DHC - Diversified Healthcare And Office Properties: The Epic Collapse Of A Controversial Engagement

2023-09-03 16:20:39 ET

Summary

- The merger between Diversified Healthcare Trust and Office Properties Income Trust has been called off, causing shares of both companies to rise.

- Some shareholders argued that the terms of the transaction favored Office Properties Income Trust and amounted to a take under of Diversified Healthcare Trust.

- The cancellation of the merger has kept me bearish on Diversified Healthcare Trust, while believing Office Properties Income Trust is better off.

September 1st proved to be a very interesting day for shareholders of both Diversified Healthcare Trust ( DHC ) and Office Properties Income Trust ( OPI ). Shares of both companies rose after the market closed in response to news that the merger between them has been called off. Leading up to this point, there was serious pushback from shareholders and other parties, the primary argument focusing on the idea that the terms of the transaction essentially worked out to a take under of Diversified Healthcare Trust. While those who pushed back against the deal have won the battle, I do believe that they sealed the fates of shareholders. Moving forward, this has caused me to become very bearish on Diversified Healthcare Trust, though I do think that Office Properties Income Trust is better off with this decision.

A brief look back

Back when the deal between Diversified Healthcare Trust and Office Properties Income Trust was announced in April of this year, I wrote an article detailing why I believed the transaction would end up being incredibly positive for shareholders of Diversified Healthcare Trust while being a negative for investors in Office Properties Income Trust. My argument largely revolved around three core points. First, while both companies have rather lofty net leverage ratios, Diversified Healthcare Trust was definitely more heavily indebted. Second, there was the issue of profitability. Financial performance achieved by Diversified Healthcare Trust over the prior couple of years had significantly fallen short of what Office Properties Income Trust had demonstrated. And lastly, there seemed to be almost no synergies associated with the transaction, with the management teams of both companies forecasting cost savings of only between $2 million and $3 million on an annual run rate basis.

I was not surprised when I started seeing different parties speak out against the transaction. But I was surprised by the nature of their arguments. Instead of arguing that Office Properties Income Trust was ending up with the bad side of the transaction, most major shareholders and proxy firms that spoke out against the merger alleged that the deal amounted to what was essentially a take under of Diversified Healthcare Trust. For those not aware of this terminology, a take under is a scenario where one company buys another one at a substantial discount to its actual value.

At face value, there definitely was some data that suggested that Office Properties Income Trust was getting the good side of the transaction. This data involved the total shareholders’ equity of the two businesses. Net assets owned by Diversified Healthcare Trust came out to $2.51 billion. By comparison, that number was $1.34 billion for Office Properties Income Trust. Had the deal gone through, shareholders of Office Properties Income Trust would have ended up with a 58% ownership over the combined company. And yet, they would have contributed only 34.8% of the net assets.

While this is a fair point to make, my argument centered around the idea that the assets owned by Diversified Healthcare Trust were generating cash outflows. For instance, while Office Properties Income Trust generated $192.6 million worth of operating cash flow in 2022, Diversified Healthcare Trust reported cash outflows of $40.4 million. Similar issues existed involving FFO, or funds from operations, adjusted FFO, and adjusted operating cash flow. Only NOI (net operating income) and EBITDA were consistently positive.

A blessing for some, a curse for others

In the months that followed the announcement of the transaction, multiple parties spoke out against it. This included two major shareholders. One of these, the famous D.E. Shaw, wrote a letter opposing the transaction. It owns about 6.1% of the shares outstanding of Diversified Healthcare Trust. Flat Footed is an even larger owner, with a 9.8% stake in the REIT. In its letter addressing the matter, it stated that the deal ‘dramatically’ undervalued the assets owned by Diversified Healthcare Trust. Flat Footed went so far as to claim that there existed ‘vastly superior alternatives’ to the merger, such as cutting back fee driven spending in order to preserve cash or selling off assets.

{kind=link}

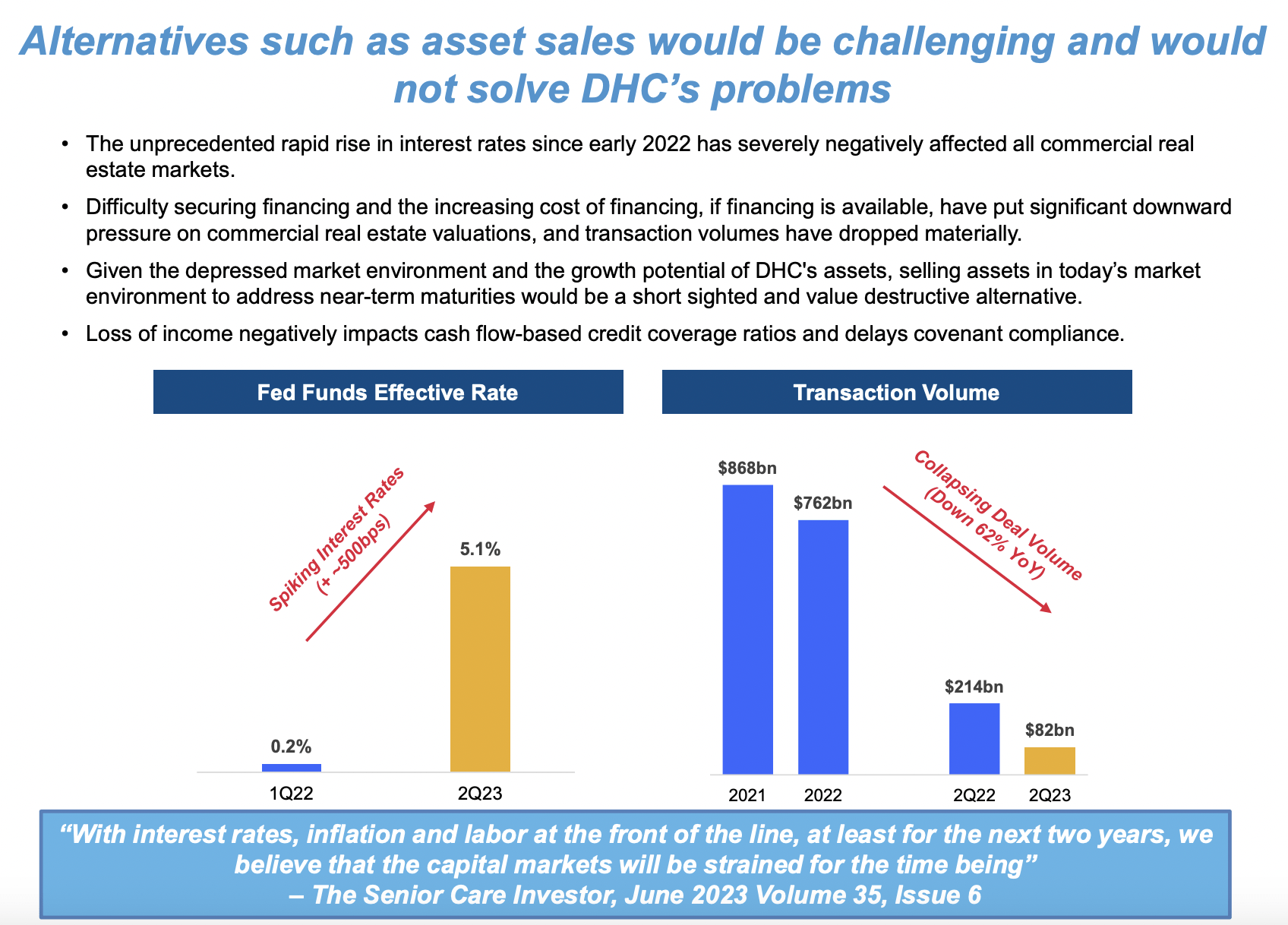

These investors were not the only parties to recommend that the deal be scuttled. All three major proxy companies that assess deals like this came out against the transaction. One of these, ISS, made several interesting remarks about the transaction. The firm argued that all unsecured debt could be eliminated if the REIT were to decide to sell off a ‘sizeable’ portion of the assets on its books. To be perfectly clear, Diversified Healthcare Trust, in an investor presentation , disagreed with this notion. Their claim was that the market for deals like this has dried up thanks in large part to soaring interest rates. While it is true that higher interest rates would make transactions less appealing, I would also add that it would be difficult to sell off assets on good terms when those assets struggle to generate positive cash flow.

At the end of the day, my assessment of this situation is significantly different then the assessment made by ISS and the two aforementioned shareholders. Having said this, ISS did make some valid arguments. For instance, it does appear as though there truly was not a competitive process for determining the best suitor for Diversified Healthcare Trust. Management did state that they received one unsolicited proposal back in May of 2022. However, they deemed that proposal to not be credible. They did claim that they were open to other unsolicited proposals. But there was nothing stopping them from shopping the company around and reaching out to other prospective suitors. But it seems as though they did not take that route.

{kind=link}

Diversified Healthcare Trust

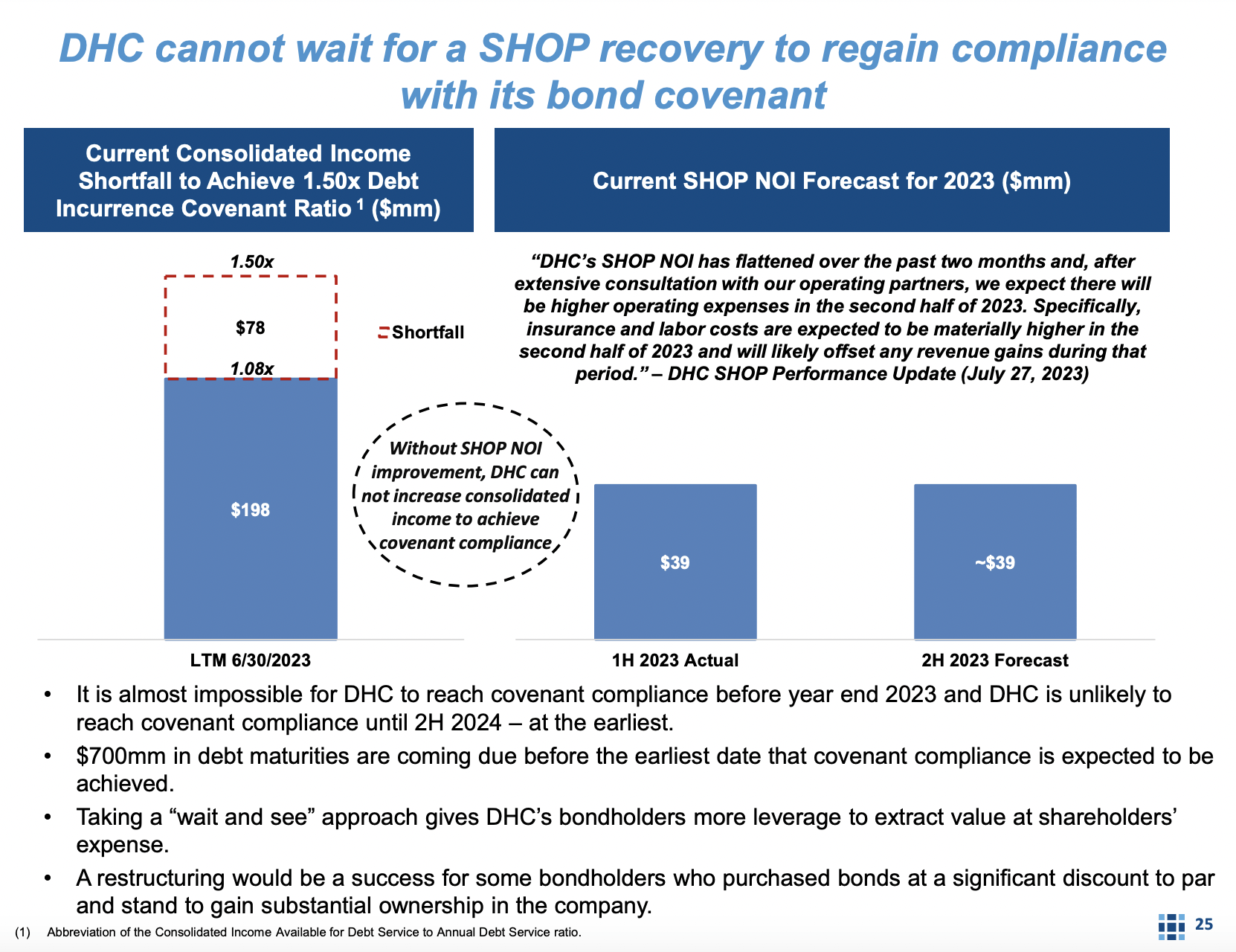

ISS made other allegations. For instance, they claimed that the management team at Diversified Healthcare Trust claimed that the firm’s liquidity issues were ‘manageable and temporary’. I am not quite sure that I agree with how stern this language is. After all, in the final quarter of the 2022 fiscal year, which is the last quarter that the company reported before announcing the merger, management acknowledged that the company was not in compliance with its covenants and only went so far as to say that they ‘believe’ there's a path to getting back into compliance. However, it would require the company to improve NOI by roughly $78 million in relatively short order.

Regardless of what these various parties think about the transaction, it is clear now that it will not come to pass. On August 30th, both companies announced that they were adjourning their shareholder votes that had been scheduled for Wednesday, with the goal of continuing discussions with representatives of major interested parties. This was followed up on September 1st with an announcement that the deal had been cancelled. Each company will pay for its respective legal and restructuring costs, and neither firm will have to pay a termination fee to the other.

{kind=link}

Author - SEC EDGAR Data

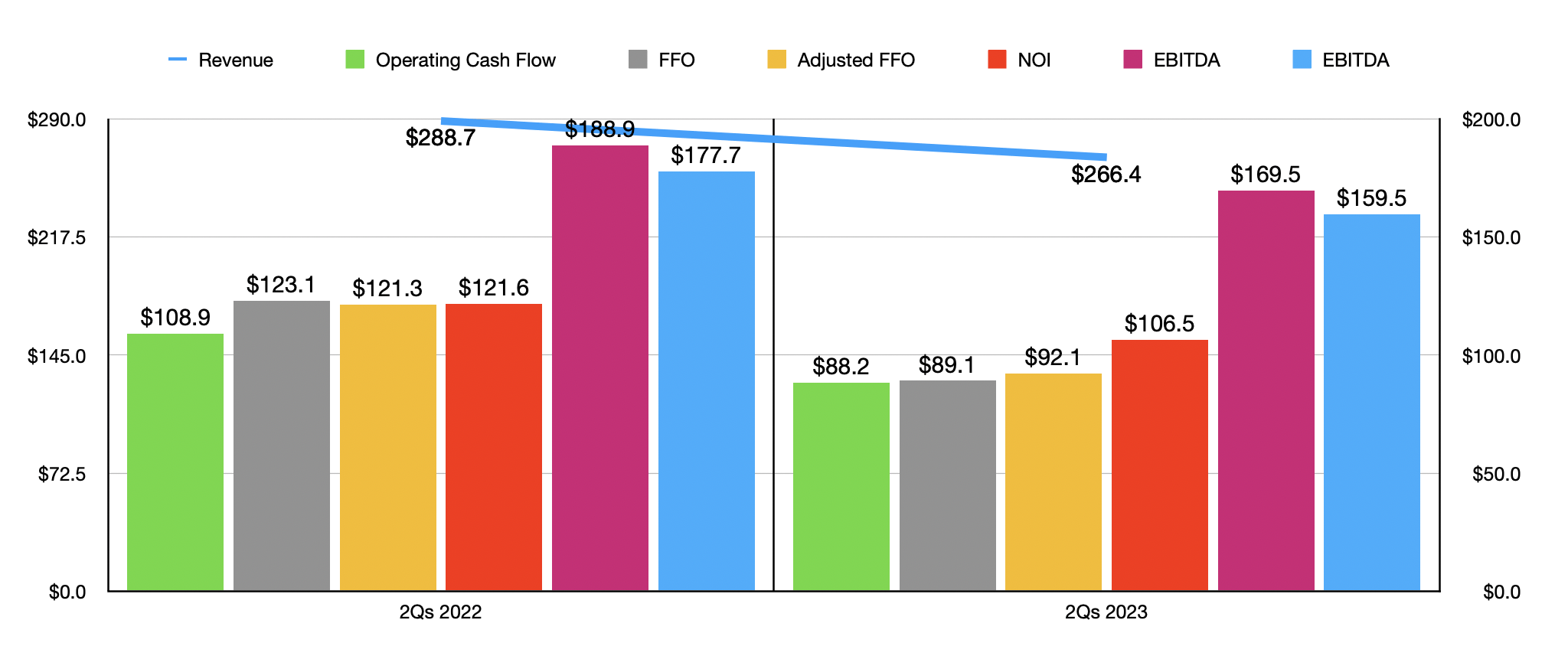

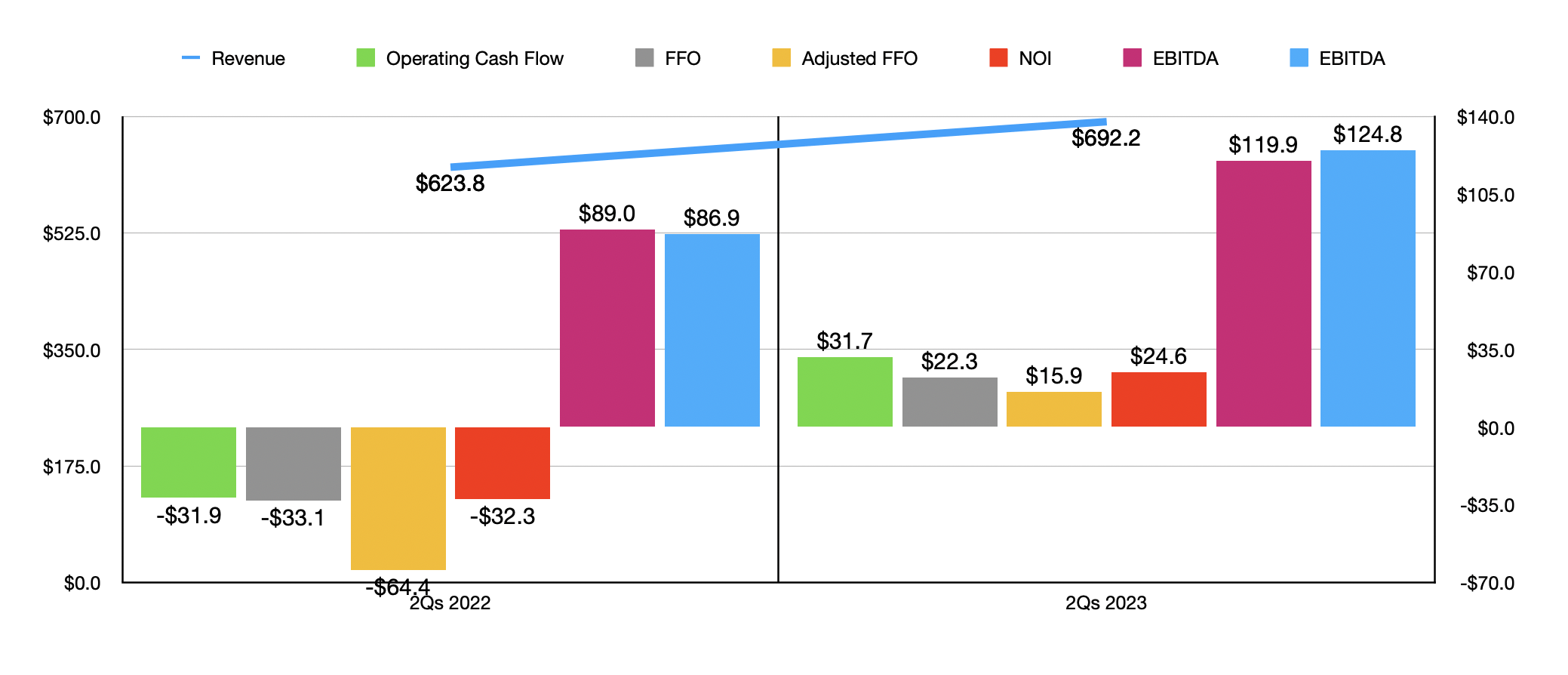

As for what this means for both parties in the long run, my view regarding Office Properties Income Trust it's fairly straightforward. As you can see in the chart above, financial performance for that enterprise has weakened a little bit for the first half of this year relative to the same time last year. This comes even as the occupancy rate of its properties grew from 89.4% to 90.6%. However, on the whole, the enterprise is still healthy. As the chart below illustrates, Diversified Healthcare Trust has actually seen a meaningful improvement in its own financial situation year over year. At least in part, this can be chalked up to improvements in the occupancy rate at some of its properties. It is true that its office properties reported a decline in occupancy from 88.1% in the first half of last year to 85.8% the same time this year. However, its SHOP portfolio jumped from 73.6% to 77.8%, while its triple net leased properties saw an improvement in occupancy from 78.7% to 80.8%. Meanwhile, it's Wellness Center occupancy remained flat at 100%.

{kind=link}

Author - SEC EDGAR Data

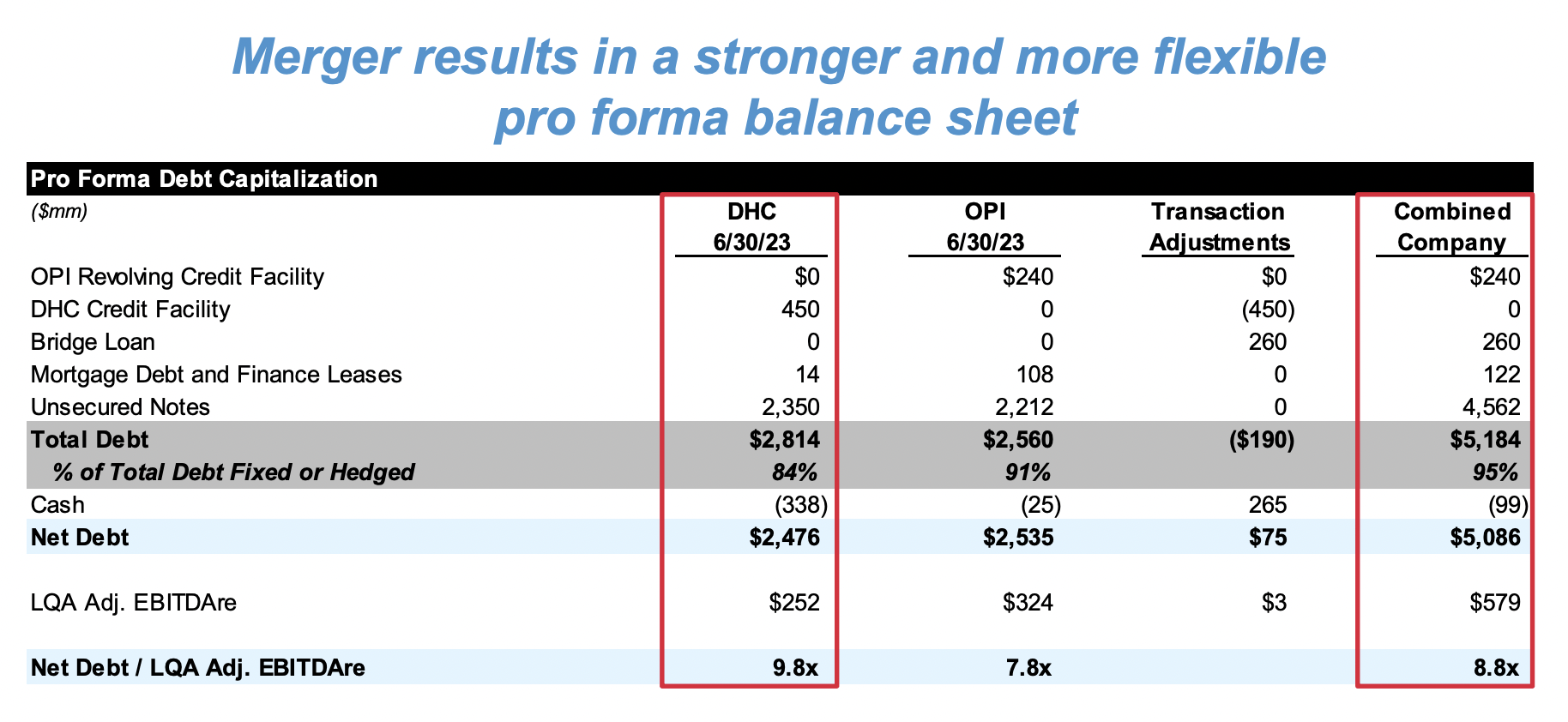

This is great to see, but there is still substantial doubt as to whether Diversified Healthcare Trust will ultimately survive. With a net leverage ratio of 9.8 compared to the 7.8 that Office Properties Income Trust had, the company was truly banking on getting its debt situation addressed. With a $650 million credit facility planned for when the merger was completed, Office Properties Income Trust would have been in a far better position to handle upcoming maturities of debt.

{kind=link}

Diversified Healthcare Trust

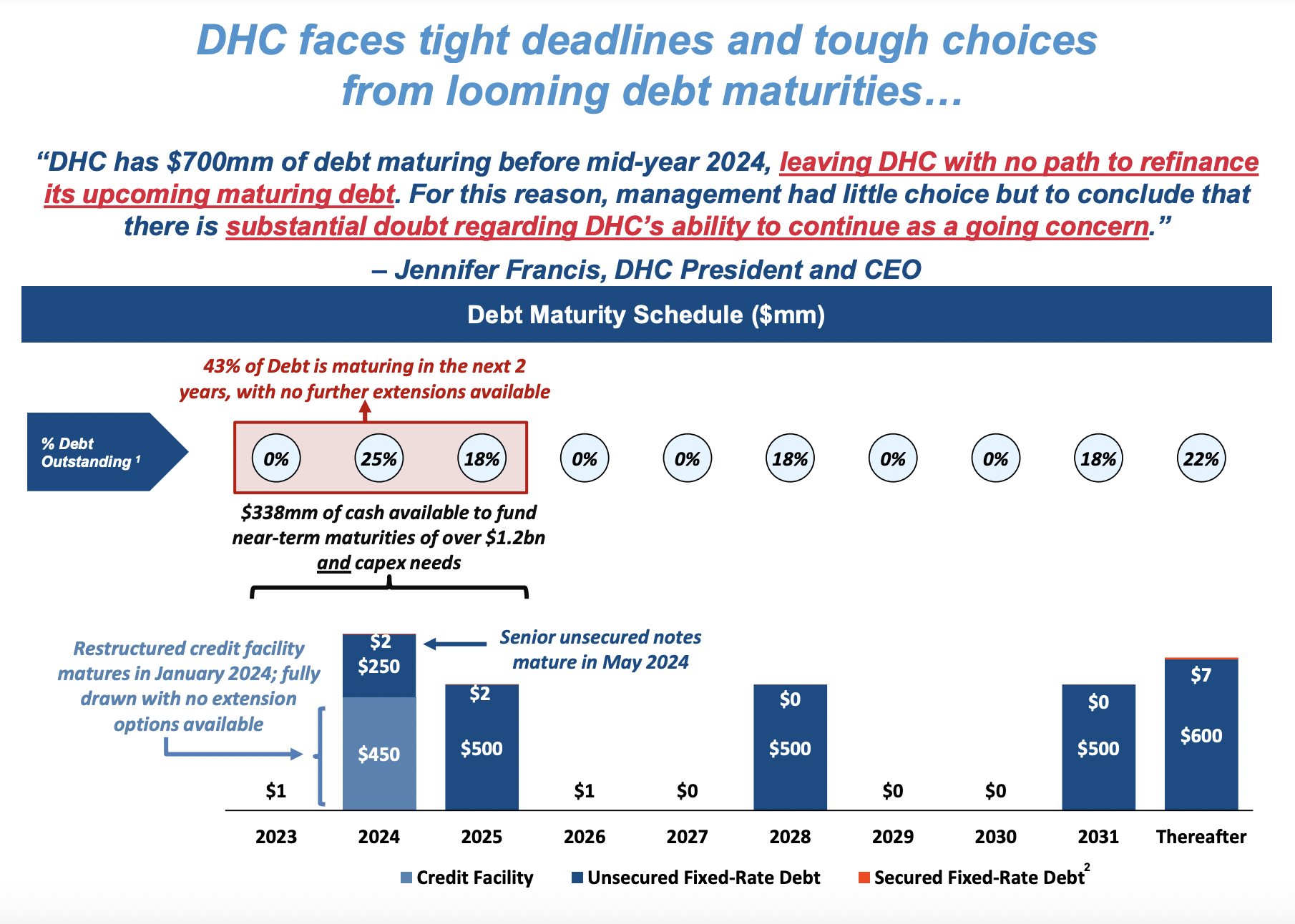

This is important because, in 2024, Diversified Healthcare Trust has $700 million of debt coming due, with $450 million of this coming due in January of next year. And in a recent investor presentation on the matter, management stated that they have ‘no ability to access the debt markets’ because of their leverage, tight market conditions, and existing noncompliance with its covenants. Management even took this a step further by claiming that a failure to complete the merger would represent an existential threat to the company.

{kind=link}

Diversified Healthcare Trust

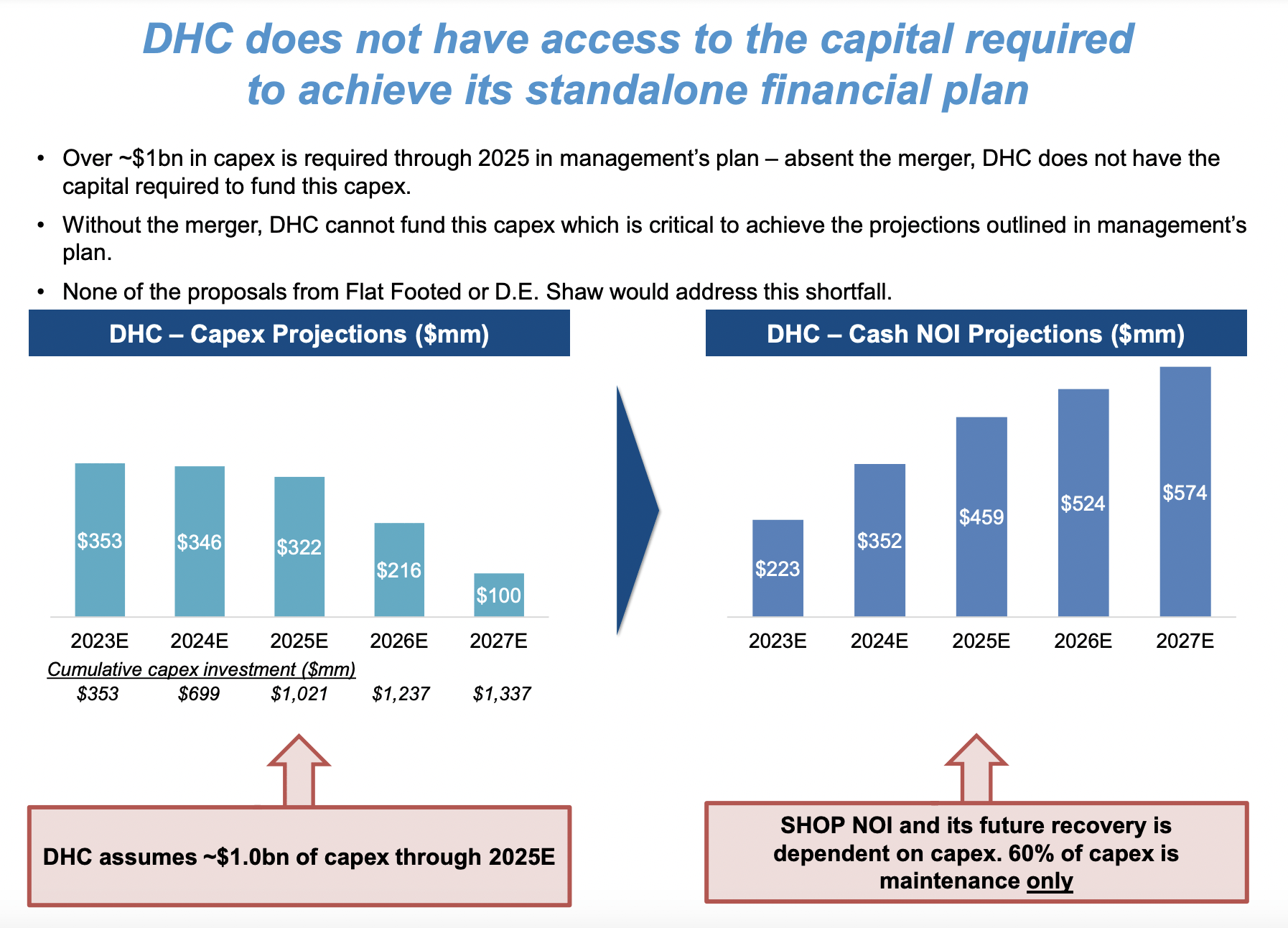

Another important issue to note is that a big part of Diversified Healthcare Trust’s survival strategy has focused around the idea of turning around its SHOP portfolio. Between this year and the end of 2025, management was planning to spend over $1 billion on capital projects aimed at revitalizing this part of the company's operations. Of this, about 60% would be in the form of maintenance spending that is needed in order to keep operations running smoothly. Given the nature of cash flows, Diversified Healthcare Trust cannot be reasonably expected to pay down debt and invest heavily in its assets simultaneously. Of course, asset sales could help. But as I stated earlier in this article, this is not necessarily an easy environment, particularly for a company that bidders will know is financially distressed. Even if the firm's troubles were not plastered all over the financial landscape, market participants understand that the company is not doing well because, earlier this year, management disclosed in their financial statements that they have serious doubts about the company's ability to continue as a going concern. This is the kind of language that is usually used leading up to bankruptcy. But it does not always result in it.

{kind=link}

Diversified Healthcare Trust

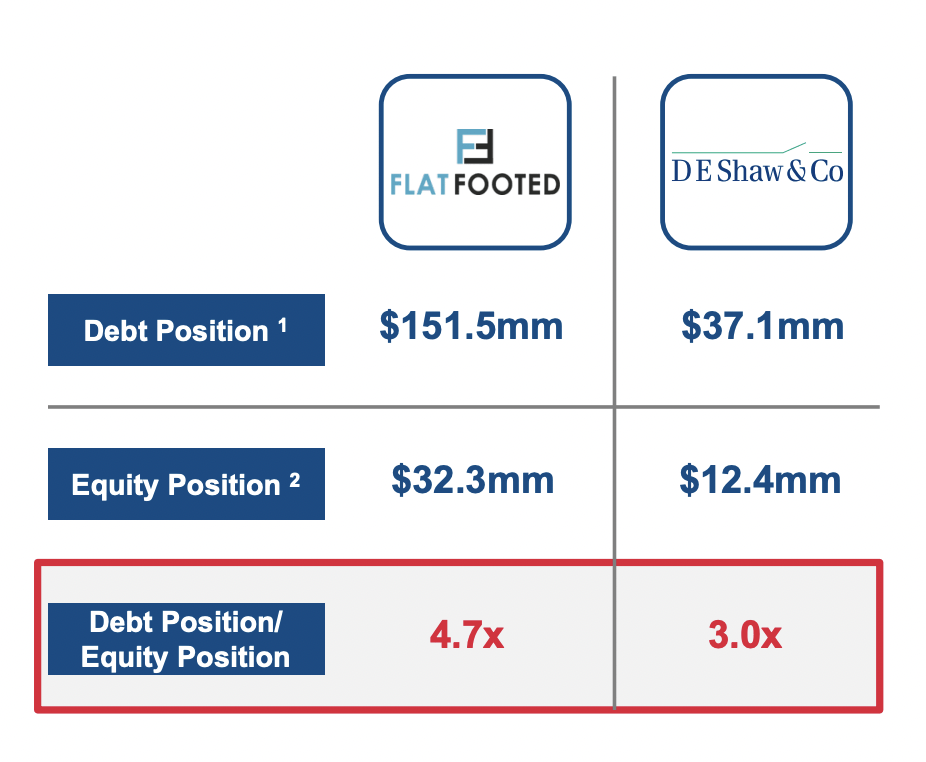

The last thing I would like to address is that while it may seem as though the two major shareholders of Diversified Healthcare Trust would have the best interests of all shareholders in mind, this is not necessarily the case. In addition to owning sizable amounts of stock in the firm, they also have tremendous amounts of debt. As of July 19th of this year, the value of equity in Diversified Healthcare Trust that D.E. Shaw owned came out to roughly $12.4 million. However, the value of debt that they had in Diversified Healthcare Trust amounted to $37.1 million. For Flat Footed, these numbers were $32.3 million and $151.5 million, respectively. The outsized debt exposure is interesting because, in theory, banking on the company going bankrupt could result in a significant payday since debt holders would very likely end up owning the entire company while simultaneously wiping out the common shareholders. I am not saying that this is the plan by either or both of these investment firms. There is no concrete evidence to suggest that is the case. But it is certainly a possibility.

{kind=link}

Diversified Healthcare Trust

Takeaway

After the market closed on September 1st, shares of Diversified Healthcare Trust shot up at 11.8% in response to this news, while shares of Office Properties Income Trust appreciated 1.9%. Clearly, market participants are happy that this transaction fell apart. Personally, I believe that while this is a great development for Office Properties Income Trust, the end result for Diversified Healthcare Trust might not be all that great. It is possible that management could find a way to monetize assets and pay down debt considerably between now and when it owes its existing debts. But I would also argue that the risk of an even worse outcome, such as one involving a complete financial restructuring, absolutely exists and is elevated. Because of this, I have decided to rate Diversified Healthcare Trust a ‘sell’, while upgrading Office Properties Income Trust to a ‘hold’.

For further details see:

Diversified Healthcare And Office Properties: The Epic Collapse Of A Controversial Engagement