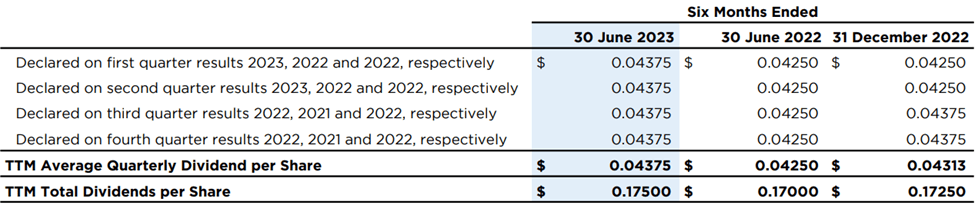

The firm has historically paid out a very robust dividend relative to their share price, recently at $0.04375 per quarter. Management has subsequently declared the q2'23 dividend to be paid on December 29, 2023, for $0.04375/share. Annualized, the dividend yields 20%.

{kind=link}

Below is a schedule of their historical dividend payouts.

{kind=link}

In addition to their dividend policy, management has made strides in share buybacks in the last few months since reporting their 1h23 results. Since reporting, management has repurchased 4,475mm shares for $3.4mm.

Overall, I believe Diversified Energy is trading at a relatively high valuation compared to its competitors in the natural gas producing space. Given their smaller generating footprint and less concentrated assets, as well as their high levels of debt and unique capital structure, I believe DECPF equity is significantly overvalued. Given these risk factors as well as their heavy dependence on the futures market, I rate DECPF shares a SELL rating with a price target of $0.47/share.

{kind=link}

Because this firm trades on the London Stock Exchange, trading this company has significant limitations. This firm currently does not have an options market and it appears that shares cannot be shorted on major US-based trading platforms. Given these features, I recommend the next best option and to just avoid ownership in this firm.

For further details see:

Diversified Energy Company May Face Headwinds In Their Derivatives Book