SBRA - Diversified Healthcare: Is It Actually Worth Over $9.00?

2023-06-09 11:08:35 ET

Summary

- Diversified Healthcare Trust was slated to be merged with Office Properties Income Trust.

- The stock has rallied as Flat Footed LLC got into a battle with the manager of both these stocks, RMR Group.

- We dissect the fight and tell you what is relatively undervalued.

Most merger announcements tend to be free of drama and the markets move on. That has not been the case with the Office Properties Income Trust ( OPI ) and Diversified Healthcare Trust ( DHC ) proposal. When we covered the action after the announcement, we left with specific ideas of how to take advantage of the distortions in the way their bonds were trading. We look at the recent news flow and the price action to tell you what we think about these two today.

The Price Action

There was a lot to chew on when the news was first released. The merger was combined with OPI's stealth dividend cut (sold as a dividend increase for DHC). So it was hard to decipher what was being priced in. But towards the end of May, you could see a clear move by DHC away from the implied price of the deal. Something was wrong.

We found out what that was when the markets saw the open letter from Flat Footed LLC. to The RMR Group ( RMR ).

Previous Offer

The letter has some exciting hits. It leads off with DHC being radically undervalued based on the board having rejected a $4.00 takeover price a year earlier.

Under the terms of the proposed merger, DHC shareholders are set to receive consideration worth only $0.97, which is 43% below the headline $1.70 offer and 22% below the trading price the day before the announcement – clearly not a takeover premium, but a remarkable take-under. 2 We value DHC’s portfolio of high-quality assets at approximately $5 billion and believe the Company’s stock should be trading between approximately $9 and $10 per share. 3 Therefore, the proposed merger’s contemplated $0.97 per share takeover price represents a 90% discount to DHC’s intrinsic value. Notably, just one year ago, the Board deemed a $4.00 per share cash offer for DHC to be inadequate. 4 Yet, now, the Board is recommending a transaction in which DHC shareholders are forced to accept $0.97 per share of OPI stock

Source: Seeking Alpha-Flat Footed LLC Letter

$4.00 offer? We did not hear about this at the time (May 2022). Going through the S-4 showed that there were other concerns beyond the price.

The independent trustees of the DHC board of trustees invited S&C and BofA Securities to participate in a separate session held without the DHC managing trustees or executive officers present to further discuss the May 2022 unsolicited proposal. Following a discussion of the May 2022 unsolicited proposal, the independent trustees of the DHC board of trustees determined that there was insufficient evidence that the proponent had any track record of making acquisitions of this type, and that the price proposed was inadequate and was not supported by any confirmed equity or debt financing (or disclosed prospects for obtaining confirmed financing).

Source: OPI S-4

We will add that the markets are rather different today than they were a year back. The risk-free rate is 400 basis points higher. Most real estate asset classes are under pressure. Even quality medical office space has lost a lot of value since then.

Those shown above have a far lower debt to EBITDA than DHC. Since DHC has more debt, it would be logical to assume that a similar drop in enterprise value as those above, would drop the share price a lot more. By itself a $4.00 offer in 2022 means nothing.

Poor Rationale For The Merger

Flat Footed sites 4 things that make the merger a poor idea. These include,

1) High fees (relative to market capitalization) for the transaction of $75 million.

2) Poor long term management by RMR.

3) Extremely low synergies.

4) Saddling higher quality assets of DHC with poor office properties of OPI.

Let's address these.

1) Yes the fees are extremely high. Out of the $75 million, $3 million has already been incurred. A good deal relates to the external management contract with RMR.

Represents an adjustment to accrue $72,000 of estimated acquisition related costs that OPI expects to incur in connection with the Merger and the elimination of a $48,360 liability recorded by DHC related to its previous investment in RMR Inc., which DHC sold in 2019. The liability was being amortized over a 20 year period based on the terms of DHC’s management agreements with RMR, which will be terminated upon consummation of the Merger.

Source: OPI S-4

No surprise there. RMR will extract its pound of flesh regardless of where DHC goes. We saw a similar even when Global Net Lease ( GNL ) decided to merge with Necessary Retail REIT ( RTL ). Both are managed by the same manager.

Pursuant to the internalization agreement, upfront consideration to the External Manager will consist of $325 million of GNL stock and $50 million in cash.

Source: Seeking Alpha-GNL

2) The poor long term management by RMR is also something that we cannot disagree with. The stocks have underperformed their respective benchmarks by a huge amount and this stands true even after the recent DHC rally.

The underperformance versus Sabra Health Care REIT Inc. ( SBRA ) is particularly notable as DHC has more resilient medical office buildings vs SBRA which holds only senior housing and skilled nursing assets.

3) The low synergies were also virtually guaranteed. The two portfolios have little overlap and it is not like RMR would reduce the fee structure on the OPI side to actually create any synergies.

4) The final point is one that is likely to be the hardest for DHC shareholders to swallow. DHC's medical office buildings and senior housing properties are way more flexible than the single tenant buildings that OPI has. While the latter is producing better cash flow relative to asset value today, they also carry a greater risk over the next 5 years. Flat Footed adds more color on this.

In stark contrast to the senior housing market, the prospects for commercial office properties are bleak and will continue to darken as the market shifts towards work-from-home employment. Relative to other office REITs, OPI is even more negatively exposed, given its focus on single-tenant buildings, which leads to an inability to counter tenant downsizing and to tremendous tenant leverage in negotiating lease terms, tenant improvements and owner-funded capital expenditures. In its first quarter 2023 earnings release and call, OPI management acknowledged two troubling items. First, OPI failed to renew at least half of its leases due for renewal during the year to date and expects this trend to continue beyond 2023. Second, the rates for the mere 50% of leases that actually did renew declined by 19.7%.

Source: Seeking Alpha-Flat Footed LLC Letter

If you read our previous work on OPI as a standalone entity, this is precisely what we have been saying for the last 2 years.

Fair Value

Flat Footed valued DHC at over $9.00 a share based on the following calculations.

Seeking Alpha-Flat Footed LLC Letter

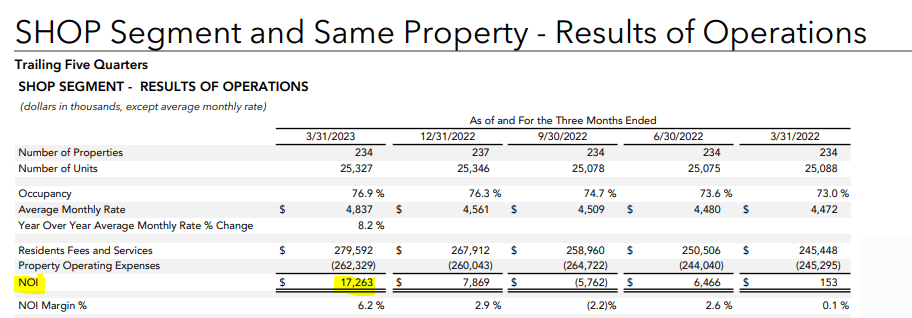

The good part about their calculations is that they have shown their assumptions. The bad part here is where exactly were they for the last 3 years before the announced merger? If any of this held true then surely they would have engaged with the board way before that time point. Even arguing from RMR's standpoint, if selling a few assets at those cap rates to deleverage would have been feasible, they might have done so in the last year at least. Instead they have had to get waivers from covenants to continue operating without a default. While we don't dispute those cap rates for the non-SHOP segments, we think the SHOP 14X EBITDA multiple comes off a little distorted. The SHOP segment was producing less than $70 million of net operating income annualized as of Q1-2023.

{kind=link}

So going from that to 2024 "EBITDA" of $210 million is where the biggest distortion lies between Flat Footed's valuation and the market perception. There is no chance in our opinion of selling this today at those multiples.

Verdict

If we value the SHOP segment at 12X Q1-2023 NOI (annualized) of $70 million, we get that segment valued at $840 million. That is a cool $2.1 billion lower than what is shown. Then the net asset value drops from $2,189.5 shown to $89.5 million or less than 40 cents a share. Of course we are not remotely claiming that our valuation is right, but using that expected $210 million 2024 EBITDA is a reach. We think the current rally in DHC should be sold. While the proxy fight has resulted in a tremendous rally, Flat Footed might also decide that they have "won" enough here and decide to exit. They own about $45 million of the equity based on last disclosure and current price but almost 4 times as much as that in DHC bonds. They may also shift their equity stake to the bond side and the stock could move back down.

The big issue here will be for OPI if the merger does not go through. The merger would help them at the expense of DHC and we believe they would be fighting for survival within 12 months. Currently while the stock price trajectories have diverged, the near term bonds maturing in 2024 have higher yield to maturity for DHC.

{kind=link}

Even more interestingly, DHC's 2031 bonds yield 8.5% while OPI's yield over 13%.

{kind=link}

So the best long bet in our opinion would be the DHC 2024 bonds which remains radically underpriced compared to where other bonds and the equity is trading.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Diversified Healthcare: Is It Actually Worth Over $9.00?